Florida Canyon Study Delivers $601M NPV, Powers Integra’s Growth Strategy

Integra Resources' Florida Canyon feasibility study delivers $601M NPV5, $800M free cash flow over 8 years, self-funding growth toward DeLamar and Nevada North.

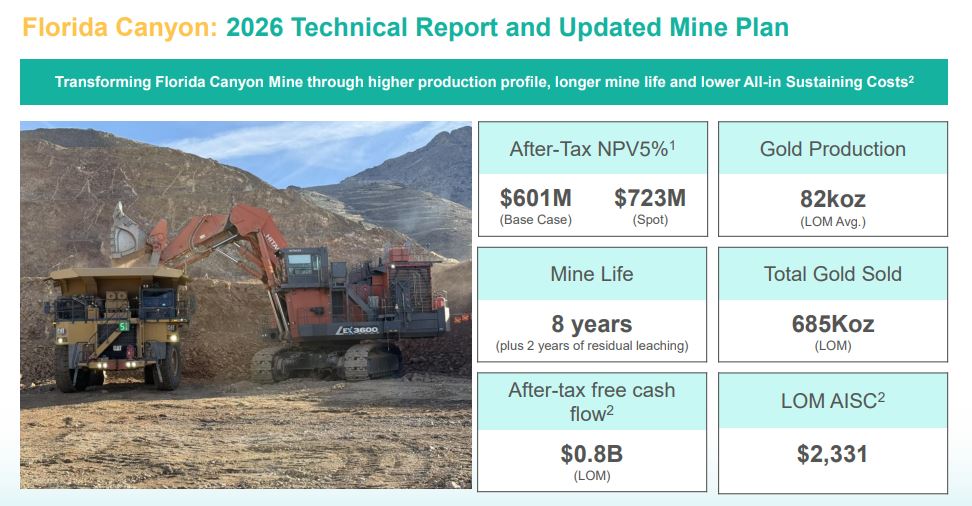

- Integra Resources' Florida Canyon feasibility study delivers an NPV5 of $601 million, an 8-year mine life, and approximately $800 million in after-tax free cash flow, with no upfront capital required.

- Reserves grew 78% and resources grew 128%, driven by 18 months of structural and lithological re-interpretation, infill drilling, steeper pit slope angles, mine sequencing changes, and increased crushing of ore.

- The next two quarters involve an intensive waste-stripping campaign to reach the higher-grade Main C pits, after which costs are expected to decline toward a life-of-mine average AISC of roughly $2,300 per ounce.

- Free cash flow from Florida Canyon is earmarked to sustain the operation, fund DeLamar's construction (targeted in roughly two years, partly debt-financed), and ultimately support development of the Nevada North project.

- A 42,500-metre exploration program is underway, focused on infill drilling between existing pits and, for the first time, on the historical Standard Mine resource south of the operation, last drilled 15 years ago.

Integra Resources, a New York Stock Exchange and TSX Venture-listed gold producer operating in the western United States, has released a feasibility study for its Florida Canyon mine in Nevada. President and CEO George Salamis discussed the results in an interview, outlining the project's economics, the operational changes expected over the coming year, and how the asset is intended to fund the company's broader growth pipeline. The study matters to investors because it formalises Florida Canyon's role as the financial backbone of Integra's strategy, providing the cash flow the company says it needs to advance its other development assets without relying heavily on external capital markets.

Florida Canyon's Cash Flow Engine

The feasibility study reports an after-tax net present value (at a 5% discount rate) of $601 million, an 8-year mine life, and a production profile that is expected to improve over time alongside declining costs. Salamis emphasised that the more significant figure for shareholders is the cumulative free cash flow the operation is expected to generate.

"The real story here, however, is the cash flow that this generates over the entire eight years, close to $800 million of after-tax free cash flow, which should be welcome news to our shareholders. Florida Canyon becomes the cash flow engine which funds everything else."

Importantly, the study assumes no upfront capital expenditure, since the mine is already built, permitted, and operating.

Rebuilding the Resource Model

The study reflects a 78% increase in reserves and a 128% increase in resources compared to prior estimates. Salamis attributed this partly to a higher gold price assumption, but also to an 18-month internal effort to better understand the ore body's geological controls. Historically, the deposit had been mined largely on the basis of grade shells.

"There's more to the story than just simply grade distribution. There's the controls that go with that grade distribution. There are the structural controls, there are the lithological controls, how those two interact."

Additional contributors included roughly 16,000 metres of drilling completed within the first year of ownership, geotechnical work that allowed for steeper pit slope angles (reducing the volume of non-revenue-generating waste rock), revised mine sequencing, and a decision to direct more ore through the crusher rather than placing it directly on the heap leach pad.

The Waste-Stripping Campaign Ahead

Over the next two quarters, the majority of mining and haulage at Florida Canyon will involve waste rock rather than ore, as the company works through material left in place by the previous owner. This stripping is intended to expose the higher-grade Main C pits, which Salamis described as having better grades, metallurgy, and mining conditions than areas currently being mined.

Capital spending during this period includes additional mining equipment, with a full replacement of the inherited haul truck fleet planned over the next two years, alongside adjustments to the crushing circuit.

Interview with George Salamis, CEO, Integra Resources

Funding the Growth Pipeline

Florida Canyon's free cash flow is intended to first sustain the operation itself, then build a treasury sufficient to fund construction of the DeLamar project, which the company hopes to begin in approximately two years. Salamis indicated that a debt component is expected to supplement that construction financing. Beyond DeLamar, the company is also advancing Nevada North, a project located 25 miles west of Florida Canyon.

Salamis suggested the two assets could eventually operate in parallel, with Florida Canyon's cash flow funding Nevada North's development in the interim, and the combined cash flow from DeLamar and Florida Canyon eventually supporting it directly. This structure is positioned as reducing the company's reliance on equity issuance, and therefore shareholder dilution, as it advances its growth pipeline.

Tightening Costs Through Better Recovery

Like other gold producers, Integra is currently facing elevated fuel and explosives costs, which are reflected in near-term all-in sustaining costs (AISC). Salamis expects costs to decline meaningfully once the stripping campaign is complete, with AISC averaging just over $2,300 per ounce across the mine life. He was clear that Florida Canyon's grade profile means it will not become a sub-$2,000-per-ounce producer.

On metallurgical recovery, the study reports a blended life-of-mine recovery rate of 57%, which combines lower recovery from run-of-mine ore (roughly 40s to low 50s percent) with higher recovery from crushed ore (low-to-mid 60s percent). The company is evaluating options to push more ore through the crusher, and potentially expand crushing capacity further, to improve the blended recovery rate over time.

Drilling Toward Credibility

A 42,500-metre exploration program is planned, with most drilling focused within the mine gate, including the ridges and saddles between existing pits that Salamis described as historically under-explored due to a piecemeal, pit-by-pit mining approach. The company is also drilling outside the mine gate for the first time, targeting the historical Standard Mine resource south of the current operation, which has not been drilled in roughly 15 years.

Salamis acknowledged that, despite the improved study results, the market retains a "show-me" attitude toward Florida Canyon given its history of under-investment under prior ownership. "Show us that you can actually do that... yes, we can drop costs, yes, we can raise production, yes, we can run this operation far more efficiently than anybody else has, and yeah, we're fully aware that we have to show our shareholders that," he said, pointing to 2027 through 2029 as the period in which the company expects to demonstrate sustained production in the 80,000- to 85,000-ounce range. He also noted that Integra's $65-66 million acquisition of DeLamar is now projected, per the study, to generate an approximate 11x return on that initial investment.

The Investment Thesis for Integra Resources

- A feasibility study supporting an NPV5 of $601 million and approximately $800 million in after-tax free cash flow over an 8-year mine life at Florida Canyon, with no upfront capital required.

- A self-funding operating model in which an already-built, permitted, and producing mine generates the cash flow needed to advance the company's growth pipeline without relying on major equity raises.

- Substantial reserve (78%) and resource (128%) growth following 18 months of geological re-interpretation, drilling, and engineering refinement, suggesting further upside as additional infill and extension drilling continues.

- A clearly sequenced capital allocation plan: sustain Florida Canyon first, build a treasury for DeLamar's construction (targeted in roughly two years, supplemented by debt), then fund Nevada North's development.

- Multiple sources of near-term reserve and resource growth still untested, including ridges and saddles between existing pits and the historical Standard Mine target, which is being drilled for the first time in 15 years.

- An identifiable cost-reduction pathway, with AISC expected to decline from current inflation-affected levels toward a life-of-mine average of roughly $2,300 per ounce once the current waste-stripping campaign concludes.

- A defined performance window (2027-2029) in which management expects to demonstrate sustained production in the 80,000- to 85,000-ounce range, providing investors a concrete timeline against which to measure execution.

Macro Thematic Analysis

Integra's update reflects two macro dynamics currently shaping the gold mining sector: persistently elevated input costs and a higher, more durable gold price environment. Fuel and explosives costs remain inflated industry-wide, pressuring near-term all-in sustaining costs across producers, not just Integra. At the same time, a stronger gold price has supported larger reserve and resource estimates and wider operating margins, allowing companies like Integra to fund growth internally rather than through dilutive equity raises. Salamis tied this directly to the company's strategy, noting:

"If we assume that the gold prices remain high for an extended period of time, there'll be lots of margin again to build up our treasury and our cash flow to pay for the other things going forward."

TL;DR

Integra Resources' Florida Canyon feasibility study delivers an NPV5 of $601 million and roughly $800 million in after-tax free cash flow over an 8-year mine life, with reserves up 78% and resources up 128%. The mine is designed to self-fund its own sustaining capital as well as the development of DeLamar and, eventually, Nevada North, reducing reliance on equity financing. Near-term costs remain elevated due to an active waste-stripping campaign and industry-wide inflation, but management expects AISC to decline toward roughly $2,300 per ounce over the life of mine. A 42,500-metre exploration program, including first-time drilling outside the mine gate, offers further potential resource growth.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed