Higher US Interest Rates & Government Funding Shift Critical Mineral Equity Valuations as 2026 Rate-Cut Odds Fall Below 3%

Higher US interest rates are pushing critical mineral projects toward government funding, reshaping equity valuations and financing access.

- The Fed’s appointment of Chair Kevin Warsh on 15 May 2026 reduced market-implied odds of a 2026 rate cut to below 3%, according to CME FedWatch, raising financing costs for Western critical mineral projects as governments accelerate efforts to reduce dependence on Chinese supply chains.

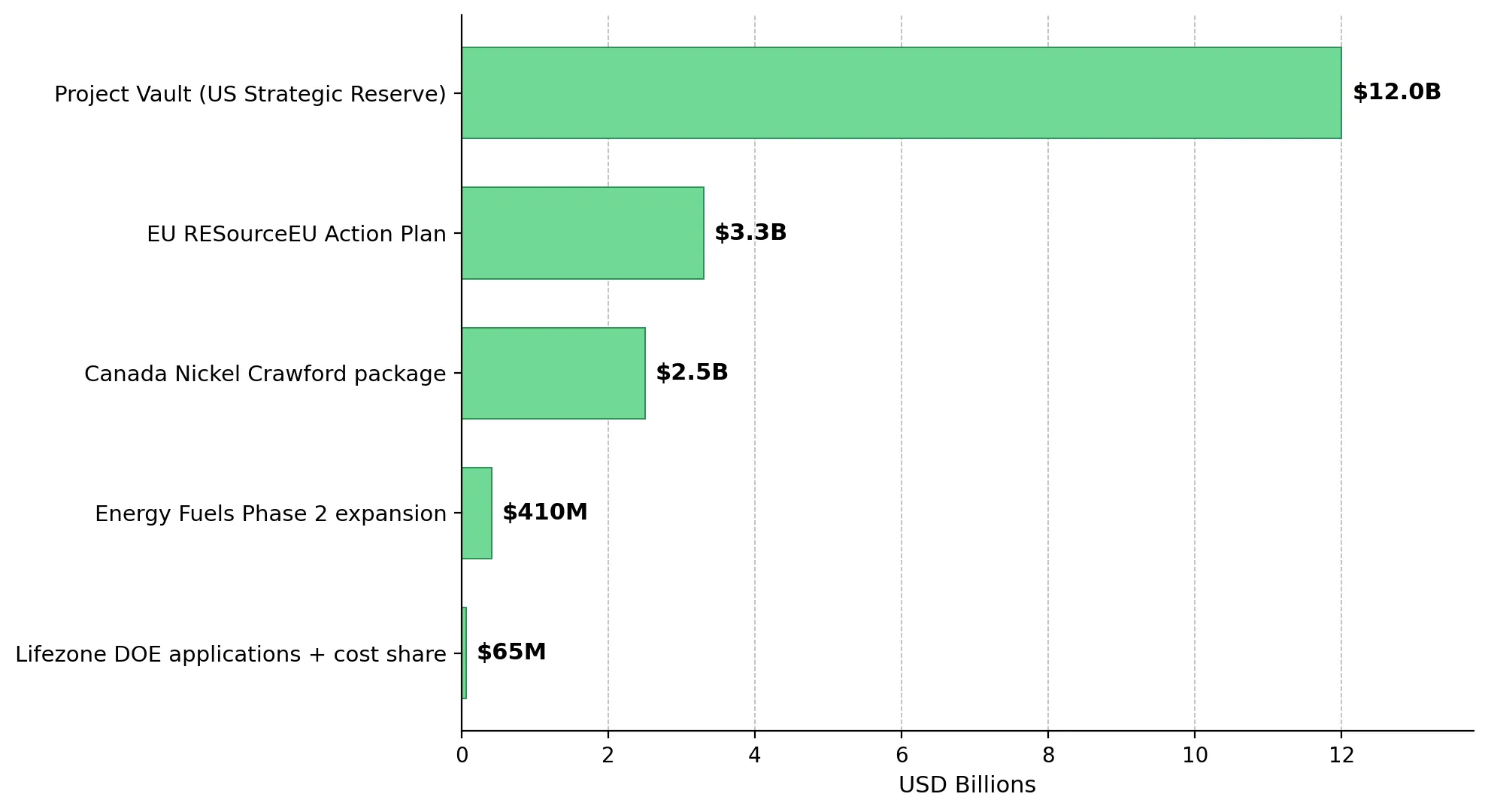

- The US, European Union, and allied governments are offsetting tighter private financing conditions through public funding and offtake agreements, including Project Vault’s $12 billion facility, US Export-Import Bank loans, US Development Finance Corporation due diligence programs, and supply agreements involving Mitsui, Samsung SDI, and Traxys.

- Government-backed funding and offtake agreements now provide more financing support for Western critical mineral projects than commercial bank lending.

- Access to government-backed financing now depends on existing cash flow, the quality of feasibility studies, and the level of technical and permitting documentation provided to allied lenders.

- Investors should prioritize financing credibility and funding access over headline net present value estimates.

Higher US Interest Rates Push Critical Mineral Projects Toward Government Funding

The Fed has held its policy rate at 3.50% to 3.75% since the 18 March 2026 Federal Open Market Committee meeting, while its Summary of Economic Projections raised 2026 Personal Consumption Expenditures inflation forecasts to 2.7%. Kevin Warsh’s confirmation as Fed Chair on 13 May 2026 reinforced expectations that interest rates will remain elevated through 2026. Chase Wealth, citing CME FedWatch data after Warsh’s confirmation, showed less than a 3% market-implied probability of a 2026 rate cut and increasing odds of another hike by year-end. Higher real interest rates reduce the discounted cash flow value of critical mineral projects, especially pre-revenue developers with large upfront capital requirements.

Project Vault and Offtake Accelerate Western Supply-Chain Financing

As private financing tightened, Western governments expanded public funding support for critical mineral projects. Project Vault launched on 2 February 2026 with $12 billion in funding, including a $10 billion US Export-Import Bank loan, to build a US Strategic Critical Minerals Reserve. The European Union also committed €3 billion through its RESourceEU Action Plan in December 2025, while advancing the amended Critical Raw Materials Act to accelerate domestic supply-chain financing and permitting. A 10 May 2026 Council on Foreign Relations analysis concluded that China retained significant control over critical mineral supply chains, reinforcing Western support for domestic and allied mining projects.

Sovereign Metals provides an early example of this shift. A February 2026 graphite marketing memorandum of understanding with Traxys could provide access to Project Vault demand, as Traxys was selected as one of three firms supplying the US Strategic Reserve, according to the company’s March 2026 quarterly report.

Sovereign Metals Chairman Ben Stokovich said the project’s low-cost profile could improve its competitiveness within Western graphite supply chains:

"China produces around 1.2 million tonnes of natural graphite annually, representing about 75% of global supply, at an average production cost of roughly $257 per tonne. Kasiya sits at the lower end of the global cost curve, which positions Sovereign Metals to remain profitable and competitive even in weaker graphite markets."

Offtake Agreements Replace Commercial Debt in Critical Mineral Financing

Since Kevin Warsh’s appointment reduced expectations for lower interest rates, offtake agreements have become a primary financing support for critical mineral developers. These agreements reduce demand risk for development finance lenders and provide contracted revenue that improves access to project financing. Between 2020 and 2024, most offtake agreements focused on securing competitive pricing, while current agreements prioritize long-term supply security for Western supply chains.

Contracted Uranium Cash Flow Funds Rare Earth Expansion

Energy Fuels operates the only conventional uranium mill in the US and holds six long-term utility contracts through 2032. In Q1 2026, the company sold 510,000 pounds of triuranium octoxide at an average realized price of $70.04 per pound, generating $35.7 million in uranium revenue against production costs of $23 to $30 per pound at Pinyon Plain. TradeTech assessed long-term triuranium octoxide contract prices at $93.00 per pound on 1 May 2026, supporting cash flow for Energy Fuels’ $410 million Phase 2 rare earth expansion. The project carried a $1.9 billion net present value in the January 2026 AACE Class 3 Bankable Feasibility Study.

Mark Chalmers, who served as Chief Executive Officer of Energy Fuels at the time of his recorded interview and was succeeded by Ross Bhappu effective 15 April 2026, articulated the cumulative financial scale linking the producing business to the next capital cycle:

"Uranium is now. We’ll provide guidance of up to 2.5 million pounds, which is greater than any other producer in the US. We’ve also completed the feasibility study for the Phase 2 expansion. Taken together, those assets represent a net present value approaching $4 billion."

Mitsui and Samsung SDI Offtake Agreements Support Critical Mineral Financing

Sovereign Metals signed a non-binding rutile offtake memorandum with Mitsui & Co. in March 2026 covering up to 70,000 tonnes per annum of rutile concentrate, or more than half of planned Phase 1 production. US Geological Survey data showed Japan supplied more than 70% of US titanium sponge imports in the first half of 2025, linking the agreement to US titanium supply chains. Canada Nickel is also assembling a targeted $2.5 billion Crawford funding package, including an expected $100 million tied to Samsung SDI’s offtake option, ahead of a federal permitting decision expected in early summer 2026.

Development Finance Institutions & Export Credit Agencies Fill the Mining Funding Gap

As higher interest rates reduce private project financing, Western critical mineral projects are relying more heavily on development finance institutions, export credit agencies, and government tax incentives. The World Bank’s 28 April 2026 Commodity Markets Outlook forecast a 17% increase in metals and minerals prices for 2026, improving the economic outlook for large-scale critical mineral financing. Goldman Sachs Research previously estimated global lithium mining investment requirements at $500 billion to $600 billion through 2040. With higher interest rates limiting private financing capacity, governments and state-backed lenders are increasing support for critical mineral projects.

US Government Financing Supports Critical Mineral Recycling & Processing

Lifezone Metals is pursuing support from multiple US government and development finance programs. According to its 30 April 2026 Q1 release, the company’s Simulus facility recovered up to 99% platinum, 99% palladium, and 95% rhodium from US-sourced spent automotive catalytic converters. The Simulus laboratory generated $1.2 million in third-party technical services revenue in Q1 2026, up from $0.2 million a year earlier. Lifezone Recycling US also submitted two US Department of Energy funding applications in January 2026 seeking $41.5 million in federal support alongside a $24 million private cost share, while the US Development Finance Corporation completed the public consultation phase for the broader portfolio.

Ingo Hofmaier, Chief Financial Officer of Lifezone Metals, framed the depth of Washington engagement that underpins the multi-channel positioning:

"We’re traveling to Washington frequently at the moment, and there’s strong dedication there. We’ve gone through the public consultation process with the US DFC, so the project is already relatively advanced in that context."

Financing Access Reshapes Critical Mineral Equity Returns Across Project Stages

Government-backed financing programs are favoring critical mineral developers with stronger financing and commercial profiles. Equity valuations now depend more on financing credibility and funding access than on headline project economics alone. Developers with existing cash flow, financeable feasibility studies, and advanced offtake agreements are attracting stronger investor interest.

Contracted Cash Flow Allows Producers to Fund Expansion Internally

Energy Fuels reported working capital of $956.6 million as of 31 March 2026, including $108.4 million in cash, $802.2 million in marketable securities, and $8.3 million in Q1 2026 operating cash flow from uranium sales. The company plans to fund its $410 million Phase 2 rare earth expansion internally rather than through external debt markets, reducing exposure to higher borrowing costs caused by current Fed policy.

Definitive Feasibility Study Projects With Offtake Support Attract Higher Valuations

Sovereign Metals reported a pre-tax net present value of $2.2 billion for the Kasiya project at an 8% discount rate, against $727 million in capital expenditure to first production, according to the Definitive Feasibility Study released on 16 April 2026. The project’s NPV-to-capex ratio was 3.0x. Even with rutile and graphite prices 25% below Definitive Feasibility Study assumptions, the project retains a pre-tax net present value of $913 million at the same discount rate and an internal rate of return of 15.2%. This downside resilience could support financing and commercial participation from institutions such as the International Finance Corporation and Mitsui.

Pre-Construction Developers Depend on Permitting and Financing Alignment

Canada Nickel is targeting a final federal permitting decision for the Crawford project in early summer 2026 while assembling a $2.5 billion funding package that includes Samsung SDI’s offtake option, Canadian flow-through tax structures, and government funding support. The Crawford Front-End Engineering and Design study reported an after-tax net present value of $2.8 billion at an 8% discount rate, a 17.6% internal rate of return, and a life-of-mine net C1 cash cost of $0.39 per pound, placing the project in the global first quartile of nickel cost producers. Lifezone Metals also reported pilot autocatalyst recovery rates of 99% for platinum and palladium and 95% for rhodium, while stating that engineering design and feasibility work for its platinum-group metals recycling project is nearing completion.

Execution Risk & Higher Interest Rates Threaten Government-Backed Critical Mineral Financing

Government-backed financing typically takes longer to secure than commercial bank debt because it requires additional policy, environmental, and compliance reviews. The primary investment risk is project timing and execution rather than the availability of Western government-backed funding. Investors should focus due diligence on three key risk categories.

Project Vault Procurement & Offtake Timelines Remain Unproven

The US Strategic Critical Minerals Reserve launched on 2 February 2026, leaving limited operating history for investors to evaluate. Large-scale procurement processes, offtake agreements, and delivery timelines under the reserve program have not yet been tested commercially. Traxys being selected as one of three procurement firms supports the reserve strategy, but the program has not yet produced priced multi-year supply contracts.

Permitting Delays Remain the Biggest Execution Risk for Critical Mineral Projects

Canada Nickel is targeting a final federal permitting decision for the Crawford project in early summer 2026. Sovereign Metals plans to submit its Environmental and Social Impact Assessment to the Malawi Environmental Protection Agency in Q2 2026, a key step toward project permitting. Energy Fuels said in its Q1 2026 release that the Vara Mada Project in Madagascar requires a fiscal and legal stability agreement with the Government of Madagascar.

Canada Nickel Chief Executive Officer Mark Selby said the project could become the first major mining development approved under Canada’s updated permitting framework:

"We’re the first mining project in Canada operating under the 2019 legislation to reach this stage. If we receive our permit in early summer, we would become the first mining project approved under the 2019 framework."

Higher US Interest Rates Continue Pressuring Long-Duration Critical Mineral Projects

If the Federal Funds rate remains at 3.50% to 3.75% beyond 2026, discounted cash flow valuations for long-duration critical mineral projects could decline further. CME FedWatch data currently shows rising market expectations for another rate increase rather than a cut. Government-backed financing can offset higher borrowing costs, but mainly for projects that meet the technical, environmental, and compliance standards required by development finance institutions such as the International Finance Corporation.

The Investment Thesis for Critical Mineral

- Investors now place greater value on financing credibility, government-backed support, and allied offtake agreements than on incremental improvements in project net present value.

- Producers with contracted revenue and positive operating cash flow are less exposed to higher borrowing costs because they can fund expansions internally.

- Developers with definitive feasibility studies, advanced International Finance Corporation engagement, and near-binding offtake agreements are attracting stronger equity valuations, particularly where projects also carry strategic-partner validation and high-confidence resources.

- Recycling and midstream processors supported by the US Department of Energy and US Development Finance Corporation can typically scale faster than greenfield mining projects.

- Pre-construction developers still face higher execution risk because permitting, financing, and offtake milestones must all align before production begins.

Since the Inflation Reduction Act, critical mineral valuations have shifted from focusing mainly on Chinese supply policy and commodity prices toward financing access. The key question is whether Western governments and development finance institutions can deploy programs such as Project Vault, International Finance Corporation financing, US Development Finance Corporation lending, and US Department of Energy funding quickly enough to offset tighter private financing conditions caused by higher US interest rates. Over the next 12 to 18 months, investors will likely differentiate between developers that meet government-backed financing standards and those still dependent on increasingly constrained private debt markets. Financing credibility is now a primary driver of critical mineral valuations.

TL;DR

Higher US interest rates and Kevin Warsh’s appointment as Federal Reserve Chair have sharply reduced expectations for 2026 rate cuts, increasing financing pressure on critical mineral developers. In response, Western governments are expanding public funding through Project Vault, export credit agencies, development finance institutions, and strategic offtake agreements involving companies such as Mitsui, Samsung SDI, and Traxys. The article argues that financing credibility now matters more than headline project economics, with investors favoring producers with existing cash flow, developers with financeable feasibility studies and strategic offtake support, and recycling or processing companies aligned with US government supply-chain priorities.

FAQs (AI-generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed