Beyond the DFS: 7 Catalysts That Could Re-Rate Sovereign Metals

Sovereign Metals' Kasiya project moves beyond the DFS with seven re-rating catalysts, including financing, rare-earth upside, permitting, and US interest.

Project Overview

Sovereign Metals Limited (ASX: SVM | AIM: SVML | OTCQX: SVMLF) has delivered a definitive feasibility study (DFS) for the Kasiya Rutile-Graphite Project in Malawi, establishing a pre-tax net present value at an 8% discount rate (NPV8%) of US$2.2 billion alongside a 23% internal rate of return (IRR) and projected annual earnings before interest, taxes, depreciation, and amortisation (EBITDA) of US$476 million. Those headline economics, however, are only 1 dimension of the re-rating thesis. A May 27, 2026, announcement confirmed that monazite recovered from the DFS flowsheet's non-conductor tailings stream carries dysprosium-terbium and yttrium ratios within the total rare earth oxide (TREO) basket approximately 7 times higher than the world's 5 largest rare earth producers, with dysprosium, terbium, and yttrium all present in pits scheduled for Year 1 production. With a potential third revenue stream requiring no additional mining capital, a US government actively seeking to secure critical mineral supply chains, and a US listing under consideration, the investment case has accumulated several near-term catalysts that extend well beyond the DFS base case.

1. A DFS That Resets the Scale Benchmark for Critical Minerals

Kasiya's DFS positions Sovereign as the world's largest and lowest-cost producer of both rutile and graphite, with economics underpinned by conservative commodity price assumptions. The DFS establishes a 25-year mine life with initial throughput of 12 million tonnes per annum from a single southern processing plant, scaling to 24 million tonnes per annum from Year 5 as the northern plant comes online. Annual free cash flow is projected at well over US$400 million at full production. Rio Tinto holds a strategic stake in the company. The DFS base case uses a realised rutile price of approximately US$1,670 per tonne and a graphite price of approximately US$1,288 per tonne, both supplied by independent commodity consultants. The graphite price is conservative relative to current US market pricing for jumbo flake of approximately US$2,000 to US$2,200 per tonne, reducing downside scenario risk.

2. Free-Dig Mineralogy Drives a Structural Cost Advantage

Kasiya's surface mineralisation eliminates the capital-intensive comminution circuits that drive costs at hard-rock mining peers. The deposit sits within a deep tropical weathering profile on the flat Lilongwe Plain. Rutile, monazite, and graphite are hosted in a laterally extensive blanket within the weathered zone above the saprock boundary. The processing flowsheet targets a starting power requirement of 30 megawatts, scaling to 60 megawatts at full capacity. The current Malawi national grid can supply both stages, and the World Bank, Total, and EDF are doubling the capacity of Malawi's electricity grid, providing additional power security for the ramp-up phase. The free-dig orebody requires no drilling, blasting, or pre-strip, keeping the processing flowsheet simple and low-energy across both production phases.

3. Monazite Introduces a Potential Third Revenue Stream at Near-Zero Incremental Cost

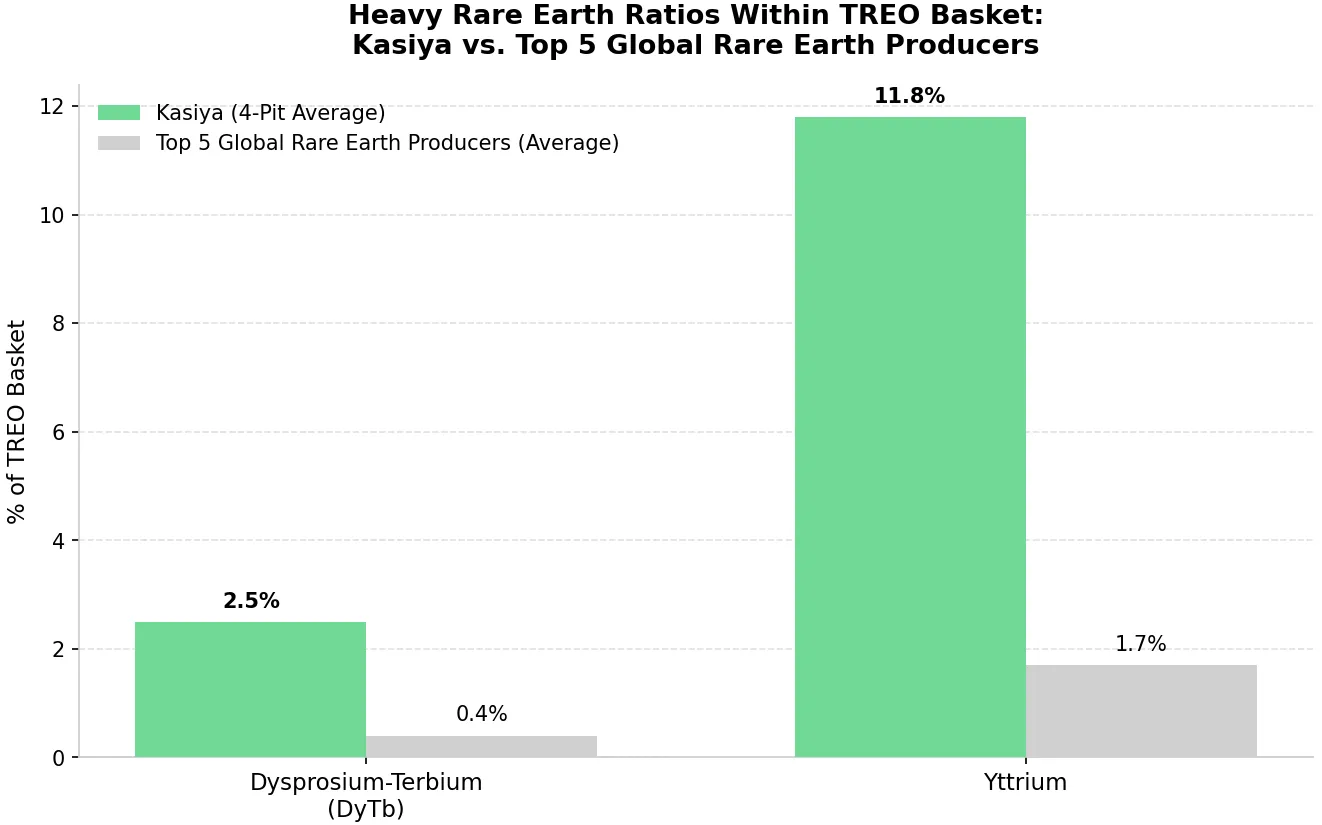

Heavy rare earth-bearing monazite confirmed across 4 DFS pits, including Year 1 production areas, introduces upside not captured in the US$2.2 billion NPV8% base case. The May 27, 2026, announcement confirmed monazite concentrates containing all 4 magnetic rare earth elements (REE) across the Babbler, Kingfisher, Sparrow, and Mousebird pits. The 4-pit weighted average total rare earth oxide (TREO) basket carries 2.5% dysprosium-terbium and 11.8% yttrium, compared to 0.4% dysprosium-terbium and 1.7% yttrium across the 5 largest global rare earth producers. Near-surface intervals from 0 to 6 metres return dysprosium-terbium up to 3.1% and yttrium up to 17.2%.

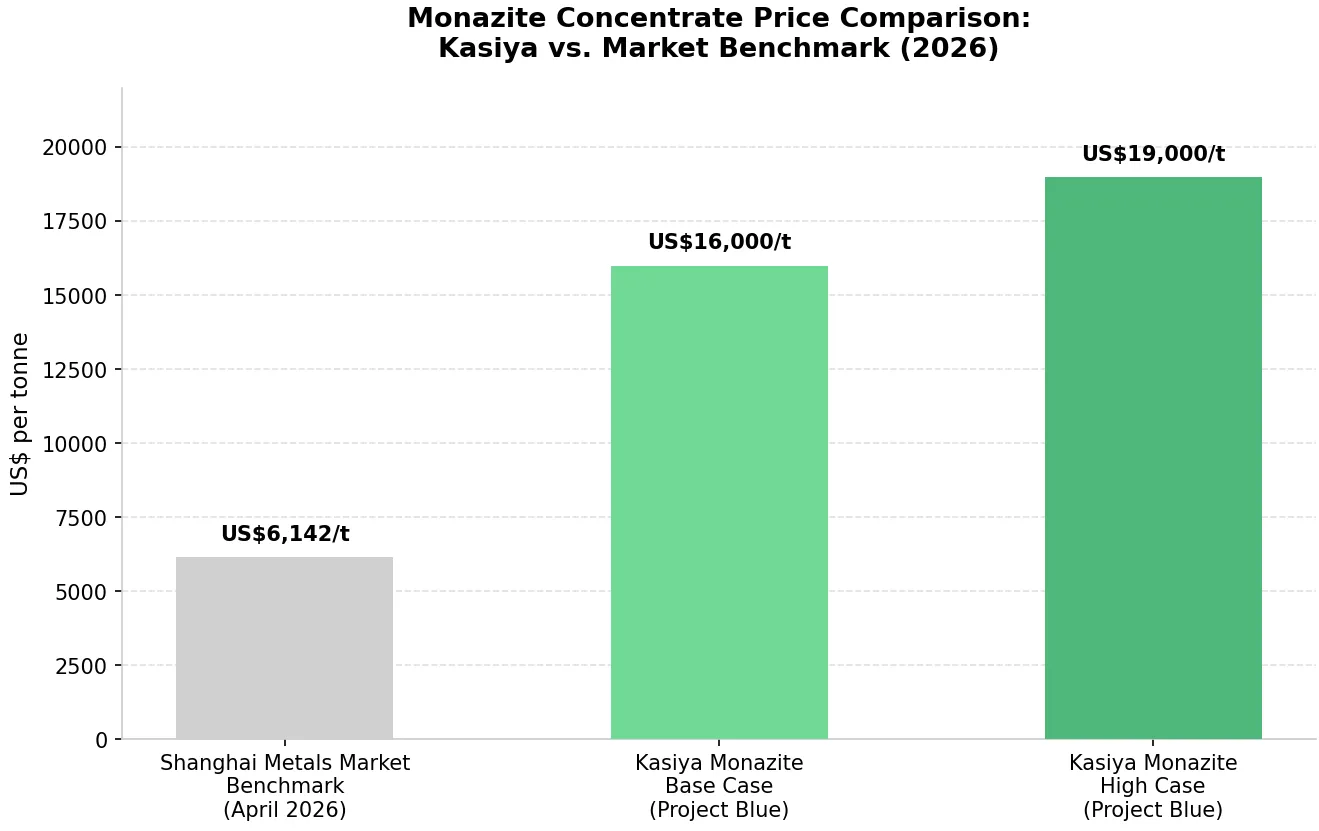

Recovery requires no additional mining, no new primary processing circuits, and no additional reagents. An independent price forecast by Project Blue Group Limited values a 60% TREO monazite concentrate at US$16,000 per tonne base case and US$19,000 per tonne high case, against the April 2026 Shanghai Metals Market benchmark for standard monazite of US$6,142 per tonne. The premium reflects Kasiya's exceptional heavy rare earth proportion of the TREO basket.

4. Western Supply-Chain Decoupling Reprices the Strategic Value of Kasiya's Rare Earths

On February 24, 2026, US Assistant Secretary of War for Industrial Base Policy Michael P. Cadenazzi Jr. testified before the Senate Armed Services Committee that China controls 95% of global heavy rare earth output and the US imports almost 100% of what it uses. China's April 2025 export controls on dysprosium, terbium, and yttrium have tightened Western supply, with the US 100% reliant on imports for yttrium. MP Materials Corp., America's only fully integrated rare earth producer, reports no measurable dysprosium, terbium, or yttrium, leaving no domestic US equivalent to Kasiya's heavy rare earth profile.

Chief Commercial Officer of Sovereign Metals, Sapan Ghai, outlined the scale of America's critical minerals dependency:

"The US has a critical minerals problem. Zero domestic titanium, zero domestic graphite, zero domestic heavy rare earths. The minerals that build America's industrial complex, its defence systems, and its advanced tech are all controlled by nations it would rather not have controlling those supply chains. And so we can unlock that entire ecosystem for the US."

Recent M&A activity frames the valuation context. On April 20, 2026, USA Rare Earth, Inc. agreed to acquire Serra Verde Group for approximately US$2.8 billion, underpinned by a 15-year US government-backed offtake with floor prices of US$575 per kilogram for dysprosium and US$2,050 per kilogram for terbium. On January 20, 2026, Energy Fuels announced a US$299 million acquisition of Australian Strategic Materials Limited. Both transactions crystallise the premium Western capital markets now ascribe to scaled, non-Chinese REE supply.

