Refining Concentration Reaches 86% & Capital Flows to Non-China Critical Metals Processing

Refining concentration reached 86% in 2024, driving capital toward non-China processing, recycling, and alternative critical minerals supply chains.

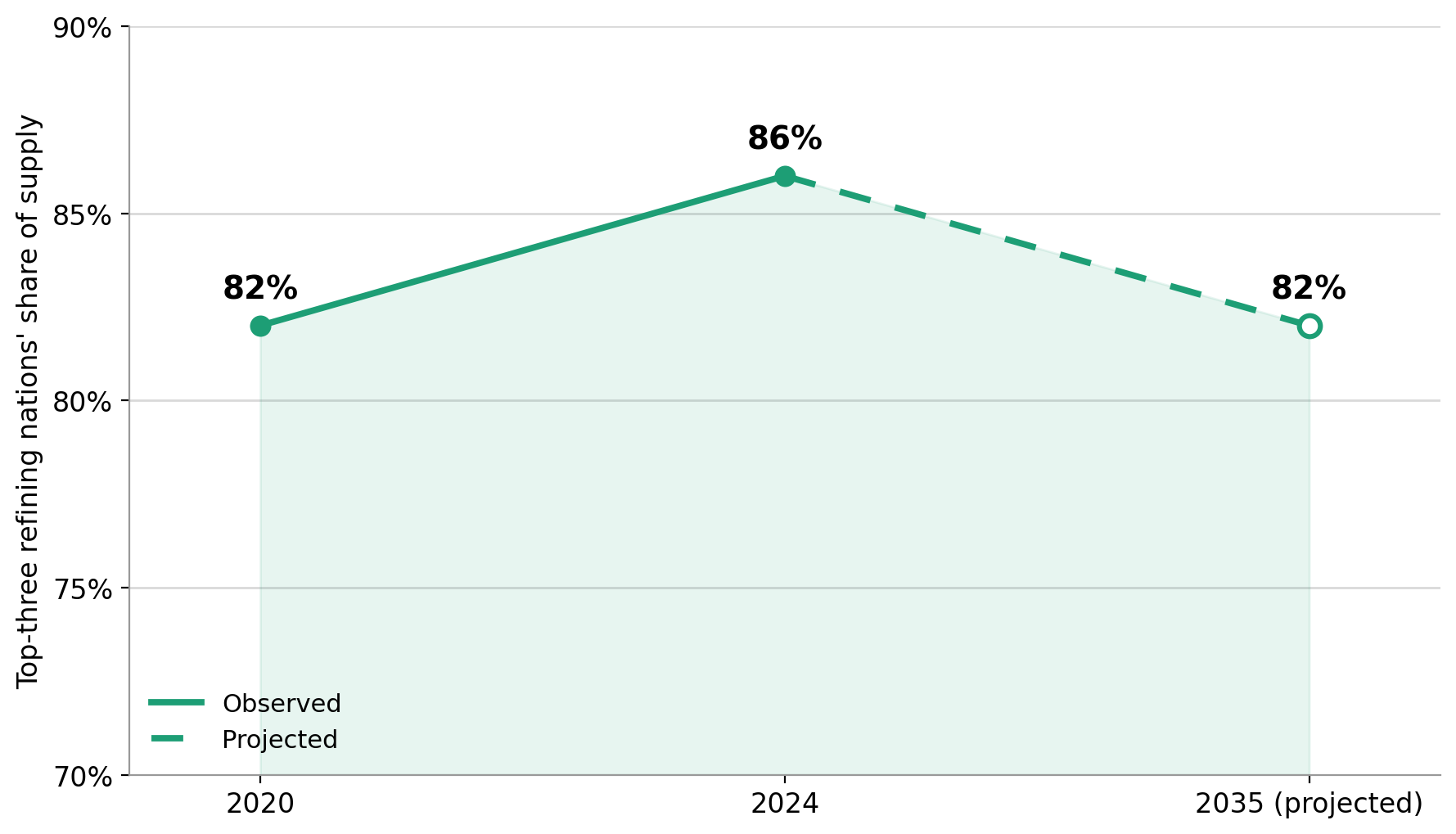

- China, Indonesia, and Chile controlled 86% of refining supply across key battery and critical minerals in 2024. The IEA's 2025 Global Critical Minerals Outlook shows refining concentration has increased from roughly 82% in 2020 to 86% in 2024, making processing capacity, rather than mine ownership, the primary bottleneck in critical mineral supply chains.

- While mining supply is becoming more diversified, refining remains highly concentrated. The IEA projects China will still supply more than 60% of refined lithium and cobalt and roughly 80% of battery-grade graphite and magnet rare earths by 2035 under current policies.

- China's export controls on key rare earths demonstrated how processing capacity can influence access to critical minerals, accelerating government funding, strategic offtakes, and private-sector investment in non-China refining assets.

- Governments are expanding support through stockpiles, development finance, equity participation, and offtake agreements. Washington's critical minerals stockpile initiative alone targets roughly 60 days of demand cover, with lithium representing an estimated US$416 million component.

- The thesis remains dependent on policy support, commercial-scale execution, and sustained demand growth. Changes in refining capacity, government funding, recovery economics, or end-market demand could weaken the investment case.

Refining Concentration Becomes the Critical Minerals Bottleneck

For most of the past decade, critical minerals investors focused on mine ownership, ore grades, and jurisdiction because those factors were viewed as the primary drivers of supply growth and project value. That focus is becoming less useful because refining capacity, rather than resource ownership alone, has emerged as the main bottleneck in several critical mineral supply chains. The key constraint on Western supply chains now sits downstream in refining and processing, where raw concentrate is converted into battery-grade and magnet-grade materials.

Across copper, lithium, nickel, cobalt, graphite, and rare earths, the market share of the top three refining nations rose to 86% in 2024 from about 82% in 2020, according to the IEA's 2025 Global Critical Minerals Outlook. Under the IEA's current-policy scenario, China is projected to supply more than 60% of refined lithium and cobalt and roughly 80% of battery-grade graphite and magnet rare earths by 2035, reinforcing the strategic importance of refining capacity outside the country.

The IEA also projects that the top three producers' share of mined lithium will fall below 70% by 2035 as new suppliers enter lithium, graphite, and rare earth markets. While mining is becoming more diversified, refining remains highly concentrated. For investors, that means scarcity is increasingly found in processing capacity rather than mineral deposits, making projects with refining or processing assets outside China better positioned to secure government support, attract strategic capital, and access higher-value supply chains.

Chinese Export Controls & the Premium on Non-China Processing

China's April 2025 export controls on dysprosium, terbium, and yttrium reduced access to key rare earth inputs for Western manufacturers, and Beijing expanded strengthened dual-use export controls to Japan in January 2026, highlighting the supply-chain risks created by concentrated processing capacity. These restrictions accelerated government funding, strategic offtake agreements, and private-sector investment in non-China refining projects by demonstrating that control of processing capacity can influence access to critical minerals. As a result, investors are increasingly assigning higher valuations to companies that can produce refined material outside China because their output offers greater supply-chain security and strategic value to Western customers.

Government Capital Expands Critical Minerals Processing Capacity

Governments are responding to refining concentration by directing capital toward processing projects that can expand non-China supply chains. Government support now extends beyond grants and includes stockpiles, offtake agreements, development financing, and direct equity investment.

These measures include strategic stockpiles that reduce supply disruptions, offtake agreements that secure future revenue and can establish minimum pricing, and direct equity investments that lower financing risk for project developers. By classifying processed minerals as defense-critical under US national security frameworks, policymakers have expanded the justification for government funding, strategic procurement, and long-term support of domestic processing capacity.

Washington's critical minerals stockpile initiative targets roughly 60 days of demand cover, with Benchmark Mineral Intelligence estimating lithium as the largest component at approximately US$416 million, creating an additional source of demand for strategically important supply chains. Government equity participation in domestic producers and developers, alongside precedents such as the US$565 million financing package arranged for a Brazilian rare earth project, has expanded access to capital for processing projects that previously struggled to secure funding on commercial terms. For investors, government participation can reduce financing risk and support minimum demand through stockpiles and offtake agreements, but it also creates policy risk because funding priorities can change after elections or budget reviews.

Vertical Integration Strengthens Non-China Rare Earth Processing

Energy Fuels provides a publicly listed example of the non-China processing theme because it combines uranium production with rare earth processing infrastructure in the US. The company operates the only fully licensed conventional uranium mill in the US and is modifying the facility to process mixed rare earth carbonate from third-party feedstock, including ionic adsorption clays. A planned Phase 2 expansion targets approximately 6,300 tonnes per annum of neodymium-praseodymium oxide production, alongside terbium and dysprosium processing capacity. Vertical integration can reduce supply-chain bottlenecks by combining multiple processing stages within a single platform, which may improve feedstock security and increase the strategic value of the asset to customers and government stakeholders.

Mark Chalmers, Chief Executive Officer of Energy Fuels at the time of the interview, argued that vertically integrated processors are gaining an advantage as governments and customers seek secure supply chains:

"The industry is made up of fragmented players, but we are not one of them. As the market increasingly recognizes that those fragments cannot succeed on their own, that realization is working strongly in our favor."

By-Product Recovery Lowers Costs & Expands Rare Earth Exposure

Recovering a strategic metal as a by-product of an existing operation can lower development costs because the primary mine, infrastructure, and processing facilities are already funded by another revenue stream. By recovering minerals from existing process streams or tailings facilities, developers can avoid building a new mine, dedicated processing circuit, and standalone refining plant, reducing both capital requirements and project risk. Large capital costs and lengthy permitting timelines for rare earth separation facilities have increased investor interest in lower-cost alternatives such as by-product recovery.

Sovereign Metals illustrates this approach through its Kasiya project, which can potentially generate rare earth output from material already being processed for its primary products. Kasiya reports a pre-tax net present value of US$2.2 billion at an 8% discount rate, a pre-tax internal rate of return of 23%, and operating costs of US$450 per tonne, while metallurgical testwork indicates monazite can be recovered from the non-conductor tailings stream at near-zero incremental cost. Across four pits, the total rare earth oxide basket averages 2.5% combined dysprosium-terbium and 11.8% yttrium, roughly seven times the ratio reported by the world's five largest producers. Support from the World Bank, International Finance Corporation, Mitsui, and Traxys suggests both strategic capital and potential customers are already backing development of the project.

The cost logic of by-product recovery was put plainly by Ben Stoikovich, Chairman of Sovereign Metals, speaking on the project's graphite by-product:

"Our incremental cost of producing graphite as a by-product from the Kasiya project is just $241 per tonne, placing us at the bottom of the global cost curve at a time when many competing projects struggle to generate economic returns."

Recycling Creates a Mine-Free Route to Refined Supply

Recycling offers an alternative route to refined metal supply because it bypasses mine development and recovers metal directly from existing material streams. Lifezone Metals is advancing a US platinum group metals recycling project based on its proprietary Hydromet processing technology, which the company states uses less energy and produces fewer emissions than conventional smelting. A one-tonne pilot campaign on spent automotive catalytic converters demonstrated recoveries of up to 99% for platinum and palladium and 95% for rhodium.

The project remains pre-final-investment-decision, and current revenue is generated from third-party laboratory services rather than metal sales. The recycling business also includes a 6% partner stake from Glencore and two US Department of Energy grant applications totaling US$41.5 million, providing external validation while leaving execution and funding risks unresolved.

Ingo Hofmaier, Chief Financial Officer of Lifezone Metals, linked the company's recycling strategy to broader concerns about supply security and growing Western dependence:

"A deposit like Kabanga ensures the traceability of nickel sulfates that ultimately pass through Western smelters. Nickel remains one of the fastest-growing commodities, with demand growth of more than 4%, and Western governments would not want to see dependence on Indonesia continue to increase."

Indonesian Supply Discipline Increases the Value of Western Sulfide Nickel

Processing capacity remains important in nickel, but access to large sulfide deposits still determines which projects can supply high-purity battery materials. Battery and defense supply chains favor class-one nickel from sulfide deposits because it can be converted into high-purity nickel sulfate, while the laterite deposits that dominate Indonesian output require more energy-intensive processing. Large sulfide nickel deposits outside Indonesia are uncommon, which can support higher valuations for Western developers capable of supplying battery-grade nickel without relying on government subsidies.

