Lotus Resources (LOT) - Low Capex Uranium Focused on Production

Interview with Keith Bowes, Managing Director of Lotus Resources

Lotus Resources Ltd is an Australian-based minerals exploration and development company. The Company acquired their key asset, the Kayelekera Uranium Project in northern Malawi from Paladin Energy in March of last year.

The Kayelekera Uranium Project is a 157km2 tenement package with excellent exploration potential and hosts a high grade resource with an existing open pit mine and demonstrated excellent metallurgical recoveries.

We had a chance recently to speak with Keith Bowes, managing director at Lotus Resources. He shared with us some of the latest information about the company’s business with low-CAPEX uranium production in Malawi.

Overview of Lotus Resources

Lotus Resources Limited is an Australian-based minerals exploration and development company. The Company’s flagship asset is a 65% ownership of the Kayelekera Uranium Project, an open-pit mine located in northern Malawi, Africa. Lotus is in the process of increasing its stake in Kayelekera to 85%. In addition, the company is involved another project, the Hylea Cobalt Project, in New South Wales, Australia.

Management Team

The management team at Lotus is made up of Adam Kiley, Corporate Development; Chris Knee, CFO; Theo Keyter, Country Manager; Kobie Cilliers, Commercial and Project Administrator; John Mwenelupembe, Technical Supervisor; and Ronarld Kapira, Security Manager. Keith Bowes, Grant Davey, Mark Hanlon, and Michael Bowen serve as directors for Lotus.

Bowes’ Introductory Remarks

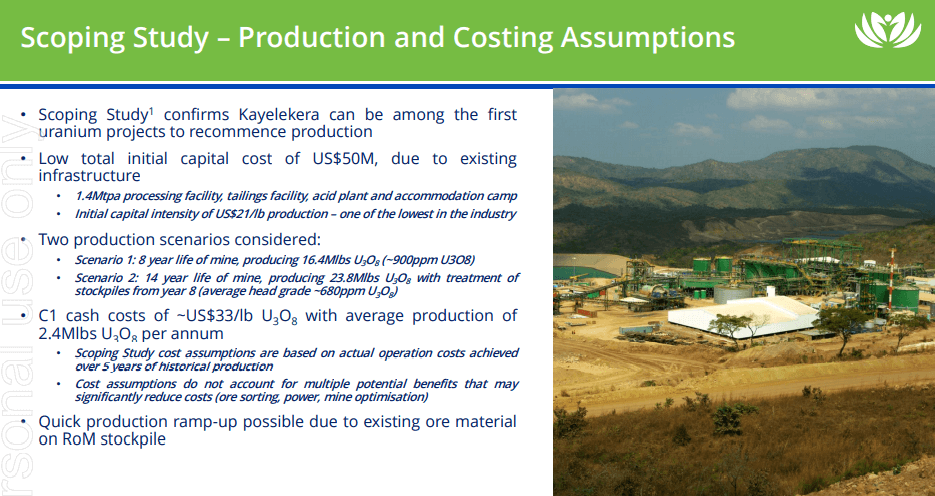

Lotus recently acquired the Kayelekera Uranium Project from Paladin Energy in 2020. The Kayelekera mine is currently non-operational but is on a care-and-maintenance schedule. Bowes told us that the company is undertaking several studies to determine the viability of restarting production at Kayelekera.

Kayelekera in Brief

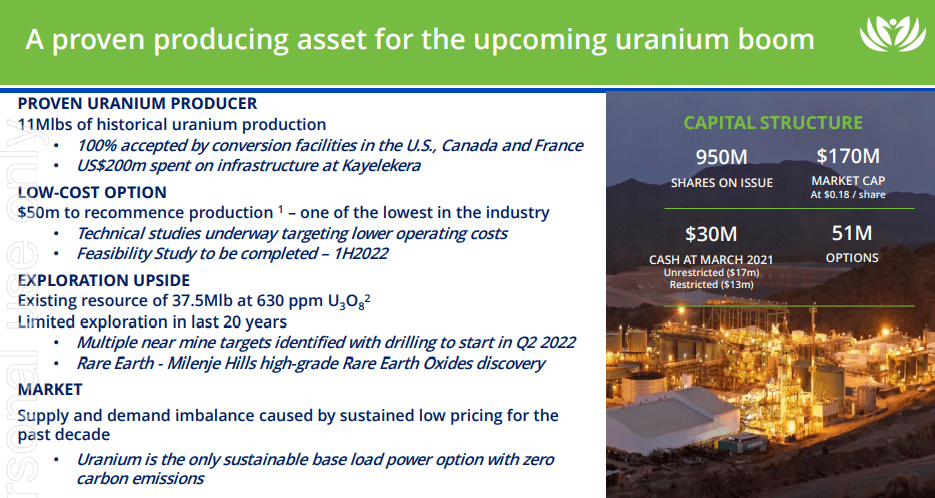

The Kayelekera Uranium Project is a 157km two-tenement package with excellent exploration potential and hosts high-grade uranium resource and has an existing open-pit mine. It produced nearly 11 M lbs. of uranium from 2009 until the mine was closed in 2014.

Recent OTC Listing

Since we last spoke with Bowes (be sure to check the Crux Investor write-up on the previous conversation), Lotus has gone through a successful IPO process. We asked him how the IPO went.

Very smoothly, he responded. But, he said, the heavier lifting will probably be with the upcoming marketing campaign they intend to pursue. They have appointed a broker over in Canada and a market maker in the US who are helping us to be introduced to a number of different funds. But overall, the OTC liftoff was great, he summarized.

The share price has bounced around a bit, he said. Perhaps there were some jitters in June with the reports of a leak at China’s Taishan nuclear plant, he mused.

Upcoming Rollup

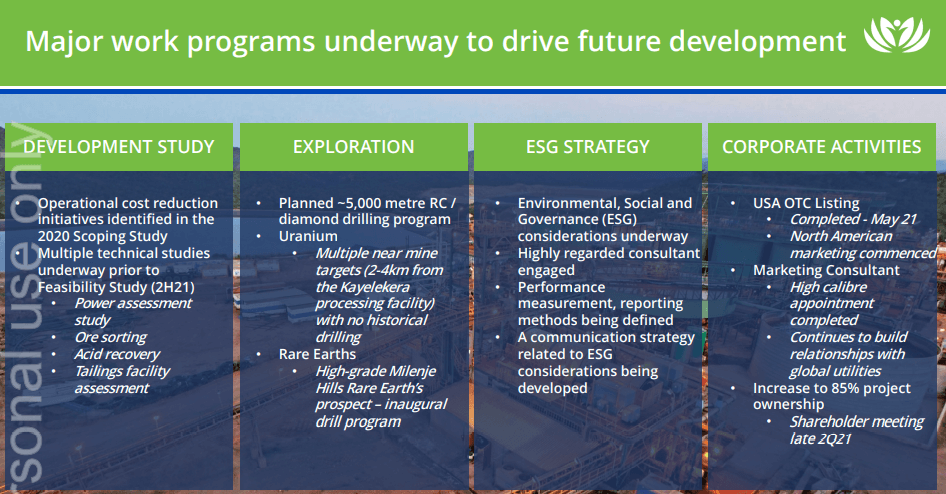

From there we spoke about Lutus’ upcoming plans for a rollup that would bring their total stake at Kayelekera up from 65% to 85%. They will soon have a shareholder meeting, when the rollup will be discussed and he doesn’t see any impediments coming out of that meeting.

We then asked him to explain how this rollup will be done. Michael Bowen and Mark Hanlon formed a subcommittee that was responsible for the rollup, Bowes told us. Lotus appointed an independent technical expert who performed a review of the potential rollup and assigned a value to it. This information was passed onto an independent company, BDO, the global accounting firm, who modeled potential share price behavior prior to and post rollup. This report, along with a summary of all points raised by the independent expert, will be supplied to the shareholders. We expect they will like what they see and approve the deal.

We wondered how independent these people are because, in fact, they are being paid by Lotus. Bowes could see a potential issue there, he said. He responded by saying that they are going to companies that do this type of thing as their regular job. BDO does this on a regular basis for a number of companies on the ASX. They are well known in the space in terms of being an independent reviewer. There's a fixed compensation agreed to up front, and as they state clearly in any documentation or agreements that they sign, and the result of the report is not dependent on these payments, said Bowes.

What Does the Rollup Do For Lotus?

Why is a rollup a good thing for Lotus, we wondered? Bowes suggested that it is a smart action to take from two perspectives:

1. If Lotus needs to raise money by taking on debt, they will have more leverage with a lender if they have an 85% versus a 65% interest in the project.

2. It also will play a role when Lotus gets into negotiations for offtake, because they’ll be negotiating on the largest percentage ownership (85%) allowed by the government (Malawi automatically takes 15%).

Hylea Cobalt Project

We moved on to Lotus’ other project, the Hylea Cobalt Project in Australia. Bowes told us that it was the original cobalt project that Lotus Resources held prior to the acquisition of the Kayelekera project. Upon acquiring Kayelekera, Hylea became non-core, he said.

Bowes told us that Lotus made a deal with an adjacent tenement holder, Australian CleanTech. Since Lotus had no intention to do anything with the asset, it was a very easy deal to do. Lotus retains some share exposure and collected US $1 M in the deal.

Kayelekera Marketing Update

We then moved back to Kayelekera and inquired about marketing efforts. Bowes told us that they have appointed Robert Rich, a New York-based marketing executive, who has been involved with the industry for decades and has worked with other Australian companies including BHP Billiton. He has expertise both in purchases and in sales in the uranium space.

Rich has initiated conversations with various utilities on behalf of Lotus as well. He is confident that all of Kayelekera’s production – expected to be somewhere between 2.5M to 3 M lbs./year, could effectively be sold to US utilities. He is currently putting together a detailed marketing plan to address this, Bowes told us. He’ll help uncover what type of contracts Lotus should look for, whether some yellowcake be reserved for the spot market, and other similar questions. Lotus is looking to establish contracts with companies such as ConverDyn, Cameco, and Orano, Bowes told us.

We asked if the marketing plan would become public once it is agreed upon. It hasn’t been discussed yet, said Bowes, but he envisions that at least part of it could be. He added that at a concept level, he’d be comfortable with sharing with the general marketplace how they intend to approach their marketing strategy.

Buying Physical Uranium as a Strategy?

Some companies have bees raising cash and buying physical uranium, we brought up. Have you considered that route, we asked? Bowes told us that they have not. The main reason, he said, is that Lotus doesn’t foresee the need to raise a particularly high amount of capital. If they envisioned that need, they may have taken that route.

One way or another, he said, everyone agrees that the price of uranium is going to go higher. One thing that he would consider, he shared, is purchasing call options on uranium, but these are “quite difficult to come buy”. They decided, said Bowes, that in the long run, if they're going to raise money they prefer to do other things with the money: Build a plant, conduct an exploration program, or develop a rare earth element (REE) option that they have in mind.

Technical Progress at Kayelekera Over the Last Few Months

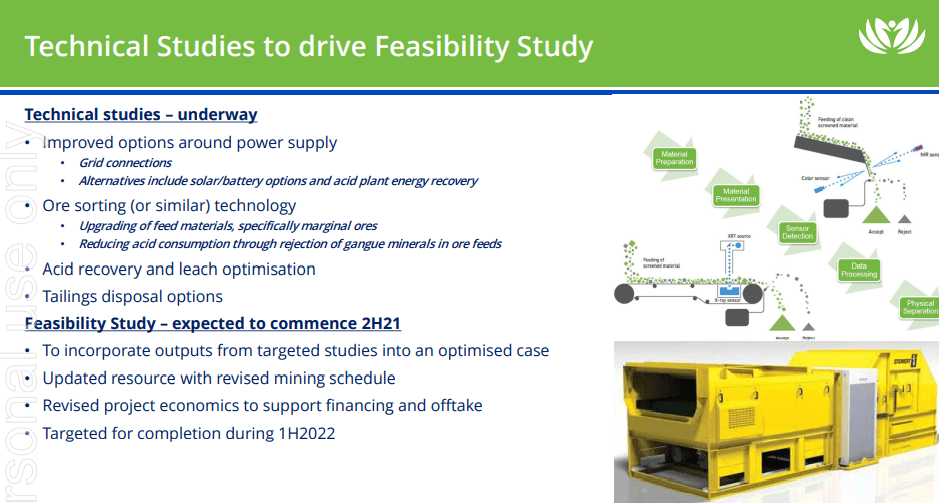

One technical issue that Lotus is working on at Kayelekera is an ore-sorter solution. Bowes told us that having an ore-sorting unit was deemed a key factor in managing their economics. Having an ore sorter can be huge, he indicated: For example, if they take a low-grade ore that has about 400 PPM of uranium in it, put that through an ore-sorting unit and increase the grade to 700-800 PPM ore, then feed that into the main plant, it becomes a lot more economic to process. In another example, having a sorting capability that removes high-calcite rock from the feedstock would reduce the acid costs tremendously, again improving economic results.

The ore sorter that they are looking at is a technologically advanced piece of equipment. It has two detectors: one for optics and another for x-rays, both running at the same time. Here’s an example, he said: A very high density material that picks up from the XRT detector, but happens to be light in colour, would be accepted by the XRT but rejected by the colour system. But because it's high density, we will be confident it has a high grade of uranium in it so we want it to be accepted. Again, if you look at the reverse, if you've got a dark material that would be accepted by the optical, but has a very low density, we don't want that because we don't think it has the uranium in it.

Energy supply to the Kayelekera site is also being addressed. The current power source on site is from diesel gensets. They are expensive and they leave a high carbon footprint. So they are looking for options. One is to connect to the national grid. Another is to use the heat generated from the sulfuric acid plant to run a steam turbine and generate power. Preliminary studies run by Auto Tech have suggested that this would be a low-cost solution. Finally, the company is also looking at a solar, wind and battery option as well. They will have the decision in hand within two or three months, he said.

Does Lotus Have Enough Cash?

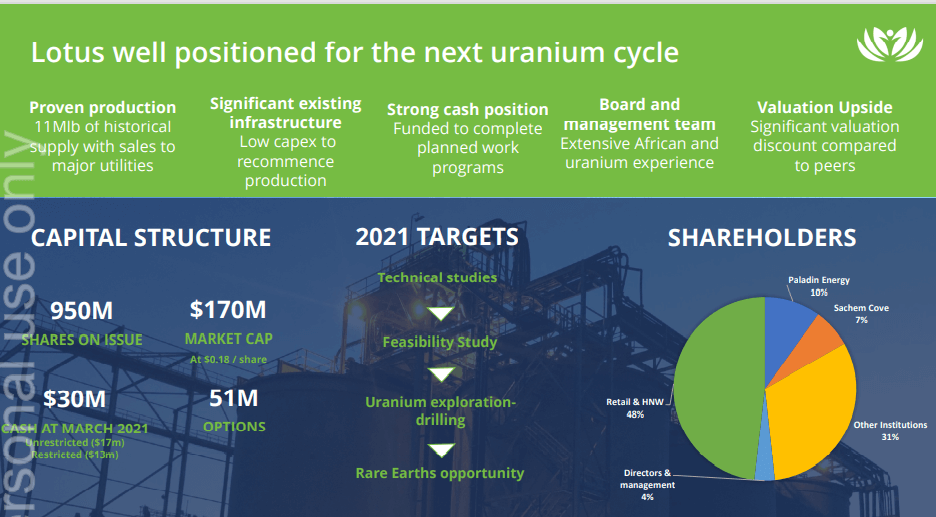

We moved on to the company’s cash position. Bowes told us that they have $16 M to $17 M of usable capital in the bank at the moment. Exercise of warrants and options could bring in another $5 M if needed.

The plan is to start a feasibility study soon. By the middle of 2022, they intend to have an updated feasibility study with refreshed cost estimates, including capital cost estimates. Whether that includes or excludes things like ore sorting, they would have made a decision by then.

After that, there will be the opportunity to open up discussions with banks. Again, there's always the proviso: what is the uranium price going to be at that point in time. They need to have a price that enables them to pull the trigger to start the mine back up again.

Exploration Synopsis at Kayelekera

Finally, we touched on Lotus Resource’s exploration plans. They intend to spend about $1 M to expand the size of the resource, starting at the perimeter of the open pit, where some extensions have been identified. Five anomalies several km from the pit have been identified as well and need to be explored, Bowes told us.

Additionally, they appear to have a REE anomaly about 2 km north of the open pit. They will explore this opportunity carefully, he shared.

Final Thoughts

Bowes closed out our chat by suggesting we keep tuning into company news releases over the next six months. Results on the ore sorting will be coming. Results on the power study should also be coming soon. Look for news about exploration and some updates around REE’s as well, he told us.

To find out more, go to the Lotus Resources Website

Analyst's Notes

Subscribe to Our Channel

Stay Informed