Sprott's $200M Raise Signals Market Inflection Point as Institutional Capital Returns to Uranium

Sprott's $200M uranium raise signals institutional return. Advanced developers access capital while juniors consolidate. North America assets command premiums.

- Sprott Physical Uranium Trust raised $200 million (double their initial $100 million target) and immediately began purchasing uranium on the spot market, demonstrating strong institutional demand and tightening supply conditions.

- Advanced development companies are successfully raising capital indicating renewed investor confidence in near-production uranium assets.

- Merger and acquisition activities are accelerating in the uranium sector after decades of inactivity, with companies consolidating assets to achieve scale and operational efficiency in a challenging funding environment.

- Spot uranium prices are responding positively to market dynamics, with prices moving upward following Sprott's purchasing activity, though the relationship between spot and long-term contract prices remains complex.

- Exploration companies face continued funding challenges, driving consolidation among junior miners while advanced development stories with clear production pathways attract institutional capital.

The uranium sector is experiencing a fundamental shift in market dynamics that presents compelling investment opportunities for institutional and individual investors. After years of market malaise, recent developments suggest the sector is entering a new phase characterized by supply tightening, renewed institutional interest, and strategic consolidation among market participants.

Institutional Capital Returns to Uranium Markets

The most significant recent development has been Sprott Physical Uranium Trust's oversubscribed capital raise. The trust initially sought $100 million but received nearly $200 million in commitments, demonstrating substantial pent-up institutional demand for uranium exposure. As Chris Frostad noted in a industry discussion,

"They obviously see that the markets that it's time. They're watching this closer than anybody, I guess, from a day-to-day basis. They picked up 200 million almost immediately ehich demonstrates the interest right now in the space."

This institutional interest extends beyond passive investment vehicles. Advanced development companies are successfully accessing capital markets after extended periods of funding difficulties. Bannerman Energy is raising A$85 million to advance its Etango Uranium Project, while IsoEnergy completed over C$50 million financing. These transactions signal that institutional investors are becoming more selective, favoring companies with clear pathways to production over early-stage exploration stories.

The selectivity of institutional capital is particularly evident in the distinction between advanced development companies and junior explorers. While established companies with near-term production prospects are attracting significant investment, smaller exploration companies continue to face funding challenges. This dynamic is creating opportunities for investors who can identify undervalued assets with legitimate development potential.

Supply Market Fundamentals Improve

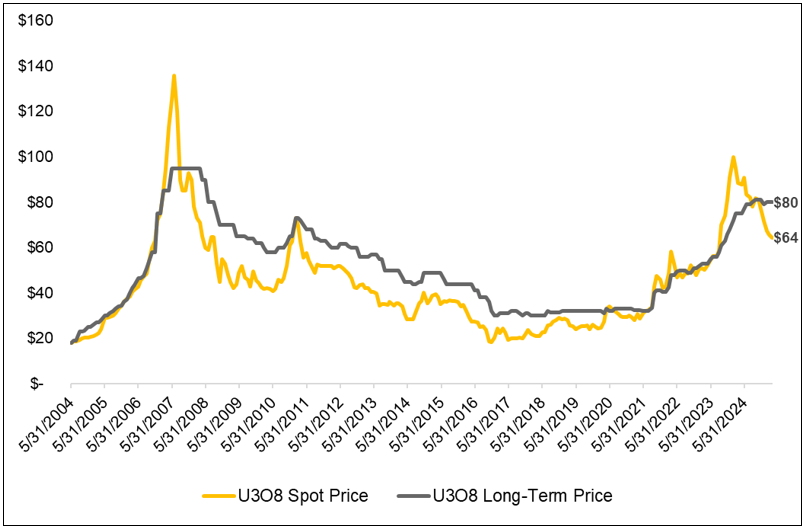

Sprott's immediate deployment of raised capital into spot uranium purchases has created noticeable market effects. The trust's buying activity has contributed to spot price increases and market tightening, with Frostad observing shareholders are soaking up whatever is sitting around on the spot market. This purchasing pressure is narrowing the spread between spot and long-term contract prices, historically a positive indicator for uranium market health.

Long-term contract markets, which represent the majority of uranium transactions, remain relatively stable around $80 per pound. The relationship between spot and long-term pricing is complex, with spot prices serving more as a market sentiment indicator than a direct driver of contract negotiations. However, sustained spot price strength typically translates into improved long-term contract pricing over time.

The spot market's responsiveness to institutional buying demonstrates the relatively small size of available uranium supplies. Unlike other commodity markets where large institutional purchases might have minimal price impact, the uranium market's structure makes it particularly sensitive to sustained buying pressure. This sensitivity suggests that continued institutional interest could drive meaningful price appreciation.

Frostad noted the significance of these capital raises, stating:

"To see that kind of money coming back into a story like that is really good news. It's fantastic for everybody."

Strategic Consolidation Accelerates

The uranium sector is experiencing unprecedented merger and acquisition activity after decades of relative inactivity. Three significant transactions have occurred in recent weeks, following years of minimal corporate activity. This consolidation trend reflects both the challenging funding environment for smaller companies and the strategic value of assembling larger, more diversified asset bases:

- The merger between Paladin Energy and Fission Uranium last year exemplifies successful strategic consolidation. Paladin recently announced a CEO transition, bringing in operational expertise from Rio Tinto as the company moves toward production. This management change signals a shift from development to operational focus, reflecting the company's advancing project timeline.

- Recent smaller-scale mergers include the combination of Nexus Uranium and Basin Uranium, both small-cap exploration companies seeking operational efficiencies and cost savings. While these transactions may not create immediate value, they reflect the broader industry trend toward consolidation as companies seek to survive in a challenging funding environment.

- More strategically significant is the acquisition of Nuclear Fuels by Premier American Uranium, which reunites historical Uranium One exploration assets under common ownership. This transaction creates an exploration incubator model that could support sustained development activity across multiple projects.

Regional Focus Shifts to North American Assets

The uranium investment landscape is increasingly focused on North American assets, driven by energy security concerns and domestic supply chain priorities. The United States faces significant uranium supply challenges, with domestic production meeting only a small fraction of reactor requirements. This supply-demand imbalance creates long-term investment opportunities for companies with North American assets.

Wyoming and Utah have emerged as primary focus areas for uranium development, with established regulatory frameworks and existing infrastructure supporting new projects. New Mexico represents an emerging opportunity, though projects in this region face additional complexity related to local community relations and regulatory approval processes. Frostad emphasized the strategic importance of domestic production,

"I think anything going on in the US right now is going to get significant support. The US needs uranium. They need fuel. They need security supply. They need to increase their domestic supply drastically. And so there's a lot of support all over the place for that kind of thing."

The emphasis on North American assets reflects broader geopolitical considerations affecting uranium supply chains. Investors are increasingly valuing domestic production capabilities and secure supply sources, creating premium valuations for strategically located assets with clear development pathways.

Market Maturation & Investor Expectations

The uranium sector is experiencing a maturation process that affects both company strategies and investor expectations. Unlike previous uranium market cycles characterized by rapid price appreciation and speculative investment, current market conditions reflect more measured investor expectations and strategic company behavior.

Companies are adopting more conservative capital allocation strategies, focusing on asset consolidation and operational efficiency rather than aggressive exploration programs. This strategic shift reflects lessons learned from previous market cycles and the recognition that sustainable value creation requires disciplined execution.

Investor expectations have similarly evolved, with greater emphasis on management execution capability, asset quality, and clear production timelines. The days of purely speculative investment based on uranium price appreciation alone have given way to more sophisticated investment analysis focused on fundamental company metrics and strategic positioning.

The Investment Thesis for Uranium

- Institutional Capital Influx: Sprott's oversubscribed $200 million raise demonstrates returning institutional interest, suggesting larger capital flows into uranium investments ahead.

- Supply Tightening: Active spot market purchasing by major funds is reducing available uranium supplies, creating potential for sustained price appreciation.

- Selective Capital Access: Advanced development companies are accessing capital while early-stage explorers struggle, creating opportunities for investors to identify undervalued near-production assets.

- Strategic Consolidation: Accelerating M&A activity offers opportunities for investors to benefit from asset value realization and operational synergies.

- North American Focus: Energy security concerns are driving premium valuations for domestic uranium assets, particularly in established mining jurisdictions.

- Production Timeline Advantage: Companies with clear pathways to production within 3-5 years are attracting disproportionate investor interest and capital.

- Management Quality: Operational experience and execution capability are becoming primary differentiators in management team evaluation.

- Long-term Contract Exposure: Companies with existing long-term uranium contracts provide downside protection and predictable cash flows.

- Infrastructure Advantage: Assets located near existing processing facilities and transportation networks offer operational cost advantages.

- Regulatory Clarity: Projects in established uranium mining jurisdictions benefit from predictable regulatory frameworks and approval processes.

Key Takeaways & Investment Implications

The uranium sector is transitioning from a period of market uncertainty to one of selective institutional engagement and strategic consolidation. The oversubscribed Sprott financing and successful capital raises by advanced development companies indicate that institutional investors are returning to uranium with more sophisticated investment criteria than in previous cycles.

The current market environment favors companies with clear production timelines, experienced management teams, and strategically located assets. While early-stage exploration companies continue to face funding challenges, this dynamic creates opportunities for investors to identify undervalued assets with legitimate development potential. The accelerating pace of merger and acquisition activity suggests that strategic value realization opportunities will continue to emerge as the sector consolidates.

For investors, the uranium sector offers exposure to a commodity with improving supply-demand fundamentals, increasing institutional interest, and strategic importance to energy security. Success in this sector requires careful evaluation of management capabilities, asset quality, and production timelines rather than purely speculative investment approaches.

Analyst's Notes

Subscribe to Our Channel

Stay Informed