The Salt Deficit: Navigating North America’s US$2.6 Billion De-Icing Market (2/3)

North America's $2.6B de-icing market shifts from lowest-bid to supply security, creating structural advantages for domestic salt producers over imports.

- North American road salt procurement is structurally shifting away from lowest-bid rules toward supply security, domestic reliability, and fiscal multipliers. This alters how investors should evaluate cost curves and competitive advantage in bulk infrastructure commodities.

- New York's Buy American Salt Act was signed into law in December 2022. The legislation formalised the ability of state agencies to prioritise domestic supply over lowest-price mandates, setting a template that materially disadvantages overseas swing supply dependent on international logistics chains.

- The 80/120 tender rule embeds delivery risk into contracts. This framework favours geographically proximate assets and exposes importers to severe logistics and penalty risk during extreme winters when demand variability is highest.

- Development projects with competitive projected all-in sustaining costs on a cost-insurance-freight basis are positioning to operate within frameworks where logistics, tariffs, and currency stability function as durable economic moats. These factors protect margin resilience across policy and trade environments.

- Advanced-stage North American salt development projects demonstrate how policy alignment and cost positioning can translate into sticky, recession-resilient cash flows. These assets carry lower downside risk than traditional bulk commodities exposed to cyclical demand destruction or discretionary spending constraints.

The End of Globalised Procurement: When Security of Supply Overrides Lowest Cost

For decades, municipal de-icing procurement operated under a lowest-bid framework. Road salt was sourced globally based solely on delivered cost, with limited consideration for supply chain reliability, domestic economic impact, or strategic sourcing risk.

That framework is breaking down as climate volatility increases peak-demand risk, with extreme winter events causing delivery failures that cascade into public safety crises. Simultaneously, fiscal leakage from imported bulk commodities is drawing political scrutiny as trade tensions and supply chain fragility have elevated the strategic importance of domestic production capacity.

Salt represents an essential infrastructure input with limited practical substitutes for winter road maintenance. Delivery failures carry immediate political and operational consequences. Procurement agencies are beginning to prioritize certainty of delivery and supply chain sovereignty over marginal cost savings, particularly when domestic assets can compete on delivered cost without requiring protectionist subsidies.

Atlas Salt Chief Executive Officer Nolan Peterson, speaking at the November 2025 Resourcing Tomorrow conference in London, frames the competitive shift in logistics terms:

“Our port proximity and our presence in Newfoundland allow us to move the same types of boats that foreign salt does to the same markets in 15 to 20% or sometimes even less the time and the cost, and that gives us a huge advantage for shipping and delivery."

Legislative Protectionism: Policy Frameworks as Market Re-Rating Catalysts

New York's Buy American Salt Act (S.9441/A.7919-A), signed into law in December 2022, represents the first formal legislative precedent allowing state agencies to bypass lowest-price mandates when domestic supply offers strategic advantages. The legislation explicitly permits procurement agencies to consider factors beyond delivered cost, including supply reliability, domestic economic impact, and fiscal multipliers.

This reduces downside price-compression risk and improves contract-renewal visibility. Domestic assets are competing within a framework that recognizes logistical optionality and supply chain resilience as economically valuable attributes.

Fiscal Multipliers & Political Incentives

Domestic production generates measurable fiscal returns for regional and state governments. New York State estimates approximately three dollars per tonne in retained tax revenue from domestic production, encompassing payroll taxes, corporate income taxes, and property taxes from mining operations and associated infrastructure.

This shifts procurement math beyond delivered cost. When a contract is awarded to a domestic asset, the fiscal offset partially recovers the procurement cost through tax revenue while supporting regional employment. For imported salt, competitive positioning now requires a margin sufficient to offset fiscal and logistical disadvantages relative to domestic supply.

Displacement Risk for Overseas Supply

Imports have historically covered approximately 20% to 35% of North American demand over the past decade, according to United States Geological Survey data. However, this role is becoming structurally more vulnerable through legislative exclusion, port congestion during peak winter months, and shifting trade policy, including potential tariffs on Canadian exports.

Nolan Peterson characterizes the supply chain dynamics:

"What you find is that in North America there is a salt shortage year-over-year when you're balancing domestic production versus domestic needs… We've had to supplement to the tune of 30% to 40% of our salt needs from other jurisdictions. Egypt and Chile primarily come to mind."

Tendered Bid Mechanics: Why the 80/120 Rule Creates a Structural Advantage for Local Supply

Municipal de-icing contracts are typically structured around an 80/120 tender rule, which sets the contract base price at 80% of estimated annual demand but creates a legal obligation to supply up to 120% during severe winters. This introduces asymmetric risk for suppliers depending on their logistics flexibility.

For domestic assets with geographic proximity to demand centers, the 120% obligation is manageable. For overseas suppliers dependent on ocean freight, it introduces severe tail risk. Panamax vessel availability is constrained during the winter months, and lead times of 3 to 4 weeks create the potential for contractual default if demand surges unexpectedly.

Logistics as a Hidden Cost Curve

Proximity allows just-in-time delivery, reducing working capital burden and storage costs for municipal buyers. Overseas swing supply operates on a forecast-and-ship model, introducing both demand and cost risks. From an investor perspective, delivery optionality has economic value that is not fully captured in traditional cost-curve analysis.

Nolan Peterson quantifies this delivery advantage:

"In theory you could call Egypt and say I need some salt, I need 50,000 tons of salt. But you're looking at a one month to two month lead time on that order… By having us closer we can respond faster to these types of shortages in the market."

Atlas Salt's Great Atlantic Salt Project in Newfoundland demonstrates this proximity advantage. Located 2km from the Turf Point Deep Water Port, the project can deliver product to Boston in less than three days once in commercial production, estimated by 2030.

Cost Structures, AISC & Geography as an Economic Moat

Salt is a low-unit-value, logistics-heavy commodity, with freight accounting for up to 90% of the delivered cost for imports. Geographic location represents a structural cost advantage that cannot be replicated by operational improvements in overseas production.

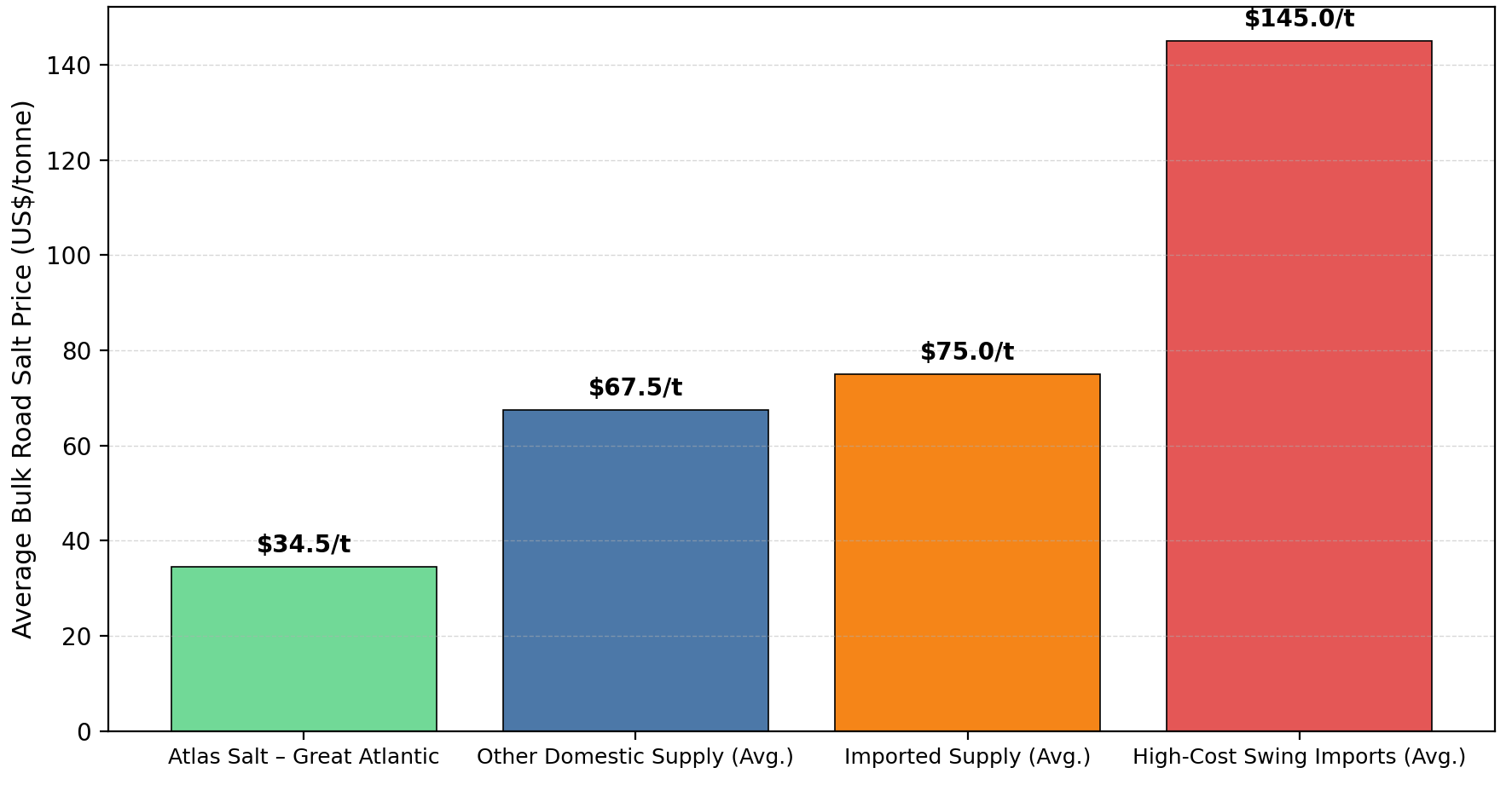

Competitive Cost Benchmarking

Atlas Salt's Great Atlantic Salt Project, North America's first new salt mine in nearly three decades, projects a life-of-mine average all-in sustaining cost of $34.45 per tonne on a cost-insurance-freight basis to Northeast United States demand centers.

This compares favorably to Chilean and Moroccan imports, which face materially higher delivered costs. The implication is that advanced-stage domestic development projects can position to compete on cost without requiring protectionist policy support. Projects with inclined ramp access and shallow deposit geometry further support long-term cost stability. Atlas Salt's deposit, located up to 180 meters from surface with homogenous ore characteristics, exemplifies this structural advantage.

Tariffs, Currency & Jurisdiction: Macro Volatility as a Tailwind, Not a Risk

United States trade policy has exhibited increasing protectionist tendencies in recent years, with tariffs functioning as asymmetric risk for importers. While salt has not been the primary focus, the broader trend creates structural uncertainty for overseas suppliers that domestic assets do not face.

Currency Stability & Margin Preservation

Foreign exchange exposure represents another source of earnings volatility for international supply chains. Chilean, Egyptian, and North African producers face currency risk on both revenue and cost sides. For North American assets operating within dollarized economies or closely correlated currency regimes, this risk is minimal.

Jurisdictional Safety Premium

Operating within established Canadian and United States mining jurisdictions can provide greater regulatory predictability relative to certain international alternatives. Atlas Salt's Great Atlantic Salt Project in Newfoundland has been released from the provincial environmental assessment process with conditions, with remaining permits currently in progress for full-scale construction targeting production by 2030.

Nolan Peterson highlights the demand stability, and regional alignment:

"There's supply chain stability. There's a buy-Canadian, buy-North American mentality that is very helpful, creates local jobs which is always good indirectly for the economy of the regions we're talking about."

The Investment Thesis for Salt

- Policy-aligned demand structures favor domestic assets through legislative frameworks like New York's Buy American Salt Act that prioritize supply security and domestic economic impact over marginal cost differentials, creating contractual defensibility that improves margin resilience and contract renewal visibility.

- Recession-resistant revenues are driven by public safety mandates rather than discretionary spending, insulating cash flows from cyclical demand destruction and ensuring stable production volumes across macroeconomic environments.

- Sticky contracts result from annual tender processes and delivery obligations that reduce customer churn risk, with municipal buyers prioritizing reliability and logistics flexibility over marginal price advantages once a supplier has demonstrated operational performance.

- Cost leadership on a delivered basis positions advanced-stage development projects to compete even in the absence of policy support, with competitive projected all-in sustaining costs ensuring that cash flows remain robust across a range of tariff, currency, and regulatory scenarios.

- Scarcity value emerges from the absence of new large-scale North American salt mine development in recent decades, with no other new rock salt mines currently planned in the United States or Canada, limiting supply response to demand growth and supporting pricing stability during periods of capacity tightness.

- Execution visibility is enhanced by advanced permitting, defined financing pathways including engaged debt advisors, and early offtake interest from institutional buyers, reducing development risk and improving the probability of successful project delivery within expected timelines and budgets.

Climate volatility, trade friction, and infrastructure fragility appear to be persistent rather than purely cyclical factors. Advanced-stage domestic salt development projects like Atlas Salt's Great Atlantic Salt Project represent policy-backed, recession-resistant cash flow opportunities with execution visibility and competitive projected cost structures, positioning them as differentiated exposures within bulk commodities for investors seeking stable returns in an increasingly uncertain macro environment.

Road salt is no longer a purely commoditized, lowest-bid market where price alone determines competitive outcomes. Legislative frameworks, logistics constraints, and supply chain sovereignty considerations have introduced structural advantages for domestic assets that are unlikely to be fully offset by operational efficiency improvements in overseas production.

TL;DR

North American road salt procurement is undergoing a structural transformation from lowest-bid purchasing to prioritizing supply security and domestic reliability. New York's Buy American Salt Act (December 2022) established legislative precedent allowing agencies to consider supply chain resilience over marginal cost savings. The 80/120 tender rule creates asymmetric risk for overseas suppliers, who face 3-4 week delivery times versus domestic assets capable of just-in-time delivery. With freight representing up to 90% of delivered cost for imports, geographically proximate domestic projects offer durable competitive advantages. Advanced-stage developments targeting a competitive all-in sustaining costs position to capture recession-resistant municipal revenues backed by public safety mandates rather than discretionary spending.

FAQs (AI-Generated)

New York's Buy American Salt Act (S.9441/A.7919-A), signed in December 2022, allows state agencies to prioritize domestic salt supply over lowest-price mandates by considering factors like supply reliability, economic impact, and fiscal multipliers.

Municipal de-icing contracts set base pricing at 80% of estimated annual demand but obligate suppliers to deliver up to 120% during severe winters, creating significant logistics risk for overseas suppliers with extended shipping times.

Domestic assets offer delivery within days versus 3-4 weeks for overseas supply, reducing demand risk during winter surges. Geographic proximity also minimizes freight costs, which can represent up to 90% of delivered cost for imports.

Extreme winter events increase peak-demand risk and delivery failure potential, prompting procurement agencies to prioritize supply chain certainty over marginal cost savings from international sources.

New York State estimates approximately $3 per tonne in retained tax revenue from domestic production through payroll taxes, corporate income taxes, and property taxes from mining operations and associated infrastructure.

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

.jpg)

.jpg)

Stay Informed