Top Uranium Plays Soar on Nuclear Renaissance

Uranium hits $74.60/lb amid Iran tensions. Energy Fuels, Global Atomic, ATHA Energy offer diversified exposure to nuclear renaissance. Supply constraints support multi-year bull market

- Iran's nuclear acceleration and reduced IAEA transparency have pushed uranium to $74.60/pound by August 2025, with investors seeking politically stable sources from Canada, Kazakhstan, and the U.S., creating a sustained "fear premium" in the market.

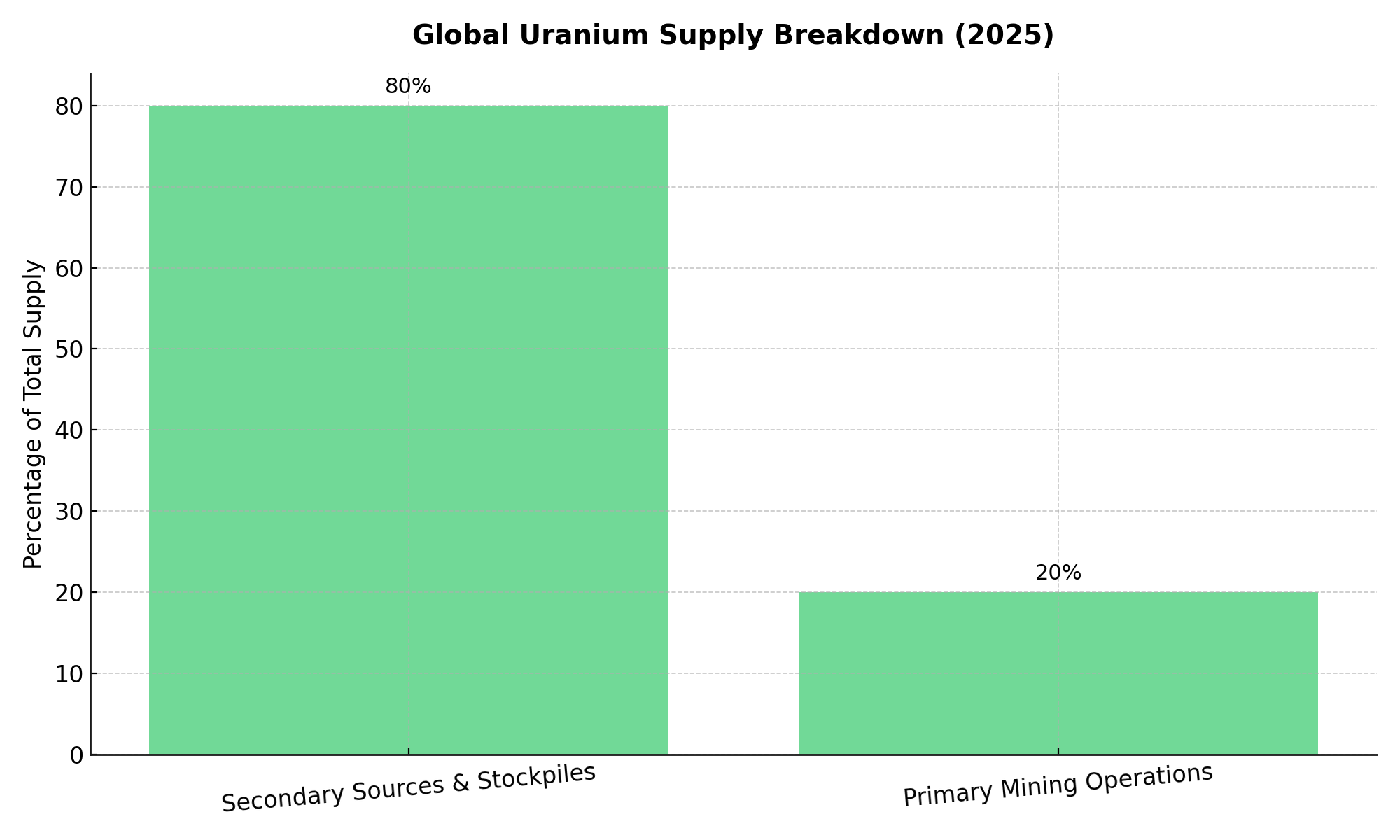

- Over 80% of uranium supply comes from secondary/military stockpiles while new mines face environmental delays and financing issues, coinciding with global uranium market growth projected at 4.86% CAGR through 2032 to reach $13.59 billion.

- U.S. expansion of enrichment facilities, France's €300 million allocation to Orano, and tech giants like Microsoft and Amazon investing in nuclear-powered data infrastructure for AI operations signal strong institutional backing for the sector.

- Leading companies are integrating rare earth elements, vanadium, and other critical minerals into their operations, with Energy Fuels positioning as the only U.S. facility processing monazite for rare earth oxides alongside uranium production.

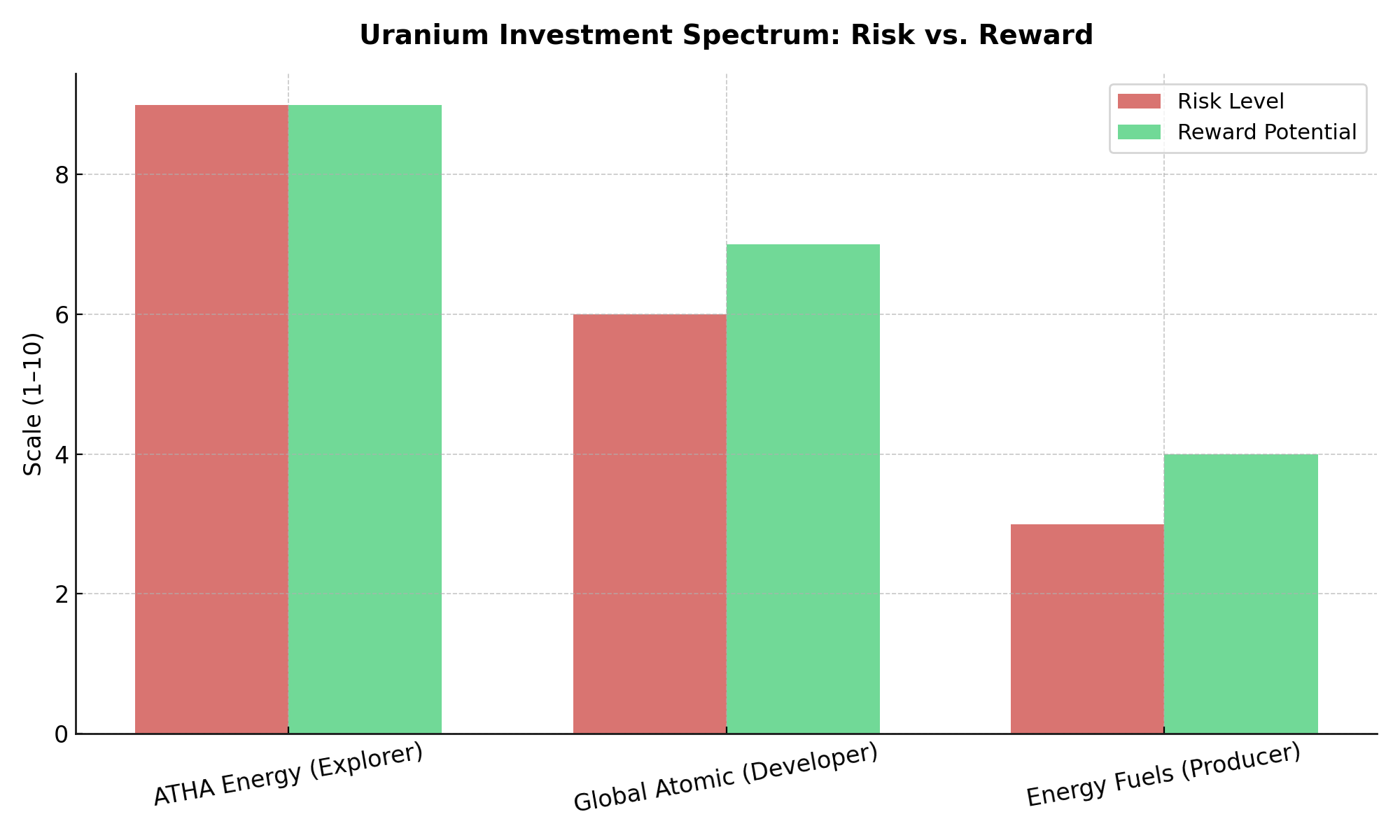

- While established producers like Energy Fuels trade on operational metrics, exploration companies like ATHA Energy (EV ~C$176M) offer significant torque potential compared to developed peers like NexGen (C$5.1B), creating distinct risk-return profiles across the uranium investment spectrum.

Uranium's Evolution from Commodity to Strategic Asset

The global uranium market has undergone a fundamental transformation in 2025, evolving from a cyclical commodity play into a strategic asset class driven by geopolitical tensions, supply constraints, and an unprecedented nuclear renaissance. With uranium prices surging to $74.60 per pound by August 2025, a dramatic increase fueled by Iran's nuclear program acceleration and broader energy security concerns, investors are repositioning their portfolios to capitalize on what many analysts believe is the beginning of a multi-decade uranium supercycle.

This shift represents more than just another commodity boom. The convergence of geopolitical instability, supply chain vulnerabilities, technological advancement in nuclear power, and the urgent need for carbon-free baseload power has created a perfect storm that's reshaping how institutional and retail investors approach uranium exposure. From uranium ETFs posting 30% year-to-date gains to tech giants investing in nuclear-powered data centers, the investment landscape is rapidly evolving.

Iran Nuclear Crisis & Global Geopolitical Tensions Reshape Uranium Pricing Dynamics

The current uranium price surge is intrinsically linked to Iran's rapid nuclear program advancement, which has fundamentally altered global supply security perceptions. Iran's accumulation of 400 kg of near-weapons-grade uranium and deployment of IR-9 centrifuges has reduced the country's breakout time to under a week, according to recent intelligence assessments. This acceleration, combined with strikes on the Fordow and Natanz facilities leading to IAEA inspection suspensions, has created a sustained "fear premium" in uranium markets.

The market's response has been swift and decisive. The European Union's threat of UN snapback sanctions on Iran has intensified uncertainty, driving investors toward politically stable uranium sources. Canadian and Kazakhstani supplies, traditionally preferred for their reliability, now command premium pricing as buyers seek to avoid potential supply disruptions from geopolitically sensitive regions.

Energy Security as National Priority

Beyond Iran-specific concerns, the broader geopolitical landscape has elevated uranium to strategic asset status. The Russia-Ukraine conflict's impact on energy supplies has reinforced nuclear power's role in energy security strategies across developed nations. This shift is reflected in policy decisions: the U.S. has expanded enrichment capacity at Urenco USA, while France has allocated €300 million to Orano for uranium supply chain strengthening.

These policy tailwinds extend beyond traditional nuclear powers. Countries previously skeptical of nuclear energy are reconsidering their positions as climate commitments and energy security concerns converge. The result is a global policy environment increasingly supportive of nuclear power development, creating sustained demand for uranium supplies.

Secondary Supply Dependency & Structural Supply Chain Constraints

A critical vulnerability in the current uranium market is its overwhelming dependence on secondary sources. Over 80% of uranium supply currently comes from secondary sources and military stockpiles rather than primary mining operations. This dependency, while historically stabilizing prices during periods of oversupply, now represents a significant constraint as these secondary sources are gradually depleted.

The transition from secondary to primary supply occurs during a challenging period for new mine development. Environmental permitting processes have lengthened significantly, while financing for new uranium projects remains constrained despite higher prices. This timing mismatch between supply constraints and growing demand creates the fundamental imbalance driving current price appreciation.

Mining Sector Challenges & Opportunities

Global Atomic's Dasa Project in Niger exemplifies both the challenges and opportunities in uranium mining development. As the company notes, theirs is the "only greenfield uranium project under development today," highlighting the scarcity of new supply coming online. The project's economics—with an after-tax IRR of 57% at $75/lb uranium rising to 92.9% at $105/lb—demonstrate the profitability potential for new developments at current price levels.

However, development timelines remain extended. Global Atomic began its ramp decline in late 2022, reached the ore body by late 2023, and targets commissioning for H2 2026. This multi-year development cycle, repeated across the industry, ensures supply constraints will persist even as prices incentivize new project development.

Small Modular Reactors (SMR) & Technology Evolution Drive Next-Generation Nuclear Demand

The nuclear industry's evolution extends beyond traditional large-scale power plants to include Small Modular Reactors (SMRs), which are gaining strategic attention amid supportive policy environments. Companies like NuScale Power and TerraPower are positioning for growth as SMR deployment accelerates, creating new categories of uranium demand with different timing and volume characteristics.

SMRs represent a paradigm shift in nuclear deployment, offering shorter construction timelines, reduced capital requirements, and enhanced safety features. Their modular nature allows for incremental capacity additions, making nuclear power accessible to smaller grids and industrial applications previously uneconomical for traditional nuclear plants.

Troy Boisjoli, CEO of Atha Energy, highlights the unprecedented nature of current nuclear demand growth:

"We see extremely robust demand being layered on in the nuclear energy space that you have to go back to the 1960s and 70s to find a comparable ramp-up. That's why we're investing heavily in projects with the scale this market is going to need."

Data Center Nuclear Integration

Perhaps most significantly, major technology companies are directly investing in nuclear-powered data center infrastructure to support AI operations. Microsoft and Amazon's commitments to nuclear power represent a new category of uranium demand driven by the exponential growth in computational requirements for artificial intelligence and cloud computing services.

This trend reflects uranium's expanding role beyond traditional electricity generation into specialized industrial applications. The combination of 24/7 power requirements, carbon neutrality goals, and long-term price predictability makes nuclear power particularly attractive for data-intensive operations.

Energy Fuels' Integrated Approach: Investment Strategies Across the Uranium Value Chain

Energy Fuels represents the integrated critical minerals approach, positioning itself as more than a pure uranium play. The company's Q2 2025 production of 665,000 lbs U₃O₈ from multiple mines demonstrates operational capability, while its expansion into rare earth elements, vanadium, and other critical minerals provides diversification benefits.

The company's White Mesa Mill stands as the only operating conventional uranium mill in the U.S. with 8M+ lbs annual capacity, providing strategic infrastructure advantages. More importantly, it's the only U.S. facility processing monazite for rare earth oxides, positioning Energy Fuels uniquely in the critical minerals supply chain beyond uranium.

Energy Fuels' cost trajectory improvement, from $50-55/lb in 2025 to projected $30-40/lb in 2026, demonstrates operational efficiency gains that should enhance margins as uranium prices remain elevated. The company's four long-term contracts with U.S. utilities through 2030 provide revenue stability while maintaining spot market exposure for additional volumes.

Mark Chalmers, CEO of Energy Fuels, captures the optimism driving the sector's current momentum:

"Well, I just think, I think, you know, we're in this new era that is really exciting. And I think that, you know, nuclear over 50 years has proven itself and the future looks brighter than I've ever seen it.”

Pure-Play Exploration: ATHA Energy's Discovery Potential

ATHA Energy represents the high-risk, high-reward exploration approach with 7M+ acres across Canadian uranium districts. The company's positioning as "Canada's Premier Uranium Exploration Company" reflects its scale advantage in a consolidating sector.

The Angilak Project's 43.3M lbs historic resource and conceptual exploration target of 61-98M lbs U₃O₈ provide substantial resource upside potential. More importantly, the project's district-scale potential along a 31km corridor offers the possibility of a major discovery that could transform company valuation.

ATHA's diversified approach across the Athabasca Basin, Thelon/Angikuni Basin, and Central Mineral Belt provides multiple opportunities for success. The company's 10% carried interest in parts of NexGen and IsoEnergy lands offers leveraged exposure to these companies' exploration success without additional capital requirements.

Near-Term Production: Global Atomic's Development Timeline

Global Atomic's Dasa Project offers the clearest near-term production catalyst among development-stage companies. With commissioning targeted for H2 2026 and yellowcake delivery expected by Q1 2026, the company provides investors with defined timeline exposure to production growth.

The project's highest-grade uranium deposit in Africa status, with reserve grades of 4,113 ppm (0.41%) rising to 5,109 ppm in the first 12 years, positions it in the industry's lowest cost quartile. The 68.1M lbs U₃O₈ production over 23 years provides substantial scale for a single-asset developer.

Global Atomic's four uranium offtake agreements, including three with U.S. utilities, demonstrate market validation and provide revenue security for financing completion. The company's zinc recycling joint venture with Befesa Zinc adds cash flow diversification outside uranium market cycles. As Global Atomic recently noted:

"Positive Credit Committee review will mark a significant step forward towards loan approval by the Bank's Investment Committee and Board of Directors.”

Exploration Excellence: IsoEnergy's Discovery Momentum

The exploration segment continues to deliver exciting developments, with companies like IsoEnergy making significant strides in resource definition and expansion.

Philip Williams, CEO and Director of IsoEnergy, illustrates the ongoing exploration success driving sector optimism:

"Each new hole is giving us a clearer picture of the mineralized system at Nova. The assays confirm the strength of the mineralization and reinforce the importance of this discovery.”

ETF Performance & Investment Vehicle Market Dynamics

Uranium ETFs, particularly the Global X Uranium ETF (URA), have delivered 30% year-to-date gains, providing broad sector exposure for investors seeking uranium market participation without individual stock selection risk. These vehicles offer liquidity and diversification advantages while capturing sector-wide appreciation.

The ETF approach particularly benefits from the sector's correlation during uranium price appreciation phases. As geopolitical premiums and supply constraints affect all uranium assets similarly, broad-based exposure captures this systematic appreciation while mitigating company-specific risks.

Critical Minerals Portfolio Integration

Leading uranium investors are increasingly adopting diversified critical minerals approaches, combining uranium exposure with lithium, rare earth elements, and other strategic materials. This strategy recognizes the interconnected nature of clean energy supply chains and energy security concerns driving commodity appreciation.

Energy Fuels' rare earth element production capabilities exemplify this integration. The company's commercial-scale NdPr production achieved in 2024, with heavy REE separation expected by 2025, creates multiple value streams from shared infrastructure and expertise.

Geopolitical Risk Diversification & Portfolio Construction Strategies

Current uranium investment strategies must account for heightened geopolitical risks affecting different jurisdictions differently. Niger, despite hosting Global Atomic's high-grade Dasa Project, faces political instability that could affect operations. Conversely, Canadian and U.S. assets benefit from stable regulatory environments but may face higher operational costs.

Geographic diversification across stable jurisdictions provides risk mitigation while maintaining exposure to the uranium price appreciation theme. Companies operating in multiple countries or those with assets in Tier-1 jurisdictions command valuation premiums reflecting this risk reduction.

Timeline & Liquidity Considerations

Uranium investments span multiple time horizons, from near-term production growth to long-term exploration potential. Energy Fuels and Global Atomic offer relatively near-term operational catalysts, while ATHA Energy provides longer-term discovery upside potential.

Liquidity considerations vary significantly across uranium investments. Larger producers and development companies typically offer better liquidity than junior explorers, an important factor for institutional investors or those requiring position flexibility.

The Investment Thesis for Uranium

- Combine established producers (Energy Fuels), near-term developers (Global Atomic), and exploration upside (ATHA Energy) to capture different stages of the uranium cycle while managing risk through operational diversity.

- Prioritize companies like Energy Fuels that combine uranium production with rare earth elements and other critical minerals, providing multiple value drivers and reduced dependence on single commodity pricing.

- Iran nuclear negotiations, Russia-Ukraine conflict resolution, and broader energy security policies will continue driving the uranium price volatility position for sustained elevated prices while maintaining flexibility for policy changes.

- New mine development timelines of 3-5 years ensure supply constraints will persist through 2028-2030, while SMR deployment and data center nuclear adoption provide new demand categories supporting higher sustained prices.

- Canadian and U.S. uranium assets command valuation premiums for political stability; this premium should persist and potentially expand as geopolitical tensions continue affecting global supply chains.

- Current uranium price appreciation reflects early stages of a potential multi-decade nuclear expansion driven by climate policies, energy security concerns, and technological advancement position for sustained sector outperformance beyond current geopolitical catalysts.

Analyst's Notes

Subscribe to Our Channel

.jpg)

Stay Informed