Rising Real Rates, Geopolitical Risk & Capital Rotation into Platinum: Why PGM Markets Are Repricing Despite Structural Deficits

Platinum markets are mispriced by macro pressure, not fundamentals, structural deficits, rising institutional flows, and strong demand signal upside potential.

- Platinum is attracting renewed institutional flows, with CME options volumes rising approximately 35% month-to-date, indicating diversification demand driven by macro volatility rather than speculative positioning.

- Higher real interest rates and geopolitical tensions are suppressing near-term precious metals prices while simultaneously driving capital rotation into platinum group metals (PGMs), creating a dislocation between price and fundamentals.

- Structural supply constraints anchored in South Africa and Russia continue to underpin long-term deficits, with the World Platinum Investment Council (WPIC) projecting sustained above-ground stock depletion through the medium term.

- Platinum's dual role as a monetary hedge and industrial input for hydrogen and automotive applications is repositioning it relative to gold and silver within institutional commodity allocations.

- Development-stage assets in alternative jurisdictions, particularly Brazil, are gaining strategic relevance as investors prioritize supply chain diversification and jurisdictional optionality in their portfolio construction.

A Market Repricing Driven by Macro Forces

Platinum is trading near multi-year lows versus gold, yet options activity diverges from that signal. CME data shows volumes up approximately 35% month-to-date, consistent with institutional positioning rather than capitulation. This gap between weak spot prices and rising derivatives activity is the defining feature of the current PGM market.

Elevated real rates and a strong US dollar have pressured non-yielding assets, pushing gold and silver lower. Platinum is subject to the same pressure, but tightening supply fundamentals and stable industrial demand have created a growing disconnect between price and underlying value that long-term investors are beginning to reflect in their positioning.

This analysis examines how macro forces are shaping PGM pricing, the structural supply constraints underpinning the deficit case, and the implications for investors seeking leveraged exposure to a potential platinum re-rating.

Real Rates, USD Strength & Commodity Repricing

The relationship between real interest rates and precious metals pricing is direct and well-documented. When real yields rise, the opportunity cost of holding non-yielding assets increases and capital reallocates toward interest-bearing instruments. The Federal Reserve's sustained restrictive stance through 2024 and into 2025, driven by persistent core inflation, has kept the 10-year real yield above levels consistent with commodity bull markets. The US dollar index has remained elevated as a consequence, compressing dollar-denominated commodity prices across the board.

For PGMs specifically, this macro suppression has driven a wedge between price and fundamental value. Platinum is down approximately 13 to 14% year-to-date as of mid-2025, a move that reflects macro-driven liquidation rather than demand destruction. Managed money net long positions in platinum futures have declined sharply, consistent with broad commodity de-risking rather than sector-specific deterioration.

Monetary Policy and Geopolitical Inflation Are Driving Near-Term PGM Volatility

Market expectations for Federal Reserve rate cuts continue to be deferred as core inflation remains elevated, while policy divergence with the European Central Bank has strengthened the US dollar and pressured commodity pricing. Higher real yields increase the opportunity cost of holding non-yielding assets, keeping macro forces, not fundamentals, as the dominant driver of short-term PGM price direction.

Geopolitical tensions in the Middle East and persistent energy market disruptions are sustaining inflation, limiting central bank flexibility. This creates a structural contradiction: geopolitical risk strengthens the long-term case for commodities, yet reinforces restrictive monetary policy that suppresses near-term prices. For platinum, this is widening the gap between current price weakness and its medium-term demand outlook, a gap that has historically preceded re-rating cycles.

Capital Rotation into Platinum Reflects Institutional Repositioning, Not Tactical Hedging

The approximately 35% increase in CME platinum options volume reflects a reallocation within commodity portfolios, not purely hedging activity. As gold and silver underperform in a high real-rate environment, capital is moving into platinum, driven by its combination of monetary characteristics and structural industrial demand. This represents a shift away from autocatalyst-driven pricing toward a more diversified demand framework that systematic allocators are beginning to price in.

Platinum's dual-use profile underpins this shift. It functions both as a store of value and as a critical industrial input in hydrogen fuel cells, hybrid vehicle catalysts, and chemical processing. This demand base reduces correlation with both gold and base metals, creating a structural demand floor that is relevant to systematic commodity allocators building resilience across macro cycles

The increase in volume is broad across strikes and maturities, consistent with institutions building upside exposure through optionality rather than hedging downside risk. This pattern is consistent with early-stage positioning ahead of a potential recovery, historically the phase that offers the most favorable entry point for long-duration investors.

Why the Long-Term Thesis Remains Intact

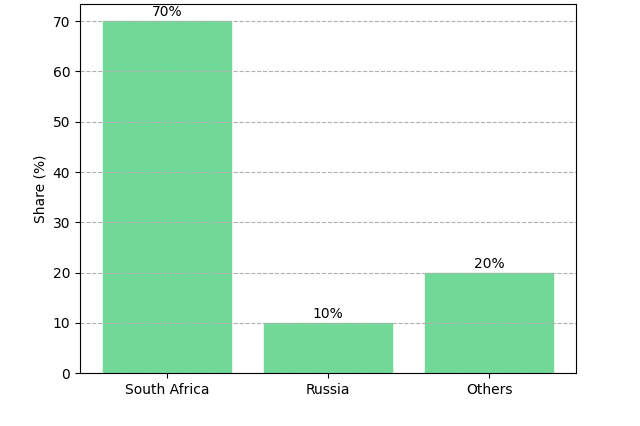

Approximately 70% of platinum output comes from South Africa, where power instability, rising costs, and declining ore grades constrain production. A further approximately 10% comes from Russia, where sanctions create supply uncertainty. Limited greenfield investment and development timelines of 8 to 12 years mean few new projects can offset depletion at existing operations.

Unlike oil or copper, platinum production cannot respond quickly to price signals due to long development cycles, and recycling volumes remain insufficient to close supply gaps. Deficits persist as a result, and prices must eventually adjust to reflect physical scarcity.

WPIC forecasts continued market deficits, with above-ground stocks declining after masking shortages in recent years. As inventories draw down, pricing will increasingly reflect physical availability rather than financial positioning, the inflection point that current options activity suggests institutional investors are beginning to anticipate.

Price Weakness vs Fundamental Strength

The approximately 13 to 14% year-to-date decline in platinum prices, despite tightening supply and stable industrial demand, reflects macro forces overriding fundamentals. Comparable patterns appeared in iron ore in 2015, uranium in 2017, and palladium in 2017, where macro-driven weakness preceded sharp re-ratings as supply constraints reasserted.

Automotive use, approximately 40% of total demand, is supported by hybrids, which require similar catalytic loadings to internal combustion engines. Industrial demand across glass, chemicals, and electronics is stable. The current price weakness is driven by financial liquidation, not demand erosion.

At the equity level, EV/oz multiples for developers and explorers have compressed alongside spot prices. If prices recover, both the commodity price and EV/oz multiples tend to expand, producing leveraged returns. Current valuations reflect macro risk, not project fundamentals, a distinction that defines a cyclical entry point rather than structural impairment.

Relevance of Non-Traditional Jurisdictions

Platinum's concentrated supply base in South Africa and Russia means that disruptions, from power outages to geopolitical events, can trigger outsized price moves in an already supply-constrained market. This has directed investor attention toward alternative jurisdictions. Brazil is emerging as a credible option, supported by mining reforms, established infrastructure, skilled labor, and policy positioning to attract critical minerals investment.

Scale, Cost Efficiency & Development Pathway

ValOre Metals is advancing the Pedra Branca palladium-platinum project in Brazil's Ceará state. The project carries an inferred resource of 2.2 million ounces at 1.08 g/t 2PGE+Au, composed of approximately 60% palladium and 40% platinum, across a 50,000-hectare land package with multiple zones open for expansion. Discovery costs remain below $6/oz, and the resource has doubled since acquisition.

On the resource scale and composition, Nick Smart, Chief Executive Officer of ValOre Metals, states:

“2.2 million ounces at 1.08 grams per ton, mixed PGEs, primarily palladium (~60%) and about 40% platinum. It’s a large land package, covering approximately 50,000 hectares.”

Metallurgy has historically constrained low-grade PGM projects, but at Pedra Branca, testwork on weathered ore supports bioleaching as a viable and potentially transformative route. Recoveries in the high-70% range, combined with heap leach potential from near-surface material, suggest a competitive cost profile. A PEA is targeted for end-2026, providing clarity on NPV and IRR relative to the current valuation.

Development Assets vs Producers: Risk-Reward in the Current Macro Cycle

The PGM investment landscape divides between established producers and development-stage assets. Producers such as Impala Platinum and Sibanye Stillwater carry operating cash flow and balance sheet resilience, but face constrained growth from aging assets, rising costs, and infrastructure limitations in South Africa. Development assets carry higher execution risk, across financing, permitting, and metallurgy, but offer materially greater exposure to a recovery in platinum prices.

That leverage operates on two levels. Rising platinum prices directly increase the in-situ value of defined resources, while EV/oz multiples expand as capital re-enters the sector. Historically, an approximately 20% move in the underlying commodity has translated into 40 to 60% re-rating in development-stage valuations, as improving project economics coincide with renewed investor risk appetite. This convexity differentiates developers from producers in a recovery phase.

Institutional capital typically lags the commodity cycle by 12 to 18 months, waiting for confirmation of price direction before allocating to higher-risk assets. The recent increase in platinum options activity suggests early-stage positioning may already be underway. Investors entering ahead of that institutional flow assume execution risk but gain exposure to the valuation expansion that accompanies a broader sector reclassification.

Risk Factors & Market Constraints

Elevated real interest rates, sustained US dollar strength, and the risk of a global growth slowdown could extend the current period of price suppression. If real yields remain above approximately 2%, capital will continue to favor fixed income over commodities, while a strong dollar will exert additional downward pressure on platinum pricing regardless of physical demand levels.

The long-term demand outlook faces headwinds from the rise of battery electric vehicles, which reduce autocatalyst demand over time. Palladium-to-platinum substitution and emerging demand from hydrogen fuel cell technologies provide partial offsets, reinforcing platinum's relative positioning within the PGM complex.

At the project level, development-stage assets introduce execution risks independent of commodity prices. Financing constraints in a high-rate environment, permitting timelines, and the challenge of scaling metallurgical processes from testwork to commercial operations remain key uncertainties. For Pedra Branca, advancing from metallurgical validation to PEA and ultimately feasibility will depend on demonstrating consistent recoveries at scale while progressing through Brazil's regulatory framework.

The Investment Thesis for Platinum Group Metals

- For investors evaluating commodity allocation in a late-cycle macro environment, the PGM sector presents a convergence of macro, structural, and company-level factors. The following elements define the core case.

- The macro-driven price dislocation has compressed EV/oz multiples to levels that reflect financial liquidation risk rather than fundamental project impairment, providing asymmetric upside when real yields decline and capital returns to the sector.

- Structural supply constraints embedded in South African and Russian production geography cannot be resolved within the investment horizon of current market participants, ensuring that fundamental deficit conditions persist regardless of near-term price movements.

- Platinum's dual demand profile, spanning monetary reserve characteristics and industrial applications in hydrogen, automotive, and chemical processing, provides demand resilience that single-use commodities cannot match, reducing the risk of prolonged demand destruction.

- Development-stage assets in jurisdictions outside South Africa and Russia offer both commodity price leverage and jurisdictional diversification, two return drivers that compound positively when geopolitical risk premiums are elevated.

- Near-term catalysts at the project level, including the Pedra Branca PEA targeted for end-2026, provide defined value inflection points at which EV/oz multiples can re-anchor to discounted cash flow metrics rather than sentiment-driven discounts.

Real interest rates, dollar strength, and broad commodity de-risking have pushed platinum prices below where the fundamentals sit, and none of those conditions are permanent. The WPIC's supply deficit is not narrowing. Industrial demand in hydrogen and hybrid automotive applications is not contracting, and CME options data shows institutional positioning shifting to reflect these conditions.

When those conditions turn, unresolved supply deficits, recovering institutional flows, and compressed EV/oz multiples will push a re-rating. Development assets in solid jurisdictions with defined resources, proven metallurgy, and clear timelines carry the most upside when that happens.

The main risk is that the pressure runs longer than most expect. CME options data suggests institutional capital is already accounting for that by sizing positions carefully and waiting for catalyst-driven entry points.

TL;DR

Platinum group metals (PGMs) are currently mispriced due to high real interest rates and a strong US dollar. Despite a ~13-14% decline in platinum prices, structural supply deficits (driven by concentrated production in South Africa and Russia) and stable industrial demand remain intact. Institutional investors are beginning to reposition, as reflected in rising CME options activity, signaling early-stage accumulation ahead of a potential re-rating. This environment creates a disconnect between price and value, offering asymmetric upside, particularly in development-stage assets in alternative jurisdictions like Brazil, which provide both leverage to rising prices and diversification benefits.

FAQs (AI generated)

Platinum prices are being suppressed primarily by macroeconomic forces rather than supply-demand deterioration. Elevated real interest rates increase the opportunity cost of holding non-yielding assets like precious metals, while a strong US dollar compresses commodity prices globally. This has triggered broad-based liquidation across commodities, including PGMs. However, underlying fundamentals, such as constrained supply and steady industrial demand, remain intact, creating a temporary dislocation between price and intrinsic value.

Institutional capital is rotating into platinum due to its dual role as both a monetary hedge and an industrial metal. Unlike gold and silver, platinum benefits from demand in hydrogen technologies, automotive catalysts, and industrial applications, which provides structural support. The rise in CME options volume (~35% month-to-date) indicates investors are building upside exposure rather than hedging downside risk, suggesting early positioning ahead of a potential price recovery cycle.

PGM supply is highly concentrated geographically, with around 70% coming from South Africa and ~10% from Russia. These regions face persistent challenges, including power instability, geopolitical risks, and declining ore grades. Additionally, long project development timelines (8-12 years) and limited new investment make supply inelastic. As a result, deficits are expected to persist, with above-ground inventories gradually depleting, eventually forcing prices to adjust upward to reflect scarcity.

Development-stage PGM assets offer higher risk but significantly greater upside leverage compared to established producers. When platinum prices recover, these assets benefit not only from rising commodity prices but also from expanding valuation multiples (EV/oz). Historically, modest increases in commodity prices have translated into disproportionately large equity re-ratings. In the current environment, compressed valuations driven by macro factors create a favorable entry point for investors willing to take on execution risk.

Brazil is gaining attention as a credible alternative to traditional PGM supply regions due to its stable regulatory environment, established mining infrastructure, and government support for critical minerals. Projects like Pedra Branca demonstrate the potential for scalable, cost-efficient development outside geopolitically sensitive regions. For investors, this offers both jurisdictional diversification and exposure to long-term supply deficits, aligning with broader portfolio strategies focused on resilience and geopolitical risk mitigation.

Analyst's Notes

Subscribe to Our Channel

Stay Informed