Gold's Safe-Haven Rally Produced Spillover Demand in Silver

Gold's safe-haven rally is pushing capital into silver amid a 67Moz supply deficit, rising investment demand, and expanding industrial applications.

- As investors sought additional precious-metal exposure following gold's surge to record levels, silver attracted both institutional and retail capital, pushing prices above US$100 per ounce in early 2025 before retracing toward the US$80 range.

- The global silver market is projected to enter its sixth consecutive year of supply deficit in 2026, with an estimated shortfall of 67 million ounces, forcing reliance on finite above-ground inventories.

- Physical investment demand is rising sharply as silver investment volumes are forecast to increase 20% in 2026 to approximately 227 million ounces, the highest level in three years, driven by geopolitical uncertainty and tightening physical liquidity in major trading hubs.

- Industrial applications are expanding silver's long-term demand base. Artificial intelligence infrastructure, electric vehicles, and advanced battery technologies are reinforcing demand in ways not fully captured by earlier market models.

- Whether silver's current repricing represents a durable structural shift or a volatility-driven satellite trade anchored to gold will depend on the persistence of supply constraints and the pace of industrial demand growth.

Silver's Role in the Precious-Metals Hierarchy

Safe-haven demand in precious metals has historically concentrated in gold, which benefits most directly from monetary uncertainty, geopolitical instability, and concerns about central bank policy credibility. Silver occupies a distinct position within the same asset class, functioning simultaneously as a monetary hedge and an industrial input metal. This dual identity means that when gold attracts defensive capital, silver frequently follows, but with higher sensitivity to incremental flows given the relative size of its market.

In early 2025, gold's surge to record levels drew renewed investor attention toward silver, which crossed the US$100 per ounce threshold before retracing toward the US$80 range. The gold-to-silver ratio, a widely tracked relative valuation measure, compressed below 50 for the first time since 2012. Historically, compressions of this ratio have coincided with periods when silver begins to outperform gold, as capital rotates deeper into the precious-metals complex in search of higher-beta exposure.

Silver's relatively small market size amplifies these dynamics. Compared with gold's multi-trillion-dollar investable market, silver's available supply is substantially smaller, meaning incremental capital flows can produce disproportionate price movements in both directions. For institutional portfolio managers, this positions silver as a higher-beta complement to gold within a broader precious-metals allocation, rather than a substitute for it.

Supply Conditions & Physical Market Dynamics

Silver's price sensitivity is further shaped by persistent imbalances between production capacity and total demand. The market is projected to record its sixth consecutive annual supply deficit in 2026, with an estimated shortfall of 67 million ounces. A deficit occurs when total demand, comprising industrial fabrication, physical investment, and jewelry - exceeds newly mined and recycled supply, requiring the market to draw on existing above-ground inventories, including London vault holdings and exchange-held stocks.

Global silver supply is forecast to grow only 1.5% in 2026, driven primarily by incremental production increases in Mexico and a 7% rise in recycling activity as higher prices incentivize holders to monetize existing inventory. New mine supply remains structurally constrained. Approximately 70% of global silver production is extracted as a by-product of base-metal mining, primarily zinc, lead, and copper, meaning supply responses to rising silver prices are governed more by the economics of primary metals than by silver prices alone.

Bringing a new underground silver mine into production typically requires seven or more years from discovery through permitting, feasibility, and construction. Even when prices justify new investment, supply responses take years to materialize. The interim reliance on above-ground inventories to bridge the annual deficit is an arrangement that cannot persist indefinitely - and sustained drawdowns of those reserves could themselves become a price-supportive signal.

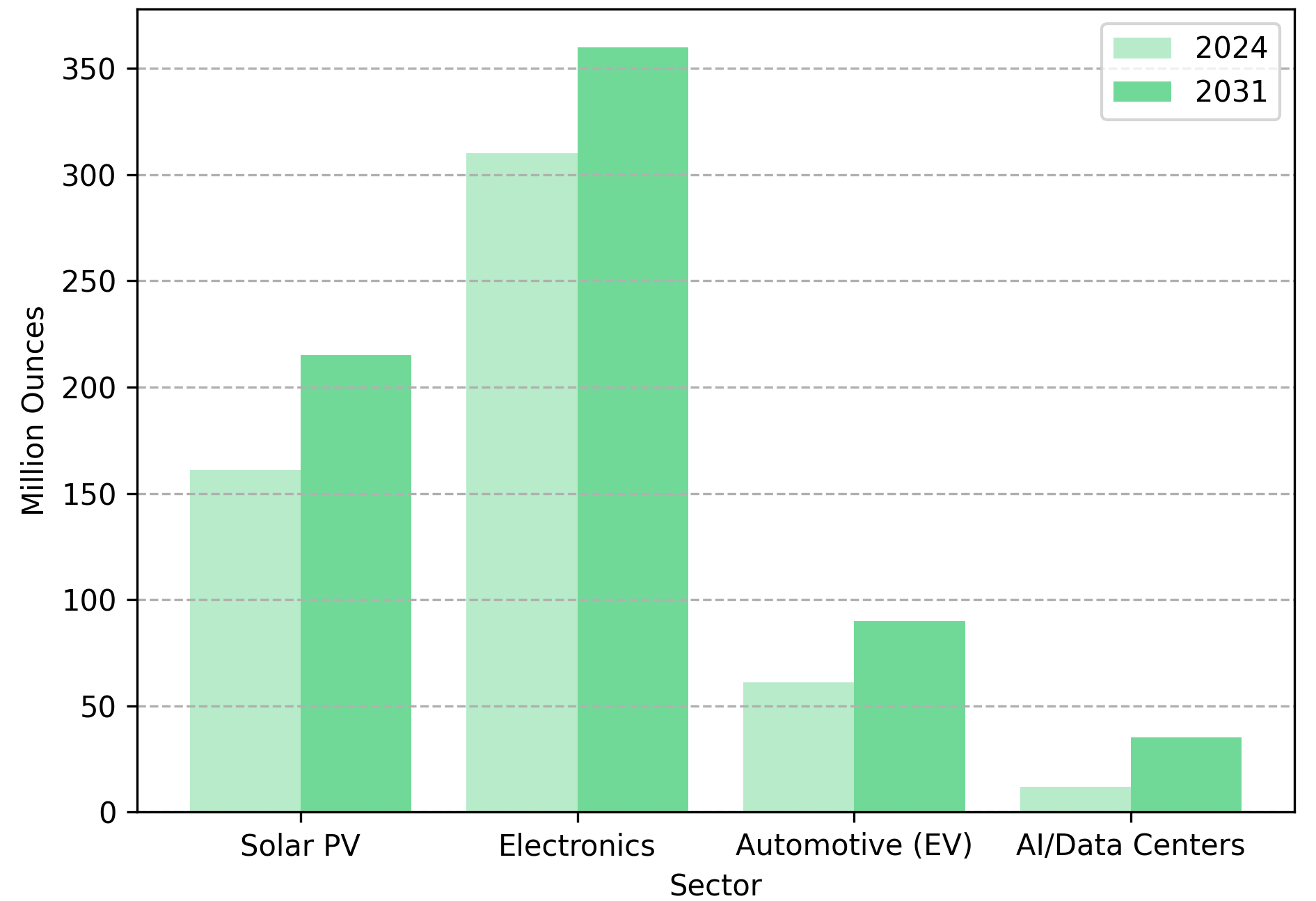

Industrial Demand Across Technology Sectors

While investment flows drive near-term price cycles, silver's long-term demand profile is increasingly shaped by technology applications. Silver's electrical conductivity, among the highest of any pure metal, makes it the material of choice across advanced manufacturing sectors where performance tolerances leave limited room for substitution.

The build-out of artificial intelligence infrastructure has emerged as one of the more significant new demand drivers. Silver is used in electrical contacts, circuit boards, and thermal management systems within large-scale data centers, where managing heat generated by high-density processors is a critical operational challenge. As AI processing requirements continue to scale, per-unit silver intensity in these systems is likely to increase rather than decline.

The automotive sector represents a parallel and well-documented demand driver. Electric vehicles require significantly more silver per unit than internal combustion engine vehicles, due to silver's use in power electronics, battery management systems, and charging infrastructure. Industry forecasts suggest automotive silver demand could grow at a compound annual rate of 3.4% between 2025 and 2031, with electric vehicles projected to become the dominant source of automotive silver consumption by 2027, based on current adoption trajectories. Research into ultra-thin silver coatings for ceramic battery electrolytes represents an additional long-term demand pathway, though these applications remain at early stages of development as of 2025.

Project Economics, Cost Structures & Operational Positioning

In a supply-constrained market with a multi-year development lag, where a company sits in its stage of development determines how directly it captures the current price environment, and how much of its value depends on conditions that have not yet materialized.

Americas Gold & Silver is a silver producer operating the Galena Complex in Idaho and the Cosalá operations in Mexico. The company's EC120 mine is projected to operate with cash costs near US$9.60 per ounce and AISC of approximately US$10.80 per ounce, based on projected parameters from the company's Pre-Feasibility Study filed in June 2019. In February 2026, Americas entered a formal joint venture agreement with US Antimony (USAC), structured at 51% Americas and 49% USAC, targeting the construction of a leaching facility in Idaho that would extract antimony from the company's existing concentrate stream. The refining infrastructure is targeted for completion within 18 months.

Paul Huet, Chief Executive Officer of Americas Gold & Silver, outlined the company's near-term development and cash flow priorities:

"We just bought Crescent Mine, we're going to have a bunch of drills turning. We're going to be very focused at generating free cash flow from our operations in both the US and Mexico."

The Crescent Mine acquisition closed on November 13, 2025, for US$65 million in cash and shares.

Project Development Economics

At the development stage, Vizsla Silver is advancing the Panuco district in Sinaloa, Mexico. As of the feasibility study with an effective date of November 4, 2025, the district holds proven and probable reserves of 170 million ounces of silver equivalent—comprising 123 Moz at Kopala and 47 Moz at Napoleon and La Luisa. The study outlined a post-tax NPV of US$1.802 billion at a 5% discount rate and an IRR of 111.1%, based on base-case metal prices of US$35.50 per ounce for silver and US$3,100 per ounce for gold, with projected AISC near US$10.61 per ounce silver equivalent. The company is targeting a construction decision in H2 2026 and initial production in H2 2027, subject to permitting, financing, and board approval.

Jesus Velador, Vice President of Exploration at Vizsla Silver, described the scale of the company's most recent resource update, which for the first time established a measured resource in the high-grade core of the Panuco district:

"There was a substantial increase of 43% in the measured and indicated category, and for the first time we put out a measured resource in the core of the high-grade central portion of Kopala, where we are going to have our initial production years."

Exploration & Alternative Development Models

GR Silver Mining holds 134 million ounces of silver-equivalent resources in Mexico's Sinaloa region, based on its 2023 NI 43-101 Mineral Resource Estimate, with a major resource update targeted for H2 2026 following more than 20,000 metres of step-out drilling conducted in 2025. Daniel Shea, Vice President of Corporate Development, quantified the company's capital efficiency in resource development:

"We have 134 million ounces of silver equivalent that are growing at a very efficient rate. Our discovery cost per ounce of silver is 17 cents, for every dollar we put in the ground, we get about five ounces of silver out of that."

This figure is a company-calculated metric based on drilling expenditure relative to ounces defined and should be understood in that context.

An alternative operational model is being advanced by Cerro de Pasco Resources, which is developing a tailings reprocessing project in Peru. The project's concentrate contains gallium at 53.2 grams per tonne and indium at 19.9 grams per tonne, with internal metallurgical studies assuming overall metal recoveries of 40% to 70%, though commercial recoverability at scale remains subject to further assessment. The company received a Supreme Resolution granting a land easement in May 2024, and the project is structured to generate local tax revenue and support environmental remediation of acid water contamination in the surrounding area.

Constraints & Risks Within the Silver Market

Despite the constructive supply-demand backdrop, several factors could interrupt the current pricing trajectory. Solar photovoltaic manufacturers have systematically reduced the amount of silver used per solar cell through thrifting, optimizing cell architecture to achieve equivalent efficiency with less metal. If thrifting accelerates faster than new solar installations expand, industrial demand from this sector could decline even as global renewable energy capacity grows. This is not a theoretical risk: silver content per cell has declined materially over the past decade, and further reductions are technically feasible.

Physical silver's reliance on above-ground inventories to bridge the annual supply deficit introduces a separate consideration. Large-scale liquidation of stored bullion, whether from institutional holders, exchange inventory drawdowns, or government sales - could temporarily suppress prices even when the underlying supply-demand balance remains in deficit. Silver's historical price volatility, which significantly exceeds that of gold, means speculative positioning can amplify both rallies and corrections in ways disconnected from physical market conditions.

The Investment Thesis for Silver

- Safe-haven spillover from gold provides an established capital rotation pathway, as investors seeking diversification within precious metals have historically directed incremental allocations toward silver when gold's rally becomes extended or crowded.

- Six consecutive years of projected supply deficits underscore the structural difficulty of bringing new silver production online, with above-ground inventories serving as a partial and finite buffer that may itself become a price-supportive signal as it depletes.

- Rising technology demand from artificial intelligence infrastructure, electric vehicle adoption, and advanced battery research is expanding silver's industrial footprint, diversifying the demand base beyond traditional monetary and jewelry applications in ways likely to persist across economic cycles.

- Producers with AISC profiles in the low double-digit range per ounce and high-grade deposit configurations may generate significant operating margin expansion during periods of sustained price strength.

- Development timelines of seven or more years reinforce supply constraints and create a structural lag that supports prices even after market sentiment begins to normalize, as committed production capacity cannot reach market quickly even when economics justify the investment.

- Exploration-stage companies with low discovery cost profiles and district-scale resource bases offer optionality to resource growth that has historically attracted acquisition interest from larger producers seeking reserve replacement at a cost advantage relative to greenfield development.

The central question is whether the current repricing represents a durable structural shift or a volatility-driven rally anchored to gold sentiment. The answer will depend on whether physical inventory drawdowns continue, how quickly demand from artificial intelligence and electric vehicle adoption scales relative to supply growth, and whether sustained higher prices are sufficient to accelerate new project development. The conditions underpinning silver's current market position are more substantive than safe-haven flows alone, and companies capable of delivering low-cost production into a supply-constrained market may attract institutional attention as project economics become more visible.

TL;DR

Gold's record-level rally in early 2025 compressed the gold-to-silver ratio below 50 for the first time since 2012, triggering capital rotation into silver as investors sought higher-beta precious-metal exposure. Silver crossed US$100 per ounce before retracing toward US$80, while the physical market moved toward its sixth consecutive annual supply deficit of 67 million ounces. Supply growth remains structurally constrained by the dominance of by-product mining and development timelines exceeding seven years. Industrial demand from electric vehicles, artificial intelligence infrastructure, and advanced battery research is reinforcing the long-term demand base. Whether the current repricing evolves into a sustained bull cycle depends on the persistence of inventory drawdowns and the pace of technology-driven demand growth.

FAQs (AI-Generated)

Silver occupies a dual role as both a monetary asset and an industrial input metal. When gold attracts defensive capital during periods of geopolitical or monetary uncertainty, investors seeking higher-beta exposure within the same asset class frequently rotate into silver. Silver's significantly smaller investable market means that incremental capital flows produce disproportionate price movements compared with gold, making it a natural spillover destination once gold's rally becomes extended.

Approximately 70% of global silver production is extracted as a by-product of zinc, lead, and copper mining, meaning supply does not respond directly to silver price signals. New primary silver mines require seven or more years from discovery to production. These constraints mean that even sustained high prices cannot quickly bring new supply to market, forcing the industry to draw on finite above-ground inventories to bridge the annual gap between demand and newly mined supply.

Silver's electrical conductivity makes it difficult to substitute in high-performance manufacturing applications. Electric vehicles require significantly more silver per unit than combustion-engine vehicles, AI data centers rely on silver in thermal management and circuit applications, and next-generation battery research is exploring silver coatings to extend cell life. These applications are expanding the demand base beyond traditional monetary and jewelry uses, providing a structural demand floor that is less correlated with investor sentiment cycles.

The gold-to-silver ratio measures how many ounces of silver are required to purchase one ounce of gold. When the ratio compresses—meaning silver is rising faster than gold—it has historically signaled a period of capital rotation deeper into the precious-metals complex. The ratio fell below 50 in early 2025 for the first time since 2012, a level that institutional investors track as an indicator of relative value and momentum within the precious-metals allocation.

Three primary risks apply. First, solar thrifting—the ongoing reduction of silver content per photovoltaic cell—could reduce industrial demand even as renewable energy deployment expands. Second, large-scale liquidation of above-ground bullion stocks could temporarily suppress prices regardless of the underlying supply-demand balance. Third, silver's inherent price volatility significantly exceeds that of gold, meaning speculative positioning can amplify corrections as sharply as it amplifies rallies, creating meaningful short-term risk for investors with lower volatility tolerance.

Analyst's Notes

Subscribe to Our Channel

Stay Informed