Toubani Resources - (TSX-V: TRE) - Investors Drawn to ASX Listing and Exploration

Interview with Danny Callow, President & CEO of Toubani Resources (TSX-V:TRE)

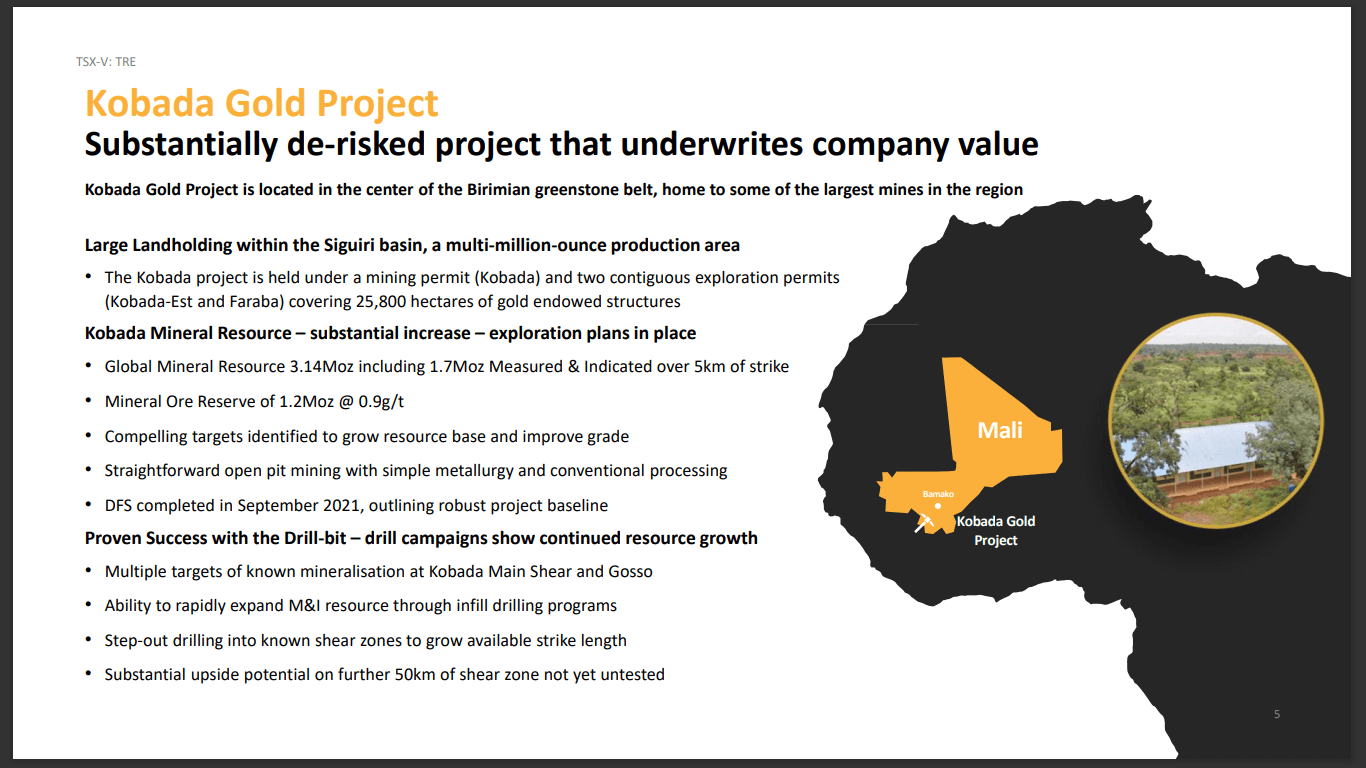

Toubani Resources Inc. (Formerly African Gold Group Inc.) is a listed Canadian gold company with expansive holdings in West Africa’s prolific Birimian Greenstone Belt including more than 460 square kilometres across Mali and Burkina Faso. The company is focused on the development of the Kobada Gold Project located in Southern Mali, a low capital and low operating cost gold project with the potential to produce more than 100,000oz of gold per annum along with a 16-year mine life.

Matt Gordon caught up with Danny Callow, President, and CEO, Toubani Resources. Mr. Callow has over 25 years of experience in building and operating mines in Africa. He was Head of African Copper Operations for Glencore PLC, CEO and Executive Director of Katanga Mining Limited, and CEO of Mopani Copper Mines PLC. Mr. Callow is a Professional Mining Engineer and holds an MBA from Henley Management College, a Bachelor (Hons) of Mining Engineering from the Camborne School of Mines, and a Non-Executive Director professional diploma from FT-London. Mr. Callow has overseen more than $2.5Bn in mining projects from conception through to full production.

Company Overview

Toubani Resources is a Canadian exploration and development company with a focus on developing a gold platform in West Africa. The company has a highly experienced board and management team with a proven track record in the African mining sector, operating mines from development through to production. The company was founded in 2002 and is headquartered in Toronto, Canada. It is listed on the Toronto Stock Exchange (TSX-V: TRE).

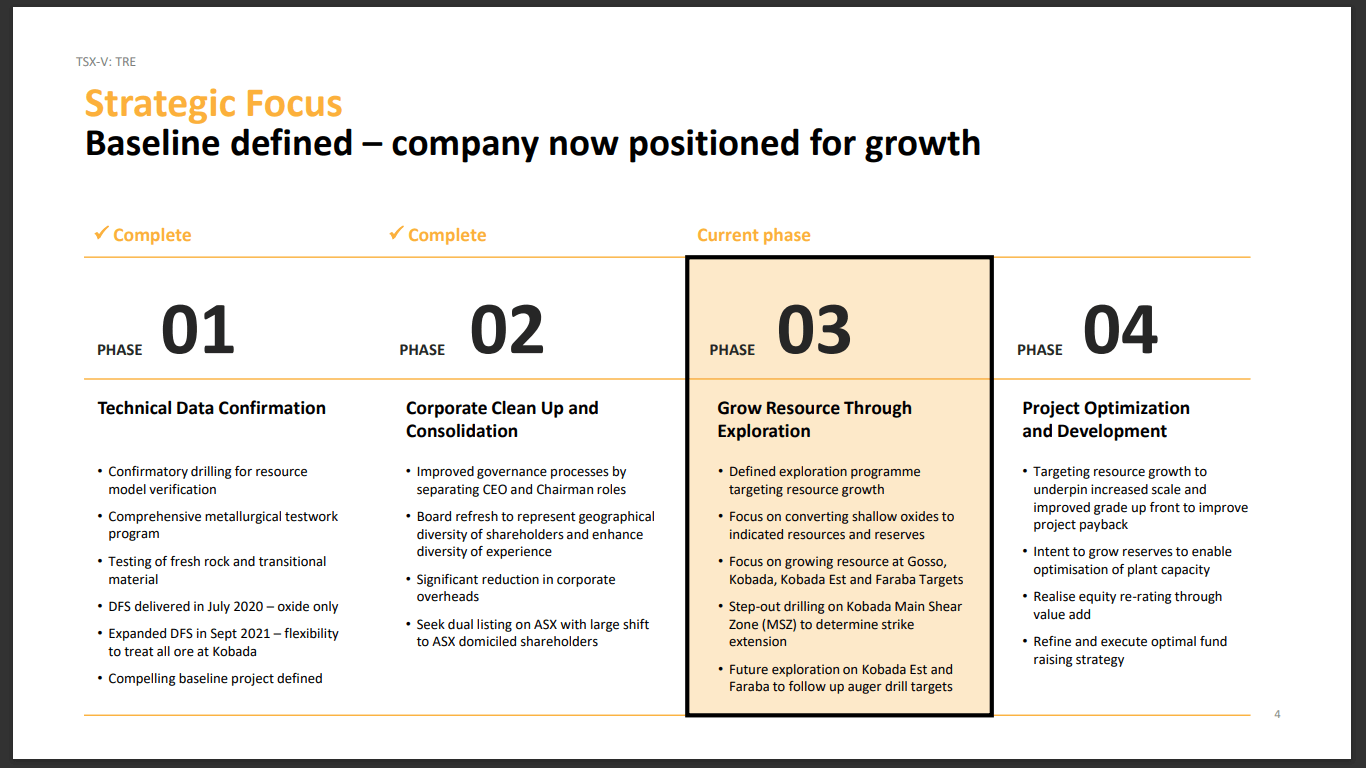

Toubani Resources is a TSX-listed company that is soon to be listed on the Australian Stock Exchange (ASX). The company has a flagship project in southern Mali, the Kobada project. Here, the company has delineated 3.2Moz of resources along with a 1.25Moz reserve. The company published a DFS (Definitive Feasibility Study) in late 2021, that shows a 100,000oz/year mine for 10 years with plenty of exploration upside. The company is currently going through the paperwork for the ASX listing, which is expected to be completed within the next 1-2 weeks. The listing will enable the company to grow its investor base.

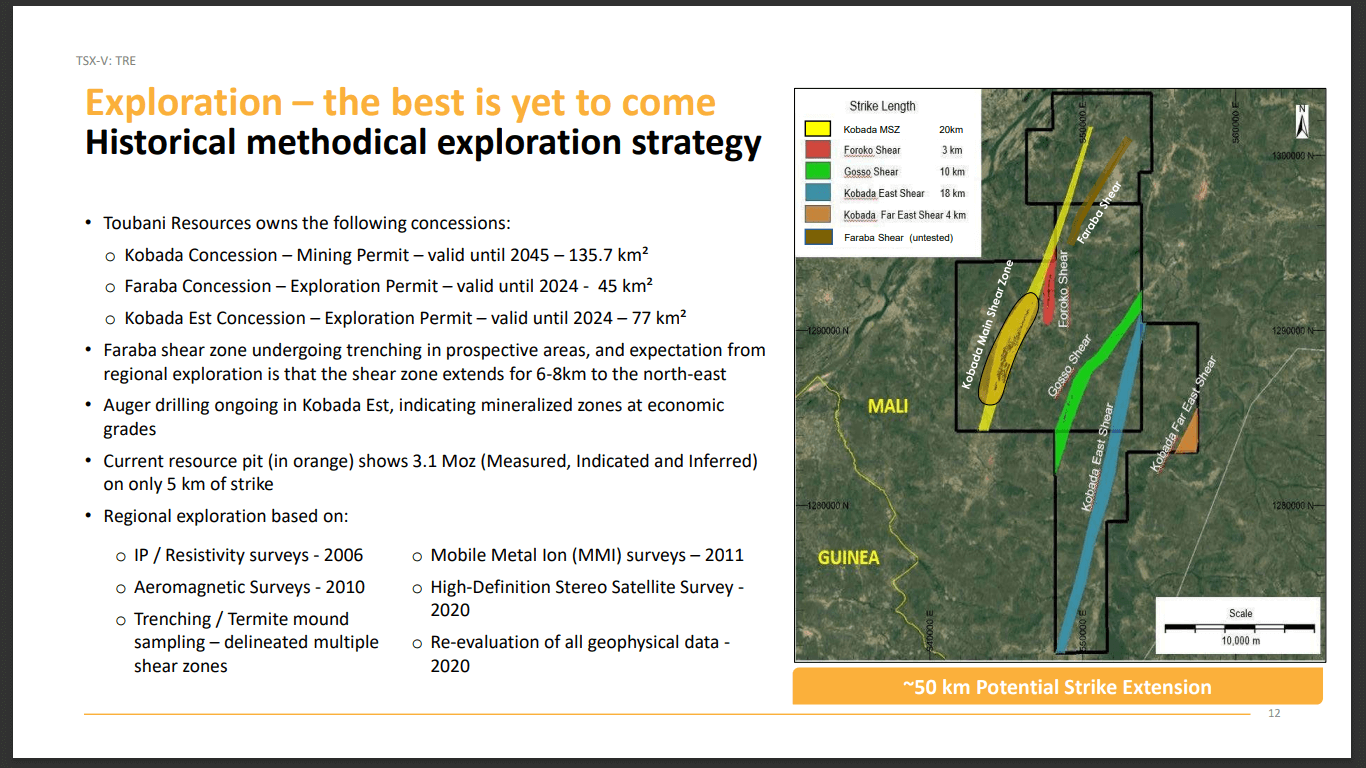

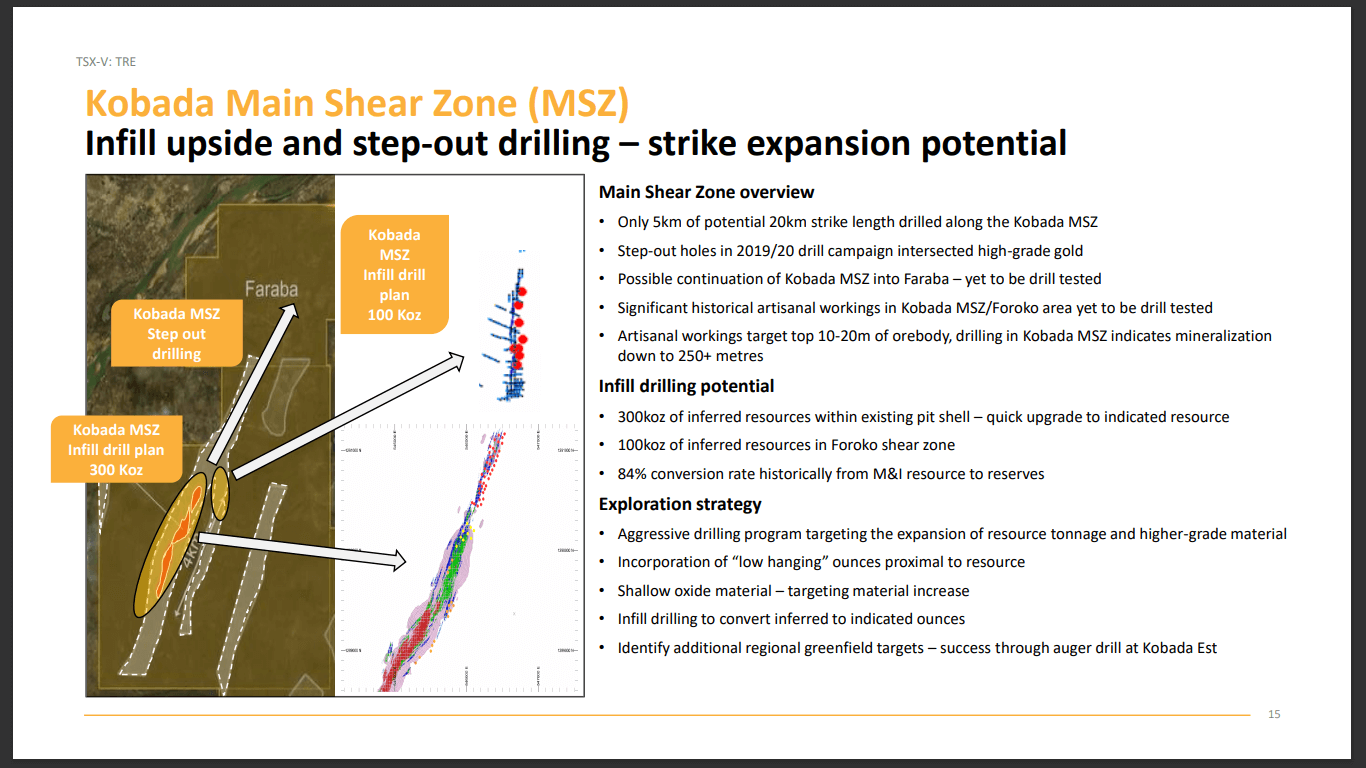

Due to the downward pressure on the gold price and the ongoing inflationary environment, it is harder for a company to market itself and raise capital. While the company has a lot of discussions surrounding the capital raise, there is a lot of pressure from some of the Australian investors to put the drills back into the ground. The company anticipates that it likely has 50km of shear zones that need to be drilled. It has laid out an aggressive drill program on the back of the IPO (Initial Public Offering) and raise. It expects good news on the strike extension. The company’s first priority is to extend the strike length and demonstrate that it is bigger than 5km. This can be revisited later infill drill and increase the resource significantly. The company anticipates that over the next 12-24 months, there will be a sizable increase in the resource.

While the company is looking to raise additional capital, the raise should be acceptable to the existing shareholders. It has a number of really good institutions in Australia that are on board. The stakeholders’ preference over the last 6 months has been on drill operations. Drilling is a relatively cheap way to add value to a project as it can add a lot of ounces to the existing resource. The company has the opportunity to substantially increase the strike length.

Ongoing Operations

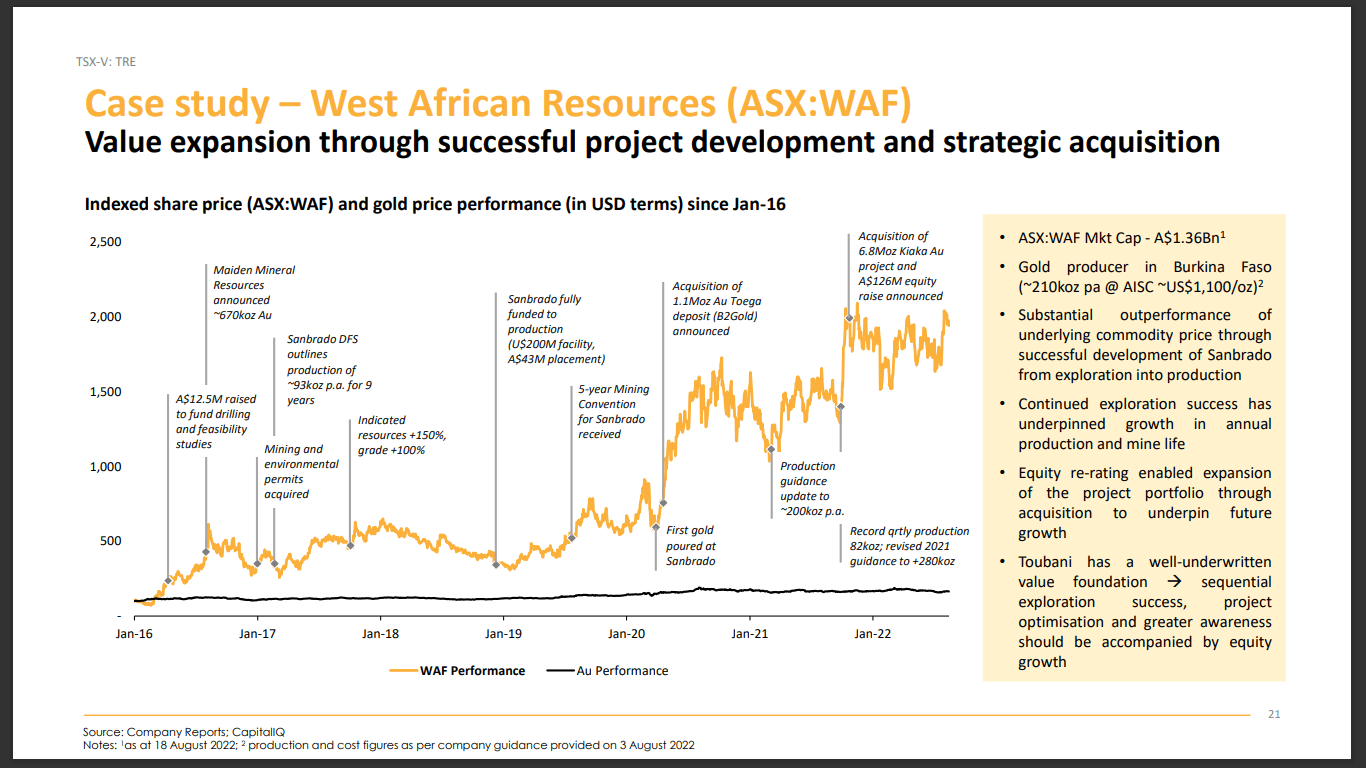

Toubani Resources is looking forward to a potential re-rating. Currently, the company sits at about $4 per EV resource ounce. In comparison, the company’s peers in Mali are currently sitting at $20-$25/oz. Even if a re-rate is based on EV total resource, the company believes it should be at least 5x-6x its current value. It has been successful in developing a strong baseline that comprises a 3Moz resource along with a 1.25Moz reserve. The asset is fully permitted. Through the DFS, the company found that the gold can easily be treated through a process plant. Every ounce added will add substantial value to the project.

According to the company, a DFS is good on the day it is published, and following that, everything is variable. The company was quite conservative with the DFS cost metrics, while also including a wide range of sensitivity in it. Interestingly, the company has maxed out on the gold reserve and production. Additional ounces will provide it with more flexibility, which will enable the company to work on different plant throughputs, which, in turn, can help bring in the higher-grade stuff early.

The company isn’t necessarily looking to produce more than 100,000oz a year but is still open to the possibility. It isn’t looking to extend the mine life beyond 16 years, but the additional ounces do provide it with the flexibility to play around with the mine plan and optimization in order to get more upfront and steady ounces over a longer period.

Tesoro Resources is a good example of this strategy. The company started off with a 3Mt/year throughput plant, which was later increased to 4.5Mt/year as the resource ounces grew. This led to a starkly different model than the company had started with. Toubani Resources has a great baseline along with a significantly de-risked project. The company has already determined the gold extraction and treating process and has finalized the plant design. It is now looking to work on the plant throughput so that it can bring higher grades forward. At the same time, the company intends to add ounces in the next 12-24 months.

Material Grades

Within the deposit’s shear zone structures, the grades can be upwards of 100g/t. Having the flexibility of mining these ounces provides an opportunity to stockpile high-grade material and blend it through the plant. At the northeast boundary of the Kobada project, Cora Gold has come out with a resource with 1.15g/t material grades, which is a bit higher than Toubani’s 1g/t. Cora Gold anticipates that it will put about 1.2g/t-1.4g/t into the process plant. The company is currently working on a DFS. This means that if Toubani moves to the north, it can potentially see some improvements in grades. It is important to note that within the resource, Toubani Resources has found some very high-grade pockets. Once it has more ounces to play with, the company will have more flexibility in devising a mining strategy. It is often seen that in West African projects, multiple satellite pits are mined and combined with the lower-grade stuff.

Toubani Resource has taken its entire resource and reserves and mined them in one big pit. While this strategy lowers the overall grade, it also reduces the cost element. Once the company has additional ounces, it can be more selective and bring the material grades up.

ASX Listing

Toubani Resources is prioritising its ASX listing. Over the last 18 months, the company has seen significant support from its Australian investor base. These investors have also supported the company in substantial ways. This time around, Cornerstone Capital was also a participant in the capital raise. Toubani Resources is also bringing some new institutions on board that are quite big in Australia. As a result of these factors, the company anticipates that its institutional shareholder base post-IPO will look highly attractive. All of the interested parties understand that the asset is going to get bigger and it will enter production at some stage.

The investors have indicated that they will continue to support the company in the market. In Australia, the company has a bigger pool of capital available. The investors here understand the project better compared to West Africa. The Australian investors seem to be willing to drive the story forward.

The company intends to carry out extensive marketing for the Kobada Gold Project. Recently, the company’s representatives were in Perth, Australia. They had between 20-25 meetings that were highly positive from a stock perspective. Once the company gets listed on the ASX, it expects to see good volume along with a lot of support. If the company continues to deliver good drill results as it has in the past 2-3 years, re-rating could possibly happen fairly quickly.

Cash Position

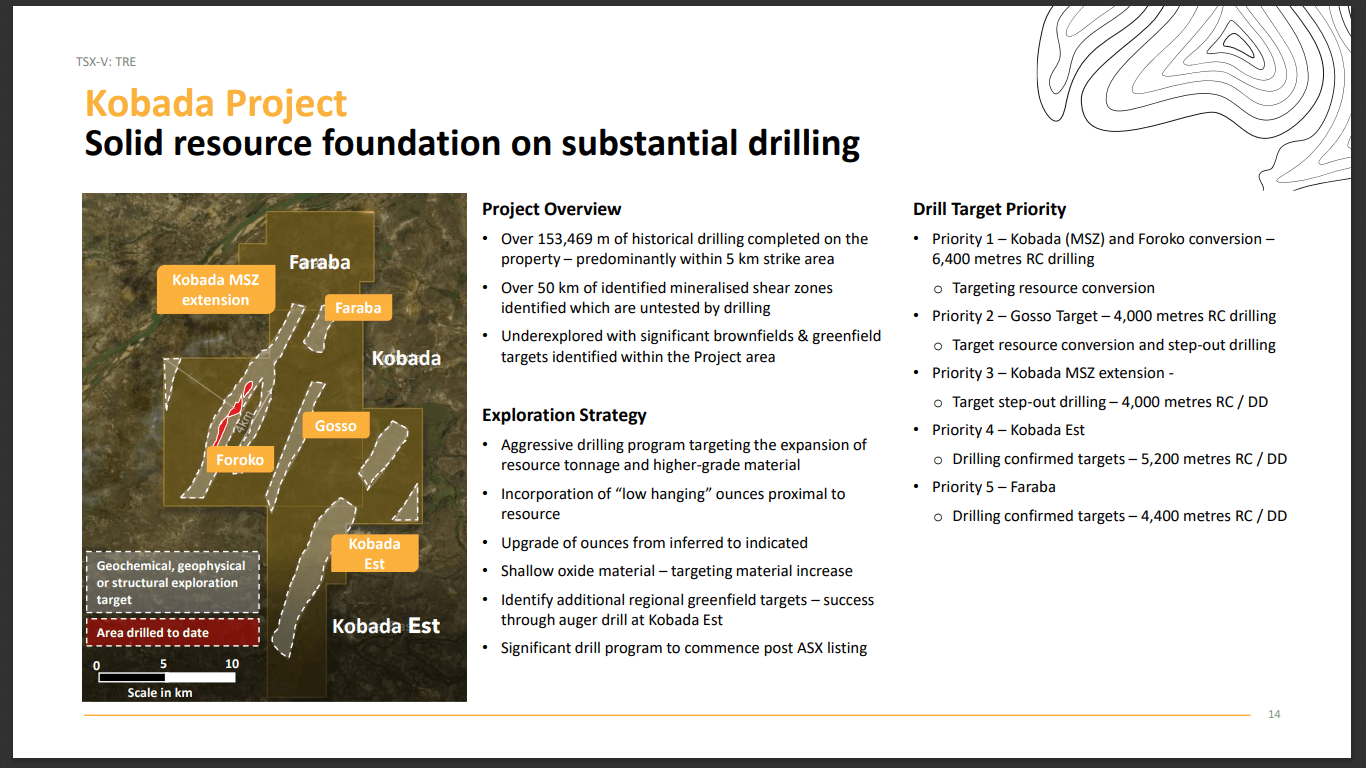

Toubani Resources expects to have around AUD$6M-$7M in the bank following the IPO, listing fees, and other expenditures. The company intends to put all the money in the ground, which would cover the first 15,000m of the drill program. This would encompass a fairly large area of strike length, which the company is looking to determine. Following this, it plans to raise additional funds and come back for infill drilling. Currently, it has 55km of shear zones on the property, out of which, only 5km has been drilled so far. Over the next 6 months, the company is looking to extend the strike length. This would lead to an increase in the news flow, which, in turn, will help people better understand the resource potential.

Targets 2022 and Beyond

The flexibility of having additional ounces leads to a better financial model. It can be highly attractive for mid-tiers or majors as a second or third project. While the company is open to the possibility of a potential M&A (Mergers and Acquisitions), it is looking for a better valuation. Once the project is re-rated closer to its true value, it could serve as an exceptionally good asset for a second or third project.

The Kobada project has had 2 DFS in the last 3 years. This is because the company focused on oxides first. Oxides are always easier to process as they can be put through a fairly straightforward CIL (Carbon-in-Leach) process. In comparison, fresh rock and sulphides can be trickier to process. Between 2020 and 2021, the company took a bulk representative sample across the entire ore body and put it through sulphide testing. Interestingly, 94%-95% recoveries were achieved through the CIL using the same process plant as the oxides. The only difference here is that the material needs to be milled a little bit finer.

Essentially, the deposit has an ore body with oxide transitional and sulphides, all of which can be processed through a typical gravity plus CIL plant. It does not feature any penalty minerals such as arsenic. Material extraction is a simple, straightforward process that was made easier because the project features a geology of oxide sitting on top of transitional sitting on top of the sulphide. Unlike some deposits, the Kobada Gold Project does not feature a mixed ore body.

Toubani Resources renewed both its exploration permits last year along with the environmental permits. The mining permit is valid until 2045. Despite the changing political landscape, the company has maintained strong relationships with the government. It is looking to deploy the drill rigs by November-end or early December.

Over the last 2 decades, the Mali government has done a commendable job in growing gold production in the country. In terms of output, Mali sits in the third or fourth position. The country has a responsible mining code which is balanced between perks offered to the country and the investors. The Kobada project is a great asset that is going to be built at some stage.

Over the last 3-4 months, companies including B2Gold have come out with USD$50M exploration programs to expand its resource in Mali. Barrick gold has also come out to support its Mali operations by further increasing the reserve life. These developments serve as encouragement for investors. Toubani Resources expects to get listed on the Australian Stock Exchange within the next two weeks.

To find out more, go to the Toubani Resources website

Analyst's Notes

Subscribe to Our Channel

Stay Informed