Marimaca Copper: MOD's Capital Profile, the Financing Process & Pampa Medina Exposure

Marimaca Copper's MOD project can be financed without a major mining partner, giving shareholders exposure to the Pampa Medina district at no additional cost.

- At US$587 million in pre-production capital expenditure, Marimaca Copper's MOD project sits in a category of copper development projects that can be financed without a major mining partner.

- Endeavour has been engaged to lead the financing process, with a primary mandate to minimise dilution for existing shareholders.

- At spot copper pricing, Marimaca Oxide Deposit (MOD) generates a net present value at an 8% discount rate (NPV8%) of US$1.1 billion, with Pampa Medina deposit exposure currently carried at no incremental cost to shareholders.

- Remaining sectoral permits are targeted for October 2026, with early pre-final investment decision site works expected to begin by the end of 2026 or early 2027.

- A 30,000-metre Pampa Medina delineation drill programme is expected to conclude by the end of September 2026, with a maiden inferred mineral resource estimate targeted for 2027.

The financing pathway for a copper development project is largely determined by its capital scale. Projects requiring several billion dollars to reach production face a structural constraint: lenders are unwilling to absorb that level of balance-sheet risk without a major mining company anchoring the structure. That dependency limits the field of available financing partners and shifts negotiating terms in favour of the financier. Marimaca Copper (TSX: MARI | ASX: MC2) occupies a different position.

MOD as a Standalone Development Project

Marimaca Oxide Deposit’s (MOD) capital profile defines the field of financing options available to the company. Pre-production capital of US$587 million, total life-of-mine capital of US$1,198 million, and a capital intensity of US$11,700 per tonne of annual copper production capacity each place MOD within the range of comparable North and South American projects, including El Pilar, Costa Fuego, Vizcachitas, Santa Cruz, and Santo Domingo.

Projects priced in the multi-billion-dollar range routinely require a major mining company to assume balance-sheet risk before commercial lenders engage. That structural requirement constrains partner optionality and limits what management can negotiate from an independent position. MOD's capital scale places it outside that category.

Chief Executive Officer of Marimaca Copper, Hayden Locke, describes the distinction directly:

"Copper is traditionally, if you look at the development projects, multi-billion dollar projects which are far too big for banks to take on that balance sheet risk without a major coming in and providing finance and assistance, whereas we are a standalone project that can be financed by ourselves, and so there's a huge number of groups that would like to be our financing partner."

Management points to a prior track record of raising US$300 million in capital markets as evidence of the company's self-financing capability. Current market conditions are described as supportive, with strong interest from a wide range of potential financing groups already engaged in the process.

The Financing Process & Dilution Objective

Endeavour has been brought in to assist management in evaluating financing options, with a primary mandate to minimise dilution for existing shareholders. Management describes the scope of that process as understanding "the art of the possible," covering a wide range of potential structures and partner types.

Marimaca enters the process from a position of financial strength. As of March 2026, the company held US$147.2 million in cash and carried no debt. That starting position removes the urgency that would otherwise narrow the field of viable financing structures and limit management's ability to assess the full range of options.

The existing shareholder register reflects established institutional support. Major shareholders include Assore (18.7%), Ithaki Limited (14.9%), Greenstone (6.4%), and Mitsubishi Corp. (3.4%). Those holdings define whose interests the Endeavour mandate is structured to protect, with the process focused on evaluating the full range of options to secure the best possible deal for existing shareholders.

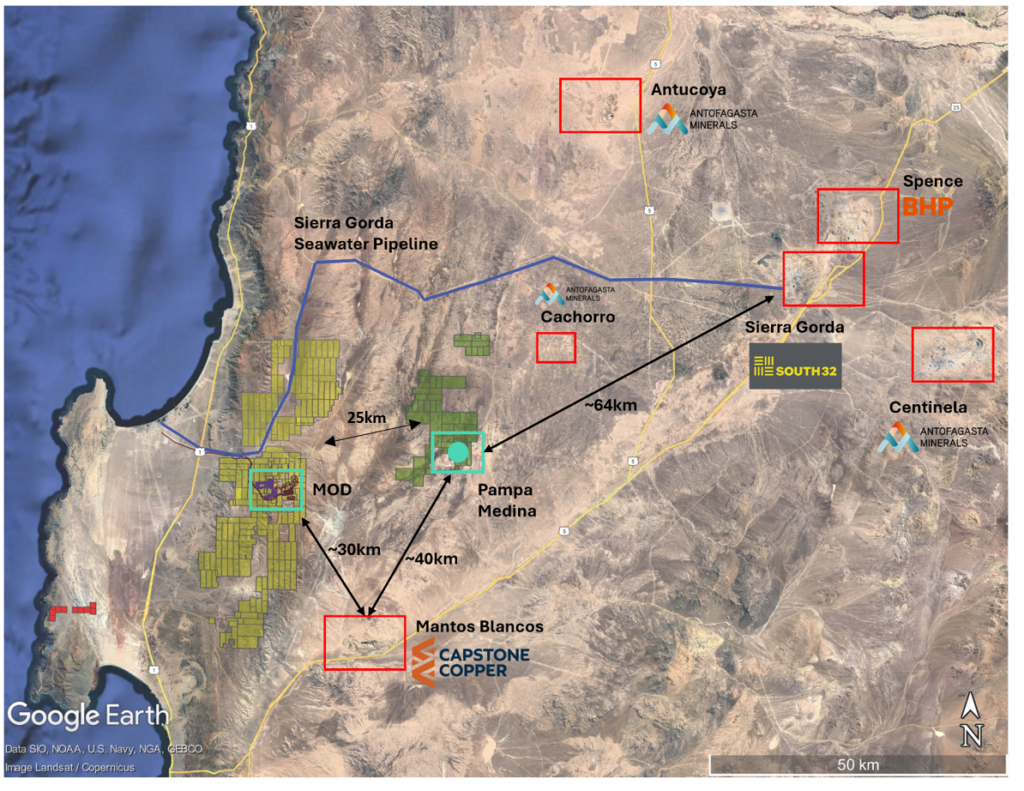

Pampa Medina Exposure & M&A Optionality

MOD's project economics form the foundation for the Pampa Medina argument. In a base case using US$4.30 per pound copper, MOD delivers a post-tax net present value at an 8% discount rate (NPV8%) of US$709 million, an internal rate of return (IRR) of 31%, and a capital payback period of 2.5 years. At spot copper pricing of US$5.05 per pound, the post-tax NPV8% reaches US$1.1 billion, the IRR increases to 39%, and payback compresses to 2.2 years. First 5-year all-in sustaining costs (AISC) average US$1.97 per pound and first 5-year C1 cash costs average US$1.45 per pound, with life-of-mine figures of US$2.29 and US$1.84 per pound, respectively. Average annual post-tax free cash flow over the first 5 years reaches US$222 million, while average annual earnings before interest, taxes, depreciation, and amortisation (EBITDA) over the same period are US$326 million.

Pampa Medina sits alongside MOD as a separate mineralised deposit with its own delineation programme now underway. Management's position is that the current enterprise valuation reflects MOD's economics without assigning independent value to the district.

Locke frames that gap in direct terms.

"We're trading at the value of the MOD, and you're effectively getting the stuff that we already know about, which is the Pampa Medina oxide opportunity, which we know full well can become an additional 25,000 tonnes a year of production. You're getting this world-class, potentially tier-one exploration opportunity for free. That's the kind of deal that I like."

The plan is to advance MOD to production, with the resulting cash flow funding concurrent exploration and definition of Pampa Medina's oxide and sulphide potential without relying solely on equity markets. As that delineation programme advances, the combination of a producing oxide operation and an emerging district-scale opportunity is characterised as highly attractive to major global copper producers. That outcome is explicitly conditional on successful tier-one delineation at Pampa Medina and on MOD's location in the low coastal cordillera.

Near-Term Catalysts & Timeline

With detailed design and engineering actively underway and long-lead items requiring more than 50 weeks for delivery being identified and secured, the company is targeting early pre-final investment decision (FID) site works before year-end.

Locke describes how the construction and financing tracks are expected to come together.

"Our intentions today are that we're deep into detail design and engineering, we're running our debt financing process, the objective is that at the end of this year, we're ready to start early pre-FID construction work, and we're starting to march our way towards an eventual FID when we're ready."

Remaining sectoral permits are targeted for completion by October 2026, a milestone that gates the commencement of early pre-FID site works expected to begin by the end of 2026 or early 2027. On the Pampa Medina side, a 30,000-metre delineation drill programme with 150-metre spacing is expected to conclude by the end of September 2026, with results released continuously following the resolution of earlier core-cutting delays. The 6 to 7 months of data compilation that follow are targeted to produce a maiden inferred mineral resource estimate for Pampa Medina in 2027.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed