Troilus Gold (TLG) - Reinvention Through Aggressive Drilling

Troilus Gold Corp is a Gold exploration and development stage mining company. Their project offers a unique opportunity for a mine restart in Quebec Canada

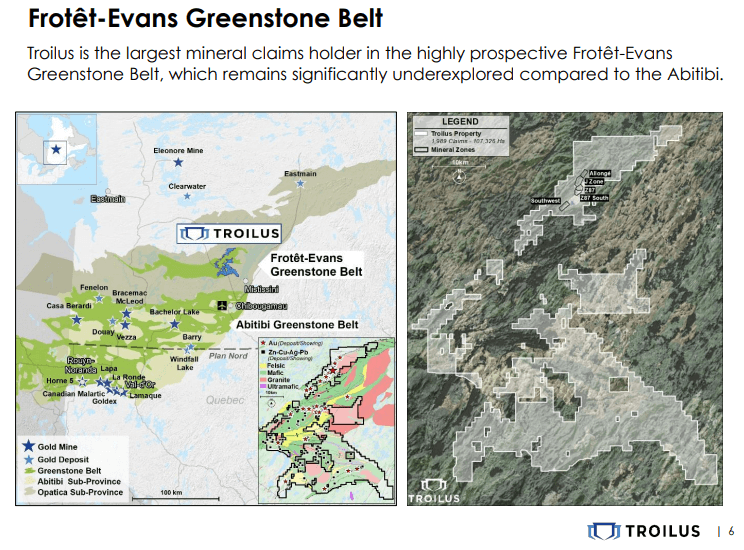

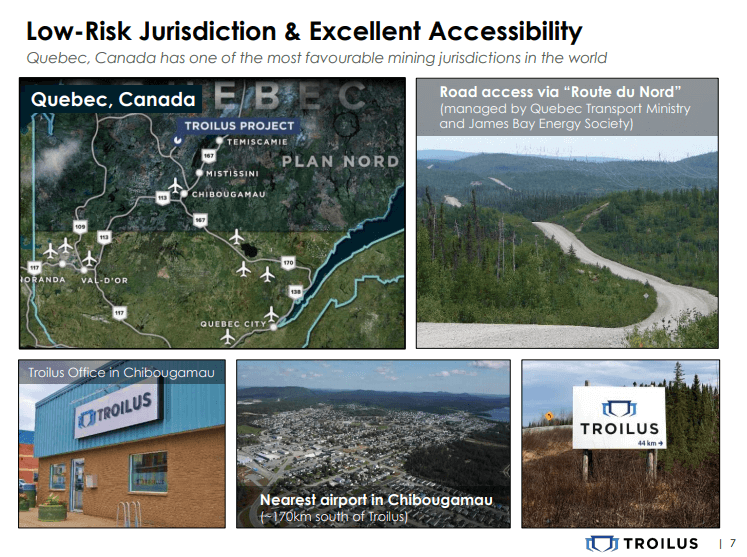

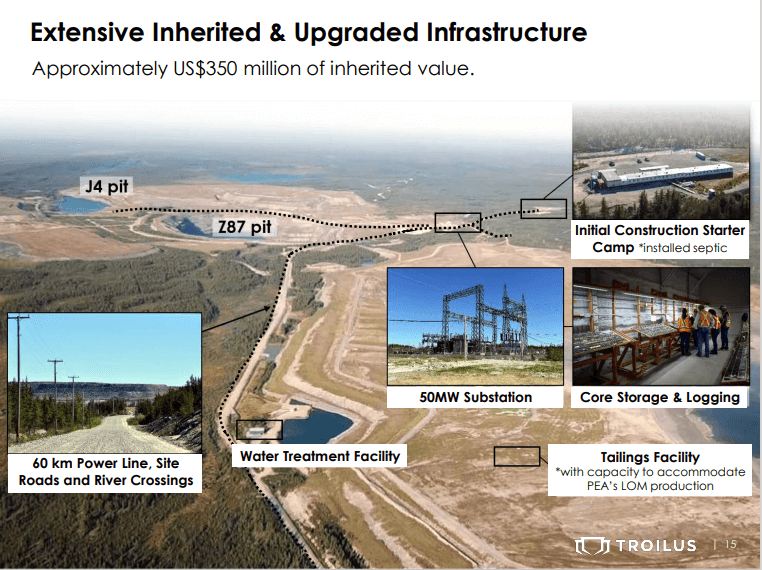

Troilus Gold is a Gold exploration and development stage mining company. Their project offers a unique opportunity for a mine restart in Quebec, Canada - one of the world’s most attractive mining jurisdictions - with significant existing infrastructure worth an estimated US$350 million. Over 80,500m of drilling over the last 2 years has resulted in a 142% increase to estimated indicated mineral resources and a 350% increase to estimated inferred resources.

We met for the first time with Justin Reid, CEO of Troilus Gold as we have been keen to talk to them for a while to find out more about the company.

Company Overview

Troilus Gold is a CAD$150M-250M market cap, well-capitalized Quebec-focused explorer-developer. They have taken an historic-producing asset which produced 2Moz over 14-years and reinvented it. They had an aggressive drill programme and are now sitting with 8.1Moz equivalent at PEA and CAD$300M-400M in inherited and upgraded infrastructure. Troilus is working through the process towards ultimately getting back into production.

CEO's Background & Team Experience

Justin Reid is a geologist by training and was an early mining analyst for Eric Sprott in Cormark Securities and spent some time leading the Mining National Bank. He has since taken a Gold asset, with a team, almost to development, which they sold to Alex Black at Rio Alto. They kept the team together, acquired Troilus and are trying to do the same thing.

Business Plan: Data Inherited & Progress so far

The team identified the history of Troilus first of all as a low-grade bulk tonnage asset put into production in a CAD$350 Gold environment. The objective of the mine, for Inmet who operated it, wasn't necessarily to be a Gold producer. They wanted the Gold multiple as a global base metal, and they accomplished that. As soon as the reserve was exhausted it was put on care and maintenance and then eventually shut down because First Quantum came in.

It was clear that Inmet hadn’t done any work with the mine as it was undercapitalized and underexplored. It’s a lower-grade bulk tonnage deposit which in an appreciating environment could become very profitable and has opportunity to expand.

They inherited 2Moz underground, below the Z87 pit. From 350m down to 500m of 1.8g/t equivalent, very consistent grade - 50m thick 1.2km strike length, very analogous to Agnico’s Goldex Mine. More importantly, they inherited, as well as 2 flooded pits, about CAD$350M-$400M in infrastructure: roads, power line, substation, fully permitted 6.5km sq tailings facility, which is the real value. All the earthworks have been done, septic, sewer, water at the camps, buildings etc. Some upgrading needed to be done but they have a mining lease, a permitted tailing and some infrastructure, which gets them halfway there.

Managing Risks: Hurdles & Liabilities

After spending time at Goldex, the team came to the realization that they did think there was an economic entity there, and they were willing as a management team and a board to take on that liability. They came to market, the shareholders agreed with them and they did it. But they had to ensure they had the right people to manage that risk.

Financing it All: Why is the Shareholder Registry so Institution-Heavy?

Troilus Gold raised CAD$12.8M in February, then CAD$25M in June. Apart from the management team, the company is 90% institutional which is unusual for a junior company with their market cap. But it is simply a case of that's what they know, having always worked in institutional markets. The company is expanding now with work at Troilus moving ahead with 6 drills, PEAs, engineering and environmental work. It's a great opportunity for the team and their goal is to invest and to be a producer which has been their goal since day one.

Great PEA Numbers, yet Market Doesn't Care; Why the Disconnect?

There are some really great numbers in the PEA with 246,000oz average production for the first 14 years, the AISC is around CAD$1,000. The numbers on the PEA, which is plus or minus 30%, suggest that they could have made the right call and are looking at something which should get the market excited, but it's not. Troilus Gold is a CAD$140M market cap so where is the disconnect?

There are a couple of reasons for this disparity, firstly, the institutional investors who are there when the company needs them, but they don't trade. There’s not a lot of liquidity, so they buy their stock and they hold the stock. Secondly, they are a lower-grade bulk tonnage deposit. They’ve expanded the resource by 6.5Moz in 2-years which is incredible, but they are a low-grade bulk tonnage deposit which doesn’t seem hugely exciting for the market.

The company needs to be focusing more on the marketing side and get the word out to the retail side to increase their rating within the market. They have spent a huge amount of time and money in the last 2.5-years building the team to do it and now that is the absolute focus.

Mining in Quebec: ESG, Permits, & Relations with Locals

Social licenses are extremely important and so Troilus has a specific team for ESG and management. It is about focusing, communicating and documenting it in a way that is expected by the regulators. Quebec established a new program called ECOLOGO about a year ago which gave Troilus a pathway to meet their objectives and they were the first to receive their ECOLOGO certification in Quebec and in Canada. They have won awards for sustainability at the AMQ, with Agnico and others, and the government acknowledges that they're doing the right things. This just means that when they go through the various stages of permitting, it will make things faster for the company.

On the First Nation stakeholder side, Troilus Gold was lucky as they have inherited an incredibly good relationship with the Mistissini Cree who are very commercial. It was the first IBA ever signed in the James Bay, between Inmet and Mistissini and Troilus signed their pre- development agreement 3-weeks into being a company, and they were ready to go. They meet all the various requirements and they create employment and contracting. There was already a relationship with the mine, and it was favourable, so it's up to Troilus Gold to keep up that relationship.

Troilus Gold will need to empty water from the 2 pits so they have already completed an EIA on the dewatering and have completed a full environmental impact assessment. They included the First Nations from day one and all the consultations with their stakeholders, including the government and the environment has culminated in the permit to dewater being agreed 5-months ago. So, in the spring they will be in a position to start dewatering.

PFS Timeline & Expectations: Open-Pit VS Underground

The plan is to complete the PFS this year as they have the capital to do it and the team and the plan is in place. They have over 5Moz of indicated with 6 drills going on multiple fronts. They're spending CAD$1.5M on geo-tech work at the moment and doing tailings characterization, all parts of the engineering. They are expanding the resource and the PEA currently is 3/4 open pit, ¼ underground, coming in at the end of the mine life. It's a low-grade bulk tonnage deposit, analogous to a number of other underground operations. It's very economic and they have had success drilling, finding Gold at under CAD$3/oz now, which is market-leading. They have a 98% hit rate in their drilling and have added 6.5Moz open pit material in 2.5-years.

A new discovery was made last December called the Southwest, 3km from the mine. After one month of drilling, they have 600,000oz at surface, which is almost twice the grade of the main deposit so they have 3 drills going on that and have already finished 20,000m, with more to come. There is a delay on those results which are currently still in the lab. What they hope to show is a 20+-year open-pit and will think about the underground later or optionality in a different environment.

For a 250,000oz producer, this is good on a capital intensity basis. The inherited infrastructure: power, substation, roads, tailings, permits, etc, gives you CAD350M-$400M of inherited value, and they've invested close to CAD$20M in 2-years upgrading it.

So what else does the project need? They need a CAD$187M, 35,000t/day mill and some ancillary buildings in the plant. It's an CAD$850M-$900M mine to build from scratch, but because of their location, what they've inherited and the upgrades they have already made, they will be able to do it for under CAD$400M.

Getting the Market Excited: Timeline for Deliverables

Drill results will usually get the market excited, especially if there are some high-grade numbers in there and Troilus is expecting results back from the drilling at the Southwest zone imminently. Drills are still turning and they are drilling 7,000m/month now for the foreseeable future in a combination of infill drilling, expansion drilling and Southwest drilling, to make the deposit better.

Troilus needs good communication with the market. There is a huge, broad, low-grade halo to the deposit but they have now identified a cross-cutting, deformation of a high-grade zone which replicates section after section across the belt which they are excited to bring into the mine plan and convey to the market.

Easy to Raise Money so far, Will That Continue in the Future?

Troilus Gold plans to open up to retail investment going forward. They have supportive shareholders who are there for 5-6-years but they need other money and need diversification in the shareholder group. The institutional investors are the strategic investors but the company needs to build out their retail shareholding because that really drives the stock.

The Troilus story is an interesting one and we’ve been wanting to talk to the company for a while. We like the accelerator component to this as it looks like things are really moving forward quickly.

To Find out more, go to the Troilus Gold website

Analyst's Notes

Subscribe to Our Channel

Stay Informed