5. Toho Titanium Qualification De-Risks the Rutile Offtake Pathway

Toho Titanium's sign-off on Kasiya rutile removes the primary technical barrier to entering the Western defence and aerospace titanium supply chain. Toho is Japan's most technically demanding titanium producer, and, following Russia's exclusion from Western procurement post-2022, Japan is now the sole supplier of defence-grade and aerospace-grade titanium to the Western world. Toho confirmed that Kasiya rutile is fully on specification for its entire production range. The US currently produces zero domestic titanium sponge and is 100% import-reliant. The F-35B Lightning II programme uses approximately 35% titanium by weight, with Virginia-class submarines, M1 Abrams tanks, and Boeing 787 aircraft all titanium-intensive platforms.

Ghai put the supply chain stakes plainly:

"You're not going to have your jet fighters. You're not going to have your Virginia-class submarines. You're not going to have your M1 Abrams tanks. You're not going to have your 787s. They're not going to work if you don't have your titanium, and your titanium guys are saying we're not going to be able to produce this without your rutile."

6. IFC Involvement Signals a Bankable Financing Structure

The International Finance Corporation (IFC) is engaged as a potential co-lead arranger for project financing. IFC performance standards are widely recognised by commercial banks, private debt funds, development finance institutions (DFIs), and government agencies as the benchmark for project bankability. Sovereign is close to completing the environmental and social impact assessment (ESIA), which, together with the DFS, forms the mining licence application.

The indicative financing structure targets approximately 60% debt of approximately US$400 to US$450 million, with the remainder from equity, prepayments, and offtake finance. Mitsui has signed a non-binding offtake MOU covering over 50% of Stage 1 rutile production, and Traxys of North America has signed a non-binding offtake MOU with Sovereign targeting up to 40,000 tonnes per annum of graphite during Phase 1 in support of US critical minerals stockpiling initiatives, providing contracted revenue visibility to support the debt case.

7. A Potential US Listing Could Unlock a New Investor Base at the Optimal Moment

A US equity listing would align Sovereign's capital structure with the primary source of government and institutional funding now actively seeking non-Chinese critical mineral exposure. Sovereign already carries significant US capital on its share register and has been engaged with the US State Department, Department of Defense, Office of Strategic Capital, US International Development Finance Corporation (DFC), and US Trade and Development Agency. A US listing would formalise access to the institutional capital pools deploying into critical minerals, consistent with the DFC's US$565 million mine development finance commitment to Serra Verde. The company believes US investors focus on cash flow generation and cost position rather than NPV mechanics, a profile Kasiya's phased production ramp addresses directly.

Key Takeaway for Investors

- Kasiya's definitive feasibility study positions Sovereign Metals as the world's largest and lowest-cost producer of both natural rutile and graphite, with a net present value at an 8% discount rate of US$2.2 billion and annual earnings before interest, taxes, depreciation, and amortisation of US$476 million over 25 years.

- Heavy rare earth-bearing monazite confirmed across Year 1 production pits introduces a potential third revenue stream recoverable from the existing flowsheet at near-zero incremental cost, with an independent base-case price forecast of US$16,000 per tonne, not included in the current base case valuation.

- China's export controls on dysprosium, terbium, and yttrium, and the absence of any domestic US equivalent, make Kasiya's rare earth profile strategically irreplaceable to Western defence and aerospace supply chains.

- Toho Titanium qualification and strong offtake interest from Mitsui and Traxys de-risk the revenue pathway for both rutile and graphite at the project financing stage.

- A potential US listing, combined with IFC co-lead financing engagement, could catalyse re-rating by connecting Sovereign's equity to the capital base most directly incentivised to fund the project.

Bottom Line

Sovereign Metals has advanced Kasiya from a development-stage thesis to a bankable project with a US$2.2 billion NPV8%, qualified product, defined offtake interest, and a financing structure anchored by the IFC. The subsequent monazite announcement materially upgrades the investment case: a potential third revenue stream with heavy rare earth ratios 7 times above producing peers, recoverable from the existing flowsheet with no additional mining capex, at a time when the US government has described non-Chinese rare earth supply as a matter of national security. The project's path to a final investment decision runs through 4 key milestones: ESIA completion and mining licence submission, IFC financing package advancement, quantification of monazite recoverable volumes across the deposit, and any formal US listing announcement, each of which represents a discrete re-rating event for a project whose base-case valuation does not yet reflect the full scope of what Kasiya may produce.

Analyst's Notes

Subscribe to Our Channel

Stay Informed