Fourth Consecutive Platinum Deficit Creates Entry Points in Non-South African PGM Assets

WPIC’s fourth platinum deficit year and falling South African output are tightening supply, increasing focus on undervalued non-SA PGM developers.

- The World Platinum Investment Council confirmed a 1.082 million ounce platinum deficit in 2025, marking the fourth consecutive annual deficit since 2022 and reducing above-ground inventory to approximately four months of demand coverage.

- Total platinum mine supply in 2025 fell 5% year-over-year to 5.51 million ounces per WPIC, running 10% below the pre-COVID five-year average, with the 2026 base case projecting flat mine supply and a 2% lift attributable solely to a 10% increase in recycling.

- South African primary platinum output declined from approximately 5.3 million ounces in 2006 to approximately 3.9 million ounces in 2025 despite spot prices doubling year-over-year, with electricity costs rising 60% between 2021 and 2026 and 60% of South African diesel imports routed through the Strait of Hormuz.

- Bank of America Global Research raised its 2026 platinum forecast to $2,450 per ounce from $1,825 per ounce in January 2026, citing persistent market deficits and trade-related supply dislocations keeping the market structurally tight.

- Development-stage PGM equities outside South Africa with demonstrated bench-scale platinum and palladium extractions above 70% and Preliminary Economic Assessment timelines targeting late 2026 trade at material enterprise-value-per-ounce discounts to peers carrying comparable resource scale.

WPIC’s 1.082Moz Platinum Deficit & South African Output Decline Are Compressing Global Inventory Buffers

WPIC's most recent Platinum Quarterly report confirmed a 1.082 million ounce deficit in 2025, the deepest annual shortfall in WPIC data back to 2014, with a projected continued 240,000 ounce deficit in 2026. Four consecutive deficit years have reduced above-ground inventories to approximately four months of demand coverage, the threshold below which spot prices respond disproportionately to operational disruption rather than to demand variability.

WPIC Confirms 1.082Moz 2025 Deficit & Inventory Cover Falls Below Four-Month Threshold

The 2025 platinum deficit was driven by a contraction in primary supply combined with sustained industrial and investment demand. Total platinum mine supply fell 5% year-over-year to 5.51 million ounce, running 10% below the pre-COVID five-year average. WPIC projects deficits persisting through 2029 at an annual average of 348,000 to 689,000 ounces, narrowing only as recycling capacity expands rather than as primary mine output recovers.

Strong fourth-quarter 2025 investment demand was the single largest contributor to the deficit hitting its 1,082 thousand ounce record, with American Platinum Eagle and Canadian Platinum Maple volumes at their highest levels since 2008 and ETF flows turning net positive after multi-year stagnation. Above-ground stocks at approximately four months of demand cover sit below the operational threshold where short-cycle disruptions translate directly into spot price escalation, and the 2026 WPIC base case projects flat year-over-year mine supply with the only marginal 2% lift attributable to a 10% increase in recycling rather than to primary production growth.

Nick Smart, Chief Executive Officer of ValOre Metals, quantifies the supply contraction against the doubling platinum price:

“The primary mine production of platinum has been in decline over the last five years. In 2021, it peaked at just over 6 million ounces. The forecast for this year is around 5.5 million ounces of primary platinum production, and that’s in the context of a metal price that has doubled over the course of the last year. That tells you something about the inelasticity of supply and the difficulty of bringing new metal into the market.”

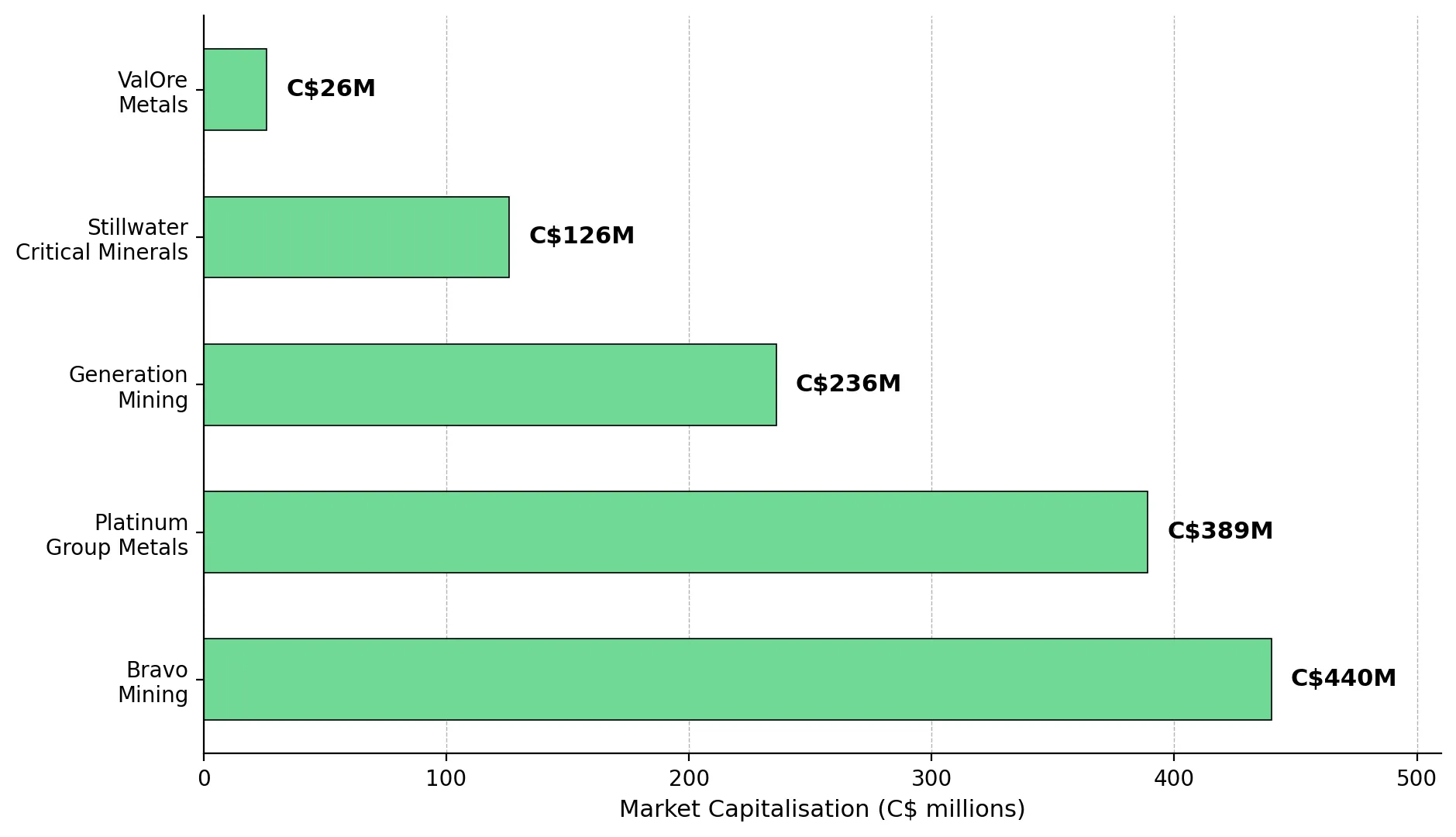

ValOre's Pedra Branca Trades at C$12/oz Inferred Against Peer Market Caps from C$126M to C$440M

ValOre Metals’ Pedra Branca project in Brazil hosts a 2.198 million ounce inferred 2PGE+Au resource across 63.6 million tonnes grading 1.08g/t, distributed across seven near-surface zones. Approximately 30% of the resource sits within weathered material targeted for bioleaching, while higher-grade chromitite material grading 6.4 to 8.5g/t 2PGE+Au accounts for roughly 5% of inferred ounces.

With a market capitalization of approximately C$26 million, Pedra Branca trades at roughly C$12 per inferred ounce. Comparable PGM developers currently trade at materially higher valuations, including:

- Stillwater Critical Minerals at approximately C$126 million

- Generation Mining at approximately C$236 million

- Bravo Mining at approximately C$440 million

- Platinum Group Metals at approximately C$389 million

ValOre is targeting a Preliminary Economic Assessment in Q4 2026, supported by stirred tank reactor testing in Q3 2026 and heap-leach column testing in Q4 2026.

South African Output Decline from 5.3Moz (2006) to 3.9Moz (2025) Caps Global Supply Elasticity

South Africa holds approximately 91% of global platinum reserves and accounts for approximately 70% of mine supply per WPIC, concentrating the world's supply response capacity within one jurisdiction. National primary platinum output has declined from approximately 5.3 million ounces in 2006 to approximately 3.9 million ounces in 2025, a contraction sustained across multiple price cycles including the 2008 spot peak above $2,290 per ounce.

Recycling, primarily from end-of-life catalytic converters, contributes roughly 25% of total platinum supply but has been compressed by lower vehicle scrappage rates and reduced auto-catalyst loadings on newer vehicles. The supply side carries fewer levers than at any point in modern PGM history, which is the process through which the deficit becomes self-reinforcing rather than self-correcting.

South African Cost Inflation & Flat Mine Supply Are Preventing Platinum Output Growth Above $2,000/oz

Standard commodity theory predicts that sustained price increases generate supply responses within two to three production cycles. The Bushveld Igneous Complex has not delivered that response. Power instability, diesel logistics exposure, labour cost inflation, and multi-year capital development timelines for new shaft sinking have together produced a marginal cost curve that compresses reinvestment economics even at platinum prices above $2,000 per ounce.

60% Electricity Cost Inflation & Strait of Hormuz Diesel Exposure Compress Reinvestment Economics

Electricity costs for South African PGM producers increased approximately 60% between 2021 and 2026 according to industry data referenced in WPIC quarterly commentary and producer disclosures. Eskom grid reliability constraints continue to extend operational downtime across major producers, with multiple shaft complexes reporting power-related production losses during 2025 and 2026. The cost trajectory directly compresses the reinvestment margin that would otherwise support shaft development and capital expansion at higher prices.

Diesel logistics layer a second cost pressure onto the same operating base. Approximately 60% of South African diesel imports transit the Strait of Hormuz, meaning haulage and processing costs for deep-level mines move directly with Middle East geopolitical risk. Sustained energy cost inflation compresses smelting margins and refinery economics, threatening the marginal portion of South African primary supply most exposed to operating cost shocks.

2026 WPIC Base Case Projects Flat Mine Supply Despite Platinum Above $2,000/oz

The 2026 WPIC base case projects total mine supply flat year-over-year, with the 2% headline lift attributable entirely to a 10% increase in recycling rather than to primary production growth. Platinum reached approximately $2,878 per ounce in January 2026 before stabilising near $2,000 per ounce by late April 2026. The 2025 platinum spot rally totalled approximately 127%, yet primary mine supply contracted by 5% over the same period, demonstrating the absence of price-induced supply response within the deficit cycle.

Bank of America Global Research raised its 2026 platinum forecast to $2,450 per ounce from $1,825 per ounce in January 2026, citing persistent market deficits and dislocations from ongoing trade disputes keeping the market tight. The forecast revision implies institutional supply models are not pricing in a material near-term primary production response, with replacement supply requiring multi-year capital programmes against a base case where existing producers face rising operating costs and declining shaft economics.

Platinum Above $2,700/oz Has Not Re-Rated PGM Developers Facing Metallurgical & Financing Constraints

Platinum surged past $2,700 per ounce during the 2025-2026 rally and palladium passed $2,000 per ounce, yet development-stage PGM equities have not re-rated in proportion to the underlying commodity move. The valuation gap reflects metallurgical complexity in near-surface deposits, financing constraints common to junior developers, and a narrow investor base familiar with PGM developer fundamentals. The result is that projects capable of validating scalable metallurgy and producing a credible Preliminary Economic Assessment in this cycle trade at material enterprise-value-per-ounce discounts to peers carrying comparable resource scale.

Limited Greenfield PGM Projects & Sub-80% Recoveries on Weathered Ores Are Constraining Near-Term Replacement Supply

Only a small number of major greenfield PGM projects globally are currently targeting near-term production, which compresses the universe of investable replacement supply against the deficit forecast. The thinness of the pipeline is partly geological, with most known economic PGM resource scale concentrated in the Bushveld Complex, the Great Dyke in Zimbabwe, and Norilsk in Russia.

Capital constraints impose a second barrier. Junior PGM developers face capital requirements that exceed typical gold or copper exploration budgets, particularly when metallurgical testwork is required at multiple scales.

Conventional sulfide flotation, the dominant processing route for Bushveld fresh-rock material, delivers materially lower recoveries on weathered or chromitite-hosted ores. Bench-scale hydrometallurgical testwork has achieved 72.88% platinum and 74.07% palladium extraction from weathered material via bioleaching, with caustic cracking on chromitite material returning 66.42% platinum and 78.81% palladium extraction per ValOre Metals' metallurgical update. Scale-up validation through stirred tank reactors and column tests remains the technical bridge between bench results and bankable plant assumptions.

The compound effect of pipeline thinness, capital intensity above gold and copper exploration benchmarks, and metallurgical scale-up risk is that near-term replacement supply cannot match WPIC's deficit trajectory of 348,000 to 689,000 ounces annually through 2029. New primary PGM production typically requires 5 to 10 years from PEA publication to first metal, meaning the supply gap widens before it narrows even if advanced developers execute on schedule. Institutional capital is therefore screening for projects combining bench-scale recoveries above 70%, near-surface mineralisation supporting open-pit mining, and PEA publication within the current deficit cycle.

The Investment Thesis for Platinum Group Metals

- Four consecutive World Platinum Investment Council deficit years totalling progressively larger annual shortfalls have reduced above-ground inventory to approximately four months of demand coverage, the threshold below which spot prices respond disproportionately to operational disruption rather than to demand variability.

- South African primary platinum output has declined from approximately 5.3 million ounces in 2006 to approximately 3.9 million ounces in 2025, a contraction sustained across multiple price cycles and driven by deep-level mining economics that current spot prices above $2,000 per ounce do not resolve.

- WPIC's 2026 base case projects flat year-over-year mine supply with the 2% headline lift attributable solely to a 10% recycling increase, confirming that primary production growth is not in the forecast horizon despite Bank of America Global Research's $2,450 per ounce 2026 platinum forecast.

- South African operating costs continue rising through 60% cumulative electricity inflation from 2021 to 2026 and Strait of Hormuz diesel exposure that compresses smelting and refining margins, threatening the marginal portion of the supply curve most likely to absorb additional ounces.

- Near-surface oxidised deposits with demonstrated bench-scale platinum and palladium extractions above 70% via hydrometallurgical routes carry capital intensity advantages over Bushveld-style deep-level operations, with scale-up validation through stirred tank reactor and column testing functioning as the bridge between current valuations and re-rating toward peer enterprise-value-per-ounce ranges.

- Developers carrying defined catalyst sequences through 4Q2026 Preliminary Economic Assessment publication and 1Q 2027 licensing initiation provide investors with dated technical proof points against which valuation gaps can be reassessed within the current deficit cycle.

The platinum market’s shift from an autocatalyst-driven metal into a scarcity asset is now visible in WPIC inventory data. Four consecutive deficit years have reduced above-ground stocks to roughly four months of demand coverage, the threshold where operational disruptions increasingly drive spot price volatility. South African supply growth remains constrained by power costs, labour pressures, mine depth, and capital intensity rather than by metal prices alone. Developers advancing near-surface projects, hydrometallurgical recoveries above 70%, and Preliminary Economic Assessments targeted for late 2026 may become increasingly important as institutional capital reassesses replacement supply exposure through 2026 and 2027.

TL;DR

The platinum market entered its fourth consecutive annual deficit in 2025 after WPIC reported a 1.082Moz shortfall and above-ground inventories fell to roughly four months of demand coverage, increasing sensitivity to supply disruptions. South African mine output continues declining despite platinum prices above $2,000/oz because power costs, labour pressures, diesel exposure, and deep-level mining complexity are limiting supply growth. At the same time, development-stage PGM equities remain discounted despite structurally tighter markets, particularly companies advancing near-surface projects with scalable hydrometallurgical recoveries and Preliminary Economic Assessment timelines targeting late 2026.

FAQs (AI-generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed