Tariff-Driven Trade Dislocation Reshapes Global Copper Markets: Strategic Investment Opportunities Emerge

Global copper markets face unprecedented tariff-driven disruptions, creating new investment opportunities in Chile, Canada, and Spain's emerging projects.

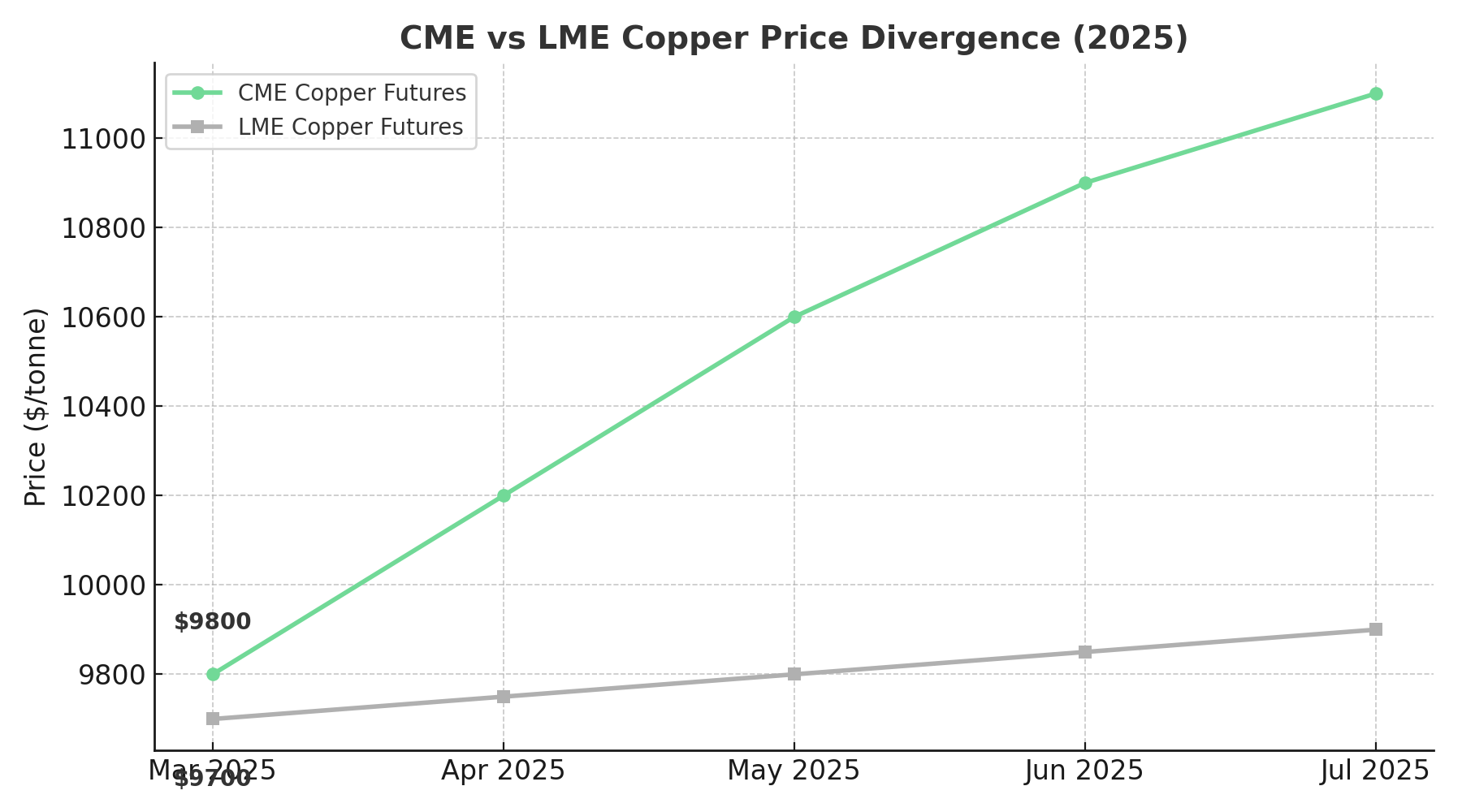

- Tariff-induced market fragmentation has created a 30% price divergence between US and global copper markets, with CME futures surging above $11,000 per tonne while LME pricing remained relatively stable, fundamentally questioning copper's traditional role as an economic indicator.

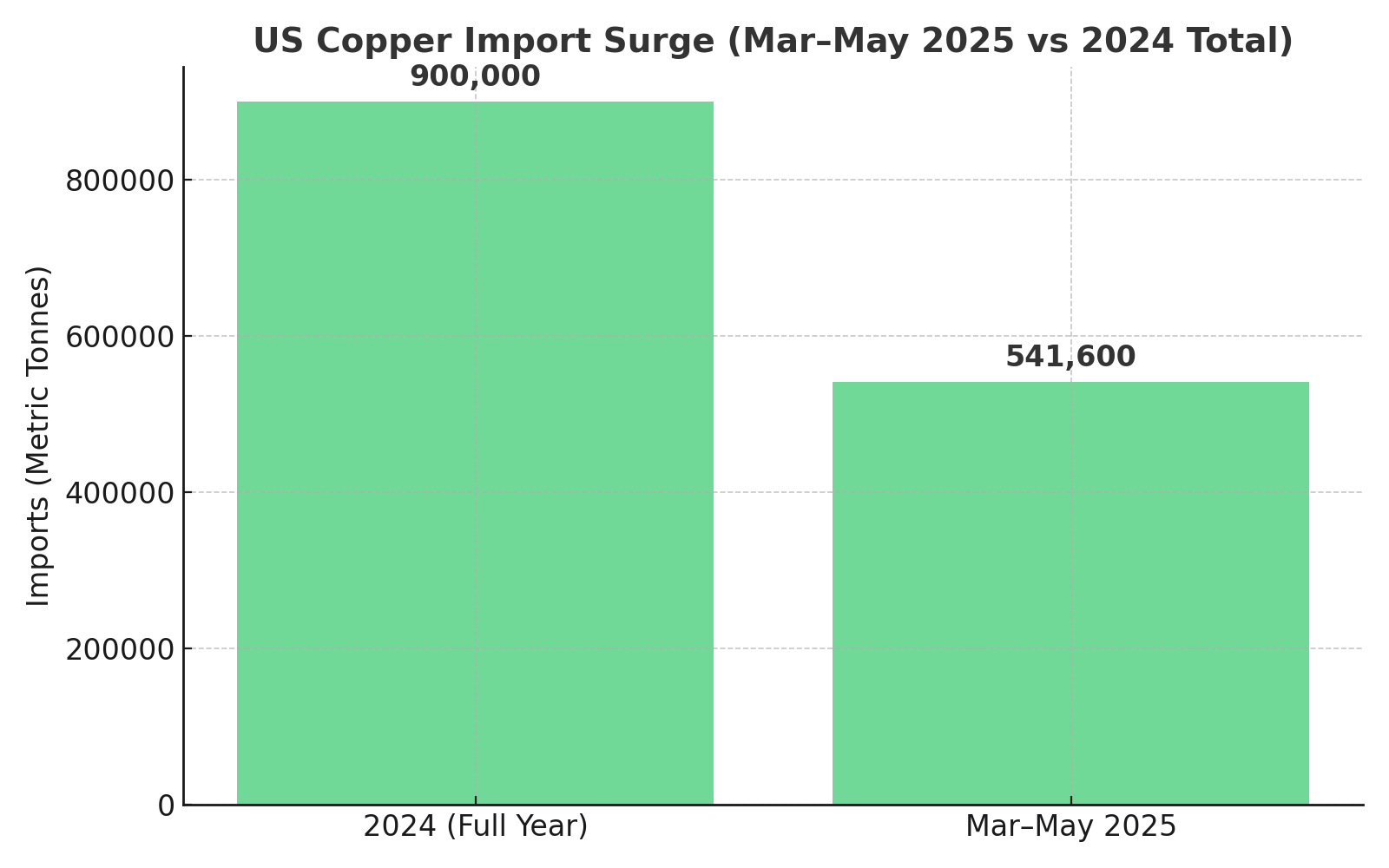

- The US copper import surge of 541,600 metric tonnes in just three months represents 60% of 2024's total imports, driven by a rush to beat the August 1, 2025 tariff deadline, resulting in an estimated 400,000-500,000 metric tonne surplus that could negate import demand for the remainder of 2025.

- Development-stage copper projects in stable jurisdictions are gaining strategic value as policy volatility highlights the importance of jurisdictional security, with Chile's Marimaca Copper Corp advancing toward FID in H1 2026 with its low-strip, high-margin oxide operation.

- European copper assets have gained prominence under the EU's Critical Raw Materials Act, which designates copper as critical and provides accelerated 24-month permitting for extraction projects, benefiting developers like Pan Global Resources in Spain's Iberian Pyrite Belt.

- Canadian copper developments offer Tier 1 jurisdictional stability with projects like Gladiator Metals' Whitehorse Copper Belt targeting over 100 million tonnes of inferred copper resources across multiple high-grade skarn systems in infrastructure-accessible locations.

Policy Shock: The Trump Tariff Surprise

US President Donald Trump's announcement of an unexpectedly high 50% tariff on copper imports, effective August 1, 2025, caught the global copper market completely off-guard. The double surprise of both the tariff rate and the short implementation timeline triggered an immediate scramble among traders and importers to exploit the arbitrage opportunity before the deadline.

This policy shift represents more than just a trade measure - it fundamentally challenges the integrated nature of global copper markets that have operated for decades under relatively free trade principles. The sudden policy implementation created an environment where physical copper flows became divorced from underlying supply-demand fundamentals, instead driven by regulatory arbitrage.

The move's strategic implications extend beyond immediate trade effects. Industry leaders, including Codelco, the world's largest copper producer and major US supplier, have expressed widespread "anxiety" about the policy's unclear scope, coverage details, and potential exemptions. Uncertainty persists around whether refined copper, cathodes, semi-finished products, or scrap exports might receive different treatment under the new tariff structure.

Surge in Physical Copper Trade

The three-month period between March and May 2025 witnessed an extraordinary surge in US copper imports, reaching approximately 541,600 metric tonnes - equivalent to 60% of all 2024 imports compressed into a single quarter. This unprecedented volume reflects the market's collective rush to capture arbitrage profits before the tariff window closed.

CME warehouse inventories more than doubled since March, climbing to near 222,723 metric tonnes and approaching the 2018 high-water mark. However, the visible inventory build represents only part of the story. Industry analysts estimate an additional off-exchange surplus of 400,000 to 500,000 metric tonnes accumulated in the US market, potentially negating import demand for the remainder of 2025.

This inventory accumulation created a unique market dynamic where physical copper became temporarily divorced from consumption patterns. Rather than flowing to end-users, significant volumes entered strategic stockpiles, creating artificial demand that masked underlying consumption trends. The scale of this stockpiling suggests that the US copper market may experience an extended period of inventory overhang as these surplus stocks gradually work through the system.

Inventory Rebalancing & Trade Reversal

As the physical import window closed with the August 1 tariff implementation, copper markets began experiencing a rapid reversal of the preceding months' trade flows. Copper stocks are now returning to global pools, with LME inventories rising again after months of depletion. The cash-to-three-month spreads shifted from backwardation to contango almost instantly, signaling the market's transition from scarcity to surplus conditions.

New LME warehouses in Hong Kong have accelerated the supply recovery process, receiving nearly 6,000 metric tonnes by mid-July as Chinese exporters redirected flows away from the now-tariff-protected US market. This rebalancing represents the natural market response to artificial trade distortions, as copper seeks its most economically efficient distribution channels.

The speed of this inventory rebalancing demonstrates the copper market's inherent efficiency when not constrained by policy interventions. However, the unwinding process is creating its own market tensions, as the surplus copper accumulated during the pre-tariff rush now competes with regular trade flows, potentially depressing prices in non-US markets.

Fragmentation of Copper Pricing

Perhaps the most striking consequence of the tariff policy has been the unprecedented fragmentation of global copper pricing. CME copper futures surged to record highs, widening their premium over LME prices from approximately $1,233 to $3,095 per tonne, expanding from roughly 13% to 31% in a matter of months.

Meanwhile, LME three-month prices have remained relatively stagnant under $10,000 per tonne, reflecting global fundamentals rather than tariff-driven distortions. This pricing bifurcation raises fundamental questions about copper's traditional role as "Doctor Copper" - the economic indicator that has historically reflected global industrial health through its price movements.

The sustained price divergence suggests that copper markets may remain fragmented for an extended period, particularly if the tariff policy persists. This fragmentation creates challenges for industrial users, miners, and investors who must now navigate multiple copper pricing regimes depending on their geographic exposure and supply chain configuration.

For investors, this pricing dislocation creates both opportunities and risks. Those with exposure to US-focused copper assets may benefit from sustained price premiums, while global copper investors face the complexity of determining which price benchmark best reflects their investment's underlying value.

Strategic Investment Opportunities in Stable Jurisdictions

The copper market's policy-driven volatility has elevated the strategic importance of jurisdictional stability and supply chain security. Development-stage projects in politically stable regions with established mining frameworks are gaining increased investor attention as market participants seek to reduce exposure to trade policy risks.

Chile: Operational Excellence and Infrastructure Advantage

Marimaca Copper - Advancing Toward Final Investment Decision (FID) in H1 2026

Chile continues to demonstrate its position as a premier copper jurisdiction, offering political stability, established mining regulations, and world-class infrastructure. Marimaca Copper exemplifies the strategic advantages available in Chile's copper sector, with its oxide project located just 25 kilometers from the Port of Mejillones and 40 kilometers from Antofagasta, eliminating accommodation and utility development requirements.

The company's permitting strategy via DIA (Declaración de Impacto Ambiental) provides a fast-track approval pathway, with FID targeted for H1 2026. The project's continuous oxide orebody features favorable geometry that reduces pre-strip requirements and enhances early cash flow generation through SX-EW processing with high recoveries.

Marimaca's 2023 Mineral Resource Estimate validated significant resource growth, with 900,000 tonnes of copper in Measured & Indicated categories and 141,000 tonnes Inferred, positioning it as one of the largest oxide discoveries in a decade. The discovery cost of under $0.02 per pound demonstrates exceptional capital efficiency in resource development.

District-scale exploration potential across targets including Pampa Medina, Sierra, Roble, and Cindy offers strong prospects for oxide and sulphide discoveries. Notable drill intercepts at Pampa Medina include 26 meters at 4.11% copper and 18 meters at 5.7% copper, suggesting potentially transformative sulphide upside beyond the current oxide resource base.

On balancing immediate production with exploration upside, President & CEO Hayden Locke explained:

"Our number one focus is on getting that into production... Once we get into production, we can use our cash flow to invest, to take these projects forward as we see fit.The intention was to go full ball forwards, to develop this project, move as quickly as we could to get it into production and get ourselves cash flowing. It is a mine that can be built and its fairly low execution risk... I think we can do it concurrently; I would say it's definitely going to be bent towards testing the exploration potential.”

Canada: Tier 1 Jurisdiction with Infrastructure Access

Gladiator Metals - Targeting Initial Inferred Resource at Cowley Park by H1 2026

Canada's mining-friendly regulatory environment and established infrastructure make it an attractive alternative for copper development. Gladiator Metals' advancement of the Whitehorse Copper Belt in Yukon exemplifies the advantages of Canadian copper development, with the project benefiting from road accessibility, hydro connectivity, and proximity to Whitehorse city.

The Whitehorse Copper Belt represents a former producing district with over 8.5 million tonnes of historical production, providing geological validation for continued exploration success. Gladiator's multi-zone approach targets over 100 million tonnes of inferred copper resources across the Cowley Park, Cub, Chief, and Arctic Chief trends.

The company's 2025 drilling campaign encompasses 27,000 meters across multiple targets: 12,000 meters at Cowley, 10,000 meters at Little Chief, and 5,000 meters at Arctic Chief. This systematic approach to resource definition positions the company for an initial inferred resource at Cowley Park by H1 2026.

Gladiator's operational advantages include grid power access, elimination of fly-in/fly-out costs, and established community relationships through a Capacity Funding Agreement with First Nations since October 2024. These factors contribute to lower capital requirements and reduced operational complexity compared to remote copper developments. Chief Executive Officer Jason Bontempo notes:

"Coming to a capacity funding agreement with [the Kwanlin Dün First Nation]… essentially what that meant was, hey, let's come together. Let's talk about what might be the next stage and how we're going to go about those discussions. It was a very positive first step. When that got announced, that was very, very much well received by the Whitehorse community."

Europe: Critical Raw Materials Policy Support

Pan Global Resources - Positioning for Maiden Resource Declaration in Q4 2025

The European Union's Critical Raw Materials Act (CRMA), implemented in March 2024, has fundamentally altered the investment landscape for European copper projects. By classifying copper as critical, the CRMA enables accelerated permitting timelines of 24 months for extraction projects and 12 months for processing, along with access to EU research and infrastructure funding.

Pan Global Resources' development of the Escacena Project in Spain's Iberian Pyrite Belt directly benefits from this policy framework. The project's location 40 kilometers from three processing plants and 75 kilometers from the Huelva copper smelter provides exceptional infrastructure advantages within the European supply chain.

Pan Global's La Romana deposit demonstrates tier-one metallurgical characteristics with 88% copper recovery and 32.5% concentrate grade, complemented by tin and silver as high-value by-products. The deposit's surface mineralization and simple flotation plus gravity circuit design support low energy intensity processing, aligning with European sustainability objectives. Tim Moody, Chief Executive Officer of Pan Global notes:

"A cubic metre of 1% copper at La Romana is worth a lot more than the same grade at any of the other mines. Why? Because of the metallurgy. Higher recovery, higher concentrate grades, have lower sulphides, and we have low deleterious metal content. When you put all those things together, it means that the net value of that 1% or half percent copper at La Romana is worth a lot more than all the other mines and as far as we can tell other advanced projects in the Iberian [Pyrite] Belt."

The company's systematic exploration approach across 188 drill holes and 37,000 meters has defined mineralization over 1.7 kilometers of strike and 400 meters depth, positioning for a maiden resource declaration in Q4 2025. Additional targets including Bravo, La Pantoja, and Cañada Honda offer district-scale expansion potential consistent with the regional VMS clustering model.

Industry Concerns & Strategic Uncertainty

The copper industry's response to the tariff policy has been marked by widespread uncertainty about implementation details and long-term implications. Codelco's public expressions of "anxiety" reflect broader industry concerns about policy consistency and trade relationship stability.

Key uncertainties include the tariff's precise scope, potential exemptions for different product categories, and possible reciprocal measures from copper-exporting nations. The lack of clarity around whether refined copper, cathodes, semi-finished products, or scrap materials might receive differentiated treatment creates planning challenges for integrated copper companies.

These uncertainties have strategic implications for investment decisions, particularly for projects with significant US market exposure or those considering supply chain reconfiguration. Companies must now factor trade policy risks into their development timelines and market analysis, adding complexity to traditional mining investment evaluation processes.

Strategic Considerations

The tariff-driven market disruption has created a complex investment environment where traditional copper market analysis must incorporate new variables around trade policy, jurisdictional risk, and supply chain security. Institutional investors are demonstrating increased caution amid policy-driven volatility, while simultaneously recognizing opportunities created by market dislocations.

Sprott's analysis highlights how structural supply-demand deficits combined with policy risk favor copper producers with strategic geographic positioning. US-exposed copper assets may sustain price premiums if tariffs persist, while projects in stable jurisdictions with established trade relationships offer defensive characteristics against policy volatility.

Investment opportunities are emerging across multiple categories: domestic US copper expansion projects that benefit from tariff protection, recycling technologies that can substitute for imported materials, and processing investments in tariff-friendly jurisdictions that can serve protected markets.

The current environment particularly favors development-stage projects with clear permitting pathways, established infrastructure access, and operational flexibility. Projects like Marimaca's Chilean oxide operation, Gladiator's Canadian skarn systems, and Pan Global's European VMS development offer different risk-return profiles that can complement diversified copper investment strategies.

Market Outlook: What Investors Should Watch

Several key factors will determine the copper market's evolution through the remainder of 2025 and beyond. Policy developments remain paramount, with particular attention required for details on tariff scope, exemption processes, scrap inclusion policies, and potential reciprocal trade measures from copper-exporting nations.

Inventory trends will provide crucial signals about market rebalancing speed and effectiveness. CME and LME stock trajectories, combined with estimates of US excess physical stock depletion rates, will indicate whether the current surplus conditions persist or resolve more quickly than anticipated.

Price convergence between CME and LME contracts will serve as a barometer for market integration restoration. Persistent divergence suggests continued market fragmentation, while convergence would indicate successful policy adaptation and trade flow normalization.

Supply-side responses will ultimately determine long-term market structure. Announcements of new mine expansions, domestic smelter capacity additions, or recycling infrastructure investments will signal how the industry adapts to the new trade policy environment.

Conclusion

The unwinding of copper's tariff-driven trade bubble represents a pivotal moment for global copper markets, with implications extending far beyond immediate price movements. While the most dramatic inventory accumulation phase has concluded, persistent inventory imbalances and pricing bifurcation are likely to dominate copper markets through late 2025 and potentially beyond.

For strategic investors, the emerging landscape rewards those who can navigate the complexity of fragmented markets while identifying assets with sustainable competitive advantages. The current environment has elevated the importance of jurisdictional stability, infrastructure access, and operational flexibility - factors that development-stage projects in Chile, Canada, and Europe are well-positioned to provide.

The copper market's experience with tariff-driven disruption offers valuable lessons about the intersection of trade policy and commodity markets. As global supply chains continue evolving in response to geopolitical tensions and strategic resource considerations, copper's role as both an industrial input and a strategic material will likely drive continued investment in geographically diversified, operationally robust development projects.

Ultimately, while policy-driven volatility creates near-term uncertainty, the underlying fundamentals of copper demand growth driven by electrification, urbanization, and energy transition remain intact. Investors who can identify and access high-quality copper assets in stable jurisdictions are well-positioned to benefit from both the resolution of current market dislocations and the long-term structural demand growth that continues to drive the global copper sector.

Analyst's Notes

Subscribe to Our Channel

Stay Informed