Saudi Arabia Speeds 17 Million Barrels to Market as Brent Holds Near $72 Amid Contango

Saudi supply and Aramco's spot pricing drive Brent contango, speeding 17 million Gulf barrels to market and pressuring Q3 oil budgets.

- Brent crude settled at $71.87 per barrel, up 0.1%, while WTI fell 0.09% to $68.63 as Saudi Arabia's faster exports and Aramco's shift to spot pricing offset the market's immediate price response.

- Saudi Arabia shipped 34 million barrels through the Strait of Hormuz from June 17 to July 2, up from 15 million barrels in the prior 10 weeks, leaving 17 million pre-war barrels still awaiting delivery and adding to near-term supply.

- Kuwait raised output from 580,000 to 1.65 million barrels per day after the Hormuz reopening, adding more deferred OPEC+ supply to the market alongside Saudi Arabia.

- Brent's forward curve flipped from backwardation to contango as front-month prices rose from $69.10 to $70.90, signaling the market expects higher near-term crude supply.

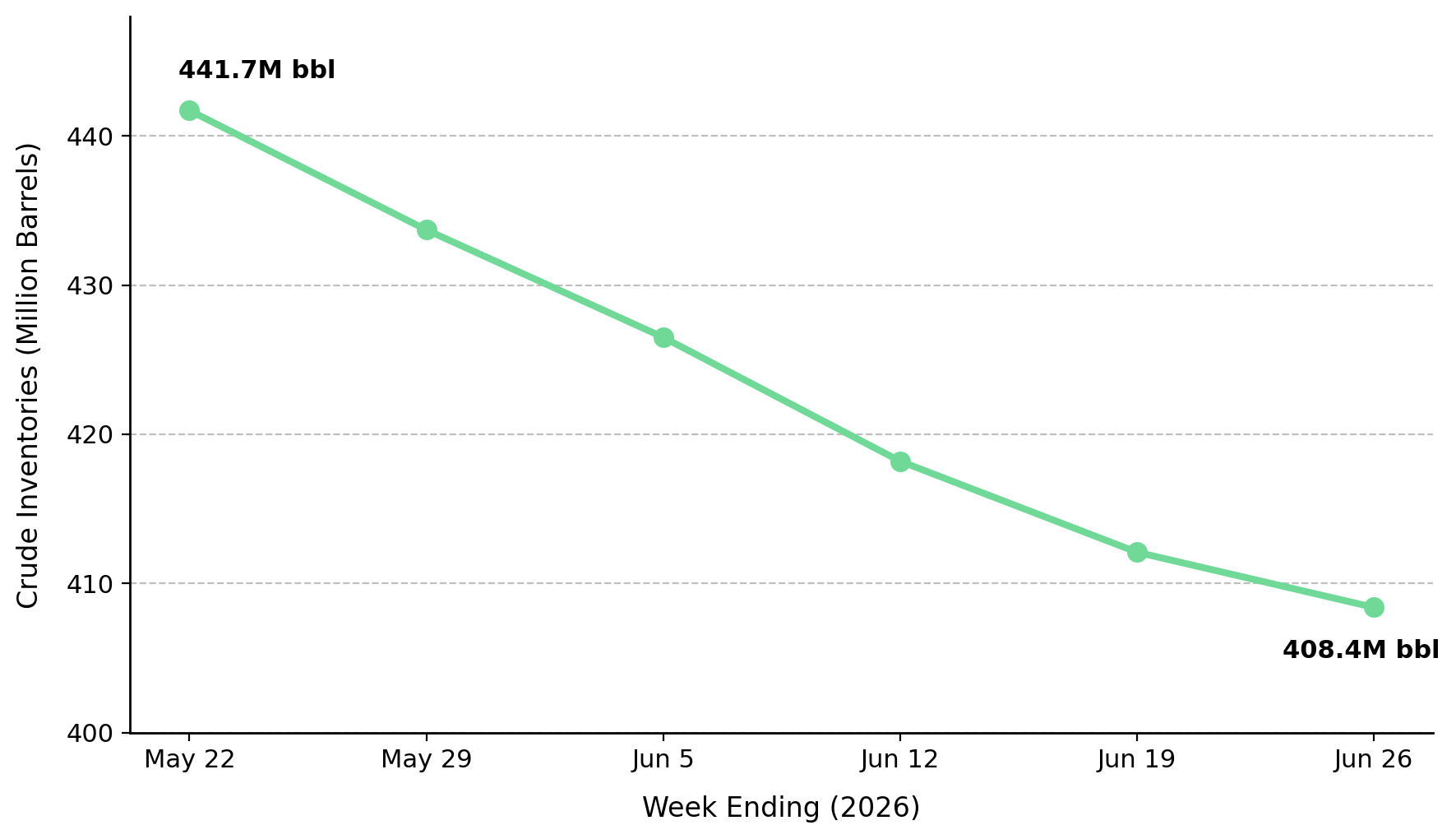

- US commercial crude inventories stood at 408.4 million barrels, 7% below the five-year average, while Hormuz throughput remained at 8.5 million barrels per day versus a 15 million barrel per day pre-war baseline, limiting supply despite faster Gulf exports.

Higher Gulf Crude Supply Limits Brent & WTI Gains

Brent crude settled at $71.87 per barrel, up 0.1%, while WTI fell 0.09% to $68.63. The muted price move came despite faster Saudi exports through Hormuz and Aramco's shift to spot pricing, both of which increased near-term crude supply.

Saudi Arabia shipped 34 million barrels through the Strait of Hormuz from June 17 to July 2, up from 15 million barrels in the prior 10 weeks, leaving 17 million pre-war barrels awaiting delivery and adding to near-term supply. Kuwait raised output from 580,000 to 1.65 million barrels per day after the Hormuz reopening, adding more deferred OPEC+ supply to the market alongside Saudi Arabia.

Brent Contango Signals Faster Gulf Crude Deliveries

Brent's forward curve flipped from backwardation to contango between June 24 and July 2. Front-month Brent rose from $69.10 to $70.90 as the market shifted from backwardation to contango, signaling expectations of higher near-term crude supply. The shift to contango signaled the market expected higher Saudi supply before Aramco announced its move to spot pricing.

According to the EIA Weekly Petroleum Status Report, US commercial crude inventories stood at 408.4 million barrels, 7% below the five-year average, while crude imports fell 10.9% year over year. Hormuz throughput remained at 8.5 million barrels per day versus a 15 million barrel per day pre-war baseline, limiting regional crude flows despite faster Saudi exports.

Aramco Spot Pricing Accelerates Near-Term Crude Deliveries

Saudi Aramco switched from formula-based to spot pricing for crude sales. Formula pricing uses scheduled benchmark prices, while spot pricing lets Aramco sell at current market prices with shorter delivery times. Faster shipments and spot pricing allow the remaining 17 million Gulf barrels to reach the market sooner, increasing near-term crude supply.

Kuwait raised output from 580,000 to 1.65 million barrels per day after the Hormuz reopening, adding a second source of deferred OPEC+ supply to the market. Faster Saudi and Kuwaiti supply helps explain Brent's shift to contango by increasing expectations of higher near-term crude availability.

Lower Hedge Prices Pressure $75-80 Brent Budgets

E&P operators budgeting for $75 to $80 Brent face pressure from weaker near-term pricing and a lower forward curve. Contango keeps near-term hedge prices below backwardated levels until the remaining 17 million Gulf barrels are absorbed. UBS's $80 Q3 Brent ceiling leaves many E&P budgets at the top of their expected price range.

Aramco's move to spot pricing allows the remaining 17 million barrels to reach the market sooner, increasing near-term crude supply. That adds downward pressure to Brent prices during the same quarter many E&P operators are hedging.

Hormuz Throughput, Brent's Forward Curve & US Inventories Signal Gulf Supply Absorption

According to the EIAt, Hormuz throughput remained at 8.5 million barrels per day versus a 15 million barrel per day pre-war baseline. Higher throughput would allow the remaining 17 million barrels to reach the market sooner. A return to backwardation would signal the market has absorbed the remaining Saudi and Kuwaiti supply, while sustained contango would indicate excess Gulf barrels are reaching the market more slowly than expected.

US commercial crude inventories stood at 408.4 million barrels, according to the EIA, 7% below the five-year average, leaving room to absorb additional Saudi and Kuwaiti supply. Weekly inventory builds of 3 to 5 million barrels would erase that deficit, remove support for Brent above $70, and show whether the market is absorbing the additional Gulf supply alongside the forward curve.

Analyst's Notes

Subscribe to Our Channel

Stay Informed