Middle East Conflict and Higher Rates Are Repricing Platinum Group Metals

Middle East conflict and higher rates pressure PGMs, but tightening supply and low inventories highlight long-term upside in development-stage assets.

- Geopolitical escalation in the Middle East has transmitted an oil-driven inflation shock into global monetary policy, forcing a hawkish repricing that is suppressing near-term PGM prices through stronger real yields and USD appreciation.

- Platinum and palladium have declined sharply despite their historical safe-haven characteristics, confirming that real interest rate dynamics and dollar strength currently dominate commodity fundamentals.

- Structural supply constraints, including geographic concentration in South Africa and Russia, aging mine infrastructure, and above-ground platinum stocks providing less than five months of demand coverage, are compressing the long-term supply response capacity.

- Development-stage assets in alternative jurisdictions, particularly Brazil, are gaining institutional relevance as supply diversification becomes a strategic priority among PGM consumers and investors alike.

- The disconnect between macro-driven spot weakness and deteriorating long-term supply fundamentals is creating measurable valuation dislocations in development-stage PGM equities, with enterprise value per ounce multiples compressing despite unchanged or improving resource economics.

Middle East Conflict Is Reshaping Inflation Expectations & Commodity Pricing Dynamics

The escalation of geopolitical risk involving Iran and key Middle Eastern transit corridors has materially altered the global macro backdrop. The channel of transmission is direct: supply disruption risk in oil has pushed energy prices higher, reigniting consumer price inflation in economies where disinflation was still incomplete. This second-round inflation impulse is delaying the monetary easing cycles that PGM markets had priced in for 2025 and 2026.

The critical distinction from prior commodity supercycles is that inflation is no longer functioning as a uniform tailwind for hard assets. When inflation is supply-driven and geopolitically sourced, central banks face pressure to maintain or extend restrictive policy, which raises real yields and strengthens the US dollar, both of which are structural headwinds for non-yielding commodities including platinum and palladium. The result is a market in which the traditional inflation hedge narrative is being overridden by monetary policy mechanics.

Higher Real Rates & a Strong USD Are Driving Near-Term Weakness in PGMs

The dominant driver of recent PGM price weakness is the repricing of real interest rates, not deterioration in physical demand. Federal Reserve rate cuts that markets had anticipated for 2026 and 2027 have been largely removed from forward pricing. The European Central Bank and Bank of England have both signaled a potential tightening bias in response to persistent services inflation, and the US dollar has appreciated against a broad basket of currencies as a result.

For platinum and palladium, which generate no yield, the opportunity cost of holding these assets rises in direct proportion to real rate levels. Higher real yields reduce the present value of future price appreciation, compress speculative positioning, and prompt institutional reallocation toward short-duration fixed income. This transmission is visible in futures markets, where open interest has declined and net long positioning has been liquidated.

Transmission Mechanisms Into PGM Markets

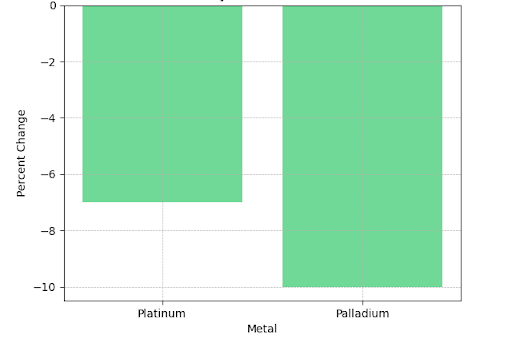

Platinum posted a weekly decline of approximately 6-8%, and palladium fell approximately 10-11%, moves that are disproportionate to any changes in auto catalyst demand, hydrogen fuel cell procurement, or physical inventory drawdown. The moves are consistent with macro factor exposure: elevated real yields, USD strength above key technical levels, and risk-off capital rotation.

These are cyclical headwinds, not structural impairments. The distinction matters because it informs whether current price levels represent fair value or a dislocation relative to long-run supply costs and demand drivers.

Structural Supply Constraints Are Tightening the Platinum Market Beyond Cyclical Forces

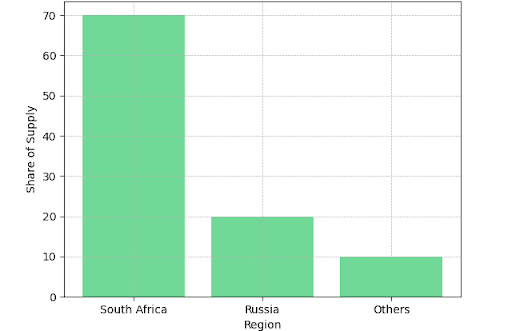

The macro overlay is masking a supply picture that has been deteriorating for years. Around 70% of global platinum supply comes from South Africa, where aging infrastructure, rising all-in sustaining costs, and limited reinvestment have constrained output. Russia remains the dominant palladium supplier. This geographic concentration creates a supply base highly sensitive to political and operational shocks, with limited ability to respond to rising demand.

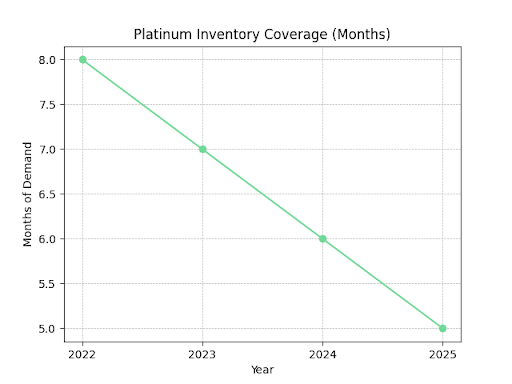

Above-ground platinum stocks are approximately 3.2 million ounces, representing less than five months of demand coverage. This buffer continues to decline as automotive demand, particularly from hybrids, remains resilient and emerging hydrogen fuel cell applications absorb supply.

Why Supply Response Is Structurally Delayed

New PGM mine supply cannot be brought online in response to price signals within a commercially relevant timeframe. Discovery-to-production timelines for underground hard-rock PGM operations consistently exceed ten years. Capital expenditure requirements for deep-level South African operations are substantial, and ESG-related financing constraints have reduced the pool of available project capital. Permitting complexity in key jurisdictions adds further lead time. The consequence is that incremental supply shocks carry disproportionate price impacts relative to what inventory levels alone would suggest, because replacement supply cannot arrive before physical deficits materialize.

Strategic Revaluation of Non-Traditional PGM Jurisdictions

The macro overlay is masking a supply picture that has been deteriorating for years. Around 70% of global platinum supply comes from South Africa, where aging infrastructure, rising all-in sustaining costs, and limited reinvestment have constrained output. Russia remains the dominant palladium supplier. This geographic concentration creates a supply base highly sensitive to political and operational shocks, with limited ability to respond to rising demand.

Above-ground platinum stocks are approximately 3.2 million ounces, representing less than five months of demand coverage. This buffer continues to decline as automotive demand, particularly from hybrids, remains resilient and emerging hydrogen fuel cell applications absorb supply.

ValOre Metals Corp. is advancing the Pedra Branca PGM project in northeastern Brazil, which hosts a 2.2 million ounce inferred resource at 1.08 grams per tonne, a mixed palladium-platinum deposit with approximately 60% palladium and 40% platinum. The project covers 50,000 hectares with an 80-kilometer mineralized trend, providing district-scale exploration upside beyond the defined resource.

Chief Executive Officer Nick Smart describes the asset's physical setting:

"Brazil, in many aspects, has a lot of what you’re looking for in terms of infrastructure. It also offers strong regulatory support. The country is actively seeking critical minerals projects, especially ones like ours, to move forward. We’re about four hours from the state capital, with a paved highway running virtually to the project site, and access to reliable electrical infrastructure"

Metallurgy, Project Economics & De-Risking as Key Valuation Drivers

In a structurally tight PGM market, development-stage valuation depends less on resource size and more on technical and economic de-risking. Investors focus on grade, resource classification (inferred to indicated), metallurgical recoveries, processing routes, and early economic indicators such as NPV sensitivity and AISC.

Near-surface, open-pittable mineralization offers a fundamentally lower-cost profile than deep underground operations. Lower strip ratios and simpler mining methods reduce capital intensity, accelerating the path to positive NPV under conservative price assumptions.

Economic Implications for ValOre Metals

ValOre's Pedra Branca project benefits from near-surface geometry and an active metallurgical program that has generated consistent recovery performance. The processing pathway combines flotation concentration with bioleaching, a relatively novel combination for PGE applications that ValOre holds the exclusive global rights to deploy.

Smart explains the economic significance of the metallurgical results:

“We’re fairly consistently seeing recoveries in the high 70s in terms of total metal recovery. With low-cost, near-surface mining and processing, we’d be in a strong range for project value. It opens the possibility of a low-cost operation, which, in my opinion, puts us in a very attractive position.”

High-70s recovery rates at surface-mineable depths position Pedra Branca favorably within the global PGM cost curve. The preliminary economic assessment being targeted for 2025 will quantify net present value, internal rate of return, and all-in sustaining cost assumptions, the milestones that determine whether a development-stage enterprise value per ounce multiple can re-rate toward producer comparables. Proprietary processing IP reduces the risk of technology replication by competitors and may provide a durable cost advantage as the project scales from demonstration plant to commercial production.

Market Dislocation vs Structural Opportunity

The PGM market is showing a clear disconnect between short-term macro-driven pricing and long-term fundamentals. Spot prices are being driven by monetary policy and USD strength, both cyclical, while underlying fundamentals, including declining inventories, constrained supply, and resilient demand from automotive and hydrogen sectors, continue to tighten.

This disconnect is compressing enterprise value per ounce multiples for development-stage equities, even as project economics remain stable or improve. This creates an opportunity to gain exposure to structural PGM supply deficits at valuations shaped by macro conditions that may not persist.

Positioning Implications

Institutional capital reacting to rate volatility is reducing short-term PGM exposure, creating entry opportunities for longer-term investors willing to take development risk. Re-rating in development-stage equities will be driven by two factors: commodity price recovery as macro conditions normalize, and project milestones, particularly PEA delivery, metallurgical validation, and resource upgrades. Both are trending positively.

A project producing 150,000-200,000 ounces annually in a supply-deficit market, with near-surface geometry and low-cost processing, could generate significant value relative to current valuations, assuming upcoming studies confirm the projected cost structure.

The Investment Thesis for Platinum Group Metals

- Supply deficits driven by declining South African output, aging mine infrastructure, and a global project pipeline insufficient to replace depleting reserves support a sustained long-term price floor above current spot levels.

- Geographic concentration of supply in South Africa and Russia creates a persistent geopolitical risk premium that is underpriced in current spot markets, particularly given the demonstrated sensitivity of palladium supply to Russian export policy.

- Alternative jurisdictions, particularly Brazil, offer investors access to large-scale PGM resources with improving regulatory frameworks, critical minerals policy support, and infrastructure profiles that reduce development execution risk.

- Development-stage assets with near-surface geometry and validated metallurgical recoveries offer all-in sustaining cost profiles that position them favorably within the global PGM cost curve, with preliminary economic assessment milestones providing near-term re-rating catalysts.

- Enterprise value per ounce compression in development-stage PGM equities, driven by macro-induced spot price weakness rather than project-level impairment, presents a risk-adjusted entry point with a 3-5 year investment horizon aligned with project development timelines.

- Demand resilience from automotive catalysts, particularly in hybrid vehicles, which continue to use platinum-group catalysts at rates comparable to internal combustion engines, and the emerging hydrogen fuel cell supply chain provides a multi-decade demand anchor independent of battery electric vehicle penetration rates.

- Proprietary processing technology secured through exclusive licensing agreements creates durable cost advantages and reduces technical replication risk for projects that have validated novel metallurgical approaches at the pilot scale.

The current weakness in platinum and palladium prices reflects monetary policy mechanics, not physical market deterioration. Higher real yields and a stronger US dollar have dominated PGM pricing in the near term, compressing spot prices and development-stage equity valuations in ways that are disconnected from the underlying supply-demand balance.

The structural reality is that PGM supply is geographically concentrated, capital-intensive to replace, and subject to development timelines that prevent rapid response to price signals. Above-ground inventory coverage below five months, declining South African output, and rising demand from hybrid automotive and hydrogen fuel cell applications are conditions that persist independent of any monetary policy cycle.

TL;DR

Platinum and palladium have declined sharply as oil-driven inflation from Middle East conflict forces central banks to delay rate cuts, strengthening the US dollar and raising real yields, both structural headwinds for non-yielding commodities. This macro repricing has masked a deteriorating supply picture: above-ground platinum stocks cover less than five months of demand, South African output is constrained by aging infrastructure and rising costs, and new project pipelines cannot respond within commercially relevant timelines. Development-stage assets in jurisdictions like Brazil, where ValOre Metals is advancing a 2.2 million ounce PGM resource with near-surface geometry and high-70s metallurgical recoveries, offer leveraged exposure to the structural supply deficit at valuations compressed by cyclical macro conditions rather than project-level impairment.

FAQs (AI-Generated)

Inflation that originates from oil supply disruptions, as seen in the current Middle East conflict scenario, forces central banks to maintain or extend restrictive monetary policy. This raises real interest rates and strengthens the US dollar, both of which increase the opportunity cost of holding non-yielding assets like platinum and palladium. The monetary policy response to inflation is currently overriding the traditional inflation hedge characteristics of precious and platinum group metals.

Above-ground platinum stocks stand at approximately 3.2 million ounces, representing less than five months of forward demand coverage. South Africa accounts for roughly 70% of global platinum production, and output from this base has been declining due to aging underground infrastructure, rising all-in sustaining costs, and limited capital reinvestment. New mine supply from discovery to production requires more than ten years, meaning the supply response to price signals cannot arrive before physical deficits materialize.

Brazil offers a combination of improving mining regulation, critical minerals policy support, and developed infrastructure that reduces execution risk for PGM development projects. The Brazilian government has explicitly prioritized critical minerals projects for advancement, and projects such as ValOre Metals' Pedra Branca, located approximately four hours from a state capital with paved highway access and established electrical infrastructure, benefit from lower logistics costs and more predictable permitting timelines relative to historically constrained jurisdictions.

Enterprise value per ounce measures a company's total enterprise value divided by its resource base in ounces. It functions as a valuation multiple that allows comparison between development-stage companies and producing peers. When spot prices fall due to macro factors without corresponding project-level impairment, EV/oz multiples compress, which can represent a dislocation between market pricing and intrinsic asset value. Preliminary economic assessment publication, resource upgrades, and metallurgical validation are the milestones that typically trigger EV/oz re-rating toward producer comparables.

Hydrogen fuel cells use platinum as a catalyst in the electrochemical reaction that generates electricity from hydrogen and oxygen. As hydrogen energy infrastructure scales, in transportation, industrial processes, and stationary power, platinum demand from this application is expected to grow materially alongside continued demand from hybrid automotive catalysts. This dual demand driver provides a long-term demand anchor for platinum that is independent of battery electric vehicle penetration rates, which is a common source of demand uncertainty in palladium market analysis.

Analyst's Notes

Subscribe to Our Channel

Stay Informed