86% Refining Concentration: Industrial and Sovereign Capital are Backing Ex-China Battery-Metal Supply

Battery-metal refining concentration reached 86% in 2024, driving strategic capital toward ex-China supply projects as governments tighten control.

- The International Energy Agency reports that the top three refining nations controlled 86% of battery-metal refining capacity in 2024, up from around 82% in 2020, increasing the risk that supply availability rather than commodity prices determines project economics.

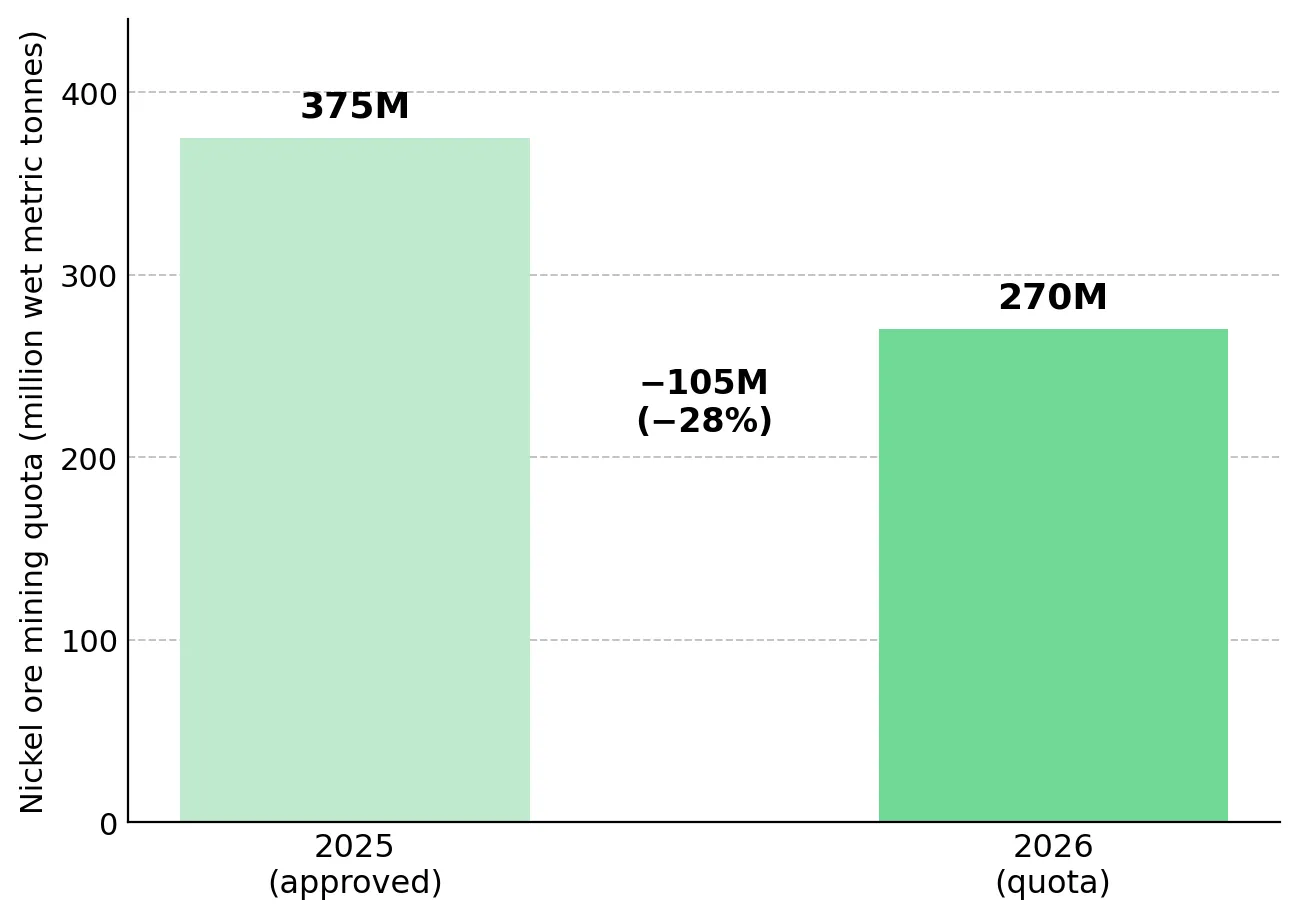

- Democratic Republic of Congo cobalt export quotas, Indonesia's nickel ore-quota cut to roughly 270 million wet metric tonnes, and Zimbabwe's lithium concentrate export ban have increased producer control over battery-metal supply and pricing.

- With the United States Federal Reserve holding its policy rate at 3.50% to 3.75% and inflation near 3.8%, higher financing costs favor projects with committed funding and increase financing risk for unfinanced developers.

- Strategic and sovereign investors, including Rio Tinto, Samsung SDI, the United States Development Finance Corporation, and Export Development Canada, are providing capital that helps advance ex-China supply projects.

- Most companies discussed are pre-production developers whose valuations rely on feasibility studies rather than operating cash flow, exposing investors to financing, permitting, and dilution risk.

Refining Concentration Reaches 86% & Governments Tighten Battery-Metal Supply

In 2026, battery-metals supply is increasingly shaped by who controls refining capacity rather than by individual metal prices. The 2021-2022 oversupply that drove lithium prices down more than 80% from their peak has been followed by export controls and supply restrictions across key producer nations. According to the International Energy Agency, the average market share of the top three refining nations across copper, lithium, nickel, cobalt, graphite, and rare earths rose to 86% in 2024. The concentration risk sits in refining rather than mining. Ore deposits are widely distributed, but processing and separation capacity remains concentrated in a small number of countries and is costly to replicate. As a result, battery-metal supply risk depends more on access to processing capacity than on access to ore deposits.

Producer nations are restricting exports and raw-material supply. The Democratic Republic of Congo, which supplies roughly 70% of mined cobalt, has capped exports at 96,600 tonnes per year for 2026 and 2027 against global output of around 220,000 tonnes in 2024. Indonesia cut its 2026 nickel ore quota to roughly 270 million wet metric tonnes from 375 million, while Zimbabwe banned raw lithium concentrate exports in February 2026. These policies restrict supply and increase government influence over battery-metal markets.

China also dominates rare-earth processing, the most concentrated segment of the battery-metals supply chain. China controls close to 90% of global rare-earth processing and roughly 95% of heavy rare-earth output. The suspension of China's expanded October 2025 export controls is scheduled to expire around November 2026, leaving future supply restrictions a continuing risk. This concentration increases the value of non-Chinese processing and supply assets to governments and industrial buyers seeking alternative sources.

Higher Interest Rates Increase Financing Risk for New Battery-Metal Supply

Higher interest rates are increasing the cost of developing new supply. The United States Federal Reserve is holding its policy rate at 3.50% to 3.75%, while inflation near 3.8% and a Middle East energy shock have increased energy, freight, and reagent costs across mining and refining. Higher interest rates reduce project economics and make financing more difficult for new developments.

Higher discount rates reduce NPV most for long-dated, capital-intensive projects because more of their cash flow arrives in later years. Nickel sulphide projects and rare-earth separation facilities are particularly sensitive to higher interest rates, despite being important sources of ex-China supply.

Projects with access to non-dilutive or strategic capital can continue advancing despite higher financing costs, while projects reliant on equity issuance face greater dilution risk. In a higher-rate environment, funding access can be as important to project advancement as resource quality.

Strategic Investors & Government Lenders Back Ex-China Supply Projects

When public-market valuations lag, strategic investors can indicate asset value through equity investments and financing commitments. Strategic equity investments and offtake agreements provide financing and commercial support that can reduce project-development risk. For many ex-China developers, strategic investors and offtake partners are becoming important sources of project funding.

Rio Tinto & Samsung SDI Back Ex-China Battery-Metal Supply

Sovereign Metals' Kasiya rutile-graphite project in Malawi has attracted investment from a major mining company. Rio Tinto holds an 18.5% equity stake and a production marketing option, while Kasiya's definitive feasibility study reports a pre-tax NPV of US$2.2 billion at an 8% discount rate. Recent test work identified a potential heavy rare-earth by-product stream that could provide additional future value beyond the project's current feasibility study.

Canada Nickel illustrates how battery manufacturers are securing future nickel supply through strategic investments. Samsung SDI holds a US$100 million acquisition option implying a project valuation of roughly US$1 billion, alongside nickel offtake rights totaling 30%. Front-end engineering reported an NPV of US$2.8 billion at an 8% discount rate, an IRR of 17.6%, and a life-of-mine net C1 cash cost of US$0.39 per pound.

Mark Selby, Chief Executive Officer of Canada Nickel, describes why battery manufacturers are seeking non-Indonesian nickel supply before 2030:

"Samsung remains equally keen. We're really now one of the only projects that can come online before 2030, and they're keen to have that non-Indonesian offtake in place."

Government Balance Sheets as the Marginal Lender

Government-backed financing is also supporting project development. Canada Nickel's US$2.5 billion funding plan targets 60% debt and 40% equity, supported by approximately US$600 million in government investment tax credits and a US$500 million letter of intent from Export Development Canada as Mandated Lead Arranger, reducing reliance on equity financing.

Lifezone Metals combines recycling revenue with nickel-project development. Its United States platinum-group-metals recycling business generated approximately US$1.2 million of external revenue in the first quarter after producing its first platinum, palladium, and rhodium. The Kabanga nickel project has completed United States Development Finance Corporation due diligence, while two United States Department of Energy applications seek a combined US$41.5 million for the recycling business.

Ingo Hofmaier, Chief Financial Officer of Lifezone Metals, describes how Indonesian supply growth is increasing concentration in the global nickel market:

"Nickel is a massive market, but it is very, very concentrated. If the development continues in Indonesia, you will have 75 to 80 percent."

Low-Cost Assets Gain Advantage as Battery-Metal Costs Rise

In a market shaped by supply controls, lower-cost producers are better positioned to withstand price declines and input-cost increases. Ore type affects processing costs because sulphide and oxide deposits require different processing routes and reagent inputs. Lifezone Metals reports a Kabanga AISC of US$3.36 per pound, while the deposit's roughly 30% sulphur content allows on-site acid generation and reduces exposure to rising sulphuric-acid costs. Canada Nickel reports a net C1 cost of US$0.39 per pound, supported by scale and concentrate quality.

Sovereign Metals' by-product structure lowers graphite production costs. Because Kasiya recovers graphite from a rutile-focused processing flow sheet, graphite production requires limited additional processing cost.

Ben Stoikovich, Chairman of Sovereign Metals, explains how Kasiya's by-product graphite could rank among the industry's lowest-cost sources of supply:

"Our incremental cost to produce a tonne of graphite as a by-product from the Kasiya project will only be 241 US dollars per tonne, right at the bottom end of the real cost curve."

Integrated Processing Helps Energy Fuels Compete with Chinese Supply Chains

Energy Fuels, the one producer among these names, provides the contrast between realised and modelled economics. As the only fully licensed conventional uranium mill operator in the United States, it generated 35.7 million US dollars of uranium revenue in the first quarter from 510,000 pounds sold at 70.04 US dollars per pound, with finished inventory cost near 36 US dollars per pound and Pinyon Plain all-in costs of 23 to 30 US dollars per pound.

Mark Chalmers, Chief Executive Officer of Energy Fuels, explains why processing integration remains important:

"To really compete with China you have to have all those steps; you can't be missing a step in the middle of it. We've been very focused on the integration at least through alloys."

Key Risks to the Battery-Metal Supply Concentration Thesis

Financing remains the main near-term risk for several developers. Lifezone Metals held roughly US$15.3 million in cash at the end of the first quarter against Kabanga capital costs of approximately US$950 million, rising to as much as US$1.2 billion, requiring project financing and strategic investment. Canada Nickel's roughly US$2 billion initial capital requirement remains unfinanced, and the Samsung SDI option has not yet been exercised.

A second risk is that project studies may not translate into operating results. The NPV and IRR figures cited for Sovereign Metals, Canada Nickel, and Lifezone's Kabanga are modelled estimates rather than operating cash flow and depend on resource assumptions and a Final Investment Decision that has not yet been taken. Permitting and jurisdictional risks remain important, as Sovereign's monazite requires radioactive-material handling, Lifezone continues tax and framework negotiations in Tanzania, and Energy Fuels depends on feedstock from Madagascar, Brazil, and Australia.

The supply-concentration thesis depends on continued geopolitical and trade tensions. A meaningful United States-China de-escalation when the export-control suspension expires in November 2026 could reduce the valuation premium for ex-China supply assets. Elevated prices could also reduce demand, while nickel remains in surplus. Development-stage mining equities are high-risk, often illiquid, and commonly subject to dilution.

The Investment Thesis for Battery & Critical Metals

- The top three refining nations controlled 86% of battery-metal refining capacity in 2024, increasing the value of diversified ex-China supply projects.

- Major miners, battery manufacturers, and government finance institutions are providing capital that supports project funding and development before full public-market recognition.

- Lower-cost producers are better positioned to withstand commodity-price declines and rising input costs.

- Higher interest rates favor projects with access to non-dilutive or strategic funding, while projects reliant on equity issuance face greater dilution risk.

- Producers with operating cash flow generally carry lower execution and financing risk than developers and explorers whose returns remain study-based.

- Permitting decisions, acquisition closings, and Final Investment Decisions can reduce project uncertainty and influence company valuations.

Battery-metals investment returns are increasingly influenced by supply control rather than commodity prices alone. Governments, industrial buyers, and strategic investors are funding alternative supply chains outside concentrated refining markets. The International Energy Agency's reported 86% refining concentration, combined with export controls across cobalt, nickel, and lithium, has increased investment in diversified supply projects through equity investments, offtake agreements, and government-backed financing. Investment outcomes will depend on project quality as well as commodity prices. Projects with strategic funding, competitive costs, and permitting progress are best positioned to advance. In a concentrated market, supply security is attracting capital from governments, industrial buyers, and strategic investors.

TL;DR

The battery-metals investment case is shifting from commodity prices to supply control. The top three refining nations controlled 86% of battery-metal refining capacity in 2024, while export restrictions in the Democratic Republic of Congo, Indonesia, and Zimbabwe have increased government influence over supply. Higher interest rates are raising financing risk for new projects, making strategic funding increasingly important. Companies attracting support from Rio Tinto, Samsung SDI, Export Development Canada, and the United States Development Finance Corporation are better positioned to advance ex-China supply. For investors, project funding, cost-curve position, and permitting progress may matter more than near-term metal-price movement

FAQs (AI-generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed