Brent Crude Returns to Pre-War Price, Supporting Refining Margins

Brent recovered to pre-war levels while constrained Hormuz flows kept fuel prices elevated, extending the margin advantage for refiners.

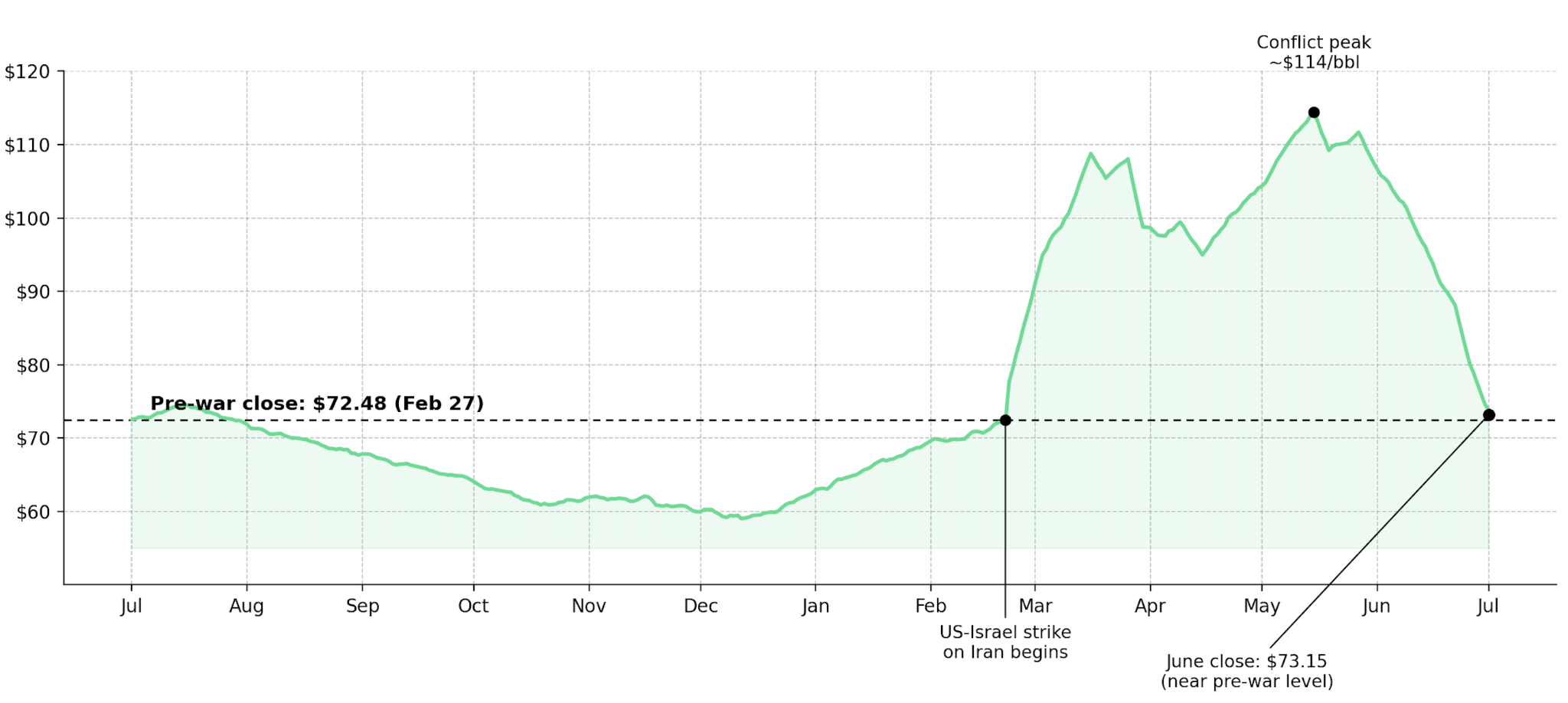

- Brent crude is set to close in June about 22% below its May level, while WTI is about 19% below its May 29 close.

- Brent settled at $73.15 a barrel, just above its $72.48 close on February 27, the day before the US and Israel struck Iran.

- Singapore gasoil is 22% and gasoline 26.6% above their February 27 pre-war prices, even as crude prices have returned to near pre-war levels.

- Crude flows through the Strait of Hormuz averaged 2.79 million bpd in June, less than one-fifth of the pre-war three-month average of 15.58 million bpd.

- US refiners ran at 96.1% of operable capacity while processing 17.1 million bpd of crude, as distillate inventories remained about 10% below the five-year average.

US-Iran Talks & Brent Returns to Pre-War Levels

Oil prices fell about 1%, reversing the previous session's gains, with Brent August futures down $0.75 to $72.40 a barrel and WTI down $0.57 to $70.18. Brent is set to close in June about 22% below its May level, while WTI is about 19% below its May 29 close as markets await potential US-Iran talks in Doha.

Brent settled at $73.15 a barrel, just above its $72.48 close on February 27, the day before the US and Israel struck Iran, returning crude prices to near pre-war levels. Refined products have not followed crude lower, with Singapore gasoil 22% and gasoline 26.6% above their February 27 pre-war prices.

Constrained Hormuz Flows & Asia's Crude Imports

Crude flows through the Strait of Hormuz averaged 2.79 million bpd in June, up from 881,000 bpd in May but less than one-fifth of the 15.58 million bpd average in the three months before the conflict. Asia's seaborne crude imports are forecast at 20.71 million bpd in June, up from 20.39 million bpd in May but below the pre-war average of 26.79 million bpd.

Refiners are still processing higher-cost crude bought outside the Middle East during the conflict, leaving Singapore gasoil 22% and gasoline 26.6% above their February 27 prices even as crude prices have returned to near pre-war levels.

Iran's Shipping Threats & Doha Negotiations

Iranian Deputy Foreign Minister Kazem Gharibabadi said Tehran would "try to obstruct vessels outside defined paths" as talks with Oman begin on redefining Hormuz transit, while Iran's foreign ministry said no meeting with the US is scheduled. Shipping through the Strait of Hormuz remains constrained as Iran continues to contest transit terms despite the ceasefire.

KCM Trade chief market analyst Tim Waterer said markets are pricing in a positive outcome from the Doha talks, even though real normalization of flows through the Strait of Hormuz is not yet visible, adding the market is cautiously hopeful but still hedging its bets. Iran denied any scheduled talks, even as President Trump called the Doha meeting "perhaps important, perhaps not," leaving the timing of any agreement uncertain.

In the base case, Hormuz flows continue recovering toward the pre-war average of 15.58 million bpd as the ceasefire holds, reducing refined-product premiums as more crude reaches Asia. In the bear case, renewed Iranian attacks on shipping could keep Hormuz flows near June's 2.79 million bpd for another quarter, keeping gasoil and gasoline premiums elevated.

Crude-Fuel Price Gap & Refining Margins

Refiners continue to benefit from wider margins as crude input costs sit within $1 of pre-war levels, while Singapore gasoil and gasoline trade 22% and 26.6% above their February 27 prices. Brent's roughly 22% decline in June also reduces revenue for E&P producers that price output against the benchmark. US refiners ran at 96.1% of operable capacity while processing 17.1 million bpd of crude.

Distillate inventories remained about 10% below the five-year average despite a 3.1-million-barrel weekly build, supporting higher gasoil and gasoline prices. Refining margins depend on how long refiners can maintain the gap between lower crude costs and higher refined-product prices.

China's Crude Imports & Refining Margin Outlook

Refined-product prices remain elevated as Hormuz crude flows averaged 2.79 million bpd in June and Asia's seaborne imports stayed below the pre-conflict average of 26.79 million bpd, even as Brent traded within $1 of its $72.48 pre-war close.

Hormuz flows recovering toward 15.58 million bpd, and Asia's crude imports returning to their pre-conflict average of 26.79 million bpd would increase crude supply and narrow gasoil and gasoline premiums.

China's seaborne crude imports recovering toward the pre-conflict average of 11.39 million bpd, with cargoes arriving from August, would signal that crude flows are normalizing and refined-product premiums are likely to narrow. The next EIA Weekly Petroleum Status Report, Kpler's tracking of Strait of Hormuz crude flows, and Asia's seaborne imports will indicate whether supply is returning to normal.

Analyst's Notes

Subscribe to Our Channel

Stay Informed