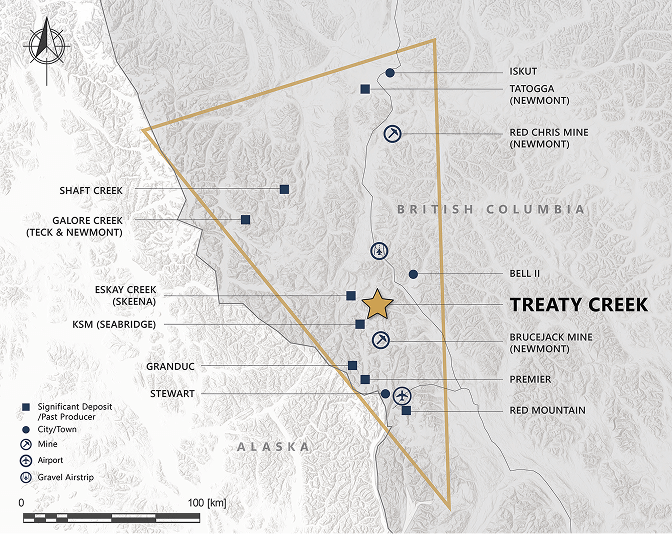

Tudor Gold's Treaty Creek: Key Milestones Achieved, Critical Questions Remain Ahead of the PEA

Tudor Gold advances Treaty Creek across ownership, resource definition, metallurgy, and social licence, with key risks and catalysts remaining ahead of the Summer 2026 PEA.

- Tudor Gold Corp. has advanced four key areas at Treaty Creek over the past twelve months: ownership structure, resource grade resolution, metallurgical testing, and social licence, each representing a substantive step toward a preliminary economic assessment (PEA).

- The acquisition of American Creek Resources increased Tudor Gold's interest in Treaty Creek to 80%, simplifying project governance ahead of the PEA; the remaining 20% interest held by Teuton Resources is under active discussion.

- The January 2026 updated mineral resource estimate (MRE) applied higher net smelter return (NSR) cut-off values to isolate higher-grade mineralisation targeted for the initial underground mine plan, a more operationally significant output than the headline indicated ounce figure of 24.9 million ounces of gold.

- Preliminary metallurgical test work confirmed gold recoveries of up to 85.1% and copper recoveries of 85.8% using conventional flotation across two distinct ore domains, with the final programme across all three deposit zones targeted for completion by end of March 2026 ahead of the PEA.

- The underground exploration ramp, currently in the permitting process, is the most consequential near-term operational catalyst; approval would enable year-round drilling of the SC-1 high-grade complex by bypassing the region's seasonal weather constraints that currently limit surface drilling.

From Five Risks to a PEA: How Treaty Creek's Development Case Has Narrowed

Tudor Gold Corp. has moved through a concentrated sequence of development steps at its Treaty Creek Project in British Columbia's Golden Triangle by consolidating ownership, certifying an updated mineral resource estimate (MRE) through an independent National Instrument 43-101 (NI 43-101) technical report, publishing preliminary metallurgical results across two ore domains , and securing formal agreements with the Tahltan Nation and TSKLH Nation.

These steps are a standard milestone in a junior mining company's development timeline. Together, they represent a material reduction in the execution uncertainty surrounding one of North America's largest undeveloped gold-copper deposits. The question is not whether Treaty Creek has advanced, but which uncertainties have been resolved and which remain heading into the planned Summer 2026 preliminary economic assessment (PEA).

Ownership: One Problem Solved, One Remaining

The acquisition of American Creek Resources, which increased Tudor Gold's interest in Treaty Creek to 80%, removed one of the more complex features of the project's governance. A multi-party ownership structure introduces decision-making friction at exactly the stage where pace matters most. The consolidation simplified that structure, but it did not resolve it entirely.

Teuton Resources retains the remaining 20% interest, and Tudor Gold's President and Chief Executive Officer, Joseph Ovsenek, has stated the company's position directly.

"We'd like 100% interest in the project. We are talking with our joint venture partner. We'll see if we can come to an agreement where we're all on the same page and it works for everybody. I'd like to say, let's move from 80% up to 100%, and 'cause that's where I believe the sum of the parts is worth more, quite a bit more, than just the parts."

Whether that consolidation occurs before or after the PEA will affect how the project's economics are presented to the market. A 100% interest changes the capital structure and potentially the financing options available. For now, it remains an open item on Tudor Gold's 2026 programme.

Resource Definition: More Resolution, Not Just More Ounces

The January 2026 updated MRE for the Goldstorm Deposit, certified by an independent NI 43-101 technical report, is often framed as a scale story with 24.9 million indicated ounces of gold. That framing understates the most significant aspect, applying higher net smelter return (NSR) cut-offs to isolate higher-grade zones within the broader resource envelope. For a company targeting selective underground mining rather than the full bulk-tonnage resource, this cut-off analysis matters more than the headline ounce figure.

At a US$125 per tonne NSR cut-off, the resource isolates 8.4 million ounces at approximately 2.5 grams per tonne (g/t) gold. At US$175 per tonne, the threshold most relevant to the underground mine plan, it narrows to 5.8 million ounces, comprising 3.4 million indicated and 2.4 million inferred ounces, with grades averaging 2.5–2.8 g/t gold. The estimate, independently certified by Garth Kirkham, P.Geo. and Renee Goold, P.Eng., satisfies the NI 43-101 disclosure requirement necessary before a formal economic study can proceed, a procedural but essential milestone. What the updated MRE does not resolve is the SC-1 Complex which remains undefined at the resource level.

Ovsenek's commentary reflects how the company is sequencing development:

"And we may find that we've got a mine that we can mine at 8 to 10 grams a ton for the first year, 10, who knows, maybe 10 years. Get that up and running. Get all the infrastructure paid for, get the capital cost all completely taken care of, and then look to bring in that three gram material."

That sequencing logic, SC-1 first, then the broader 2 to 3 g/t underground resource, then eventually the full bulk-tonnage inventory, is contingent on underground drilling that has not yet been completed. Without underground drilling, SC-1 remains a conceptual upside.

Metallurgy: Preliminary Results Are Constructive, Final Programme Pending

Metallurgical uncertainty is often the least-discussed and most consequential variable at the pre-PEA stage. Recovery rates determine the revenue side of any economic model, and for a deposit with two mineralogically distinct ore domains, the gold-copper Lower CS600 zone and the high-grade gold SC-1 Complex.

Tudor Gold has published preliminary results for both. For the Lower CS600 zone, conventional flotation returned copper recoveries of 85.8%, silver recoveries of 58.1%, and gold recoveries of 80.2% through a combination of flotation and leaching of flotation tails, producing a concentrate grading 30.3% copper, 36.5 g/t gold, and 99.8 g/t silver. For the SC-1 zone, flotation returned gold recoveries of 85.1%, with a concentrate grading 33.6 g/t gold.

Both results indicate amenability to standard flotation processing, suggesting conventional extraction methods may be sufficient to produce marketable copper and gold concentrates. That finding matters because more complex processing routes carry materially higher capital and operating costs, which would flow directly into the PEA's economic assumptions. The final metallurgical programme was targeted for completion by end of March 2026 with a potential extension into April.

Ovsenek described the timeline and its connection to the PEA:

"The target is to have the metallurgy wrapped up by the end of March 2026. It may drag a bit into April, but as of now it looks like we're on schedule for the end of March. And that will look at metallurgy for each of the upper, central, and lower zones so that we can take that metallurgy, put it with a mine plan."

Until those final results are published, the preliminary figures carry a caveat. The results are expected before the PEA is complete.

The Underground Ramp: A Permit That Changes the Drilling Programme

The underground exploration ramp, currently in the permitting process, is a key near-term operational catalyst that has received limited attention relative to its significance. Surface drilling in the Golden Triangle is constrained to approximately four to five months per year due to seasonal weather conditions. Underground drilling is year-round. For a company that needs to infill-drill the SC-1 Complex at sufficient density to support a resource classification, and that needs to define the geometry of higher-grade zones for a mine plan, the ramp permit is a practical prerequisite. Without it, SC-1 remains a conceptual input to any mine plan.

The permit remains under regulatory review. Its approval timeline is subject to the standard BC Ministry process. Tudor Gold's signed agreements with the Tahltan Nation and TSKLH Nation provide a documented social licence foundation that reduces, but does not eliminate, the risk of consultation-related delays.

At the provincial level, the BC government has made explicit public statements supporting Golden Triangle mining development, with the Minister of Mines stating in May 2025 that the province is positioning northwest British Columbia as a key economic driver. That provides supportive context for the permitting process but is not a substitute for the regulatory approval itself.

Capital: A Deliberate Reframing of the Development Scale

The most visible strategic shift Tudor Gold has made in the past twelve months is the explicit pivot away from bulk-tonnage development toward a smaller, higher-grade underground starter mine. A full bulk-tonnage operation processing the entire 24.9 million indicated ounce resource would require 150,000 to 175,000 tonnes per day of material movement and an estimated capital expenditure (capex) of approximately C$10 billion. The targeted underground operation, processing 8,000 to 10,000 tonnes per day of material grading above 2.5 to 3 g/t gold, carries an estimated capex of C$1 billion to C$1.5 billion.

That capex range is significant for a junior mining company. Construction financing at that scale will require capital markets access, project debt, or some combination of the two, and those options depend on the PEA delivering financeable economics. Recent financing rounds provide the working capital to reach the PEA. The construction financing question will be addressed post-PEA.

What to Watch Next

The Summer 2026 PEA is the next definitive event in Treaty Creek's development timeline. It will be the first document to translate the resource and metallurgical data into an economic framework: capital costs, operating costs, net present value, internal rate of return, and a production profile for the underground starter mine scenario. That framework will set the parameters for how the project is valued relative to its development stage and define what the next phase of technical and financing work needs to accomplish.

Before PEA publication, several milestones remain. Final metallurgical results will confirm or refine processing assumptions, the underground ramp permit decision will determine if SC-1 infill drilling can accelerate, and progress on Teuton Resources’ ownership will indicate whether the project reaches the PEA at 80% or closer to 100%. Additionally, the 2026 drill programme across CBS, Eureka, and PerfectStorm aims to add approximately 5 million ounces to the resource. Individually, these milestones affect execution and timeline; together, they will determine whether the PEA provides sufficient certainty for a development decision or whether key dependencies such as metallurgy, SC-1, and ramp access, extend the path forward.

FAQs (AI-Generated)

Before the acquisition of American Creek Resources, Treaty Creek was held under a multi-party ownership structure. A multi-party arrangement adds complexity to project governance. Consolidating to 80% simplifies that structure ahead of key economic studies. The remaining 20%, held by Teuton Resources, is still under active discussion.

The 2026 mineral resource estimate applied higher NSR cut-off values of US$125 and US$175 per tonne to isolate solid, higher-grade shapes within the broader resource envelope. For a company targeting selective, higher-grade underground mining rather than bulk-tonnage open-pit mining, this analysis matters more than the total ounce count. At US$175 per tonne, the resource narrows to 5.8 million ounces at grades averaging between 2.5 and 2.8 g/t gold, directly informing the PEA mine design.

Preliminary flotation test work returned gold recoveries of up to 85.1% for the SC-1 high-grade zone and 80.2% for the Lower CS600 gold-copper zone, with copper recoveries of 85.8%. Both geological zones responded to conventional flotation, indicating standard extraction methods may be sufficient to produce marketable concentrates. The final programme, targeting all three deposit zones, was due by end of March 2026 and will set the definitive processing assumptions for the PEA.

Surface drilling in the Golden Triangle is limited to approximately four to five months per year due to seasonal weather. Underground drilling is year-round, allowing consistent infill drilling regardless of conditions. For Tudor Gold to define the SC-1 Complex at the density needed to support a resource classification and mine plan, underground access is a critical operational requirement. The permit remains under regulatory review.

Mining the full 24.9 million indicated ounce resource would require 150,000 to 175,000 tonnes per day of material movement and an estimated capital expenditure of approximately C$10 billion, a scale requiring a major joint venture partner. The targeted underground starter mine, processing 8,000 to 10,000 tonnes per day of material grading above 2.5 to 3 g/t gold, carries an estimated capital expenditure of C$1billion to C$1.5 billion.

Analyst's Notes

Subscribe to Our Channel

%20(2)%20(2).jpg)

Stay Informed