Persistent Silver Supply Deficits Drive Strategic Repricing Amid Industrial Demand Surge

Silver faces 206M oz deficit in 2025, eighth consecutive year. Industrial demand from solar, EVs drives structural repricing opportunity.

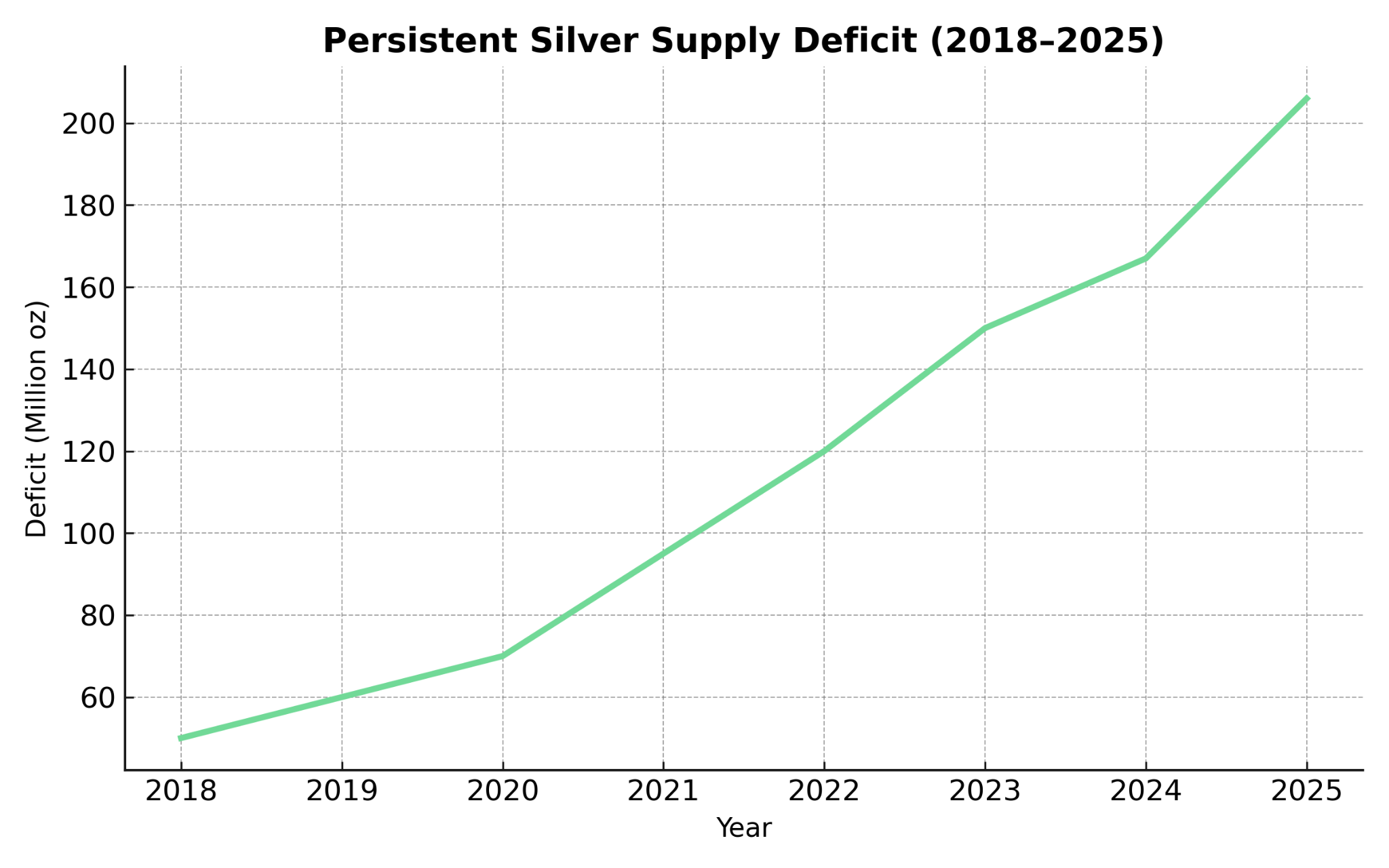

- Silver faces a structural supply deficit projected at 206M oz in 2025, marking the eighth consecutive year of imbalance.

- Approximately 70% of silver is produced as a byproduct, limiting supply elasticity even in high-price environments.

- Industrial demand is surging, led by solar photovoltaics (232M oz in 2024), EVs, semiconductors, and 5G—demand that is less price-sensitive.

- Institutional investment flows are accelerating, with $40B in silver-backed ETPs and 95M oz inflows in H1 2025, outpacing 2024 totals.

- Companies with tier-one silver assets and strong funding—such as Cerro de Pasco, Vizsla Silver, and GR Silver Mining—are positioned to benefit from both structural scarcity and long-term repricing trends.

Macroeconomic Drivers Reshaping Silver Markets

Silver's investment profile has evolved significantly as markets grapple with the metal's dual nature as both a monetary hedge and essential industrial commodity. The projected supply deficit of 206 million ounces in 2025 represents an expansion from 167 million ounces in 2024, marking the eighth consecutive year of structural imbalance. This persistent shortfall occurs against a backdrop of inelastic supply dynamics, where approximately 70% of global silver production emerges as a byproduct of copper, lead, and zinc mining operations.

Current Policy Environment & Price Pressures

Current macroeconomic indicators present a complex picture for precious metals investors. Producer Price Index data suggests inflationary pressures remain embedded in industrial supply chains, while Federal Reserve policy signals from Jackson Hole indicate continued monetary accommodation. However, near-term headwinds include US dollar resilience and easing geopolitical tensions, which have temporarily reduced safe-haven demand for precious metals.

Structural vs Cyclical Market Dynamics

The structural nature of silver's supply deficit distinguishes current market conditions from cyclical pricing dynamics. Unlike primary metal production that can respond to price signals through increased investment and exploration, silver's byproduct nature limits supply elasticity even in favorable pricing environments. This fundamental constraint underpins long-term repricing expectations as industrial demand continues expanding across multiple sectors.

Market participants increasingly recognize that traditional precious metals analysis fails to capture silver's evolving demand profile. Industrial applications now account for over 50% of annual consumption, with sectors including solar photovoltaics, electric vehicles, semiconductors, and telecommunications infrastructure driving price-inelastic demand growth that contrasts sharply with discretionary investment flows.

Structural Deficits & Investor Repricing Dynamics

Seven consecutive years of supply deficits have created market conditions reminiscent of other commodity cycles where sustained imbalances eventually triggered significant repricing. HSBC forecasts project continued deficits through 2027, with the current trajectory suggesting cumulative shortfalls exceeding 1.5 billion ounces over the next three years. This sustained imbalance parallels historical precedents in uranium markets during the 2000s and copper shortfalls that preceded the commodity supercycle.

Rising Cost Structures & Mining Economics

The persistence of these deficits reflects deeper structural issues within global silver markets. All-in sustaining costs have risen approximately 40% since 2020, driven by inflationary pressures across energy, labor, and equipment inputs. Simultaneously, declining ore grades at major producing mines have increased processing costs while reducing per-tonne metal recovery rates. These factors combine to create an environment where significant price appreciation becomes necessary to incentivize marginal production.

Evolving Investment Allocation Patterns

Investor behavior patterns suggest growing recognition of these structural dynamics. Portfolio managers are increasingly treating silver exposure as both inflation hedge and technology play, resulting in allocation strategies that differ markedly from traditional precious metals positioning. This shift reflects understanding that silver's industrial demand profile provides earnings support independent of monetary policy cycles or geopolitical risk premiums.

Supply Inelasticity in Byproduct-Dominated Markets

The byproduct nature of silver production creates fundamental constraints on supply responsiveness that distinguish the metal from other commodities. When copper, lead, or zinc producers adjust output in response to their primary metal pricing, silver production moves accordingly regardless of silver-specific market conditions. This dynamic means that even substantial silver price increases may not generate proportional supply responses if base metal markets remain subdued.

Exploration and development pipelines for primary silver projects remain notably thin compared to other precious metals. The extended development timelines required for new mining operations, typically 8-10 years from discovery to production, mean that current supply constraints cannot be rapidly addressed through new project development. Additionally, the capital intensity required for modern mining operations has increased significantly, creating higher hurdle rates for project advancement.

These supply-side constraints suggest that current deficit conditions are durable rather than cyclical. Unlike gold markets where substantial above-ground inventories provide supply buffer capacity, silver's industrial consumption results in permanent demand destruction that cannot be reversed through recycling or inventory releases.

ETP Flows as Leading Indicators

Exchange-traded product flows provide valuable insight into institutional silver positioning, with current assets under management reaching $40 billion across silver-backed investment vehicles. The 95 million ounce inflows recorded during the first half of 2025 already exceed total 2024 accumulation, signaling accelerating institutional conviction regarding silver's structural scarcity narrative.

This institutional accumulation pattern differs markedly from retail investment flows that typically respond to price momentum or macroeconomic uncertainty. Professional asset managers are increasingly treating silver ETPs as portfolio diversification tools that provide exposure to both monetary debasement themes and technology sector growth trends. The sustained nature of these inflows suggests conviction-based positioning rather than tactical trading activity.

The scale of institutional accumulation also highlights potential supply pressure on physical markets. When combined with industrial demand growth, continued ETP inflows could create conditions where available silver inventories become insufficient to meet combined investment and industrial requirements, potentially triggering more aggressive repricing dynamics.

Industrial Demand Anchored by the Energy Transition

Industrial applications have emerged as the primary driver of silver demand growth, with solar photovoltaic installations alone consuming 232 million ounces in 2024. This represents a quadrupling of solar-related silver consumption since 2015, reflecting both the expansion of renewable energy capacity and the metal's irreplaceable role in photovoltaic cell conductivity. Unlike investment demand, which responds to macroeconomic conditions, industrial silver consumption demonstrates price inelasticity driven by performance requirements and limited substitution options.

Electrification Demand Vectors

The energy transition has created multiple demand vectors for silver beyond solar applications. Electric vehicle production requires approximately 25-50 grams of silver per vehicle for electrical contacts and circuit boards, with global EV sales projected to reach 30 million units annually by 2030. Semiconductor manufacturing processes depend on silver's superior electrical conductivity, while 5G telecommunications infrastructure deployment requires substantial silver content for antenna arrays and electronic components.

Structural Demand Parallels

This industrial demand profile parallels the structural demand stories that drove lithium and cobalt markets during the early stages of electrification trends. However, silver's established industrial applications and mature supply chains provide more predictable demand trajectories compared to emerging battery materials that faced adoption uncertainty and substitution risks.

Silver as a Green Energy Enabler

Solar panel manufacturing represents the most significant growth driver for industrial silver demand, with photovoltaic applications expected to consume over 250 million ounces annually by 2027. The metal's unique combination of electrical conductivity, corrosion resistance, and thermal stability makes it irreplaceable in solar cell applications where performance degradation directly impacts energy generation efficiency.

Substitution efforts using alternative materials such as copper or aluminum have proven unsuccessful due to inferior electrical properties and reduced panel longevity. Solar manufacturers have instead focused on reducing silver consumption per panel through thinner conductive traces and improved application techniques, but these efficiency gains have been more than offset by rapidly expanding global solar capacity installations.

Electric vehicle and semiconductor applications provide additional demand support with similarly limited substitution potential. These sectors require silver's superior performance characteristics in high-reliability applications where failure costs exceed material cost considerations by substantial margins.

Case Study Integration: Cerro de Pasco

Cerro de Pasco Resources exemplifies the strategic positioning available within silver markets through exposure to both traditional precious metals and critical minerals demand. The company's approach to environmental remediation in Peru provides exposure to silver recovery alongside gallium and indium production, positioning the operation within broader critical minerals supply chain themes.

The operation's economic profile reflects favorable processing costs enabled by the pre-concentration of materials through historical mining activities. Internal projections indicate profit margins of $39 per tonne processed across a 75 million tonne life-of-mine resource, potentially generating $2.9 billion in total profits. The project's environmental remediation mandate aligns with ESG investment criteria while providing exposure to silver price appreciation and critical minerals demand growth.

Strategic Positioning of Silver Producers in a Tight Market

Mining companies with primary silver exposure are positioned to capture disproportionate leverage from structural market tightening. The combination of sustained supply deficits and growing industrial demand creates conditions where well-positioned producers can achieve significant margin expansion and valuation re-rating. Key differentiating factors include low all-in sustaining costs, strong balance sheet capacity, and scalable resource bases that can respond to favorable market conditions.

Merger and acquisition activity within the silver mining sector reflects industry recognition of these structural dynamics. Mexican silver consolidation themes have gained momentum as larger producers seek to build scale advantages in key jurisdictions. Companies with development-stage assets and strong funding positions are particularly well-positioned to benefit from both organic growth opportunities and potential consolidation premiums.

The current market environment favors producers with operational flexibility and financial strength. Rising input costs across energy, labor, and equipment categories have pressured margins at higher-cost operations, creating potential acquisition opportunities for well-capitalized companies. Additionally, jurisdictional advantages in Mexico and Peru provide regulatory stability that supports long-term development planning.

Vizsla Silver: Scaling a Tier-One Asset

Vizsla Silver’s Panuco Project in Mexico represents the development of what could become the world's largest primary silver producer upon reaching commercial production. The project's 361 million ounce silver equivalent resource supports preliminary economic assessment results indicating $1.1 billion net present value and 86% internal rate of return based on all-in sustaining costs of $9.40 per ounce.

Chief Executive Officer Michael Konnert outlines the company's development trajectory:

"We're developing Mexico's next tier one silver deposit. We've gone very rapidly from early-stage to approaching our feasibility study and project finance phase, so in the next few years we'll be rapidly moving through construction into production at which point we'll be the largest single asset silver primary producer in the world."

The company's $200 million cash position provides financial flexibility for advancing through feasibility study completion in 2025 toward production targeted for 2027. Initial production profiles indicate 20 million ounces of silver equivalent annually during the first two years of operation, with potential to maintain these production levels through extended mine life optimization.

GR Silver Mining: Consolidation & Expansion Potential

GR Silver Mining's Plomosas Project demonstrates the value creation potential available through strategic asset repositioning and exploration success. The company's 134 million ounce silver equivalent resource trades at approximately $0.65 per ounce in-ground, representing a substantial discount to peer group valuations. This valuation gap reflects both the company's recent financial restructuring and market recognition opportunities for well-executed strategic repositioning.

Executive Chairman Eric Zaunscherb emphasizes the consolidation opportunity:

"What the market wants right now is consolidation in the silver space and what we're going to see is the creation of new strong players in the silver space. That's part of the narrative that there will be consolidation happening in Mexico and it is our intent to be front and center in that."

The company has completed a financial turnaround that eliminated debt and established positive working capital, positioning the operation for resumed exploration and potential strategic transactions. The Plomosas resource includes both development-ready infrastructure and exploration upside through the San Marcial target area, providing multiple value creation pathways.

Jurisdictional Advantage: Mexico & Peru

Mexico maintains its position as the world's leading silver producer, with the new administration under President Claudia Sheinbaum demonstrating a more pragmatic approach to mining sector development. Peru's established mining infrastructure and hydroelectric power advantages support cost-competitive operations in politically stable jurisdictions.

Market Risk Factors & Investor Considerations

Several factors could constrain near-term silver price performance despite favorable structural dynamics. US dollar strength continues capping precious metals upside, while reduced geopolitical tensions have diminished safe-haven demand. Additionally, tariff policy uncertainty between the United States and Mexico could impact mining sector investment flows and operational planning.

Operational & Jurisdictional Risks

Operational risks facing silver producers include extended permitting timelines, security considerations in Mexico, and community relations management. Foreign exchange volatility can significantly impact margins for operations in emerging market jurisdictions, particularly given the capital-intensive nature of mining investments. These factors require careful evaluation when assessing individual company exposure within broader silver market positioning.

Regulatory & Cost Environment

Regulatory changes represent ongoing risks, particularly regarding environmental standards and taxation policies. However, the critical nature of silver for renewable energy applications may provide political support for strategic mining projects that advance climate transition objectives. Companies with strong environmental and social governance profiles are likely better positioned to navigate evolving regulatory landscapes.

Rising input costs across energy, labor, and equipment categories have pressured industry margins, with inflationary pressures potentially persisting despite monetary policy normalization. This environment favors operations with established cost structures and long-term supply contracts, while challenging development-stage projects facing current-market input pricing.

The Investment Thesis for Silver

The convergence of structural supply deficits with accelerating industrial demand creates compelling investment rationale for silver exposure across multiple timeframes and risk profiles:

- Persistent supply deficits driven by byproduct production dynamics and limited exploration pipelines support long-term repricing expectations independent of monetary policy cycles

- Industrial demand anchored by energy transition requirements demonstrates price inelasticity and secular growth trends that contrast with cyclical investment flows

- Institutional portfolio flows reflect growing recognition of silver's dual role as both inflation hedge and technology enabler, supporting sustained investment demand

- Well-positioned mining companies offer leveraged exposure to structural repricing through scalable resource bases, favorable jurisdictional positioning, and strong balance sheet capacity

- Mexican and Peruvian operations benefit from established mining frameworks and regulatory stability that supports multi-year development planning and operational execution

Silver’s Case for Investor Reallocation

Silver markets stand at the intersection of monetary uncertainty and technological transformation, creating investment dynamics that extend well beyond traditional precious metals analysis. The metal's unique position as both store of value and critical industrial input provides portfolio diversification benefits while capturing exposure to multiple secular growth themes.

Current market conditions present a window of opportunity during price consolidation, with institutional flows and structural deficits supporting longer-term repricing expectations. Well-positioned companies with tier-one assets, strong funding, and favorable jurisdictional exposure offer leveraged participation in these macro trends while providing operational diversification across multiple demand vectors.

The investment thesis centers on scarcity, demand growth, and accelerating institutional recognition converging to create compelling allocation opportunities within silver markets. For investors seeking exposure to both monetary hedge characteristics and technology sector growth trends, silver presents a distinctive positioning opportunity that bridges traditional precious metals allocation with critical materials investment themes.

Analyst's Notes

Subscribe to Our Channel

Stay Informed