Indonesia controls roughly two-thirds of global mined nickel and has tightened output through tiered royalties, restrictions on new processing capacity, and producer quotas, helping lift nickel prices by more than US$5,000 per tonne from their lows and improving economics for competing projects. Higher nickel prices and tighter supply conditions have concentrated investor interest on the limited number of Western sulfide projects capable of reaching production before 2030.

Canada Nickel combines exposure to a large Western sulfide nickel deposit with access to government-backed financing. Crawford reports a post-engineering after-tax net present value of US$2.8 billion at an 8% discount rate, an internal rate of return of 17.6%, a first-quartile C1 cash cost of US$0.39 per pound, and an all-in sustaining cost of US$1.54 per pound. The company's US$2.5 billion funding plan relies heavily on non-dilutive government funding and strategic investors, reducing the need for large-scale equity issuance. Investors should also consider financing risk, including a US$32 million facility repriced to 15% per annum, illustrating that access to capital remains costly despite government support.

Mark Selby, Chief Executive Officer of Canada Nickel, linked growing offtake interest to the limited number of Western sulfide projects capable of reaching production before 2030:

"We're now one of the few projects expected to come online before 2030. That has increased interest from customers looking to secure non-Indonesian supply through offtake agreements."

What Could Break the Non-China Processing Thesis

The energy transition is increasingly being shaped by processing capacity rather than resource ownership because refining has become more concentrated even as mined supply diversifies. The 86% concentration level highlights why Western governments are funding alternative supply chains and why refining assets outside China can command strategic value from investors, customers, and policymakers. Government support now extends beyond commodity prices and includes stockpiles, offtake agreements, equity investments, and development financing designed to build long-term processing capacity. If refining concentration remains high and government support continues, companies that can supply refined, traceable, non-China-exposed material through integration, by-product recovery, recycling, or large sulfide deposits are likely to attract a greater share of strategic capital and customer demand.

The Investment Thesis for Critical Mineral

- Refining concentration, not resource ownership, has become the key constraint. With the top three refining nations controlling 86% of supply across major battery and critical minerals, processing capacity outside China is increasingly becoming the scarce asset attracting capital and policy support.

- Government capital is reshaping project economics. Stockpiles, development finance, strategic offtakes, and direct investment are lowering financing barriers for projects that expand non-China processing capacity while creating new forms of policy-driven demand.

- Integrated processing platforms may command strategic value. Companies that combine multiple stages of production and refining can offer greater supply security, making them more attractive to customers, governments, and strategic investors.

- By-product recovery offers a capital-efficient route to critical minerals exposure. Recovering strategic metals from existing operations can improve project returns without requiring a new mine, standalone refinery, or major permitting process.

- Recycling provides a domestic source of refined supply. High-recovery recycling projects can bypass mine development entirely while reducing exposure to resource depletion, permitting timelines, and mining-jurisdiction risk.

- Western sulfide nickel remains one of the few geology-driven scarcity opportunities. Indonesia's dominance of global nickel supply and supply-discipline measures have increased interest in the limited number of Western sulfide projects capable of delivering battery-grade nickel before 2030.

Refining, rather than mining, has become the main constraint in critical mineral supply chains, with the top three refining nations controlling 86% of supply across key battery and critical minerals in 2024. Government funding, stockpiles, offtake agreements, and strategic investment are directing more capital toward non-China processing capacity, increasing the value investors place on projects capable of producing refined, traceable material. Energy Fuels, Sovereign Metals, Lifezone Metals, and Canada Nickel demonstrate different approaches to the same investment theme, but none should be viewed as recommendations and all remain subject to the risks outlined above. As long as refining remains concentrated, processing capacity outside China is likely to retain strategic importance for governments, customers, and investors.

TL;DR

The critical minerals bottleneck has shifted from mining to refining. The IEA reports that the top three refining nations controlled 86% of supply across key battery and critical minerals in 2024, while China is projected to retain dominant market share in several processing markets through 2035. Export controls, government stockpiles, development finance, and strategic offtake agreements are directing capital toward non-China processing capacity.

FAQs (AI-generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed