Reserve Diversification & 244 Tonnes of Central Bank Buying Strengthen Gold-Equity Fundamentals

Reserve diversification and 244 tonnes of central-bank gold buying are supporting gold prices, margins, mine life, and producer cash flow.

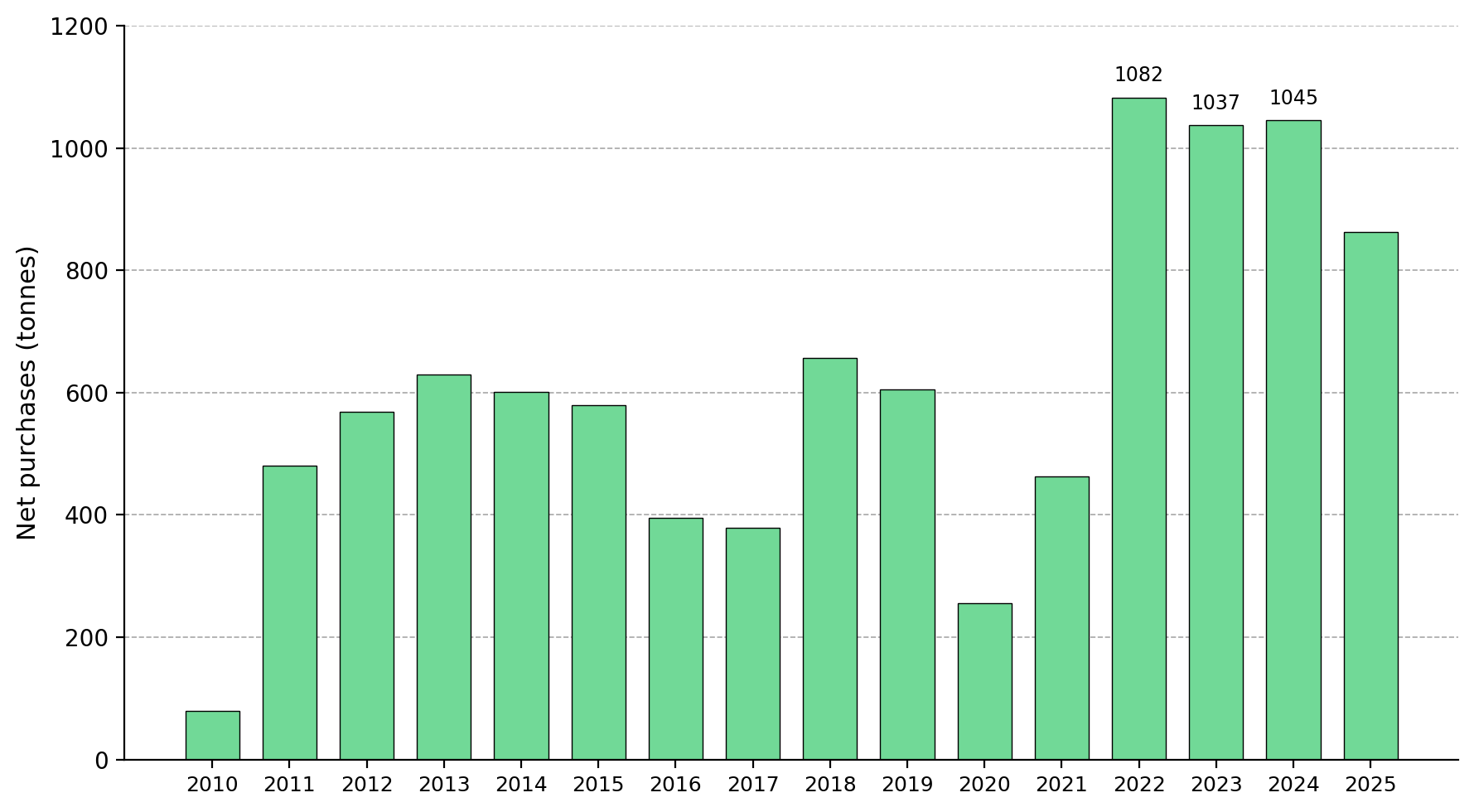

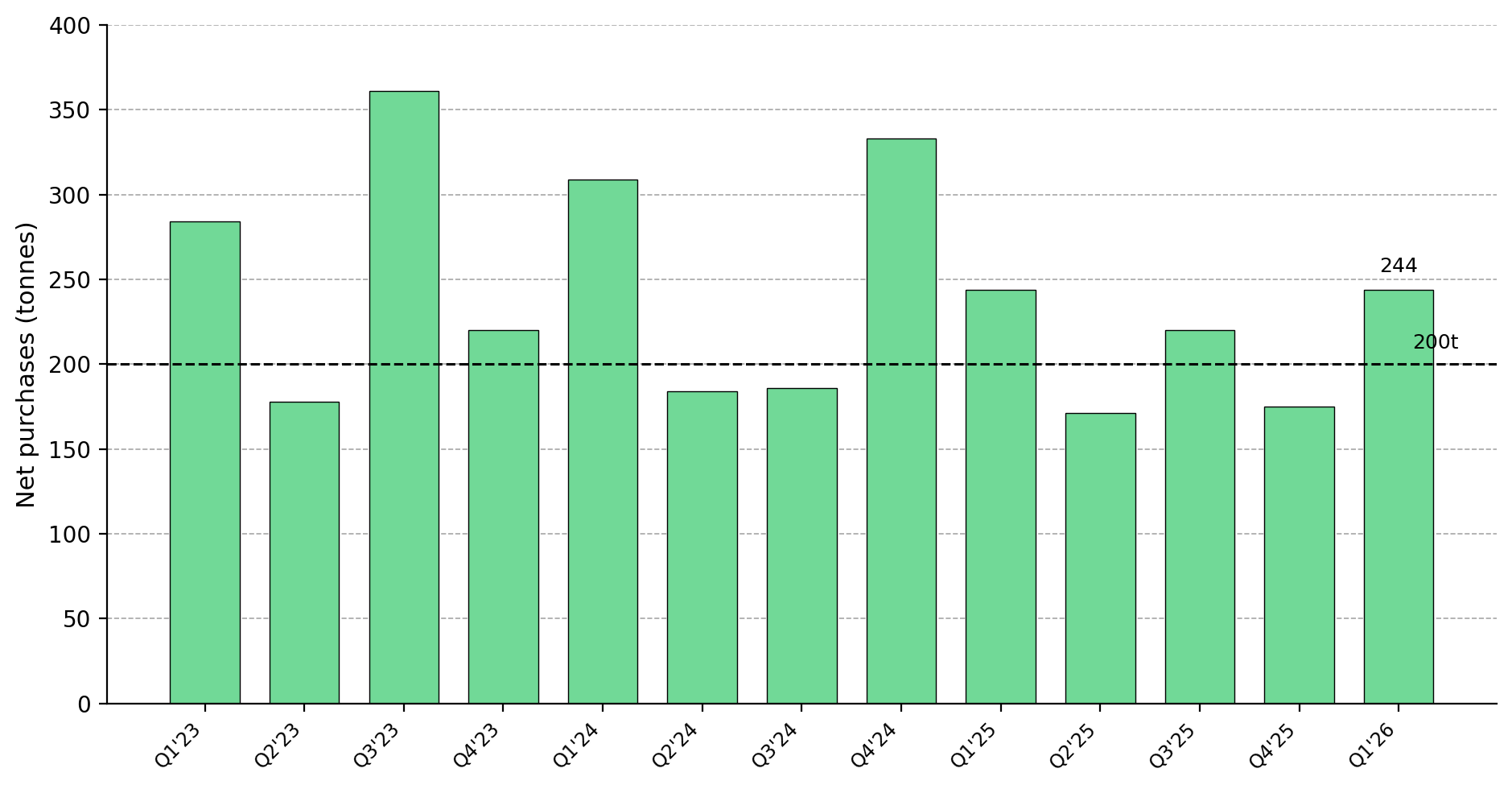

- Central banks purchased a net 244 tonnes of gold in the first quarter of 2026, according to the World Gold Council, exceeding 200 tonnes for the 10th time in the past 11 quarters and reinforcing a source of demand that supports gold prices across interest-rate cycles.

- This official-sector demand is largely insensitive to interest rates, the dollar, and inflation prints, distinguishing it from exchange-traded fund and jewellery flows and supporting a higher floor for gold prices across market cycles.

- A higher gold-price floor benefits producers first by increasing free cash flow, lowering economic cut-off grades, extending reserve life, and supporting valuation multiple expansion.

- Producers with disciplined costs and self-funding balance sheets convert higher margins into growth capital without diluting shareholders.

- Near-term headwinds include a hawkish Fed and a US dollar at a 13-month high, which influence short-term gold prices but not the demand from central banks supporting the market.

Dollar Exposure Concerns & Higher Gold Demand

Central banks are playing a larger role in setting gold prices in 2026 as official-sector purchases remain elevated. For most of the past two decades, gold prices were driven primarily by Western investors responding to changes in real yields, the US dollar, and risk sentiment. Those factors still influence gold prices, but sustained central-bank purchases now provide an additional source of demand. According to the World Gold Council's Q1 2026 Gold Demand Trends report, central banks added a net 244 tonnes of gold, exceeding both the previous quarter and the five-year quarterly average. The World Gold Council reported total gold demand reached a record $193 billion in Q1 2026, up 74% year-on-year. Central banks have purchased more than 200 tonnes of gold in 10 of the last 11 quarters, providing a source of demand that has remained in place across multiple market cycles.

Central-bank gold purchases accelerated after 2022 as reserve managers sought to reduce reliance on the US dollar. The National Bank of Poland was the largest single buyer in the quarter, adding 31 tonnes, while Uzbekistan and several Asian and emerging-market central banks also increased gold reserves. The People's Bank of China increased reported reserves to 2,313 tonnes, while J.P. Morgan's analysis of London over-the-counter and Swiss refinery flows indicated Chinese net imports reached 317 tonnes in the quarter, nearly triple the prior period. Central banks are increasing gold holdings to reduce reliance on the US dollar and limit exposure to sanctions and currency risks. Gold carries no counterparty risk, cannot be frozen by another government, and is accepted globally, making it attractive to reserve managers seeking alternatives to dollar assets.

Sustained Gold Demand & Lower Downside Risk for Producers

Producers make different capital-allocation decisions when higher gold prices are supported by sustained demand rather than a short-term market rally. More stable gold demand reduces the risk of prices falling below levels that support mine development and expansion decisions. The World Gold Council reported jewellery demand fell 23% year-on-year to 300 tonnes in Q1 2026, yet total demand still increased as official-sector and investment buying offset weaker consumer purchases.

Demand patterns in Asia and Western markets point to different sources of support for gold prices. According to the World Gold Council, Asian bar and coin demand reached 474 tonnes in Q1 2026, up 42% year-on-year and the second-highest quarterly total on record. US-listed gold exchange-traded funds recorded net outflows in March as rising real yields reduced demand from Western investors. Gold prices remained supported despite those outflows because physical buyers in Asia and central banks absorbed the selling.

Sustained central-bank demand reduces the risk of gold prices falling to levels that would undermine mine economics. When a producer commits to a stripping campaign, throughput expansion, or permitting program, project returns depend on future gold prices. Sustained demand reduces the risk of gold prices falling below all-in sustaining costs during a project's payback period, allowing more projects to meet return thresholds and support higher valuations. This thesis would weaken if central banks returned to sustained net selling on the scale seen in the late 1990s. Until that occurs, central-bank demand remains a source of support for gold prices.

Higher Gold Prices & Stronger Producer Economics

Sustained gold demand benefits producers through higher cash flow, lower cut-off grades, longer mine lives, and higher valuation multiples. Higher gold prices lower cut-off grades, allowing more mineralized material to be mined profitably, while extending reserve and resource life by making lower-grade material economic. Higher cash flow and longer mine lives can support higher valuation multiples, including enterprise value per ounce and EBITDA-based metrics, and producers benefit first because they sell ounces at current gold prices rather than future prices.

Margin Expansion & Reduced Dilution Risk

In the first quarter of 2026, Integra Resources sold 12,518 ounces at an average realized price of $4,854 per ounce and generated mine operating earnings of $24.9 million at a 40% operating margin, up from 27% a year earlier. Higher realized gold prices increased Florida Canyon's operating margin from 27% to 40% despite no change in the mine's operating footprint. George Salamis, President and Chief Executive Officer of Integra Resources, outlines how current gold prices could help fund the DeLamar project without significant dilution:

"If gold prices remain at current levels, we will have a robust enough treasury to fund the equity contribution required for the DeLamar project build. We could effectively reach the finish line without major dilution."

Free Cash Flow & Self-Funded Growth

Serabi Gold generated approximately $30 million in cash in 2025, retired its remaining debt, and ended Q1 2026 with roughly $65 million in cash, all funded from operations without issuing equity. Mike Hodgson, Chief Executive Officer of Serabi Gold, discusses how higher gold prices are supporting self-funded growth:

"We are generating enough cash to fund our growth plans from operating cash flow. We are not seeking additional capital from investors or raising debt. Higher gold prices are increasing revenue, and that additional revenue is flowing directly to the bottom line."

Higher Gold Prices & Resource Growth

Sustained gold demand affects both current cash flow and the value of undeveloped ounces. Higher gold prices increase the value of undeveloped ounces by making lower-grade and earlier-stage material economic. Lower cut-off grades can add previously uneconomic mineralization to resources, support satellite deposit development, and extend mine life. Longer mine lives and larger resource bases can support higher valuations for producers and developers.

Resource Growth & Mine-Life Expansion

West Red Lake Gold Mines achieved commercial production at its Madsen mine in 2025 and operates in Ontario's Red Lake district, which has produced more than 20 million ounces historically. The company controls a 47-square-kilometer land package centred on the Madsen processing hub and has begun a fully funded 4,000-meter drill program at the Starratt-Olsen deposit, 1.1 kilometers southwest of Madsen, which historically produced about 164,000 ounces at 6.17 grams per tonne between 1948 and 1956. Shane Williams, President and Chief Executive Officer of West Red Lake Gold Mines, explains how higher gold prices reduce the production rate required to cover operating costs:

"The previous operator required average gold production of around 4,000 ounces per month to break even. Gold prices are now roughly double what they were at that time, giving us more flexibility during the ramp-up. At Madsen, production of 2,000 to 2,500 ounces per month covers operating costs."

Production Growth & Project Economics

i-80 Gold generated approximately $43.8 million of revenue from 8,857 ounces produced at Granite Creek in Q1 2026. The investment case depends on production growth, with the company targeting an increase from under 50,000 ounces per year to roughly 600,000 ounces per year by the early 2030s across a Nevada portfolio feeding the Lone Tree plant. Lone Tree is a brownfield processing facility designed to improve recovery from refractory ore. The company is targeting recovery rates of roughly 92% at Lone Tree, up from a 55% to 60% third-party payability rate, with first gold pour targeted for late 2027. Paul Chawrun, Chief Operating Officer of i-80 Gold, discusses how higher gold prices increase the cash-flow potential of the Lone Tree hub:

"At $3,000 gold, we estimated Lone Tree could generate approximately $150 million to $200 million in annual net cash flow. At current gold prices, the potential cash flow is substantially higher. Lone Tree is just the first launch pad."

Higher Rate Expectations & Gold Price Support

Near-term gold prices are being influenced by higher US rate expectations, while sustained central-bank demand continues to support the market. On June 17, 2026, the Fed under Chair Kevin Warsh held rates at 3.50% to 3.75% but raised its median year-end 2026 projection to 3.8% from 3.4%, with half of policymakers projecting at least one additional hike. The dollar index pushed to a 13-month high and futures markets implied roughly a 77% probability of a December hike. Goldman Sachs cut its year-end gold target to $4,900 per ounce on June 19 after removing 2026 rate cuts from its base case, while J.P. Morgan maintained a $6,000 target and Wells Fargo and Deutsche Bank remained within a similar range. The difference between these forecasts reflects varying assumptions about future interest rates and Western investment demand rather than central-bank gold purchases.

The key near-term data release is the May core PCE index, the Fed's preferred inflation gauge, due June 25, with the Cleveland Fed nowcast at 3.3%. If core PCE exceeds expectations, rate-hike expectations could strengthen, the dollar could remain firm, and tactical gold demand could weaken. If it prints soft, the case for a hike weakens and Western fund buyers may return, supporting a move toward the upper end of the recent range. The data may influence short-term gold prices, but it does not change the central-bank demand supporting the market.

Interest-rate cycles have historically reversed within two to four years. Official-sector gold buying has continued for more than three years through rate hikes, rate cuts, conflicts, and a ceasefire, and the World Gold Council reported purchases remained above the five-year average in Q1 2026 despite record prices. Interest-rate expectations continue to influence short-term gold prices. Sustained central-bank purchases continue to provide support for gold prices during periods of weaker investor demand.

The Investment Thesis for Gold

- Central banks purchased a net 244 tonnes of gold in Q1 2026, exceeding the five-year average and extending a streak above 200 tonnes in 10 of the last 11 quarters, providing a source of demand that supports gold prices through changing interest-rate cycles.

- Higher gold prices lower cut-off grades at producing mines, converting previously uneconomic material into viable ounces, extending mine life, and supporting higher enterprise value per ounce.

- Producers with disciplined cost structures can convert higher margins into free cash flow for reinvestment, debt reduction, and shareholder returns.

- Producers funding growth from operating cash flow can advance throughput expansions and resource programs without equity dilution, a key consideration for institutional investors.

- Resource-growth strategies built around district-scale processing hubs benefit from higher gold prices, as each resource addition increases ounces that can be developed through existing infrastructure.

- Pre-scale producers with large project portfolios and proven financing capacity benefit when higher gold prices make net present value assumptions more defensible.

- Key risks include a sustained Fed hiking cycle, a stronger US dollar, and permitting or execution delays, all of which could reduce returns from gold equities.

Central-bank demand has become a more important driver of gold prices than in previous cycles. Central banks bought a net 244 tonnes of gold in Q1 2026 as part of reserve-diversification strategies, a form of demand that is less sensitive to inflation data and Fed policy projections. This increase in gold's share of central-bank reserves has supported demand through changing interest-rate and geopolitical cycles. Producers benefit through wider margins, lower cut-off grades, longer mine lives, and stronger balance sheets, while developers can evaluate projects against higher and more stable gold prices. Interest-rate expectations continue to influence short-term gold prices, but central-bank demand remains a source of support during periods of market weakness.

TL;DR

Central banks purchased a net 244 tonnes of gold in Q1 2026, extending a multi-year buying trend driven by reserve diversification rather than short-term market conditions. This demand has helped support gold prices despite ETF outflows and a stronger US dollar, improving producer economics through higher margins, stronger cash flow, longer mine lives, and lower cut-off grades. Companies generating cash at current gold prices are funding growth projects without significant dilution, while developers benefit from stronger project economics and more defensible valuation assumptions. Although higher Fed rate expectations may create near-term volatility, sustained central-bank demand continues to provide support for gold prices and gold-equity fundamentals.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

.jpg)

%20(1).jpg)

.jpg)

Stay Informed