GoviEx Uranium (GXU) - African Uranium Primed For Production

Matthew Gordon spoke with Daniel Major, CEO of GoviEx Uranium (TSX-V: GXU) to discuss the global uranium industry and the potential of the African uranium sector.

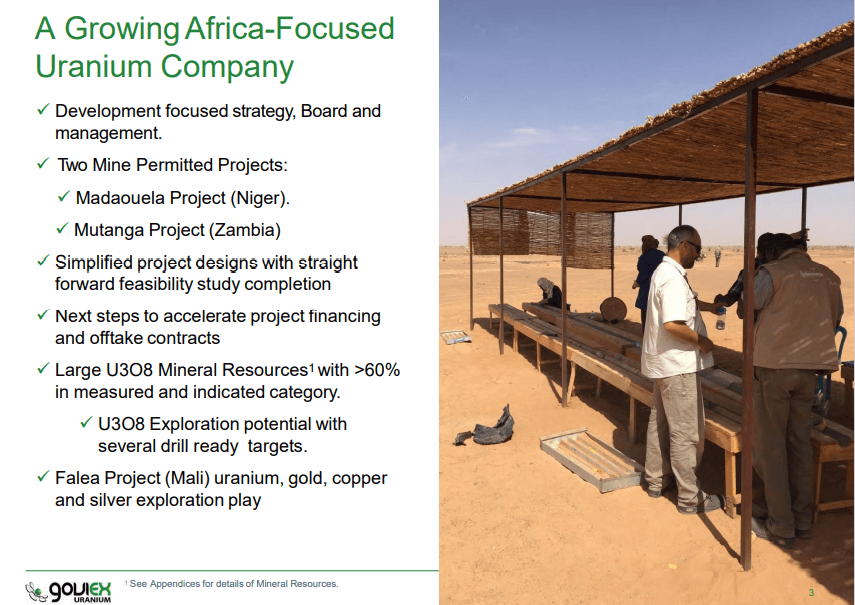

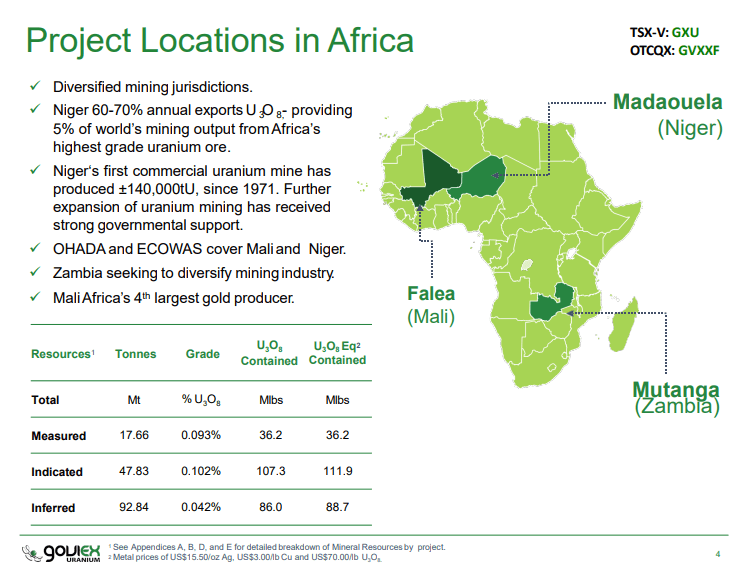

GoviEx Uranium Inc. is a mineral resource company focused on the exploration and development of uranium properties in Africa. The company has a sizable resource inventory with over 143Mlbs U₃O₈ (Triuranium octoxide) in M&I (Measured and Indicated) categories and 86.9Mlbs U₃O₈ in the inferred category. The company’s principal objective is to become a significant uranium producer through continued exploration and development of the flagship mine-permitted Madaouela Project in Niger, the mine-permitted Mutanga Project in Zambia, and the multi-element Falea Project in Mali.

Matt Gordon caught up with Daniel Major, CEO, GoviEx Uranium. Daniel is a mining engineer from the Camborne School of Mines in the UK. His career spans over 30 years in the mining industry, where he has established a solid record of accomplishment initially with Rio Tinto at the Rossing Uranium Mine in Namibia, the Amplats in South Africa, and later as a mining analyst with HSBC Plc and JP Morgan Chase & Co. in London.

Next, Mr. Major was Chief Executive and later Non-Executive Chairman of Basic Element Mining and Resource Division in Russia. He has held leadership positions at several Canadian-listed mining companies with exploration and producing assets in Canada, Russia, and South America. Daniel joined GoviEx Uranium in 2012 as a Director and CEO and has been responsible for the transition of the company from explorer to developer.

Company Overview

GovEx Uranium is a mineral resource company with projects in Africa. The company was founded in 2006 and is headquartered in Vancouver, Canada. Chirundu Joint Ventures Limited, GoviEx Uranium Zambia Limited, Pitchstone Exploration Namibia (Pty) Limited, Rockgate Capital Corp, GoviEx Nigher Holdings Limited, and Muchinga Energy Resources Limited are the company’s subsidiaries. It is listed on the Toronto Stock Exchange (TSX-V: GXU), and the OTC Markets (OTCQX: GVXXF).

GovieEx Uranium is an African-focused uranium development company. The company has projects in Niger, Zambia, and Mali. It is currently focused on advancing the Niger project through financing and entering production by 2025.

Geopolitical Ramifications

According to GovEx Uranium, the ongoing Russia-Ukraine conflict will have an adverse effect on the uranium industry which is already facing its fair share of challenges. Last year, there were market concerns in relation to the diversification of uranium supply from Kazakhstan. Notably, the number of uranium operations around the world are fairly limited, and a large portion of these operations are under Russia’s sphere of influence. The ongoing conflict has massively exacerbated the problem. The problem has now extended beyond uranium mines to encompass conversion facilities and enrichment as well. It is important to note that 20% of the uranium consumed in the US is enriched by Russia.

While steps can be taken to reduce the impact on the uranium industry, it cannot be fully eliminated. The ongoing direct and indirect sanctions against Russia have had severe implications for the shipping lines as they refuse to move material out of the country. Furthermore, the ships that do operate in Russia may not be insurable, which further adds to the mounting problem.

Uranium is a global industry, where the material is mined from all over the world and sent to different conversion points across the globe. Following this, the material is enriched in different countries. As a result, the industry can only grow when uranium can flow freely through the various processes. The current situation acts as a barrier to this growth.

Recently, there were concerns regarding a potential nuclear tragedy similar to Japan’s Fukushima incident. The Zaporizhzhia nuclear power plant in Ukraine was attacked by Russian forces. Through it was found that the resultant fires were not in close proximity to the reactors at the power plant and that only 1 out of 6 reactors are currently operational at the Zaporizhzhia plant.

It is important to note that nuclear power plants are designed to handle extreme stresses and damage. In fact, the dome that covers the reactor is designed to withstand the full impact of a passenger liner. In addition, these plants have several safety features built-in. The nuclear power industry takes the safety of reactors very seriously. Although the attacks near the power plant can be alarming, they aren’t considered high risk due to the built-in safety features and the engineering that goes into building these plants.

Industry Impact

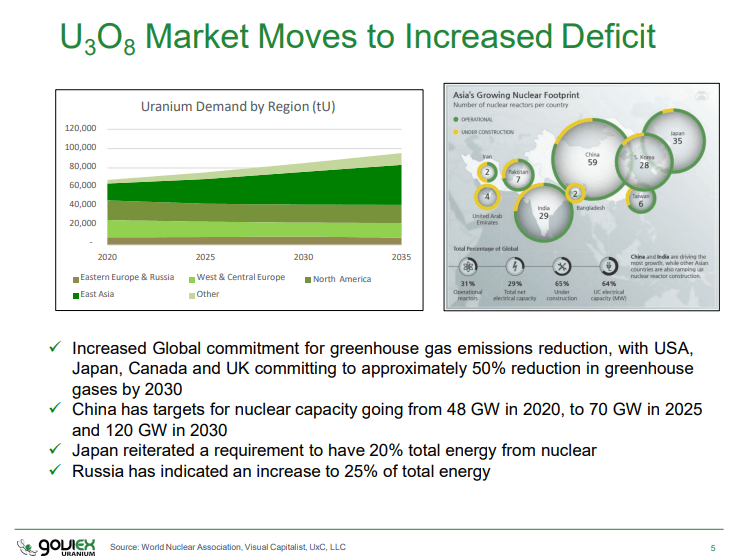

As per GoviEx Uranium, the ongoing Russia-Ukraine conflict has enabled the uranium industry to grow stronger. Since the gas supply to various European countries has been cut, it has increased the burden of energy generation on coal and oil, the majority of which comes from the Soviet bloc. In addition, the supply of a lot of minerals that are used for producing nickel and other commodities also comes from this region. There are concerns in the market about supply shortages when it comes to feeding the construction of renewables in various forms.

It is important to understand the energy throughput for various power sources. For instance, one unit of coal provides 10 units of energy. For oil, this factor is 50, while for uranium, the number is 100. This is increasingly becoming part of the ongoing discussion as nuclear power is not only safe but also has a very high energy yield. This means that nuclear power does not require large quantities of material to be moved around. Uranium offers a lot of potential, as it is available in abundance and has a fantastic power generation capacity.

China made announcements 2 months ago that it will invest $400Bn for new reactors in the country. The relationship between Kazakhstan and China has been a strong one. The former is a major uranium producer. In fact, there is a rail line that directly links both countries that has allowed China to stockpile reserves. It is expected that 40%-50% of all uranium produced in Kazakhstan will go directly to China. However, China will need a lot more uranium to meet its growing demands.

Kazatomprom, the Kazakhstan uranium giant is expected to see a decline in a lot of big uranium fields by the end of the decade. The company has made it clear that it does have additional uranium, however, it won’t be available at the same economics or have a guaranteed supply in the future.

China would still need to meet its growing demands and might consider sourcing the supply from the African continent. It is important to note that the China National Nuclear Corporation (CNNC), a state-owned enterprise, has cooperation with Ghana. However, as of August 2020, the US government issued restrictions for American companies to conduct business with CNNC due to its association with nuclear weapons. The executive order for these restrictions was signed by both President Trump and President Obama. Share ownership by certain companies in China is sanctionable. This makes direct investment by China into North American projects challenging. This situation also creates problems for companies seeking debt as a side effect of the restrictions.

Although these restrictions limit Chinese access to North American companies in Africa, China can still go through the offtake agreement route, enabling it to acquire the whole entity. However, it can be a challenging situation where a large investor is a minority. This is because China has historically shown the desire to have complete control.

While China has been looking to get into Kazakhstan, it seems to be politically distancing itself from Russia, given the ongoing crisis. As a result, China will look towards Africa to fulfil its mineral demands as it is geopolitically acceptable, and because African countries have a history of dealing with China for a long time, leading to increased chances of acceptance.

The African Mining Landscape

The African continent comprises 54 countries that have different approaches when it comes to mining and permitting. The continent is known to have the largest mobile banking platform in the world as the majority of the population conducts financial transactions by way of mobile phones. It relies on external countries for power requirements. Notably, subsistence farming is a huge market in Africa.

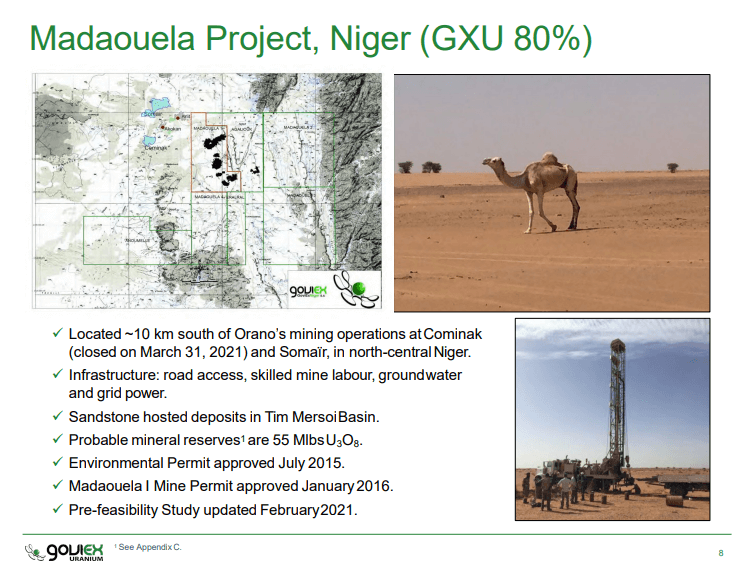

Niger has been producing uranium since the early 1970s. The government here is focused on the development of commodities. There is a reasonable shift towards growing the power base in Africa through the use of renewable sources, despite the fact that the majority of the continent is highly reliant on hydrocarbons for energy requirements. However, some countries have started looking toward nuclear energy as a power source. Africa has the highest growth rate of any continent across the world, making it a great place for investments.

GoviEx Uranium has been in Africa since 2007. The company started drilling in Niger back in 2008. It has a strong working relationship with the Niger government. Notably, the government is focused on supporting projects as it leads to job creation, which in turn, generates revenue for the government and leads to infrastructure development. This also helps the companies with CSR (Corporate Social Responsibility) and ESG (Environmental, Social, and Governance) initiatives. The local government understands that the companies need to help and support the communities that are based around the mines. Zambia is fairly similar in its approach to mining.

In comparison, it is far more challenging to conduct uranium mining operations in Australia. The Labour government either at the federal or state level can often serve as a barrier to uranium mining. As a result, companies have to wait out the tenure of the Labour government to operate.

In the United States, there is a lot of conversation around the need to develop critical commodities. However, until there are EPA (Environmental Protection Agency) changes from an environmental perspective, moving forward is difficult. Furthermore, the added power vested in the indigenous communities makes it harder for projects to continue operations. In fact, several projects have been stopped because of the indigenous groups in recent times.

Each continent has its own set of operational challenges. In Africa, companies need to deal with the local communities, while in countries such as the US and Australia, the companies need to deal with the government. All mining-related work should comply with the IFC standards. There is an overall willingness by everybody to get projects to work. As long as the community and environment are taken into account, the projects get built.

Mining permits in Africa have a significantly quicker approval timeline. In fact, Niger’s mining code states that the government has 4 months to review a licence application and make a decision. This places the commitment on the government to get the project approved so that the companies do not conduct business elsewhere. Furthermore, the African governments have land ownerships, this enables the companies to conduct business directly with the landowner, which allows them to secure the surface rights.

Zambia does not have these issues so the permitting process moves even faster. The mining code here states that the people living on the mining property need to be relocated. To achieve this, companies have to engage with the local community. These regulations come under IFC standards which have clearly defined rules for the relocation of local communities.

There’s an understanding that a company has mineral rights which enables them to conduct mining. Any company that is looking to secure foreign debt needs to follow the accredited principles in IFC when it comes to the local population. The IFC also has certain environmental permitting standards.

Although the local standards are marginally below the IFC standards, a lot of governments in Africa are tightening up these standards going forward. In order to mine, the companies need development. This is what differentiates mining in Africa from other places.

For instance, in Sweden, the environmental side comes before the mining side. This situation is being remedied by the government. Similarly, a large portion of the western governments needs to sort out the balance between environmental and mining concerns. Meanwhile in Africa, there’s an increased emphasis on dealing with the communities properly and providing support. This has enabled GoviEx Uranium to continue operating in Africa even when the uranium market prices were significantly lower.

Mali has had an ongoing coup government since last year that was a result of the dispute with the ECOWAS (Economic Community of West African States) and the French. Despite the coup, the governments prefer businesses to be as stable as possible as it leads to revenue generation in the form of tax.

The situation led to border closures, but since these countries have multiple shared borders, businesses weren’t adversely affected. Since the Guinea border was still open, GoviEx Uranium was able to continue operations. Since people need jobs and salaries to feed their families, work continues despite the mounting challenges.

Zambia has also had a tricky past when it comes to the mining industry. It faces the same set of challenges as Niger. However, since GoviEx Uranium doesn’t have assets in Sahel, there has been little to no impact on operations. Although the previous government had a socialist approach towards spending money, in the end, the support for building projects remains strong. This is because mining projects bring in substantial investments and lead to job creation. Zambia is currently working towards becoming a nuclear country and as a result, it is developing laws and rules associated with radiation. The company is a part of this ongoing program.

GoviEx Uranium continues to have a strong line of communication with the government and its ministries. In 2022, the company made a significant investment relative to the country. In addition to economic development and employment, these investments also lead to the development of infrastructure.

Financing Considerations

When it comes to financing, GoviEx Uranium is approaching the equation on three key aspects, namely debt, offtake, and equity. The spike in uranium prices has had a considerable effect on changing people’s views. On the contrary, during a market downturn, there’s often a lack of interest in the market.

The analyst communities have stopped covering uranium stories and have shifted focus to lithium instead. However, there appears to be a sustained comfort level around uranium in Africa. There has been a substantial increase in the number of banks that are willing to invest in North Africa. Additionally, the African Development Bank along with other entities have shown interest in financing export credits to drive growth in countries like Niger.

GoviEx Uranium has had strong relationships with export credit agencies. On the offtake side of the equation, the company has a natural hedging strategy called long-term contracts for uranium. Locking in these long-term contracts allows the company to approach debt providers which in turn, underpins the risk for the providers.

In terms of equity, the company has seen a lot of new players from both the private and public sectors appear in the uranium sector. As a result, an increasing number of entities are now comfortable investing in Africa due to its growth prospect.

In an attempt to sidestep the growing inflation, GoviEx Uranium strategized its project pipeline and development profile to follow the market direction. In fact, the company timed its Feasibility Study to coincide with the market readiness. Otherwise, it would need to conduct another Feasibility Study which would be a considerable cost overhead. The company’s most recent Feasibility Study was conducted in February 2021, a lot has changed since then. A lot of projects are now seeing that their PFS (Preliminary Feasibility Study) is outdated and when these companies try to conduct a Feasibility Study, they are often faced with environmental and other factors. This leads to design changes that weren’t taken into consideration previously.

Timing the PFS enabled GoviEx Uranium to clear out substantial risk. From the debt perspective, the company simplified the project. The study allowed the company to smoothly progress into the next phase. From an engineering perspective, the company is looking to forecast future inflation based on the current market conditions. The pandemic-induced shipping crisis also appears to be easing as shipping prices are observing a sharp decline. Lastly, the company has also factored in situations where the timing isn’t ideal and costs aren’t favourable to avoid any unforeseen circumstances.

M&A Considerations

GoviEx Uranium is focused on being a developer from both a strategic and operational perspective. The company has taken a practical approach to ensure that it can build the project exactly how it was presented. This is because under-delivering on a promise will let its shareholders down as the end product will be starkly different from what was initially presented to the market.

The company’s approach towards design is to build appropriately going forward. It has a strong focus on a level of detail to ensure that timelines are met and the project is built as per the Feasibility Study. Back in 2016, the company started operating as a consolidator when it acquired Denison Mining’s African assets.

Although GoviEx Uranium was a bit early as a market entrant, it was able to get it right. The company is open to the possibility of M&A (Mergers and Acquisitions). In this scenario, it would start looking for other opportunities. To balance risk, the company has put together a pipeline of projects to ensure that future demands are met.

According to the company, there is a high probability that China’s requirement for uranium may lead to an acquisition which can result in the cut-off for any ongoing offtake agreements. GoviEx Uranium has built its pipeline of projects to ensure that it is more attractive for a potential M&A. Since 2 of its projects are already permitted, the geopolitical risk is no longer a part of the equation.

Growth Prospects

As a developer, GoviEx Uranium is looking to minimise its project risk. Once it enters production, the risk would be massively reduced and it will help the company to achieve the desired outcome. This is because once a project starts generating cash flow, the capital investment and dilution risk are considerably lowered.

The company was able to go from no uranium to achieving 2Mlbs-2.5Mlbs uranium production. Furthermore, the company was able to double its uranium output to 5Mlbs.

The company’s existing projects in Niger benefit from the sheer scale of exploration and deposits. It seeks to further expand its production capacity and develop an additional mine. Following this, the company will have the flexibility to add new Niger properties to its portfolio which will enable it to grow without taking on acquisition risks.

To find out more, go to the GoviEx Uranium website

Analyst's Notes

Subscribe to Our Channel

Stay Informed