Fed Policy Dissent & Russian Palladium Tariffs Reprice Platinum Group Metals Beyond the Automotive Cycle

Platinum and palladium markets are repricing as supply deficits, Russian disruptions, and hydrogen demand tighten global PGM supply.

- The World Platinum Investment Council confirmed a 1.1 million ounce platinum deficit in 2025 and projects a 240,000 ounce deficit in 2026, reducing above-ground inventories to approximately four months of demand cover and limiting the market's capacity to absorb additional supply disruption without further price escalation.

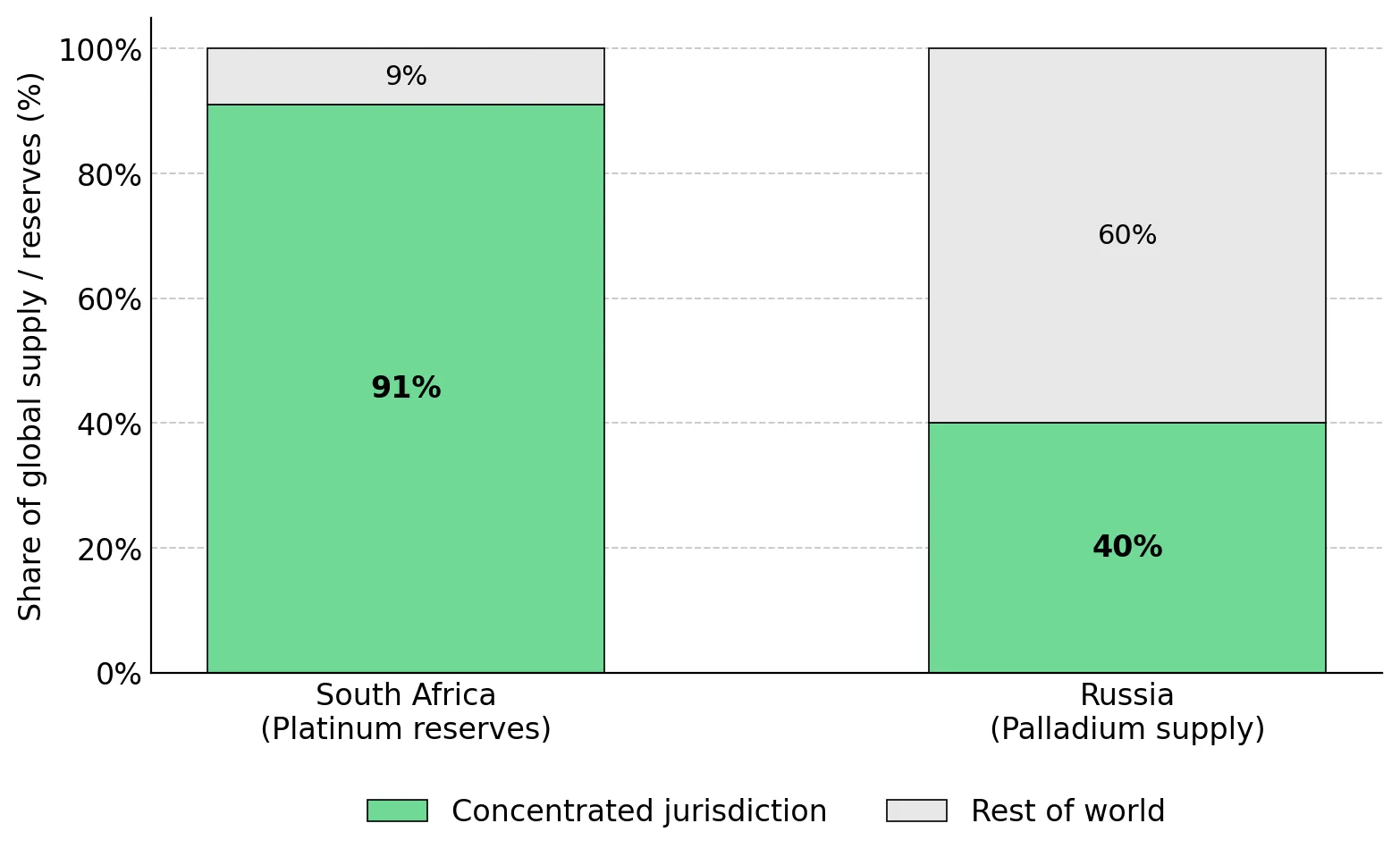

- Russia accounts for approximately 40% of global palladium supply, and the US Department of Commerce calculated a preliminary anti-dumping margin of approximately 828% on unworked Russian palladium imports, raising counterparty risk for Western refiners and industrial buyers and reshaping import economics for North American and European processors.

- Bank of America Global Research raised its 2026 platinum forecast to $2,450 per ounce from $1,825 per ounce in January 2026, citing persistent market deficits and the launch of physically-backed platinum and palladium futures contracts on China's Guangzhou Futures Exchange in the second half of 2025.

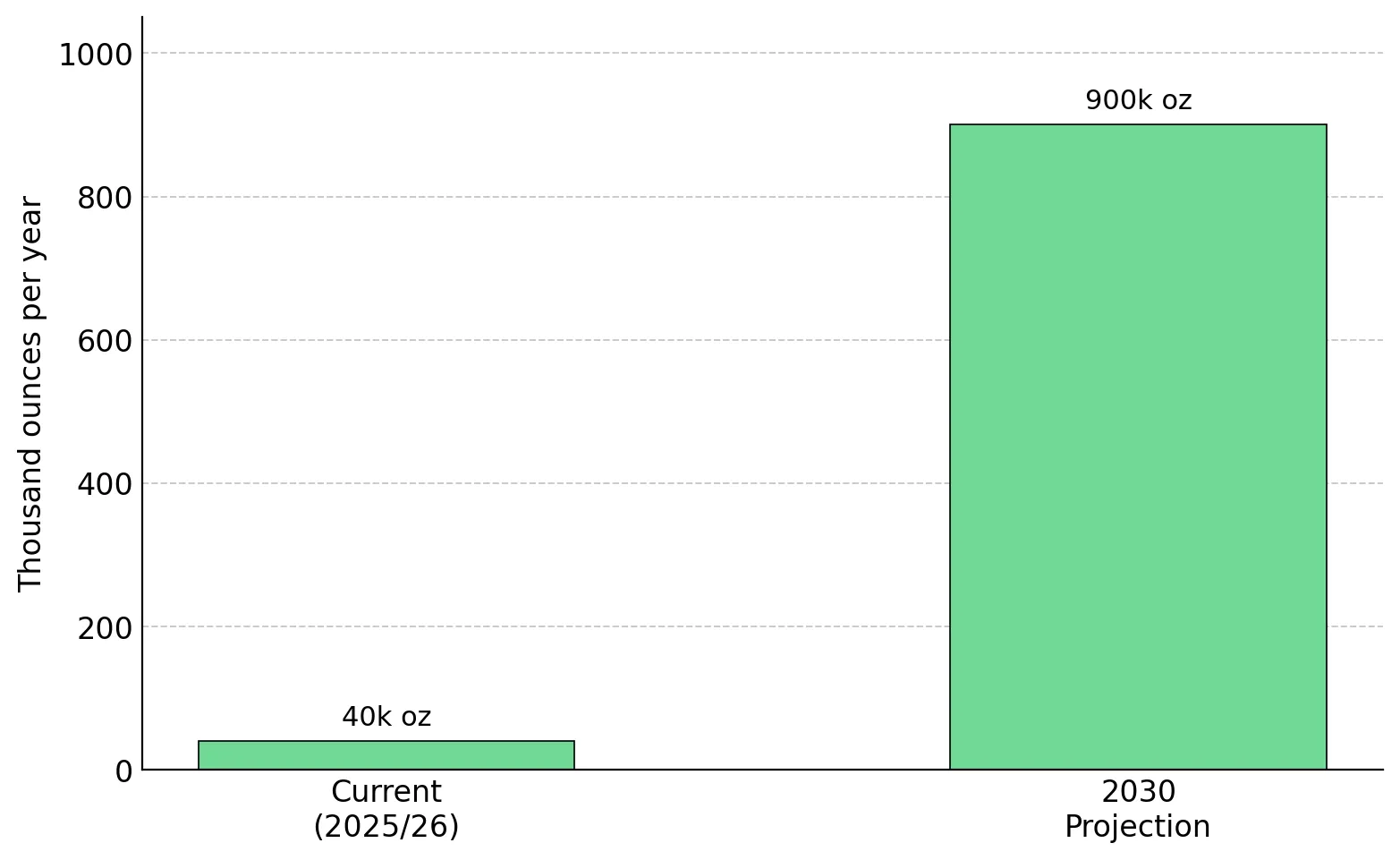

- Hydrogen-related platinum demand is targeting growth from approximately 40,000 ounces annually to approximately 900,000 ounces by 2030 according to World Platinum Investment Council projections, driven by proton exchange membrane fuel cell deployment in China, where 40,000 fuel cell electric vehicles and 574 refuelling stations were operational at the end of 2025.

- Junior developers with large-scale platinum group metals resources outside South Africa and Russia offer leveraged exposure to Western supply diversification financing and the deficit in platinum and palladium markets.

Platinum Deficits & Inventory Depletion Reprice PGMs as Strategic Scarcity Assets

Platinum and palladium historically traded as autocatalyst demand proxies tied to internal combustion engine production volumes. The investment framework changed in 2025 and 2026 because supply concentration deepened, above-ground inventories declined to approximately four months of demand cover, hydrogen demand became commercially relevant, and Western governments began deploying direct capital into critical mineral supply chains. The 2025 platinum spot rally of approximately 127% reflected the speed at which institutional investors repositioned around the deficit thesis once it became verifiable in supply-and-demand data.

Platinum reached approximately $2,878 per ounce in January 2026 before stabilizing near $2,000 per ounce by late April, while palladium gained 57% year-over-year to $1,469.50 per ounce by May 1, 2026. Bank of America Global Research lifted its 2026 platinum forecast to $2,450 per ounce from $1,825 per ounce in January 2026, citing persistent market deficits and dislocations from trade disputes keeping the market tight.

Federal Reserve Dissent & Strait of Hormuz Risk Reset Platinum Pricing in Late April

The April 2026 platinum price action reflected two distinct macro inputs hitting a market with limited inventory buffer. Federal Reserve policy uncertainty reduced opportunity costs for non-yielding assets, while Strait of Hormuz shipping risks raised input cost expectations for South African producers, simultaneously supporting prices and threatening the marginal cost curve. On May 6, 2026, platinum gained 3.4% to $2,020.05 per ounce and palladium rose 3.3% to $1,534.42 per ounce as US President Donald Trump cited progress toward an Iran negotiation, weakening the dollar against precious metals.

A Divided Federal Reserve Weakened the Dollar & Reopened Precious Metals Flows

Four dissents at the late-April Federal Open Market Committee meeting signaled internal policy support for an earlier rate cut, lowering Treasury yields and reducing the opportunity cost of holding non-yielding metals. Platinum advanced 5.72% to $2,003.30 per ounce in a single session on April 30, 2026, while palladium gained 5.24% to $1,556.70 per ounce.

Strait of Hormuz Disruption Reintroduced Energy Inflation Into Platinum Group Metals Pricing

South African deep-level platinum mines depend on diesel for haulage and on grid electricity priced largely against coal and oil-linked benchmarks, with approximately 60% of South Africa's diesel imports passing through the Strait of Hormuz. Sustained energy cost inflation compresses smelting margins and refinery economics, threatening the marginal portion of South African primary supply.

Nick Smart, Chief Executive Officer of ValOre Metals Corp., quantifies the cost trajectory facing existing producers:

“Electricity costs have increased by about 60% over the five-year period from 2021 to 2026. South Africa is also highly reliant on diesel imports, with approximately 60% of the country’s diesel supply passing through the Strait of Hormuz.”

Russian Supply Concentration and Western Procurement Shifts Are Repricing Non-Russian Palladium

Russia accounts for approximately 40% of global palladium supply, concentrated through Norilsk Nickel's Arctic operations. Norilsk Nickel reported a sharp first-quarter 2026 decline in primary metal output, tightening near-term spot supply, while a labor stoppage at Impala Platinum's Rustenburg operations during the same period removed additional South African ounces from the market. The US Department of Commerce calculated a preliminary anti-dumping margin of approximately 828% on unworked Russian palladium imports, following petitions filed by Sibanye-Stillwater and the United Steelworkers Union, materially raising the cost of Russian palladium for North American refiners and industrial buyers.

Palladium remains the dominant catalyst in gasoline autocatalysts, and hybrid vehicles use 10% to 20% more platinum group elements per vehicle than traditional internal combustion vehicles. Western original equipment manufacturers facing procurement diversification mandates now pay an implicit premium for non-Russian palladium ounces, raising the value of geographically diversified primary supply.

Western Governments Have Moved From Policy Statements to Capital Allocation

The Export-Import Bank of the US approved a $10 billion Direct Loan for Project Vault in February 2026, designed to establish a domestic reserve for critical minerals, and has issued $14.8 billion in Letters of Interest for critical minerals projects under the current administration. The US State Department hosted the 2026 Critical Minerals Ministerial in February 2026, bringing together representatives of 54 countries and the European Commission to coordinate Western supply chain responses.

Smart frames the implication for jurisdictional concentration:

“When you’ve got such a concentration within South Africa, Russia, and Zimbabwe, I think there’s going to be a realization of that, and a growing desire to diversify where those metals are coming from.”

China’s Hydrogen Buildout Is Establishing a Long-Term Industrial Demand Floor for Platinum

Platinum catalyzes the oxygen reduction reaction in proton exchange membrane fuel cells at current loading rates of 0.1 to 0.2 grams per kilowatt of output, with industry research targeting below 0.05 grams per kilowatt by 2030. Hydrogen-related platinum demand is projected by the World Platinum Investment Council to rise from approximately 40,000 ounces annually to approximately 900,000 ounces by 2030, representing approximately 11% of global platinum demand at the latter point.

China operated 40,000 fuel cell electric vehicles and 574 hydrogen refuelling stations at the end of 2025 and is targeting 100,000 fuel cell electric vehicles by 2030, with a cost reduction roadmap aimed at $3.50 per kilogram by 2030 from current end-user prices of approximately $4.80 per kilogram. The deployment volume directly translates to platinum consumption at current loading rates, providing a quantifiable demand floor for the metal independent of the automotive catalytic converter cycle.

Researchers at Washington University in St. Louis demonstrated a rhenium-molybdenum phosphide catalyst that sustained 2.0 amperes per square centimetre for more than 1,000 hours in an anion-exchange membrane electrolyser configuration in April 2026. Durability scaling, cold-start performance, and large-area manufacturing qualification still leave platinum commercially dominant in proton exchange membrane fuel cells through at least 2035 according to industry forecasts, supporting the demand-side leg of the deficit thesis through the next development cycle for advanced platinum group metals projects.

Supply Concentration & Capital Scarcity Are Limiting New Platinum Group Metals Production

Platinum group metals supply remains concentrated in jurisdictions where reinvestment economics have deteriorated. South Africa holds approximately 91% of global platinum reserves, primarily within the Bushveld Igneous Complex, while Russia dominates palladium output. Total platinum mine supply in 2025 fell 5% year-on-year to 5,510,000 ounces, running 10% below the pre-COVID five-year average according to the World Platinum Investment Council.

Replacement supply is limited because the South African reserve base requires deep underground development, the national grid faces reliability constraints, and labor disruptions at Impala Platinum and other major producers have constrained recent output.

Higher Prices Have Not Triggered an Equivalent Supply Response

The 2026 World Platinum Investment Council base case projects flat mine supply year-on-year, with the 2% supply lift attributable to a 10% increase in recycling rather than primary production.

Smart quantifies the practical constraint on bringing additional ounces to market:

“The primary mine production of platinum has been in decline over the last five years. In 2021, it peaked at just over 6 million ounces. The forecast for this year is around 5.5 million ounces of primary platinum production, and that’s in the context of a metal price that has doubled over the course of the last year.”

Western Supply Chain Security Concerns Are Repricing Non-South African PGM Projects

Investors are screening platinum group metals developers using a multi-factor framework that weights jurisdictional diversification, infrastructure access, metallurgical recovery, and resource scale. Brazil and Western Australia have emerged as alternative development jurisdictions because both offer grid power, port access, and permitting frameworks that have accommodated multiple recent mining developments outside the traditional South African and Russian supply corridors.

ValOre Metals Corp. operates the Pedra Branca platinum group metals project in Ceará State, Brazil, hosting a 2,198,000 ounce inferred two platinum group element plus gold resource across 63.3 million tonnes grading 1.08 grams per tonne, distributed across seven near-surface zones across 51,096 hectares per the company's March 8, 2022 National Instrument 43-101 technical report. Bioleaching test work conducted with the University of Cape Town demonstrated platinum and palladium extractions of 73% and 74% respectively, supporting a heap-leach development pathway with potentially lower capital intensity than conventional flotation circuits.

ValOre Metals Corp. carries a market capitalization of approximately C$26 million against 2,198,000 inferred ounces, implying enterprise value per inferred ounce of approximately C$12. The company is targeting a Preliminary Economic Assessment publication in the fourth quarter of 2026, which would establish base-case capital and operating cost guidance and provide a quantified development pathway. ValOre is a member of Discovery Group, whose member companies have collectively participated in more than C$2.6 billion in merger and acquisition transactions and raised more than $1 billion in equity since 2002, including the C$1.8 billion sale of Great Bear Resources in 2022.

The Investment Thesis for Platinum Group Metals

- Platinum deficits are now inventory-driven rather than demand-driven, with above-ground stocks at approximately four months of demand cover, reducing the market's capacity to absorb operational disruption without further price escalation.

- Russian palladium supply risk is repricing through tariff and anti-dumping mechanisms, with the US Department of Commerce calculating a preliminary 828% dumping margin that materially raises Russian palladium import costs for Western refiners and industrial buyers.

- Hydrogen infrastructure deployment is targeting a second demand curve for platinum that operates independently of the automotive cycle, with World Platinum Investment Council projections supporting 900,000 ounces of annual hydrogen-related demand by 2030.

- South African production constraints, including 60% electricity cost inflation since 2021 and Strait of Hormuz diesel exposure, limit near-term global supply elasticity despite Bank of America's $2,450 per ounce 2026 platinum forecast.

- Advanced developers in Western-aligned jurisdictions may receive valuation uplift through Export-Import Bank financing pathways and direct government equity participation, mirroring precedents already established in US rare earth and uranium sectors.

- Development-stage projects with large-scale inferred resources, near-surface mineralization, demonstrated metallurgical recovery, and favorable infrastructure access offer leveraged exposure to sustained higher platinum prices through cut-off grade flexibility and resource expansion potential.

Platinum and palladium pricing is no longer set primarily by automotive production volumes. The market is now repriced by Federal Reserve policy disagreement, Russian palladium supply disruption, hydrogen infrastructure deployment targeting 900,000 ounces of annual demand by 2030, and Western government capital deployment through the $10 billion Project Vault Direct Loan and the 2026 Critical Minerals Ministerial. Investors evaluating the sector are screening for which projects can deliver new Western-aligned platinum group metals supply within the next decade. That shift is repricing valuation frameworks for advanced exploration and development-stage companies with scalable inferred resources, demonstrated metallurgical recovery, and infrastructure access outside the concentrated South African and Russian supply corridors.

TL;DR

Platinum group metals are shifting from cyclical automotive commodities into scarcity assets driven by supply deficits, geopolitical supply risks, hydrogen infrastructure growth, and Western critical mineral policy support. Platinum inventories have fallen to roughly four months of demand cover while Russian palladium supply disruptions and anti-dumping measures are tightening Western procurement markets. At the same time, hydrogen fuel cell deployment, particularly in China, is creating a second long-term demand channel for platinum independent of the traditional automotive cycle. Investors are increasingly focusing on development-stage projects outside South Africa and Russia, especially those with scalable resources, favorable metallurgy, and infrastructure access that could supply Western-aligned critical mineral supply chains.

FAQs (AI-generated)

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed