Silver Tiger Metals Races Toward 2027 Production With High-Grade Mexico Mine Build

Silver Tiger Metals is building Mexico's only new-permitted heap leach mine, targeting Dec 2027 first pour, with ~$1.7B combined NPV across heap leach and underground projects.

- Silver Tiger Metals has received its construction permit - the first issued to a foreign company in Mexico since 2019 - and is approximately 3.5 months into building a heap leach silver/gold mine at its El Tigre project in Sonora, with first doré pour targeted for December 2027.

- The heap leach project carries a standalone after-tax NPV of ~$800 million USD and a 92% IRR at conservative prices (~$70 silver / $4,200 gold), generating approximately $100 million USD in annual after-tax net cash flow over a 10-year initial mine life.

- A separate PEA for an underground mine was released in January, showing a 15-year mine life, ~$830 million NPV, and 110% IRR - with the two projects combined representing a theoretical $1.7–1.8 billion NPV and ~$200 million in annual after-tax cash flow.

- A critical structural advantage distinguishes El Tigre: the underground ore body is entirely outside the footprint of the heap leach for the surface mine, allowing both operations to run concurrently - an unusual feature in Mexican mining where sterilisation of underground ore beneath heap leach pads is a common constraint.

- The exploration team has resumed drilling on northern veins 700 metres outside the current mine plan, targeting an additional ~3 million tonnes at approximately 350 g/t silver equivalent, which could expand the underground resource from 4 million to 7 million tonnes and materially alter the mine plan.

Silver Tiger Metals is at an inflection point. After years of navigating one of the world's most difficult mining permitting environments, the company is now actively constructing its heap leach mine at the El Tigre project in Sonora, Mexico. With a construction camp operational, earthworks underway, and a first doré pour targeted for December 2027, Silver Tiger is transitioning from a development-stage company into a near-term producer. In a recent interview, CEO Glenn Jessome outlined the construction progress, underground project economics, debt financing strategy, and a renewed exploration push - all set against a backdrop of silver at approximately $70 per ounce and gold near $4,200.

A Permit That Took Years to Secure

The foundation of Silver Tiger's position is its operating permit - the first issued to a foreign mining company in Mexico since 2019. That permit, for a surface heap leach mine, was years in the making. The company received it after a prolonged wait that began with Mexico's permit freeze following stricter government oversight of the mining sector. The significance of this cannot be understated: no comparable project has received this level of regulatory clearance in the country over the same period, creating a material barrier to entry for would-be competitors in the region.

With that permit in hand, and following a $60 million bought deal financing completed near the top of the January market - which brought the company's cash position to approximately $100 million USD - the board authorised construction. The company appointed KCA, an EPCM (Engineering, Procurement, and Construction Management) contractor, which previously handled general engineering work for the project, as the lead construction firm. The COO overseeing the build, Francisco Albelais, was previously responsible for constructing two large heap leach projects in Sonora for Argonaut Gold.

Heap Leach Construction: On Schedule and Moving

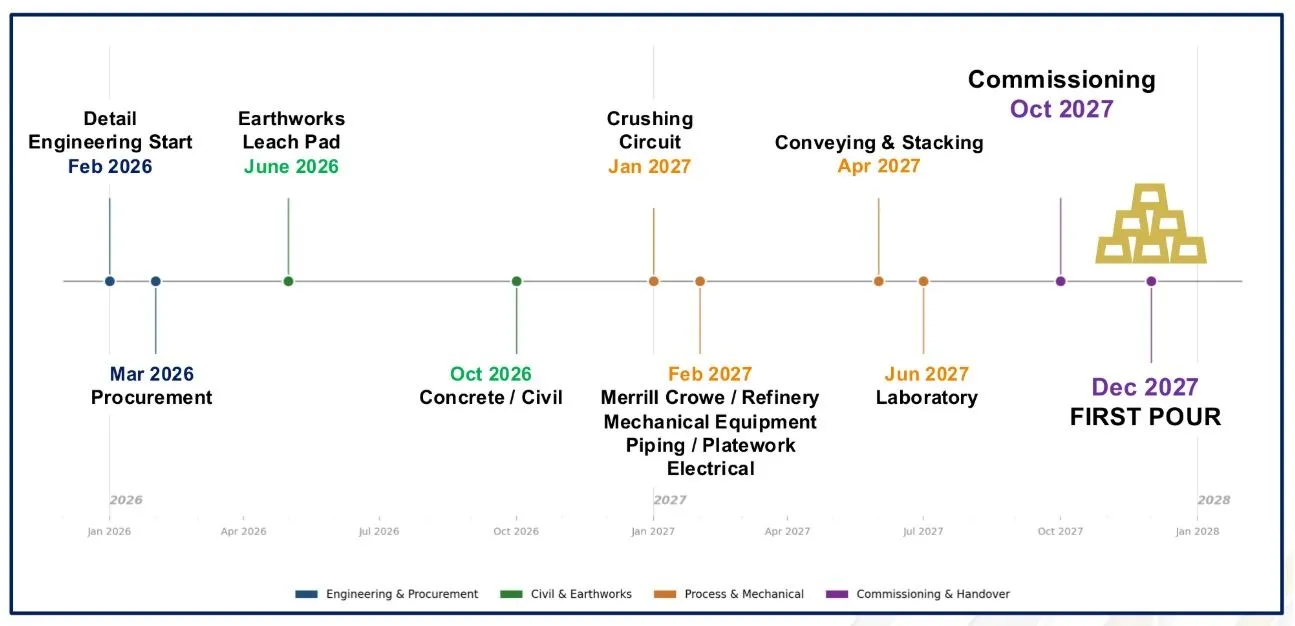

The build is approximately 3.5 months old. A 50-person construction camp is fully operational, with water and sewage infrastructure in place. KCA personnel and the internal build team are on-site daily. Long-lead procurement items are in progress, with earthworks, land clearing, and leach pad construction beginning in June 2026. The 46-kilometre access road - previously used to haul the underground mill from Canada - is being upgraded to handle mine traffic.

The forward schedule is well-defined: concrete and civil works are targeted for October 2026; the crushing circuit for January 2027; the Merrill-Crowe refinery for February 2027; stacking operations to begin April–May 2027; commissioning in October 2027; and first pour in December 2027. The project team reports they are currently ahead of the Gantt chart schedule.

Heap Leach Economics: A Standalone Case

At current spot prices of approximately $70 silver and $4,200 gold, the heap leach project generates a standalone after-tax NPV of approximately $800 million USD, with a 92% IRR and a payback period of roughly 1.1 years. Annual after-tax net cash flow is projected at approximately $100 million USD over the initial 10-year mine life - at which point the company intends to push back the pit to recover the remaining 40% of ore not yet optimised in the current plan. The deposit is open in both directions.

Importantly, the current mine plan uses only 60% of the material within the optimised pit shell. The remaining 40% - retained for a later pushback - extends the project's potential life and cash generation beyond the 10-year baseline. The low capital intensity of heap leach processing relative to conventional milling, combined with the project's grade profile, underpins the high-margin economics.

Underground Project: Door Number Two

In January 2026, Silver Tiger released a Preliminary Economic Assessment (PEA) for an underground mine at El Tigre. The underground resource is estimated at 4 million tonnes grading approximately 430 g/t silver equivalent - described as among the highest grades of any underground project on the books in Mexico today.

The company already owns and has transported to site an 800-tonne-per-day mill, originally sourced from Canada, which matches the capacity assessed in the PEA and aligns with the existing historic underground permit. At current prices, the underground PEA returns a 15-year mine life, a standalone NPV of approximately $830 million, a 110% IRR, and approximately $100 million USD in annual after-tax cash flow.

While the two studies are technically stand-alone and cannot be formally combined under securities rules, Jessome noted that nothing prevents placing them side by side. Viewed together, the heap leach PFS and the underground PEA imply a combined NPV of approximately $1.7 to $1.8 billion USD at current prices, with the two operations together generating close to $200 million USD in annual after-tax net cash flow.

The next step is advancing the underground to a Prefeasibility Study (PFS), which the company intends to pursue as quickly as possible.

Interview with Glenn Jessome, President & CEO of Silver Tiger Metals Inc.

A Structural Advantage: Running Both Mines Simultaneously

A distinctive and important feature of El Tigre is the spatial relationship between the surface mine and the underground resource. In most epithermal silver deposits in Mexico, the underground ore lies beneath the open pit or heap leach footprint, requiring a "crown pillar" to prevent collapse - effectively preventing simultaneous operation of surface and underground mines until one is exhausted.

At El Tigre, the entire 15-year underground resource identified in the PEA lies outside the footprint of the heap leach at surface. This means, in principle, both operations can run concurrently. Jessome noted that standard practice - seen at Mulatos and Pinos Altos - is to exhaust all surface production before transitioning underground, sometimes over a 20-year horizon. Silver Tiger believes it can avoid this delay entirely.

This also has direct capex implications: approximately $17 million of the $86 million estimated underground capital expenditure would already have been spent on shared infrastructure (camp, power, roads) as part of the heap leach build. The adjusted incremental cost of building the underground is therefore closer to $69 million.

Financing the Underground: Debt on Favourable Terms

With approximately $100 million in the bank and cash flow from the heap leach expected to begin in late 2027, the company is evaluating debt financing for the underground. Jessome described a material change in the negotiating environment compared to earlier years.

When the company first approached lenders, the terms on offer were heavily loaded - high interest rates, royalties, streams, off-take agreements, and warrant coverage were all part of the package. That has since changed materially. As the project has de-risked through permitting, funding, and construction commencement, debt providers are now actively seeking to participate, citing a surplus of capital and a shortage of quality projects to deploy it into. Management describes the dynamic as having shifted firmly in the company's favour.

The timing of an underground production decision will depend on the metals price environment, the availability of capital on acceptable terms, and the pace of the PFS. At $70 silver, management sees meaningful opportunity cost in delaying; at $40, they would prioritise completing the heap leach first.

Exploration: Drilling the Northern Veins

With the metallurgical and geotechnical drilling programmes for the heap leach and underground now complete, the company's exploration team has resumed drilling on a set of northern veins approximately 700 metres north of the current mine plan. These veins were identified in earlier programmes but were not drilled sufficiently to be included in the official resource estimate for the PEA.

Section 24 of the recently released PEA includes a preliminary mine plan around these zones, estimating approximately 3 million additional tonnes grading roughly 350 g/t silver equivalent - material the company believes could increase the underground resource from 4 million to approximately 7 million tonnes with further delineation drilling. Drills have been on site for approximately two weeks, with results expected to be released once an inventory of holes sufficient for a proper release is compiled.

The broader land package at El Tigre spans 25 kilometres of prospective epithermal trend. To date, all work - both the heap leach and the underground - has been conducted within approximately 2 to 3 kilometres of that trend. The northern vein drilling represents a first meaningful step outside that narrow window.

Valuation and Market Position

Despite the construction progress, the PEA releases, and the first-pour timeline, Silver Tiger's share price in June 2026 sits at roughly half its January 2026 peak - a period when silver was trading at similar levels. Management acknowledges the disconnect between operational progress and the stock price, attributing it primarily to the broader softening of the precious metals market and unresolved macroeconomic uncertainty.

The company views its current position as mid-way along the typical mining company development S-curve: past the discovery and resource delineation phase, through the trough that follows permitting delays, and into the rising portion that leads to production. The anticipated catalyst for a re-rating is the December 2027 first pour - the point at which cash flow becomes tangible and de-risking is most visible.

The Investment Thesis for Silver Tiger Metals

- Only active permitted project of its kind in Mexico - the company holds the sole new mining permit issued to a foreign company in Mexico since 2019, representing a significant and potentially irreplaceable regulatory position

- Near-term cash flow - first doré pour is targeted for December 2027, putting the company approximately 18 months from initial production at time of the interview

- High-margin, low-capex heap leach - the heap leach produces a ~$800M NPV and 92% IRR at current prices, with a ~1.1-year payback period and ~$100M/year in after-tax cash flow over a 10-year base case

- Optionality on the underground - a standalone underground PEA shows a 15-year mine life, ~$830M NPV, 110% IRR, and ~$100M/year after-tax cash flow; the two projects combined imply a ~$1.7–1.8B NPV

- No sterilisation risk - the underground ore body sits entirely outside the surface mine footprint, allowing concurrent operation - a structural advantage uncommon in Mexican epithermal deposits

- Shared infrastructure reduces incremental underground capex - approximately $17M of the $86M underground CapEx estimate will have already been spent as part of the heap leach build

- Exploration upside - northern veins outside the current mine plan may add ~3 million tonnes to the underground resource, potentially growing it from 4Mt to ~7Mt and changing the scale of the underground operation

- Discount to NPV - at mid-2026 prices, the stock trades at a material discount to the combined NPV of both projects, with management identifying the path to re-rating as execution on the build schedule

Macro Thematic Analysis

Silver is trading near multi-decade highs in nominal terms, with the $70/oz level representing a price environment that would have seemed aspirational to most silver producers only a few years ago. The drivers are a combination of monetary debasement, industrial demand growth (particularly in solar panel manufacturing and electrification), and a structural supply deficit as new high-quality silver discoveries have become increasingly rare. Mexico - the world's largest silver-producing country - is simultaneously experiencing a permitting freeze that has choked off new supply, concentrating value in the handful of permitted projects that exist. For investors seeking exposure to silver's secular move, the premium now attaches not just to ounces in the ground, but to projects that are genuinely buildable and funded. Silver Tiger represents a rare convergence: a high-grade, low-cost, permitted, and actively-under-construction project at the precise moment when silver economics are most favourable in a generation.

As Jessome put it: "At $70 or $80 or $90 or $100 silver, that's really an opportunity cost that we lose on" - a statement that frames the urgency around accelerating underground development while the price environment supports it.

TL;DR

Silver Tiger Metals is building a permitted heap leach mine in Sonora, Mexico, with first gold and silver production targeted for December 2027 and standalone economics of ~$800M NPV at current prices. A separate underground project adds another ~$830M NPV with a 15-year mine life, and uniquely, both can operate simultaneously without sterilisation of underground ore. With the stock trading at a significant discount to combined project NPV, the core investment proposition is execution risk resolving into a re-rating as the build progresses toward first pour.

FAQ (AI Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed