The Salt Deficit: Navigating North America’s US$2.6 Billion De-Icing Market (1/3)

North America's US$2.6B road salt market faces a structural deficit with 20-35% import dependence, creating investment opportunities in domestic supply assets.

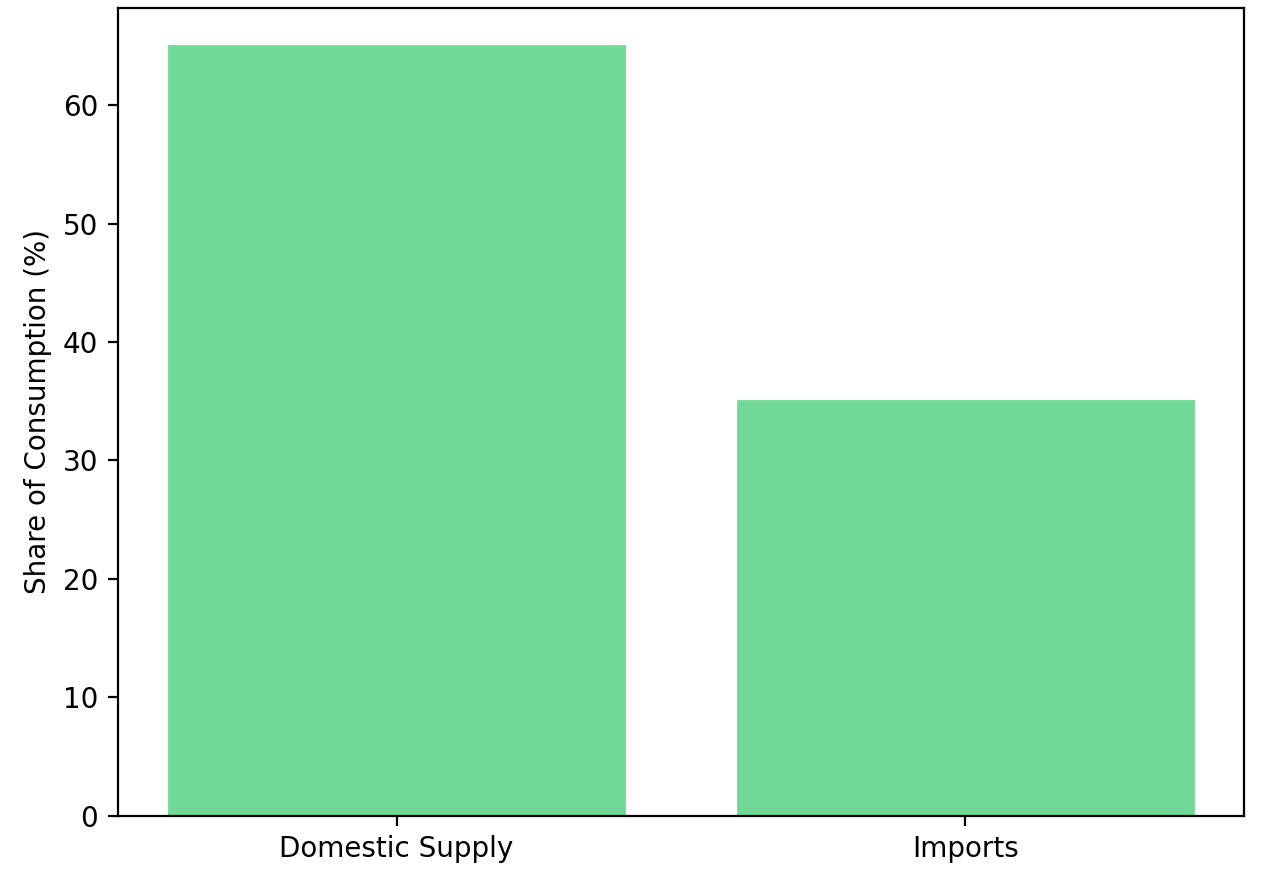

- North American road salt demand is government-mandated and recession-proof. Yet 20–35% of supply, approximately 8 to 10 million tonnes annually, depends on imports from Chile, Egypt, and Morocco, exposing the market to a mismatch between emergency-response timelines and global shipping cycles.

- Legacy mine constraints, geographic concentration, and permitting barriers have kept domestic output consistently below average demand in a market valued at approximately US$2.6 billion annually. This structural deficit is unlikely to be resolved through short-cycle capital deployment.

- Foreign swing supply operates on 3–4 week lead times, while winter storm events require delivery within days. This fundamental disconnect elevates supply security above unit economics in procurement decisions.

- Municipal and state procurement frameworks increasingly weigh delivery certainty and domestic sourcing over lowest-cost bids. New York's Buy American Salt Act and Denver's Environmentally Preferred Procurement programme reflect this shift.

- Development-stage domestic assets with cost leadership and logistical advantages represent asymmetric exposure to an under-recognised infrastructure theme with long-duration demand visibility.

Infrastructure Commodities and Strategic Mispricing

Road salt occupies an unusual position in commodity markets: a 28.5 to 36 million tonne annual market that remains largely invisible to equity investors despite its size, predictability, and capital intensity. Unlike cyclical industrial commodities, salt demand is driven by public safety mandates rather than economic growth. Municipalities face liability exposure if roads are not treated during winter weather events, creating a hard demand floor regardless of fiscal conditions.

This market's characteristics, stable volumes, government end-users, and essential service classification create defensive investment attributes rarely priced into related equities. Yet the sector faces a structural tension: inelastic demand colliding with constrained domestic capacity and rising import dependence. With only two publicly traded salt companies in North America (Compass Minerals and Atlas Salt), investor access to this theme remains limited.

These dynamics matter now because ageing domestic infrastructure, geopolitical supply chain concerns, and emerging procurement policy shifts are converging to reprice supply security relative to unit cost.

Demand Characteristics and the Safety Mandate Floor

Road salting is not discretionary but is legally mandated across northern US states and Canadian provinces as a public safety requirement. Winter severity introduces volume volatility: mild winters reduce consumption, while severe winters can deplete stockpiles within days. Procurement must anticipate worst-case scenarios regardless of actual weather patterns.

Substitution options remain limited as brine pre-treatment and sand are supplements, not replacements at the required scale. No alternative currently exists that can match salt's effectiveness, availability, and cost profile for large-scale road treatment. This places salt alongside other infrastructure commodities with similar demand characteristics: water treatment chemicals, road aggregates, and utility inputs, where consumption is non-discretionary.

As Atlas Salt CEO Nolan Peterson observed in November 2025:

"It's a recession-proof commodity. Anybody who deals in the market knows the only thing that affects it is inclement weather, and the worse the weather, the better it is... That's all anyone cares about."

Cities do not conserve salt during mild periods. Application occurs at the first sign of precipitation as a precautionary measure, and if conditions change, the process repeats. This behavioural pattern reinforces baseline demand predictability over multi-year horizons even as inter-year volumes fluctuate.

The North American Supply Structure and Its Constraints

The northeastern US and Eastern Canada consume approximately 28.5 to 36 million tonnes of road salt annually, representing a market valued at roughly US$2.6 billion. Domestic production ceilings have consistently fallen short of this demand, requiring import volumes of 8 to 10 million tonnes annually, representing 20% to 35% of total consumption, to balance the market.

This gap persists for structural reasons. Economically viable halite deposits are geographically concentrated. Legacy mines face reinvestment challenges, with some approaching end-of-life or experiencing declining output. Environmental and permitting constraints limit new development, and investment in domestic capacity expansion has been minimal over the past two decades. The result is a market where no new salt mine has been developed in North America in nearly three decades.

The Import Dependence Mechanism

Imports from Chile, Egypt, Morocco, and other distant suppliers function as a swing supply, filling gaps when domestic production fails to meet demand. This arrangement embeds multiple cost layers: ocean freight, port handling, inland logistics, and currency exposure.

Nolan Nolan Peterson's observation from November 2025 illustrates the operational reality:

"A lot of salt mines last year were trying to ramp up production to meet demand, and they failed.. They had to import a lot more salt, and that was delayed as well, and it was just lacking, and they paid a lot more premium as well."

The cost structure of imports creates vulnerability that extends beyond unit economics to delivery timing, a critical factor for a commodity required during weather emergencies.

Logistics, Lead Times, and the Import Timing Mismatch

The central vulnerability in North American salt supply lies in the asymmetry between import logistics and end-user requirements. Import suppliers operate on global shipping cycles with minimum lead times of three to four weeks. End-users operate on emergency response timelines measured in hours during severe weather events.

Salt procurement occurs months in advance, but winter weather remains unpredictable. A single severe storm system can consume weeks of supply across multiple municipalities simultaneously. When stockpiles run short, the structural mismatch becomes acute.

Nolan Nolan Peterson quantified the supply gap:

"That's a key advantage compared to foreign salt, which is two to three weeks out. You pick up the phone and say, 'I need some salt tomorrow.' They're about a month away at best; you have to get a boat hired and chartered and put over there, and we can do that in three days."

Procurement Frameworks and Risk Tolerance

Municipal procurement has historically prioritised lowest-cost bids. However, emerging policy frameworks increasingly weigh supply reliability and domestic sourcing. New York's Buy American Salt Act allows state agencies to bypass lowest-bid requirements to support domestic supply security. Denver's Environmentally Preferred Procurement programme incorporates supply chain considerations into purchasing decisions.

These policy signals suggest a structural re-pricing of logistical risk at the procurement level, a shift that favours domestic and proximate supply sources over distant low-cost alternatives.

Development-Stage Domestic Assets as a Supply Response

New domestic development represents import displacement rather than market expansion. Viable projects compete on delivered cost and reliability, not mine-gate production cost alone.

Atlas Salt's Great Atlantic project in Newfoundland and Labrador illustrates this positioning. Currently in the early works construction phase following completion of its 2025 Updated Feasibility Study and release from provincial environmental assessment in April 2024, the project represents North America's first new salt mine in nearly three decades.

Geographic positioning targets the eastern seaboard US and St. Lawrence Seaway distribution channels. The company has secured a non-binding MOU with Scotwood Industries for targeted annual volumes of 1.25 to 1.5 million tonnes, with first production estimated for 2030.

Capital Discipline, Permitting, and Jurisdictional Considerations

Late-cycle macro uncertainty heightens investor preference for long-life, low-volatility assets with predictable cash flows. Infrastructure commodities with government end-users and mandated demand offer defensive characteristics that align with this preference.

Permitting visibility functions as a key differentiator for development-stage assets. Atlas Salt has obtained environmental assessment release and multiple operational approvals including the Early Works Development Plan, Environmental Protection Plan, and various management plans. Securing remaining permits for full-scale construction remains a milestone priority, alongside finalising supply arrangements and project financing.

Jurisdictional risk matters more than grade in infrastructure commodities. Newfoundland and Labrador ranked 9th globally in the Fraser Institute's 2025 mining jurisdiction survey, supporting characterisation as a top-tier mining jurisdiction with regulatory clarity relative to overseas supply chain alternatives.

The company has engaged Endeavour Financial to lead project debt financing following a recent working capital raise, with SLR Consulting providing feasibility support, and Sandvik engaged for mining equipment and engineering.

Market Volatility, Currency Risk, and Margin Stability

Imported salt embeds cost variables that introduce margin uncertainty: foreign exchange fluctuation, ocean freight rates correlated with energy prices, port congestion, and inland logistics from coastal terminals. These variables create price volatility for end-users and margin compression risk for importers during periods of macro stress.

Domestic cost structures tied to local-currency operations, predictable power pricing, and direct logistics to end markets offer potential advantages in margin stability. Salt competes on a delivered-cost basis rather than mine-gate cost, meaning domestic assets positioned near demand centres may achieve cost parity or advantage despite higher nominal production costs.

The Investment Thesis for Salt

- Strategic Infrastructure Exposure: Road salt functions as a public-safety input with mandated demand, not a discretionary commodity subject to economic cycles or substitution risk.

- Structural Deficit Without Short-Cycle Resolution: The gap between domestic production capacity and average demand persists regardless of pricing; new supply requires multi-year development timelines.

- Policy Realignment Toward Supply Security: Procurement frameworks in jurisdictions including New York and Denver increasingly value reliability over spot pricing, favouring domestic supply sources.

- Cost Leadership on a Delivered Basis: Assets with competitive AISC profiles can gain positioning advantages by avoiding freight, currency, and logistics costs associated with imports.

- Logistical Responsiveness as Competitive Advantage: The ability to deliver within days rather than weeks during demand spikes represents structural value not captured in unit-cost comparisons.

- Long-Duration Demand Visibility: Urbanisation, road network expansion, and winter weather variability support multi-decade stability in demand.

- Limited Public Market Access: Private ownership concentration creates scarcity value for publicly traded exposure to the theme.

Why Salt's Deficit Warrants Investor Attention

Commodity markets often misprice assets whose value only becomes apparent during disruption, and salt fits this pattern.

Domestic salt supply positioned to displace imports represents a hedge against logistical failure during severe weather events, a potential beneficiary of policy-level reprioritisation toward supply reliability, and defensive exposure to a stable, government-mandated demand base.

The investment case rests on structural market dynamics rather than speculative upside: a persistent supply gap, a timing mismatch between import logistics and end-user requirements, and emerging policy frameworks that favour supply security over lowest-cost procurement. For investors seeking infrastructure-linked exposure with defensive characteristics, the North American salt deficit represents an under-recognised theme warranting analytical attention.

TL;DR

North America's road salt market represents an overlooked infrastructure investment theme. The US$2.6 billion annual market consumes 28.5–36 million tonnes yearly, yet domestic production consistently falls short, requiring 8–10 million tonnes of imports from Chile, Egypt, and Morocco. This creates a critical timing mismatch: imports require 3–4 week lead times while winter emergencies demand delivery within days. Demand is recession-proof and government-mandated—municipalities face liability exposure if roads aren't treated. Policy frameworks increasingly favour supply reliability over lowest-cost bids, signalling a structural repricing that benefits domestic producers. Development-stage domestic assets with logistical advantages represent asymmetric exposure to this under-recognised theme.

FAQs (AI-Generated)

The market consumes approximately 28.5–36 million tonnes annually, valued at roughly US$2.6 billion. Demand is concentrated in the northeastern United States and Eastern Canada, where winter road treatment is legally mandated for public safety.

Domestic production has consistently fallen short of demand due to geographically concentrated halite deposits, ageing legacy mines, environmental permitting constraints, and minimal capacity investment over two decades. No new salt mine has been developed in North America in nearly three decades.

Imports operate on 3–4 week shipping cycles, while winter storm emergencies require delivery within days. This timing mismatch means imports cannot reliably serve as an emergency supply during severe weather events when stockpiles run short.

Jurisdictions including New York (Buy American Salt Act) and Denver (Environmentally Preferred Procurement) increasingly weigh supply reliability and domestic sourcing over lowest-cost bids, signalling a structural shift in procurement priorities.

Demand is government-mandated, recession-proof, and driven by public safety liability rather than economic cycles. Combined with limited substitution options and only two publicly traded salt companies in North America, this creates scarcity value and defensive portfolio characteristics.

Analyst's Notes

Subscribe to Our Channel

Stay Informed