Global Supply Chain Realignment Reshapes Rutile Investment Landscape

Supply chain realignment drives rutile investment shifts. Diversified projects in stable jurisdictions gain premium as China decoupling reshapes markets.

- Global deglobalization and US‑China decoupling are triggering structural realignments in critical minerals, redirecting trade flows and creating strategic sourcing opportunities beyond China and South Africa.

- Rutile markets face supply chain fragmentation, with emerging sources gaining prominence amid tariff pressures and ESG-driven sustainability mandates.

- High‑quality, low‑cost assets with diversified product exposure—such as Sovereign Metals’ Kasiya rutile‑graphite project in Malawi—stand out in this new paradigm.

- Robust project metrics (NPV, AISC, free‑dig soft ore, free cash flow) will be critical selection criteria for investors seeking de‑risked exposure.

- Investors should focus on companies delivering project milestones, financial optionality, and jurisdictional resilience, while monitoring macro signals such as tariff policy shifts and global capital flow volatility.

Structural Disruption in Global Commodity Supply Chains

The current realignment of global supply chains represents more than cyclical policy adjustments, it reflects a fundamental shift toward economic nationalism and strategic resource security. This transformation carries profound implications for critical minerals like rutile, where concentrated production and complex geopolitical dynamics have historically defined market structure.

Deglobalization & Decoupling Trends

Rising protectionism and US-China strategic decoupling are accelerating the reshoring of supply chains across multiple industries. The Biden administration's continuation of Trump-era trade policies, combined with new restrictions on technology transfers and critical mineral sourcing, signals a bipartisan commitment to reducing strategic dependencies. This shift extends beyond immediate trade disputes to encompass long-term industrial policy objectives, including domestic manufacturing capacity and supply chain resilience.

For commodity investors, these trends introduce both risk and opportunity. Trade flow volatility creates uncertainty in traditional sourcing patterns, while supply risk premiums emerge for materials sourced from geopolitically sensitive regions. Mining companies with assets in stable jurisdictions outside China's sphere of influence command increasing attention from institutional investors seeking exposure to this structural realignment.

Trade Policy as a Catalyst

US tariff policies, including proposed 60% tariffs on Chinese goods and 30% tariffs on South African imports, represent structural drivers rather than temporary trade measures. These policies, subject to delays and extensions based on political cycles, nonetheless establish a new baseline for international commerce in critical materials. The semiconductor export restrictions and rare earth mineral sourcing requirements further demonstrate the systematic nature of supply chain restructuring.

For mining investment decisions, these policies fundamentally alter risk-weighted valuations. Projects previously considered marginal due to higher costs relative to Chinese or South African alternatives now merit serious consideration. Sourcing flexibility becomes a key valuation metric, as companies with diversified geographical exposure can better navigate trade policy volatility. Risk weighting in financial models must now incorporate potential tariff scenarios and their impact on competitive positioning.

Market Impact on Rutile: Fragmentation, Benchmark Loss & Opportunity

Fastmarkets' decision to discontinue its cost, insurance, and freight (CIF) China rutile price assessment reflects broader challenges in maintaining transparent price discovery mechanisms. This benchmark served as a critical reference point for contract negotiations and financial modeling across the rutile value chain. Its discontinuation signals market fragmentation, where pricing becomes increasingly bilateral and opaque.

Small and mid-sized buyers face particular challenges in this environment, lacking the negotiating power of major integrated producers. Increased price volatility follows naturally from reduced benchmark transparency, complicating long-term contract structures and hedging strategies. For investors, benchmark erosion complicates forecasting accuracy and introduces additional uncertainty into valuation models, particularly for early-stage development projects.

Structural Supply Opportunities

Supply diversification away from traditional sources creates structural opportunities for alternative producers. Projects in jurisdictions like Malawi, Australia, Mexico, and Mozambique gain premium strategic value as buyers seek reliable, politically stable suppliers. This shift elevates the importance of fundamental project metrics including AISC, NPV calculations, and geological characteristics such as free-dig mineralization.

The premium for supply chain reliability extends beyond simple cost comparisons. Buyers increasingly factor in operational continuity, regulatory stability, and ESG compliance when evaluating sourcing decisions. Projects offering transparent permitting processes, established mining codes, and proven infrastructure access command disproportionate attention to their resource size or grade characteristics.

Macro Drivers Re-Weighting Investment Risk in Rutile Mining

Low AISC remains fundamental, but investors increasingly scrutinize the sustainability and reliability of cost projections. Capital expenditure discipline becomes critical as financing costs rise and project approval processes face greater scrutiny. Short permitting windows and established regulatory frameworks provide competitive advantages that translate into measurable enterprise value per ounce (EV/oz) premiums.

Risk-adjusted internal rate of return (IRR) calculations must now incorporate supply chain resilience factors. Projects with proven infrastructure access, stable labor markets, and predictable regulatory environments justify higher valuations despite potentially higher absolute costs. The traditional focus on grade and tonnage expands to include operational reliability and political risk assessment.

ESG & Supply Chain Resilience Premiums

Environmental, social, and governance (ESG) considerations increasingly drive sourcing decisions across industrial markets. Buyers prioritize suppliers from politically stable, environmentally compliant jurisdictions, creating measurable premiums for qualifying projects. This trend extends beyond regulatory compliance to encompass broader sustainability narratives, including carbon footprint reduction and social license maintenance.

Diversified, traceable supply chains command premium valuations as industrial buyers seek transparency in their sourcing practices. Low-carbon production methods, including free-dig mineralization that reduces energy-intensive processing requirements, align with corporate sustainability commitments. These factors translate into tangible commercial advantages, including preferential contract terms and long-term offtake commitments.

Sovereign Metals (Kasiya) as a Case Study in Macro-Aligned Execution

Sovereign Metals' Kasiya project in Malawi exemplifies how mining companies can position themselves to benefit from supply chain realignment. Rather than viewing the project in isolation, its strategic attributes align directly with evolving market requirements for diversified, reliable rutile supply.

Asset Class: Tier-1 Rutile + Graphite in "Friendly" Jurisdiction

The Kasiya deposit contains 17.9 million tonnes of rutile resources alongside 24.4 million tonnes of graphite, representing world-class scale in both commodities. This resource base positions Sovereign Metals as a potential major supplier in a restructuring supply chain where scale and self-contained diversification provide strategic advantages.

The deposit's geological characteristics, free-dig, weathered ore hosted in soft, friable saprolite, offer significant operational advantages. Lower energy requirements for processing translate directly into improved AISC positioning, while the soft ore body eliminates the need for energy-intensive drilling and blasting operations typical of hard rock mining.

Chairman Ben Stokovich emphasizes the project's unique position in the rutile market:

"The Kasiya project is a primary rutile deposit and the graphite will be produced as a byproduct. In fact, it's the only known deposit where graphite is a byproduct."

Project Economics & Free Cash Flow Resilience

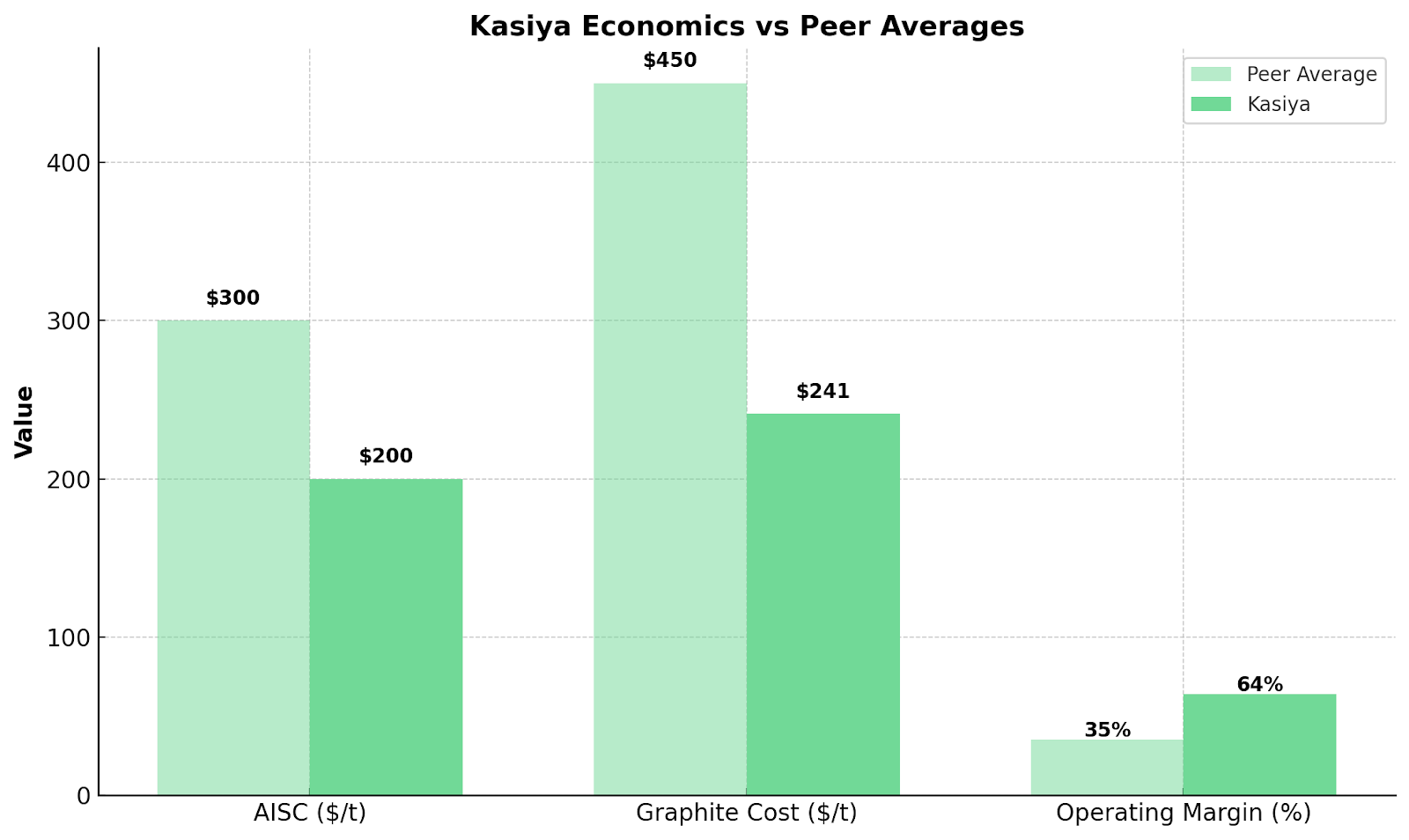

Sovereign Metals' optimized pre-feasibility study demonstrates exceptional economics with a pre-tax NPV exceeding US$2.3 billion and annual average earnings before interest, taxes, depreciation, and amortization (EBITDA) of over US$400 million. The project's 64% operating margin provides substantial buffer against commodity price volatility and cost inflation pressures.

The graphite byproduct economics prove particularly compelling, with incremental production costs of only US$241 per tonne. This cost position places Kasiya at the bottom of the global graphite cost curve, enabling profitable operations even in challenging market conditions. The byproduct structure provides natural diversification across two distinct commodity markets, reducing single-commodity exposure risk.

Stokovich notes the strategic significance of this cost positioning:

"Where do we plot on the standard industry graphite cost curve? We're at the very bottom where other projects can't make money in the current market. We'd be selling graphite at a 50% operating margin even if we only sold into the lower value battery graphite market."

Project Catalysts & Investor Timelines Under the Restructuring Lens

Development milestones carry heightened significance in the current environment, where early-stage validation and regulatory clarity directly impact risk premiums and enterprise valuations.

Technical De-risking & DFS Timeline

Sovereign Metals completed pilot mining operations in 2024, providing substantial empirical data to inform project design and validate pre-feasibility assumptions. The pilot program extracted 170,000 cubic meters of material across a 10-hectare site, completing the entire program within six months while subsequently rehabilitating the land for agricultural use.

The definitive feasibility study (DFS), targeted for completion in Q4 2025, represents a critical inflection point for investor confidence. Early-stage technical validation reduces risk premiums in volatile markets, improving EV/oz valuations relative to purely conceptual projects. The combination of pilot mining results and ongoing DFS work provides unusual visibility into project risks and operational parameters.

Strategic Backing & Capital Optionality

Rio Tinto's 19.9% equity stake and technical collaboration significantly enhances the project's strategic profile. The major's A$60 million investment since mid-2023 validates the technical potential while providing access to world-class technical expertise and operational experience. A joint Sovereign-Rio technical committee now oversees project development, ensuring alignment with industry best practices.

This institutional backing addresses multiple investor concerns simultaneously. Geopolitical risk perception improves through association with a established major, while access to network capital reduces financing uncertainty. The strategic partnership also provides operational expertise and potential downstream market access, critical factors in developing large-scale mineral projects in emerging markets.

Monitoring Macro Indicators: What Investors Should Watch

US tariff policy evolution, trade agreement negotiations, and Chinese export regulations require continuous monitoring. Policy announcements often precede implementation by months, providing positioning opportunities for prepared investors. Changes in tariff structures or trade agreement terms directly impact competitive dynamics and should be incorporated into NPV sensitivity analyses.

Investment strategies must account for policy uncertainty through scenario analysis and risk weighting. Projects with natural hedges against policy changes, through geographical diversification or cost advantages, deserve premium valuations in uncertain policy environments.

Price Trends & Benchmark Reconstruction

Titanium dioxide (TiO₂) price movements provide proxy indicators for rutile demand trends, while efforts to establish new market benchmarks signal evolving price discovery mechanisms. Industrial buyers' willingness to accept alternative pricing structures indicates market adaptation to fragmented benchmarks.

Investors should adjust price decks, off-take models, and margin assumptions based on emerging pricing trends. The transition period creates both opportunities and risks, requiring active monitoring and model updates as new market structures emerge.

Company Milestones & Newsflow

Sovereign Metals' DFS publication, permitting updates, and commercial agreements serve as sentiment catalysts in the current environment. Progress on offtake negotiations, financing arrangements, or joint venture expansions provides early indicators of commercial viability and market acceptance.

Regular milestone achievement demonstrates execution capability, reducing perceived development risk and supporting premium valuations. Investors should weight management track records and milestone delivery against broader market developments when assessing investment timing.

The Investment Thesis for Rutile in a Realigned World

The supply chain realignment and rutile market dynamics create a compelling investment framework for qualified projects and management teams.

- Supply chain resilience premium: Projects based in stable, non-China jurisdictions garner structural value uplift as industrial buyers prioritize sourcing security over absolute cost minimization, exemplified by Sovereign Metals' Malawi location and Rio Tinto partnership.

- Cash flow robustness amid volatility: High NPV, low-cost, graphite-diversified operations offer margin protection against commodity price fluctuations while providing natural hedge through byproduct revenue streams.

- Execution transparency lowers risk premium: Completed pilot mining programs and clear DFS timelines enhance project visibility and investor confidence, reducing uncertainty discounts applied to development-stage assets.

- Strategic backing amplifies scale: Major mining company investment reduces capital risk and validates technical potential while providing access to operational expertise and downstream market relationships.

- Optionality across commodities: Graphite byproduct revenue hedges against rutile-specific demand swings and adds revenue diversification, particularly valuable given evolving battery material supply chains and refractory market dynamics.

Strategic Positioning in a Fragmenting Supply Chain

Global supply chain realignment represents a structural backdrop reshaping commodity markets rather than a temporary policy shock. The rutile market exemplifies how deglobalization trends create both challenges and opportunities, with traditional sourcing patterns giving way to diversified supply chains prioritizing reliability over cost optimization.

Investors should prioritize projects combining jurisdictional stability, financial optionality, and execution certainty when evaluating rutile exposure. Sovereign Metals' Kasiya project exemplifies this new investment model, offering strategic alignment with supply chain realignment trends while maintaining the fundamental project economics necessary for long-term success. Macro themes with project-specific advantages creates compelling investment opportunities for institutio

Analyst's Notes

Subscribe to Our Channel

Stay Informed