Iran Conflict & Western Uranium Supply Constraints Drive Long-Term Nuclear Fuel Deficits

Iran war energy shock elevates nuclear to national security priority, exposing Western uranium supply gaps as demand outpaces production through 2040.

- The Iran war triggered the largest oil supply disruption since the 1970s, and IEA Executive Director Fatih Birol stated at the 2026 World Economic Forum that energy security should be elevated to the level of national security, accelerating civilian nuclear adoption across energy-insecure Western nations.

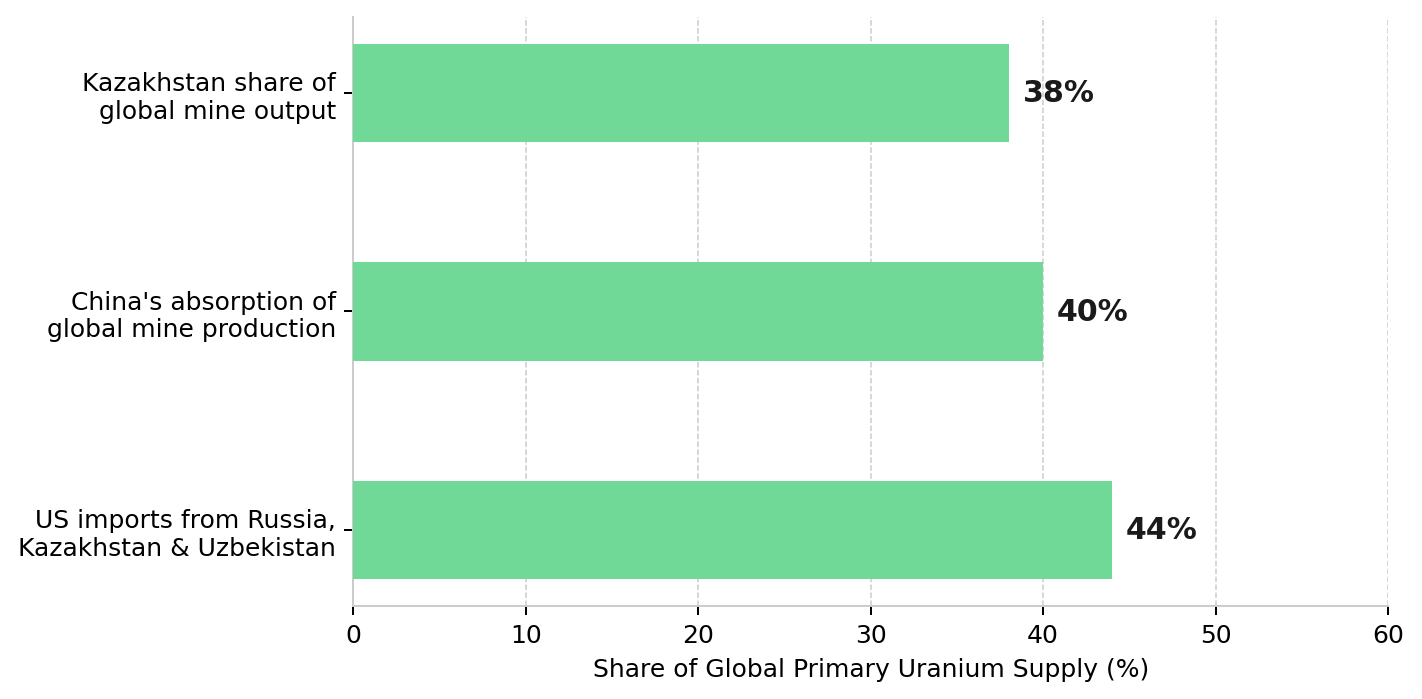

- China absorbed approximately 70 million pounds of uranium in the most recent reporting period, roughly 40% of global primary mine production, while Russian transit route uncertainty reduces the pool of material reliably available to Western utilities in a market where mine output already falls short of reactor demand.

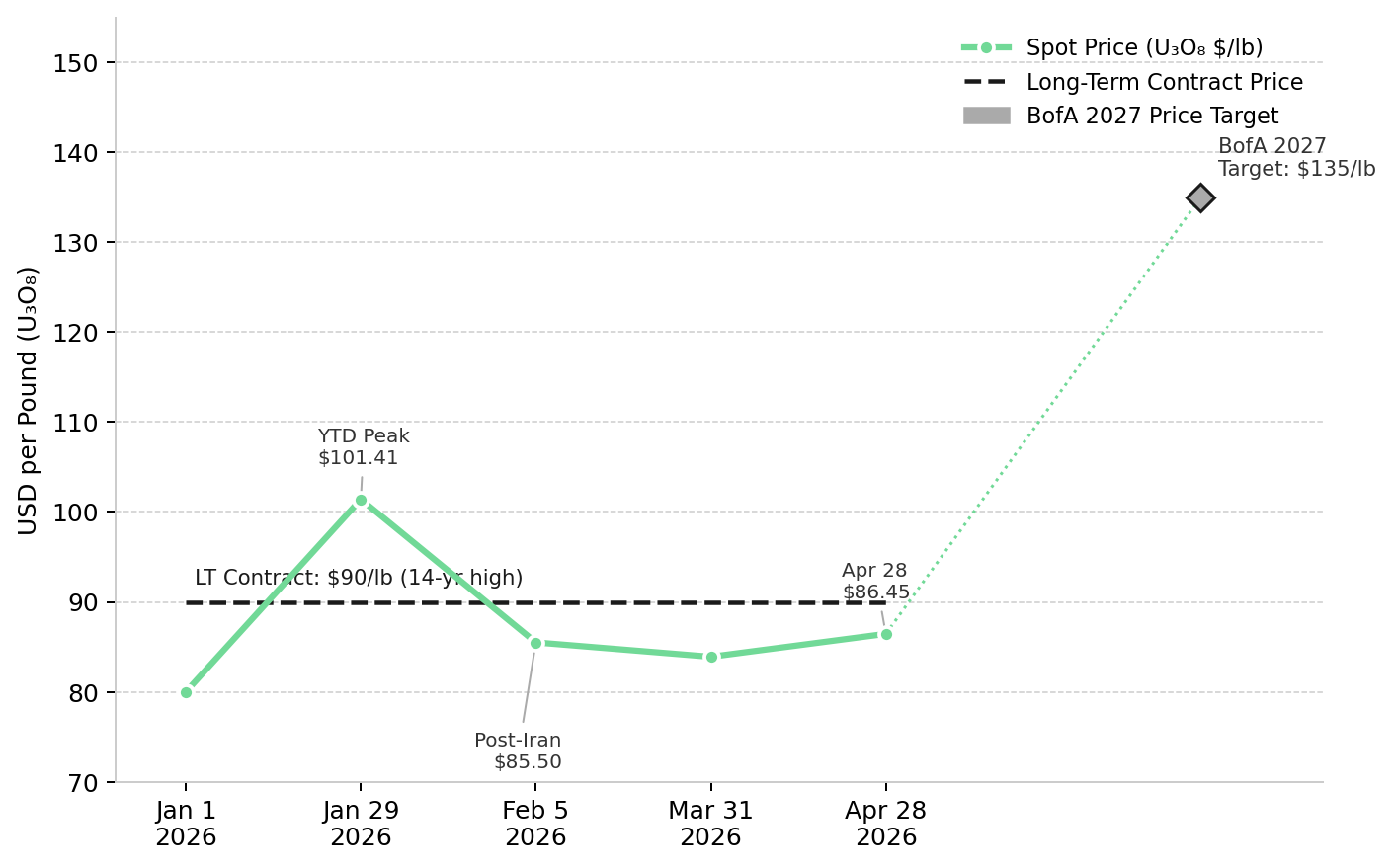

- The uranium spot price held at USD 86.45 per pound as of April 28, 2026 against a long-term contract price of USD 90 per pound, a 14-year high, while Bank of America issued a USD 135 per pound target for 2027, signaling institutional pricing of a fundamental, long-term valuation increase.

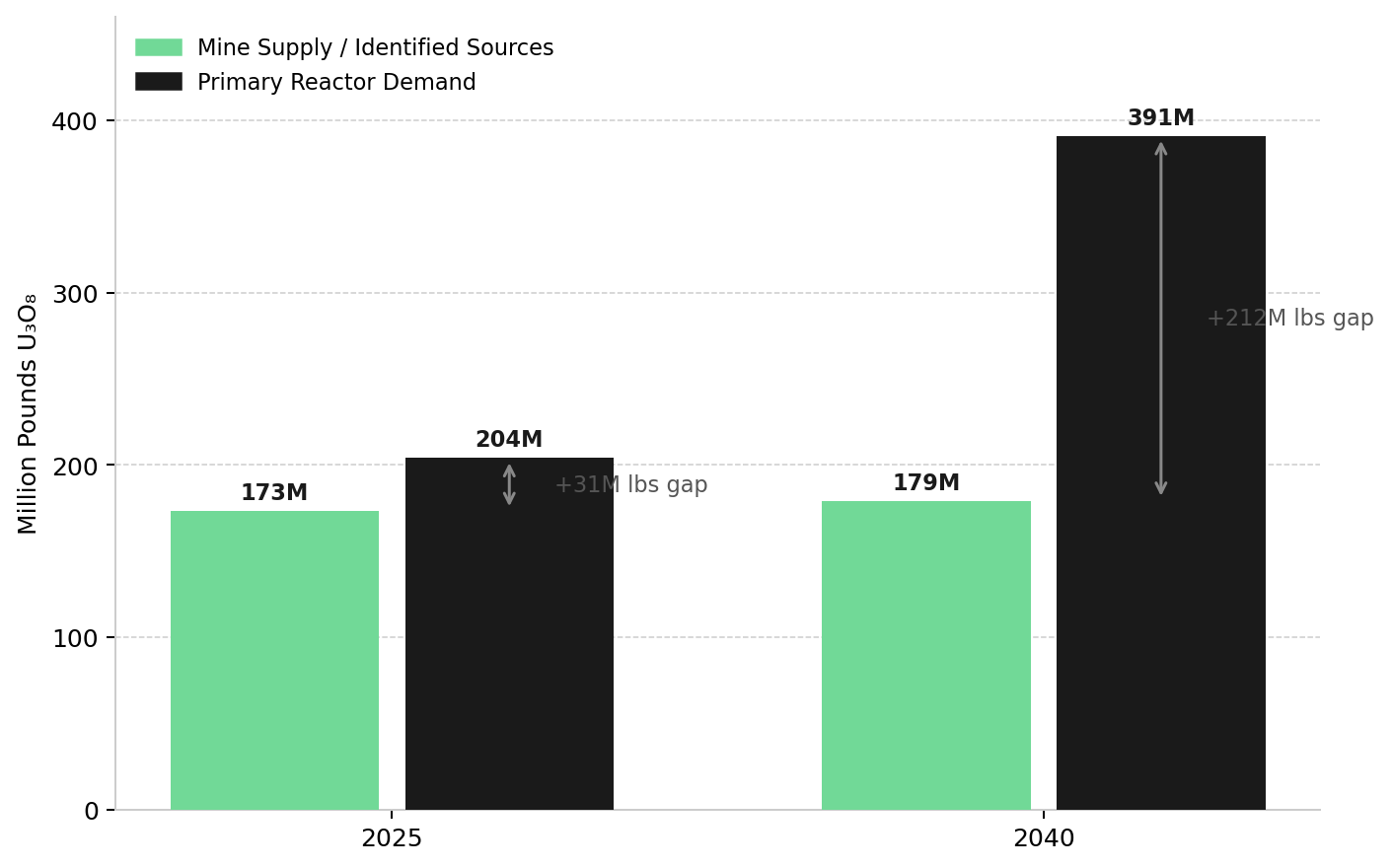

- With uranium mine development requiring 7 to 12 years from discovery to production, capital deployed in exploration and development in 2026 is the primary mechanism through which the World Nuclear Association's projected 212-million-pound annual supply gap by 2040 can begin to be addressed.

- Active US producers, advanced Canadian and African developers, and discovery-stage explorers are positioned across the uranium supply curve where Western capital allocation is most urgently needed, each carrying distinct risk-adjusted return profiles tied to the same demand driver.

In the spring of 2026, the uranium market is being shaped by a force that has nothing to do with mine grades or enrichment contracts. The US and Israel's coordinated strikes on Iran in late February, and the subsequent closure of the Strait of Hormuz, delivered the most severe oil and gas supply disruption in over fifty years, forcing energy policy out of bureaucratic planning and into the realm of national security strategy.

IEA Executive Director Fatih Birol, speaking at the 2026 World Economic Forum, stated that energy security should be elevated to the level of national security. Nuclear power has moved from a climate policy instrument to a strategic infrastructure imperative, with direct investment implications across the uranium supply curve.

Iran Conflict Accelerates Nuclear Energy Security Policy

The strategic relevance of the Iran war to uranium markets demonstrated at scale the systemic vulnerability of fossil-fuel-dependent energy systems to regional conflict. The Strait of Hormuz closure disrupted approximately 20% of global seaborne oil flows, triggering emergency supply diversification reviews in energy ministries across Europe, East Asia, and the Gulf Cooperation Council.

South Korea accelerated reactor restart approvals. Germany advanced its planning timeline for new nuclear capacity. Saudi Arabia reportedly conditioned its ceasefire mediation on US agreement to domestic uranium enrichment rights, with material long-term implications for regional nuclear demand. Concurrently, the Sprott Physical Uranium Trust purchased more than 5 million pounds of uranium in the first quarter of 2026 following more than USD 386 million raised in the first 28 days of the year, as institutional allocators repositioned ahead of a demand inflection.

The 11th Nuclear Non-Proliferation Treaty Review Conference, which opened at United Nations Headquarters on April 27, 2026, reinforces that backdrop. UN Secretary-General Antonio Guterres acknowledged that hard-won norms are eroding among nuclear states. For uranium investors, that erosion is a demand signal: when states perceive the post-Cold War security order as unreliable, nuclear power, which delivers decades of baseload capacity from a modest fuel stockpile, becomes the primary instrument of energy independence.

Western Uranium Supply Cannot Meet Accelerating Reactor Demand

The demand acceleration triggered by the Iran war is colliding with a Western uranium supply chain that is fundamentally underprepared. The US imports approximately 44% of its uranium from Russia, Kazakhstan, and Uzbekistan, a concentration the US Energy Information Administration identifies as a national security vulnerability. The Prohibiting Russian Uranium Imports Act, signed in May 2024, removes Russian-origin material from the US supply chain by January 1, 2028, tightening the available pool of Western-aligned uranium precisely as demand accelerates.

China imported approximately 70 million pounds of uranium in the most recent reporting period, equivalent to roughly 40% of global primary mine production, per Investing News Network's first-quarter 2026 uranium price review. Kazakhstan, which contributed approximately 38% of global mine output in 2024 per the World Nuclear Association, exports material via Russian transit routes carrying increasing logistical risk under ongoing Western sanctions. The result is a pool of Western-aligned uranium that is smaller than headline production figures suggest.

US Uranium Producers Benefit From Energy Security Prioritization

Energy Fuels Inc. produced 1.72 million pounds in 2025, beating its own revised guidance, and is targeting 2.0 to 2.5 million pounds in 2026. Production costs at the Pinyon Plain Mine in Arizona of USD 23 to USD 30 per pound against a spot price of approximately USD 86.45 per pound generate a wide operating margin directly funding the company's rare earth oxide expansion targeting commercial production by mid-2027.

Mark S. Chalmers, President and Chief Executive Officer of Energy Fuels, quantifies the financial link between uranium margins and the company's integrated critical minerals buildout:

"Our costs at Pinyon Plain are between $23 to $30 per pound, if you're selling at $75 a pound plus, you've got a really nice margin. If you multiply that times a million and a half pounds or two million pounds, that's a lot of cash coming into the company while we do these other steps."

ISR Mining & Permitting Advantages

enCore Energy Corp’s In-situ recovery carries average capital expenditure of less than 15% of conventional hard-rock uranium mining, and the company retains more than 50% of planned production through 2033 for spot market exposure.

William M. Sheriff, Executive Chairman and Founder of enCore Energy, draws a direct contrast between in-situ recovery and legacy uranium extraction:

"Uranium mining now in terms of in-situ is not your predecessor's uranium. It's as different as day and night. Being so environmentally friendly and so short term, short timeline, short cost to reclaim, it's a completely different chapter and new ball game."

Mine Permitting Timelines Limit the Uranium Supply Response

A new uranium mine typically requires 7 to 12 years of permitting, feasibility work, construction, and commissioning. The World Nuclear Association’s 2025 Report projects a supply gap of 212 million pounds per year by 2040 against all currently identified mine sources. That deficit cannot be closed by assets not yet discovered, permitted, or funded, making capital deployed in drill programs and feasibility studies in 2026 directly determinative of whether the mid-2030s supply position is manageable or critical.

Athabasca Basin Uranium Projects Benefit From Grade & Infrastructure Advantages

IsoEnergy Ltd. holds the highest-grade published uranium resource in Canada: the Hurricane deposit in Saskatchewan's Athabasca Basin, containing 48.6 million pounds at 34.5% U3O8 confirmed under National Instrument 43-101. The global average operating uranium mine grade is below 1%; Hurricane exceeds that benchmark by more than 30 times. The deposit sits at workable depth with no overlying water body, 40 kilometers from an already-licensed, operating processing facility. A 2026 winter drill program completed approximately 6,800 meters across 17 holes intersecting strong radioactivity along a newly identified fault zone, with laboratory assay results pending as a near-term re-rating catalyst.

Philip Williams, Chief Executive Officer and Director of IsoEnergy, describes what a recent equity raise reveals about the depth of capital now entering the sector:

"We went out to raise $50 million. There was over 300 million in demand in that book. Over six times subscribed and it was a global set of institutional investors with very large appetites, very large checks looking to write very large checks into our company into the sector and names that were new names to our company."

District-Scale Uranium Exploration Expands Resource Growth Visibility

ATHA Energy Corp. controls 100% of the Angikuni Basin in southern Nunavut and holds 6.8 million acres across Canada's most prominent uranium basins. The 2025 program produced five new uranium showings, with the RIB North maiden drill hole intersecting 34.7 meters of composite mineralization at a peak grade of 8.16% U3O8 over 0.5 meters, more than eight times the company's own high-grade threshold. A CAD 63 million treasury closed in February 2026 funds three simultaneous diamond drill rigs underway as of late April, targeting a trend mineralized over 12 kilometers of strike length.

Troy Boisjoli, Chief Executive Officer of ATHA Energy, draws a direct geological benchmark comparison to established Athabasca Basin deposits:

"We're seeing grades and thicknesses analogous to the Athabasca basin style mineralization, which was our thesis the whole time. We have mineralization over 12 km of strike length with the holes that we have tested and we have not missed yet. I've not seen a project like this through my time in the uranium space."

African Uranium Development Expands Western Supply Diversification

Atomic Eagle is advancing the Muntanga Uranium Project in Zambia, which holds 58.8 million pounds at 309 parts per million following a 24% resource upgrade in March 2026, alongside a confirmed probable ore reserve of 39.6 million pounds. The project uses an acid heap-leach process with recoveries exceeding 90% and approximately 20 kilograms of acid per tonne of ore treated, parameters directly comparable to Bannerman Energy's Etango project in Namibia, which received a strategic valuation of approximately AUD 1 billion in early 2025. The company's 30,000-meter 2026 drill program commenced April 28, 2026, targeting infill and maiden drilling across a property not explored since 2007.

Phil Hoskins, Chief Executive Officer of Atomic Eagle, explains the capital efficiency rationale for scaling the resource base ahead of committing to a revised production schedule:

"Our strategy is to grow the resource to underpin a significantly larger mining operation than that contemplated in the previous Feasibility Study. Bannerman's capex is 20% higher for a plant throughput that's more than twice as large. So you can have large improvements in production for modest increases in capital."

The Investment Thesis for Uranium

- IEA nuclear investment is projected to rise from approximately USD 65 billion annually today to USD 120 billion by 2030 under its Announced Pledges Scenario, and the Iran war has converted nuclear from a climate policy preference into a national security imperative, with governments across Europe, Asia, and the Gulf acting on that reclassification through concrete policy steps.

- World uranium mine production of approximately 173 million pounds in 2025 fell short of 204 million pounds of primary reactor demand per the World Nuclear Association Nuclear Fuel Report 2025, and the projected 212-million-pound annual supply gap by 2040 cannot be corrected by price signals alone given mine development timelines of 7 to 12 years from discovery to first commercial output.

- The Prohibiting Russian Uranium Imports Act, Chinese strategic buying absorbing approximately 40% of global primary mine output, and Russian transit route uncertainty for Kazakhstani material have reduced the pool of uranium accessible to Western utilities, creating a persistent price premium for domestically produced and allied-nation uranium independent of spot price cyclicality.

- Active producers operating in the US are direct beneficiaries of that supply chain reclassification, with current per-pound operating margins at domestic mines materially above production cost levels, long-term utility supply contracts providing revenue visibility through 2032, and the in-situ recovery method supporting accelerated permitting acceptance in states prioritizing domestic uranium output.

- Uranium developers advancing high-grade, permitted assets in top-tier jurisdictions, including Canada's Athabasca Basin, the US, and established African mining regions, represent the primary mechanism through which the projected 2040 deficit can be addressed, with current drill results, preliminary economic assessments, and bulk sample metallurgical programs directly informing the supply curve of the mid-2030s.

- The institutional investor base for uranium has broadened materially beyond dedicated commodity funds, as evidenced by recent equity raises attracting more than six times target demand from new institutional names, deepening the financing available for development-stage assets at precisely the moment such capital is most strategically necessary.

The uranium long-term contract price at a 14-year high of USD 90 per pound, alongside Bank of America's USD 135 per pound price target for 2027, reflects the institutional view that the current re-rating is supply-driven. The consequential question for investors is where, across the full spectrum from active US production through high-grade Athabasca Basin development to discovery-stage exploration in Nunavut and Africa, capital is positioned to capture the value that the energy security imperative is now permanently embedding in the uranium supply chain.

TL;DR

The Iran war converted nuclear power from a climate policy preference into a national security imperative, triggering accelerated reactor buildout across Europe, Asia, and the Gulf while exposing a Western uranium supply chain constrained by Russian import restrictions, Chinese procurement growth, and insufficient mine supply. China is buying approximately 40% of global primary mine output, Russian-origin material exits the US supply chain by January 2028, and world uranium mine production fell approximately 31 million pounds short of reactor demand in 2025 alone. With mine development requiring 7 to 12 years from discovery to production, the World Nuclear Association projects a 212-million-pound annual supply gap by 2040 that only capital deployed today in active production, advanced development, and discovery-stage exploration can begin to close.

FAQs (AI-Generated)

Iran's direct relevance to uranium supply is minimal. The market significance comes from the Strait of Hormuz closure disrupting approximately 20% of global seaborne oil flows, demonstrating in real time the vulnerability of fossil-fuel-dependent energy systems to regional conflict. That disruption is accelerating domestic nuclear buildout decisions across Europe, Asia, and the Gulf, translating into incremental uranium demand that was not priced into utility procurement schedules before the conflict began.

Three concurrent forces are compressing the pool of uranium reliably accessible to Western utilities. The Prohibiting Russian Uranium Imports Act removes Russian-origin material from the US supply chain by January 2028. China is absorbing approximately 40% of global primary mine output through strategic buying. Kazakhstan, which produces approximately 38% of global mine supply, exports material via Russian transit routes that carry increasing logistical and political risk under Western sanctions. These pressures cannot be corrected quickly because new uranium mines require 7 to 12 years from discovery to first commercial production, meaning the supply response to current price signals will not materialise at scale until the mid-2030s at the earliest.

World uranium mine production of approximately 173 million pounds in 2025 fell approximately 31 million pounds short of primary reactor demand of 204 million pounds, per the World Nuclear Association Nuclear Fuel Report 2025. The WNA projects that gap will widen to 212 million pounds annually by 2040 against all currently identified mine sources combined. Secondary supply sources, including inventory drawdowns and recycled material, are covering the near-term shortfall, but those sources are finite and are being drawn down at a pace the WNA expects to become unsustainable before 2030.

In-situ recovery, or ISR, is a uranium extraction method in which oxygenated water is injected underground to dissolve uranium in place and pump it to surface for processing, without physically excavating the orebody. It carries average capital expenditure of less than 15% of conventional hard-rock uranium mining, materially compressing the cost and time required to bring new production online. ISR operations also generate a significantly smaller surface disturbance footprint than open-pit or underground mining, which supports faster permitting acceptance in US states where regulatory agencies prioritise environmental impact minimisation in energy development approvals.

Three indicators suggest the current uranium re-rating is being driven by long-term supply constraints rather than short-term market sentiment. First, the uranium long-term contract price reached a 14-year high of USD 90 per pound as of April 2026, a level set by utility buyers with 10-plus year procurement horizons, not by short-term speculators. Second, Bank of America issued a USD 135 per pound price target for 2027, reflecting institutional modelling of demand growth that extends well beyond the current geopolitical cycle. Third, the supply gap identified by the World Nuclear Association is driven by physical production constraints, not sentiment, and those constraints cannot be resolved without a multi-year capital investment cycle in new mine development that has not yet been fully funded.

Analyst's Notes

Subscribe to Our Channel

Stay Informed