How Fed Policy is Reshaping the Investment Case for Gold Developers & Producers

Fed policy shifts drive gold mining investment strategy as developers leverage high IRRs while producers optimize margins in $3,000+ price environment.

- Strong US economic data has delayed interest rate cuts, but disinflation trends and foreign exchange weakness are beginning to reshape investor positioning in gold

- The Federal Reserve is expected to ease starting December 2025, reinforcing gold's role as a hedge against declining real yields and policy uncertainty

- Gold is consolidating near record highs, supported by central bank demand, ETF inflows, and a weakening dollar - creating margin tailwinds for miners

- Developers like Cabral Gold and New Found Gold are capitalizing on high internal rates of return and short payback periods, with minimal dilution via phased strategies

- Producers such as Perseus Mining and i-80 Gold are managing all-in sustaining costs and growth capital while maintaining operational visibility in Tier-1 jurisdictions

Monetary Shifts & Macro Tailwinds for the Gold Market

The Federal Reserve's monetary policy trajectory continues to evolve as economic data presents mixed signals for interest rate timing. June's stronger-than-expected US retail sales and falling jobless claims have effectively delayed anticipated rate cuts, creating a more complex investment environment for precious metals positioning.

Federal Reserve policymakers remain divided on the timing of monetary easing. While some officials signal a prolonged pause in rate adjustments, others indicate potential cuts beginning in late 2025. JP Morgan's current forecast anticipates four rate reductions by mid-2026, suggesting real yields may peak in the second half of 2025.

This monetary transition phase carries significant implications for gold pricing dynamics. Historical precedent demonstrates that gold typically outperforms during periods of declining real interest rates, as the opportunity cost of holding non-yielding assets diminishes. The current environment presents a compelling backdrop for precious metals allocation as investors position for this potential inflection point.

Real yields and US dollar dynamics represent the primary fundamental drivers for gold price formation. Current market positioning reflects growing confidence in gold's medium-term outlook, with major investment banks raising year-end forecasts substantially. JP Morgan, Goldman Sachs, and Macquarie have elevated their gold price targets to a range of $3,300 to $3,700 per ounce.

The dollar's recent weakness against the euro and Japanese yen reinforces gold's international bid, particularly as central banks continue diversifying reserve compositions. This foreign exchange dynamic creates additional tailwinds for gold-denominated investments, supporting both spot prices and mining sector margins.

Repricing Risk & Opportunity Across the Mining Sector

The gold mining sector is experiencing fundamental revaluation as sustained higher prices reshape project economics and investment hurdle rates. At current gold prices above $3,000 per ounce, average project internal rates of return increase by a factor of two to three times compared to historical $1,700 baseline assumptions.

Asset Revaluation in a $3,000 Per Ounce World

Development projects that appeared marginal at lower gold prices now demonstrate compelling investment characteristics. Payback periods for capital-intensive projects often contract by 50% or more, fundamentally reshaping capital allocation frameworks across the sector.

This repricing extends beyond headline metrics to operational flexibility and resource definition thresholds. Higher gold prices enable companies to include previously sub-economic material in mine plans, effectively expanding resource bases without additional exploration expenditure. The impact cascades through feasibility studies, permitting applications, and financing structures.

Enhanced project economics at Cabral Gold's Cuiu Cuiu project demonstrate this dynamic, with Chief Executive Officer Alan Carter noting:

"The numbers on the preliminary feasibility study are very very encouraging. The post-tax internal rate of return jumped from 47% nine months ago to 78% today, modelled at $2,500 an ounce gold."

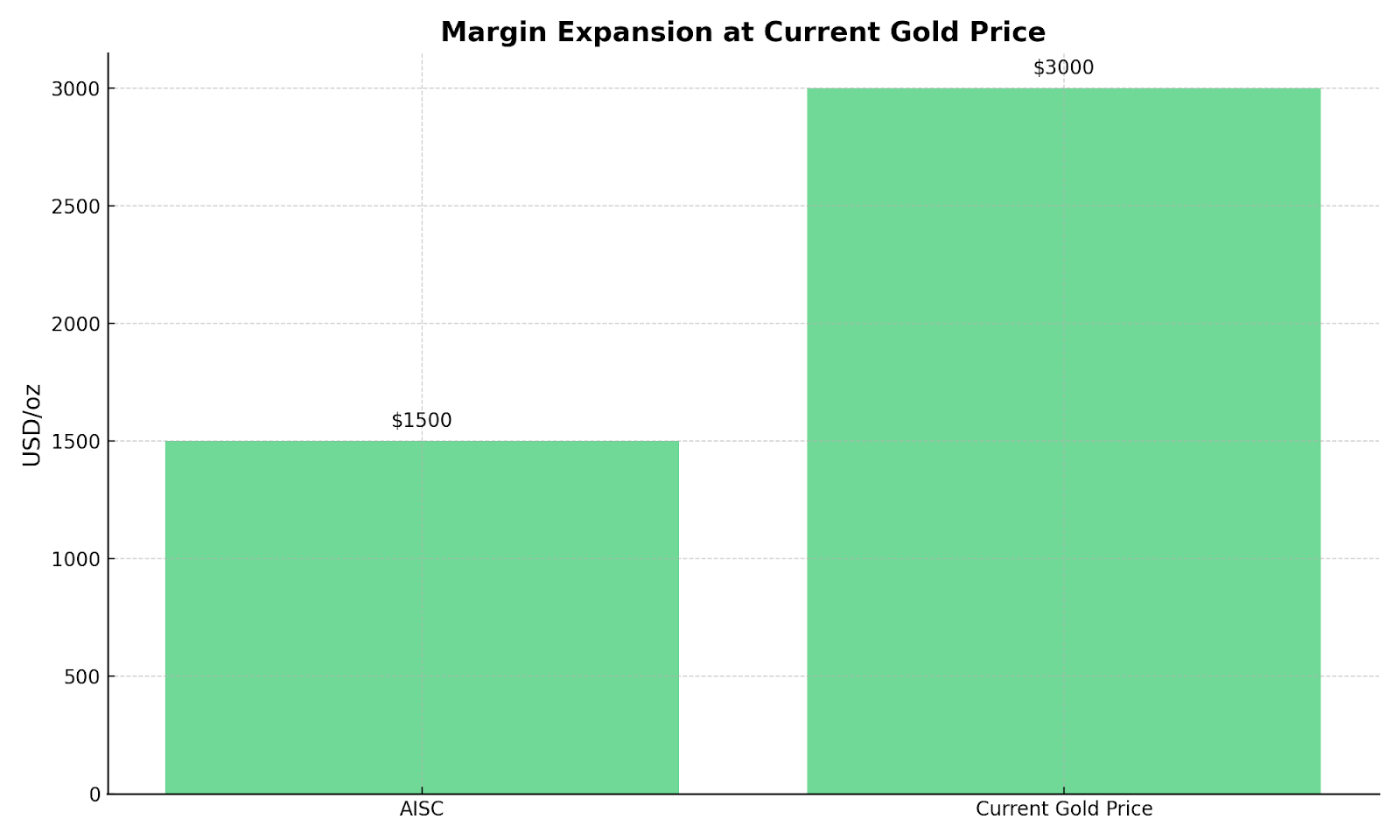

Margin Expansion for High All-In Sustaining Cost Producers

Even producers with all-in sustaining costs approaching $1,500 per ounce now generate gross margins exceeding $1,500 per ounce at current gold prices. This margin expansion enables self-funding of brownfield growth initiatives, reducing dependence on equity markets and associated dilution risks.

The operational leverage inherent in gold mining becomes pronounced at elevated price levels. Fixed costs associated with infrastructure, labor, and regulatory compliance remain relatively stable, allowing variable margin expansion to flow directly to free cash flow generation.

Strategic Capital Allocation Across the Mining Value Chain

The gold mining sector's response to Federal Reserve policy evolution varies significantly across development stages, with each category employing distinct capital allocation strategies to optimize returns in the current elevated price environment.

Development Stage Companies: Capital Efficiency & Phased Growth

Development-stage companies are positioning themselves to capitalize on high gold prices through carefully structured phased approaches that minimize external financing requirements while preserving long-term growth optionality.

Cabral Gold represents the archetypal low-capital, high-return development opportunity in the current environment. The company's starter heap leach project requires $37.7 million in capital expenditure while generating an 82.6% internal rate of return with payback periods under one year.

New Found Gold exemplifies sophisticated phased development strategy through its Queensway project. The company's Phase 1 toll-milling approach at 700 tonnes per day provides a foundation for subsequent expansion to 7,000 tonnes per day capacity while maintaining capital discipline.

New Found Gold Chief Executive Officer Keith Boyle highlights the strategic timing advantages:

"The preliminary economic assessment highlights a phased approach that gets them to cash flow rapidly. At a $2,500 gold price, the project's net present value is $743 million and the after-tax internal rate of return is 56.3% with a payback of less than two years."

Production Stage Companies: Operational Leverage & Growth Capital

Established producers are navigating the balance between growth capital deployment and shareholder returns, leveraging operational cash flows to fund expansion while maintaining dividend potential in an environment of elevated gold prices.

Perseus Mining demonstrates the operational leverage available to established producers with diversified asset portfolios. The company's five-year production outlook, supported by 93% proven reserves, exemplifies sector focus on operational visibility and capital discipline.

Perseus Mining Chief Executive Officer Jeff Quartermaine outlines the company's performance metrics:

"For the last financial year ending 30th June, production was close to 500,000 ounces. The weighted average all-in sustaining cost for the year was $1,235 an ounce, which is fairly credible in global terms."

i-80 Gold represents infrastructure-leveraged growth within established mining jurisdictions. The company's Nevada-focused strategy utilizes existing processing facilities to minimize capital intensity while scaling production significantly.

Integra Resources exemplifies self-funded development strategy through cash flow generation from existing operations. The company's acquisition of Florida Canyon provides funding capability for development at DeLamar and Nevada North projects. Jason Banducci, VP of Corporate Development and Investor Relations highlights:

“We're lucky with the acquisition of Florida Canyon we don't need to raise equity again until we uh until we end up building DeLamar"

Serabi Gold brings specialized underground mining expertise to the production category, with Chief Executive Officer Mike Hodgson's 18-year tenure demonstrating operational consistency in challenging environments:

"Coringa coming in has has has allowed us to move from being a company that was plateaued at 40,000 ounces and allows us to grow to 70,000 ounces"

West Red Lake Gold Mines showcases successful mine restart execution in established Canadian jurisdictions. The company's Matsen mine restart demonstrates operational capability in proven geological environments.

West Red Lake Gold Mines President and Chief Executive Officer Shane Williams confirms operational execution:

"West Red Lake Gold Mines is in the process of putting the Madsen mine back into production, and recently announced its restart. The bulk sample program confirmed that the resource and the work we've done is fully into place as we expected."

Market Liquidity & Investor Allocation Patterns

Gold market liquidity dynamics reflect shifting investor sentiment as monetary policy expectations evolve. Exchange-traded fund flows and institutional allocation patterns provide insight into positioning changes across different investor categories.

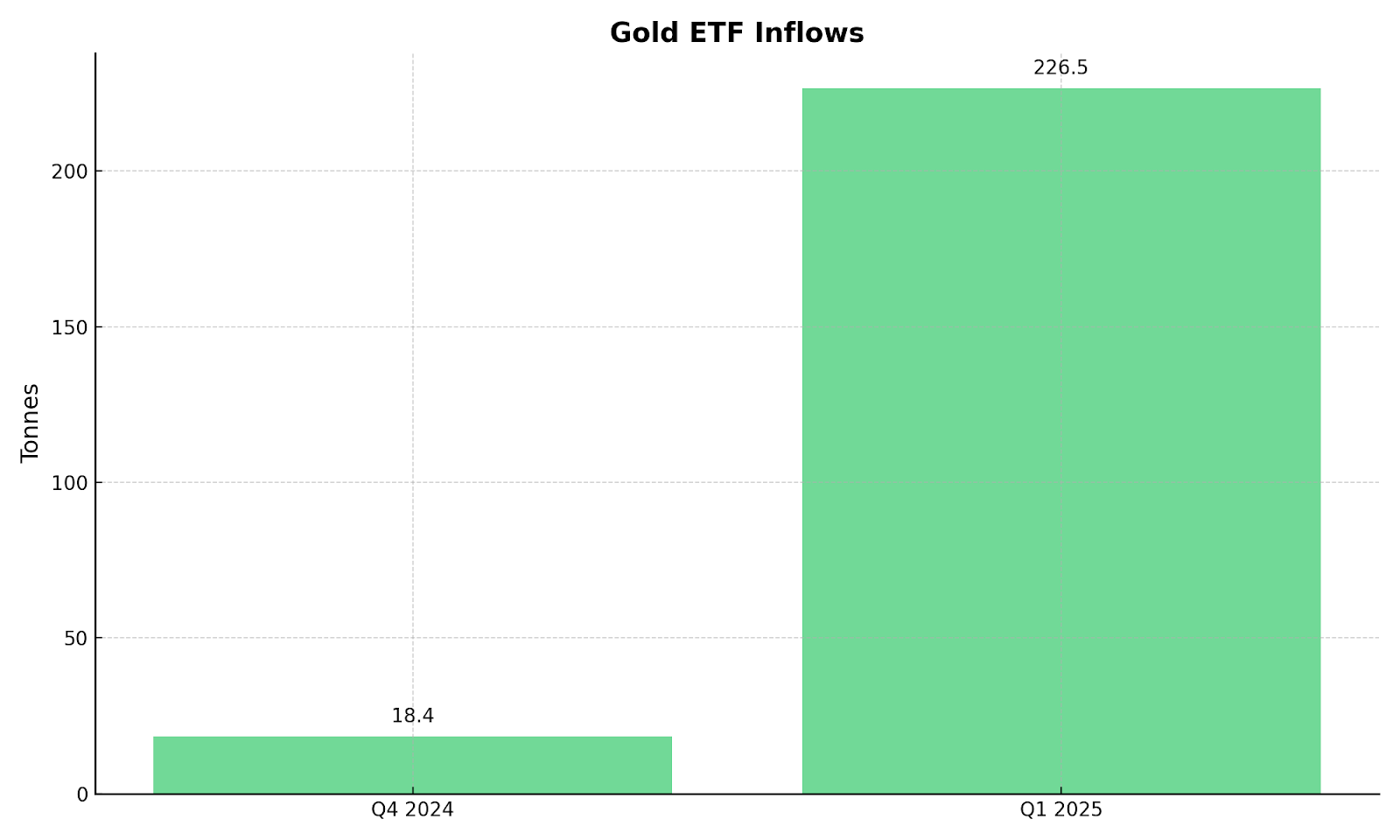

Gold ETFs & Institutional Inflows Returning

The first quarter of 2025 witnessed significant exchange-traded fund inflows totaling 226.5 tonnes, representing a 1,114% quarter-over-quarter increase. This dramatic shift indicates institutional and retail demand moving from defensive positioning to return-seeking strategies as monetary policy outlook becomes more accommodative.

Institutional investors are increasingly recognizing gold's role within diversified portfolios, particularly as correlation benefits become apparent during periods of equity market volatility. The combination of inflation hedging characteristics and potential monetary policy tailwinds creates a compelling allocation rationale for sophisticated investors.

Role of Central Banks as a Structural Demand Anchor

Central bank gold purchases are projected to reach 900 tonnes in 2025, maintaining consistency with purchasing patterns established since 2022. This demand component represents price-insensitive buying that helps absorb macro-driven volatility in gold markets.

Central bank accumulation reflects broader geopolitical considerations including reserve diversification and monetary system evolution. Unlike exchange-traded fund flows or retail investment demand, central bank purchases provide a structural floor for gold demand independent of short-term price movements.

Operational Readiness Strategies by Development Stage

Mining companies across different development stages are implementing distinct operational strategies that align with their capital availability and production timelines while positioning for Federal Reserve policy transitions.

Development Stage De-Risking Approaches: Development companies prioritize projects featuring oxide and saprolite ore bodies with minimal processing capital requirements. This approach enables rapid cash flow generation with reduced execution risk, particularly valuable during periods of monetary policy uncertainty.

Cabral Gold and New Found Gold exemplify this fast-cycle development approach within established mining jurisdictions. The strategic advantage involves adapting development timelines based on market conditions while preserving optionality for larger-scale operations.

Production Stage Operational Efficiency: Established producers focus on operational optimization and strategic expansion through brownfield development and selective acquisition activity. These companies leverage existing operational expertise and infrastructure to maintain cost discipline while scaling production.

Perseus Mining, i-80 Gold, Integra Resources, Serabi Gold, and West Red Lake Gold Mines demonstrate various approaches to production stage optimization, from multi-jurisdictional operations to specialized underground mining expertise.

Infrastructure & Jurisdiction as Valuation Drivers Across Stages

Both development and production stage companies benefit from strategic infrastructure utilization and jurisdictional selection, though the implementation varies by operational maturity.

Development Stage Infrastructure Strategy: Development companies leverage existing regional infrastructure to reduce capital requirements and accelerate development timelines. This approach proves particularly effective in established mining districts where processing facilities, power infrastructure, and skilled labor pools already exist.

Production Stage Infrastructure Optimization: Established producers utilize owned infrastructure to support brownfield expansion and acquisition integration. The ability to process ore from multiple sources through existing facilities creates operational synergies and capital efficiency advantages.

Managing Political & Permitting Risk Across Development Stages

Jurisdictional selection and permitting strategy represent critical factors for development timeline execution and operational cost management, with considerations varying between development and production stage companies.

North American Jurisdictions Lead on Regulatory Clarity

Development Stage Permitting Advantages: Canadian and US development companies benefit from established regulatory frameworks and predictable permitting timelines. New Found Gold's Newfoundland operations and Cabral Gold's strategic positioning demonstrate how development companies leverage jurisdictional stability for financing and development certainty.

Production Stage Operational Stability: Established producers including West Red Lake Gold, Integra Resources, and i-80 Gold operate within jurisdictions offering political stability and transparent regulatory processes. Federal permitting in the United States remains tied to National Environmental Policy Act reform, with Nevada and Idaho jurisdictions viewed as lower-risk pathways for operational expansion.

Select African Markets Reward Scale & Consistency

Perseus Mining leverages long-standing operations in Ghana and Côte d'Ivoire while expanding into Tanzania, demonstrating how operational trust with host governments facilitates new project approvals. The key success factor involves building sustained partnerships that align company development with local economic priorities.

Scale advantages become particularly relevant in African jurisdictions where government relationships and community engagement require consistent long-term commitment. Companies with established operational presence can more effectively navigate regulatory requirements and secure development approvals.

The Investment Thesis for Gold in a Fed-Transition Environment

The convergence of monetary policy evolution, sustained high gold prices, and operational innovation creates multiple investment rationales across the gold mining value chain. Strategic positioning now favors companies that combine jurisdictional advantages with capital discipline and operational flexibility.

- Margin compression resilience enables gold developers and producers to maintain profitability even with elevated all-in sustaining costs due to strong price floors above $3,000 per ounce

- Low capital expenditure, high internal rate of return projects like Cabral Gold and New Found Gold offer substantial value creation potential with minimal dilution risk through phased development strategies

- Operational optionality through toll milling arrangements, existing infrastructure utilization, and modular development approaches provides flexible response capabilities to price movements and market conditions

- Geopolitical alignment within Tier-1 jurisdictions including Nevada, Ontario, and Brazil delivers regulatory clarity and fiscal stability that reduces development execution risk

- Capital discipline supported by strong balance sheets and dynamic hedging strategies reduces external financing requirements while enhancing return potential for shareholders

- Central bank demand anchoring provides structural price support independent of exchange-traded fund flows or retail investor sentiment

- Real yield compression expectations as Federal Reserve monetary policy transitions create favorable conditions for gold price appreciation and mining sector outperformance

As the Federal Reserve enters a transition phase toward monetary easing, investor attention is recalibrating from timing interest rate cuts to assessing optimal asset class exposures within portfolios. Gold's repricing amid real yield compression expectations, US dollar weakness, and rising global demand positions the precious metal favorably for sustained institutional allocation.

For mining sector investors, the strategic shift emphasizes operational optionality and capital resilience rather than simply resource size or exploration potential. Developers and producers that successfully align capital expenditure requirements, jurisdictional exposure, and self-funded growth strategies are positioned to outperform during this monetary policy transition period.

The integration of phased development approaches, infrastructure leverage, and margin discipline creates a compelling investment framework for gold mining exposure. As macro headwinds evolve into strategic catalysts, institutional interest is expected to continue across the gold value chain, particularly for companies demonstrating operational excellence within established mining jurisdictions.

Analyst's Notes

Subscribe to Our Channel

Stay Informed