Higher US Rates Present Opportunity for Advanced, Low-Cost Rutile Projects

Higher US rates create financing hurdles for African rutile projects. Sovereign Metals' Kasiya offers resilient economics amid tightening capital.

- The U.S. Federal Reserve's "higher-for-longer" interest rate stance is reshaping global capital markets and increasing the cost of capital for new mining developments, particularly in emerging markets.

- Global supply chain reconfigurations and geopolitical tensions are intensifying demand for stable, alternative sources of titanium feedstocks.

- However, Sovereign Metals' Kasiya project in Malawi offers a jurisdictionally stable, high-grade alternative with low capital intensity and Rio Tinto's backing—illustrating the type of project investors may favour in this macro environment.

- Investors are advised to focus on strategic assets with low leverage, non-cyclical demand profiles, and strong off-take or financing partners to weather tightening capital conditions.

Elevated Rates & Global Risk Repricing in the Mining Sector

The Federal Reserve's commitment to maintaining elevated interest rates through 2025-26 continues to reshape global capital allocation patterns, with far-reaching implications for mining sector financing. Despite market expectations for 50 basis points of cuts across the forecast period, terminal rates are projected to remain above 3.25%, significantly constraining monetary easing globally and maintaining pressure on emerging market funding conditions.

This elevated rate environment has fundamentally altered the risk-return calculus for mining investments, particularly those in frontier markets. The combination of higher U.S. dollar-denominated debt costs, tighter credit conditions, and suppressed appetite for long-duration projects in politically sensitive jurisdictions has created a challenging backdrop for African rutile developments.

Impact on Emerging Market Financing

According to Metrobank Research, the Fed's terminal rate projections suggest sustained pressure on global liquidity conditions, with particular stress on emerging market sovereign debt issuance. International Monetary Fund projections on global fiscal deficits further compound these challenges, as rising term premia across U.S. Treasuries create cascading effects on emerging market funding costs.

Mining projects with development timelines extending beyond five years now face significantly more conservative capital allocation strategies from institutional funds and commercial lenders, forcing project sponsors to demonstrate exceptional resource quality and operational advantages to secure financing. This dynamic particularly affects capital-intensive rutile projects in sub-Saharan Africa, where jurisdiction risk premiums have widened alongside global monetary tightening.

Shifting Investment Criteria

The implications extend beyond direct financing costs. Long-duration mining projects, which historically relied on patient capital and favourable debt terms, now confront a financial environment where discount rates have risen materially, compressing net present values and requiring higher commodity price assumptions to achieve investment hurdle rates.

For mining companies operating in this environment, the focus has shifted toward projects offering immediate cash flow generation, minimal execution risk, and clear pathways to debt reduction. The market is increasingly discriminating between assets based on their ability to generate returns that compensate for elevated funding costs and political risk premiums.

Capital Costs & Project Viability in Rutile Market?

Rutile, as a critical feedstock for titanium dioxide production and aerospace-grade titanium alloys, occupies a strategically important position in global industrial supply chains. However, the intersection of rising capital costs and geopolitical supply chain pressures has created a paradox where demand fundamentals remain robust, yet financing for new production capacity has become increasingly constrained.

Financial Health & Strategic Positioning

The elevation in global discount rates has materially impacted project internal rates of return across the rutile sector, forcing developers to reassess project economics and timeline assumptions. It's a real barrier to entry. Projects that appeared commercially viable under previous cost of capital assumptions now face scrutiny regarding their ability to generate acceptable risk-adjusted returns in the current environment.

However, Sovereign Metals' Kasiya project in Malawi demonstrates the type of asset profile that can withstand elevated financing costs. The project's dual revenue stream structure, combining rutile production with graphite as a byproduct, provides economic diversification that reduces commodity price sensitivity.

Chief Executive Officer Ben Stoikovich emphasizes the project's economic resilience:

"The results of our optimized pre feasibility study were exceptional it shows a pre-tax net present value of over $2.3 billion US with an annual average earnings before interest, taxes, depreciation, and amortisation of over $400 million we would be the world's largest rutile producer and we'd have a 64% operating margin"

This economic profile reflects the advantages of high-grade, low-cost deposits in navigating tightened capital market conditions. The project's ability to generate substantial free cash flow from operations provides debt service capacity and reduces reliance on external financing during the production phase.

Foreign Exchange Risk & Debt Exposure

Emerging market currency depreciation has created additional complexity for African rutile projects, with currencies including the Sierra Leone leone and Mozambican metical declining 10-15% year-to-date against the U.S. dollar according to Bloomberg data. This currency mismatch between capital expenditure requirements typically denominated in hard currencies and local operating cost bases creates significant financial risk for project developers.

The underdevelopment of local debt markets in many African jurisdictions forces mining companies to rely heavily on international capital, exposing them to both currency risk and the full impact of global monetary tightening. Projects lacking natural foreign exchange hedges through export revenues or strategic partnerships with international counterparties face particular vulnerability to currency volatility.

Additionally, the limited availability of long-term local currency financing means that most significant mining developments must structure debt in U.S. dollars or other hard currencies, creating ongoing foreign exchange exposure throughout the operational phase. This dynamic has elevated the importance of revenue contracts and offtake agreements that provide natural currency hedging.

Strategic Resource Security Amid Trade & Geopolitical Realignment

The intersection of U.S. trade policy and supply chain security considerations has fundamentally altered the strategic value proposition for rutile projects outside traditional Chinese and Russian spheres of influence. The implementation of 30% tariffs on South African mineral sands and the systematic exclusion of Chinese goods from critical mineral supply chains has forced industrial buyers to actively seek diversified sourcing arrangements.

Supply Chain Shifts & Tariff Impacts

Recent trade policy developments have created immediate market disruption, exemplified by Iluka Resources suspending zircon pricing guidance due to tariff uncertainty. The company's decision reflects broader market confusion regarding pricing mechanisms and contract structures in an environment where traditional supply sources face punitive tariffs or regulatory exclusion.

These policy shifts have created a repricing of geopolitical risk across mineral supply chains, with investors increasingly discounting supply from tariff-exposed regions while reweighting capital allocation toward jurisdictionally stable alternatives. The effect has been to compress valuations for projects in affected regions while creating premium valuations for assets in stable, Western-aligned jurisdictions.

Industrial buyers, particularly in the aerospace and defense sectors, are actively restructuring supplier relationships to reduce dependence on potentially vulnerable supply chains. This strategic shift toward supply security over cost optimization has created new demand patterns that favor politically stable production sources, even at premium pricing.

The Role of Jurisdiction in Strategic Mineral Exposure

Malawi's position as a stable, mining-friendly jurisdiction with established rail-linked export infrastructure exemplifies the type of political and logistical environment that commands premium valuations in the current geopolitical context. The country's consistent mining code, transparent permitting processes, and access to regional export routes through Mozambique provide the operational predictability that risk-sensitive capital increasingly demands.

The Kasiya project's environmental, social, and governance-friendly metallurgy, characterized by low sulfur content and free-dig saprolite ore bodies, aligns with the environmental screening criteria applied by an increasing number of institutional investors. Chief Executive Officer Ben Stoikovich highlights the operational advantages:

"The ore body is contained in totally weathered material and in terms of graphite this leads to significant advantages the ore is free dig and has very low levels of sulfur"

These characteristics reduce both operational complexity and environmental impact, addressing two key concerns for investors navigating heightened environmental, social, and governance scrutiny while managing geopolitical risk exposure.

Structural Deficit in Rutile Supply & Price Stabilisation Signals

Global rutile supply dynamics reflect the intersection of constrained new production capacity and robust demand from non-cyclical end markets including aerospace, defense, and industrial applications. While titanium dioxide demand patterns show seasonal variability, the underlying consumption growth in strategic applications provides support for long-term price stability.

Recent Price Action & Market Signals

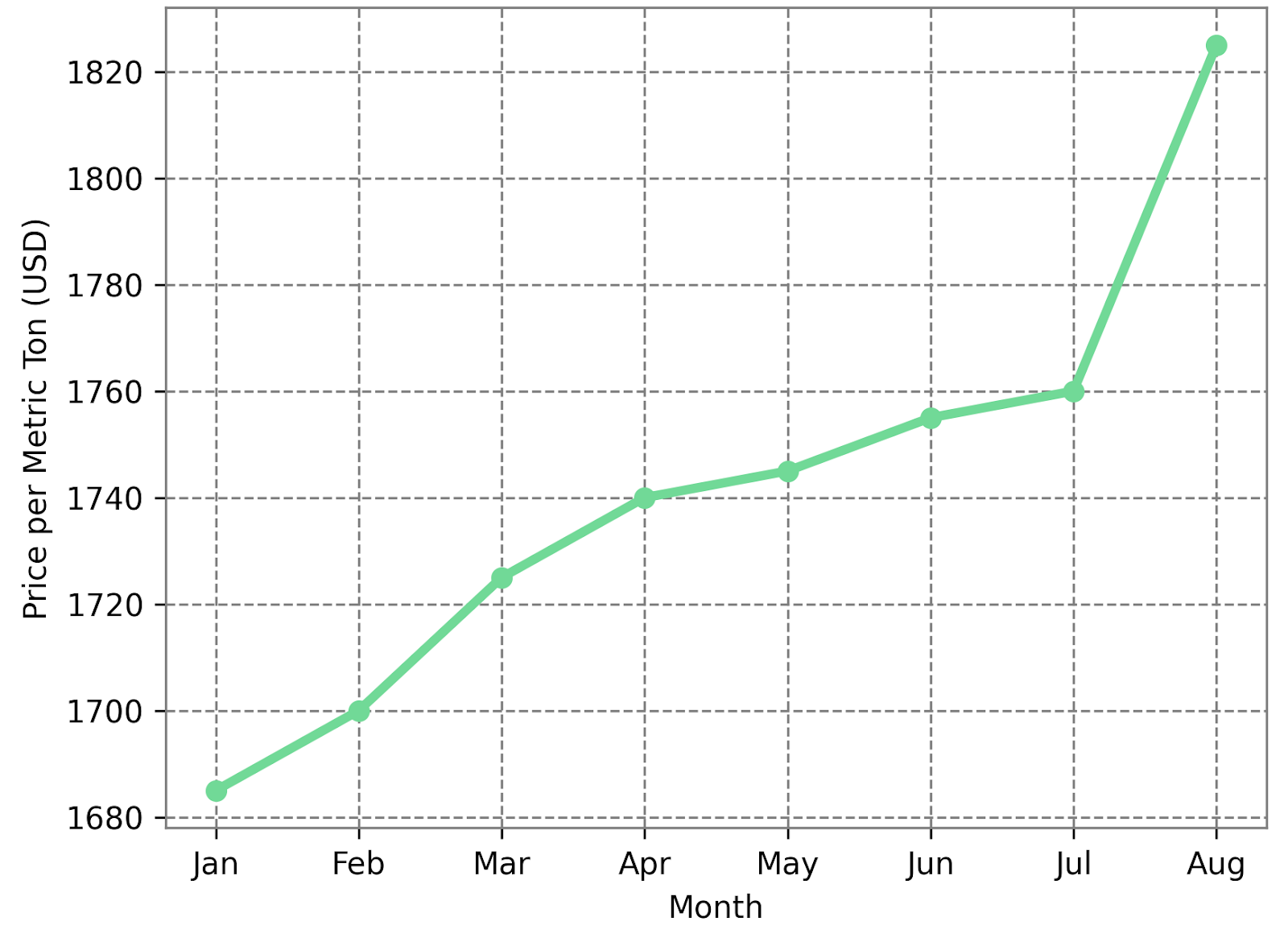

Titanium dioxide pricing has shown signs of stabilization following significant volatility earlier in the year, with free-on-board export prices reaching approximately $1,825 per metric ton in August, representing an $80 per metric ton increase from previous levels. This price recovery reflects upstream cost pressures and suggests that the market may be approaching a sustainable equilibrium between supply and demand fundamentals.

Sponge titanium markets have demonstrated greater stability due to the prevalence of long-term contract arrangements, though margin compression remains evident across the value chain. The aerospace sector's continued demand for high-grade titanium feedstocks provides support for premium rutile pricing, particularly for low-impurity grades suitable for aerospace applications.

Market participants report increasing difficulty securing reliable rutile supplies outside traditional sources, creating opportunities for new producers capable of delivering consistent quality and volume. The concentration of existing production in geopolitically sensitive regions has elevated the strategic value of diversified supply sources.

Production Discipline & Inventory Rebalancing

Chinese titanium dioxide producers have implemented production cutbacks aimed at controlling oversupply conditions and stabilizing pricing, with several major facilities reducing output by 10-15% compared to peak production levels. These supply adjustments appear designed to rebalance inventory levels and support pricing recovery through the fourth quarter.

Seasonal demand patterns typically show strengthening in September as industrial customers rebuild inventory positions ahead of year-end production schedules. Early indicators suggest this seasonal recovery may be more pronounced given the inventory destocking that occurred during the first half of the year.

The combination of supply discipline from established producers and constrained new capacity additions creates a supportive backdrop for rutile pricing, particularly for high-grade material suitable for aerospace and specialty chemical applications.

Allocating Capital in a High-Rate Environment

The current monetary policy environment requires investors to apply elevated hurdle rates when assessing mining project viability, fundamentally altering the competitive landscape between development opportunities. Capital allocation patterns increasingly favor projects demonstrating low leverage profiles, disciplined cost structures, strong execution partners, and clear development timelines.

Institutional allocators are directing capital toward assets offering defensive characteristics including established resource bases, proven metallurgical processes, and strong environmental, social, and governance alignment. Projects with clear catalysts such as definitive feasibility study completion, offtake agreement finalization, or strategic partnership announcements command premium valuations relative to earlier-stage opportunities.

Strategic Partnership Value

The emphasis on execution visibility has elevated the importance of management track records and strategic partnerships with established industry participants. Rio Tinto's strategic investment and technical collaboration with Sovereign Metals exemplifies the type of institutional backing that provides confidence in project delivery capabilities.

Sovereign Metals Chief Executive Officer Ben Stoikovich emphasizes the value of this strategic alignment:

"The Sovereign team along with our partner Rio Tinto is rapidly progressing with the Kasiya definitive feasibility study which we aim to publish in the fourth quarter of this year"

This partnership structure provides both technical expertise and financial credibility that addresses investor concerns regarding execution risk in challenging market conditions.

The Investment Thesis for Rutile

- Macro tailwinds favor jurisdictionally secure projects as global supply chain rewiring and elevated geopolitical risk create premium valuations for politically stable production sources.

- Structural supply gap conditions persist as global rutile production has declined while new capacity remains scarce and financing-constrained under elevated capital costs.

- Strategic applications provide non-cyclical demand support from aerospace, defense, and energy transition sectors that underpin long-term price stability regardless of broader economic conditions.

- Jurisdictional advantage becomes increasingly valuable as projects like Kasiya offer regulatory transparency, permitting clarity, and established logistical infrastructure in stable political environments.

- Strong financial alignment through backing from major partners like Rio Tinto provides execution confidence and mitigates project financing risk in a tightened capital environment.

- Diversified economics through dual-commodity revenue streams from graphite byproducts provide economic insulation against single commodity price volatility and enhance overall project returns.

Strategic Clarity in a Tightening Cycle

Higher U.S. interest rates and shifting global capital flows create headwinds for emerging market mining developments while simultaneously clarifying which projects possess the fundamental characteristics necessary to attract capital under scrutiny. The current environment rewards assets demonstrating exceptional resource quality, strong jurisdictional positioning, and credible execution capabilities.

Sovereign Metals' Kasiya project demonstrates resilience through tier-1 resource scale, robust economic margins, and Rio Tinto's strategic support, positioning it favorably within a constrained capital allocation environment. As supply chains realign and demand for critical minerals grows, investors must differentiate based on jurisdictional risk, cost structure, and execution visibility to navigate successfully through this monetary tightening cycle.

Analyst's Notes

Subscribe to Our Channel

Stay Informed