Underinvestment & a 25-Year Build Gap Create a Security-of-Supply Premium for New Salt Supply

A 25-year gap in new North American salt supply, stable demand, and import reliance are creating a security-of-supply premium for new projects.

- North America has not added a new greenfield salt mine in roughly 25 years, limiting supply growth while demand remains anchored by de-icing and chemical feedstock consumption.

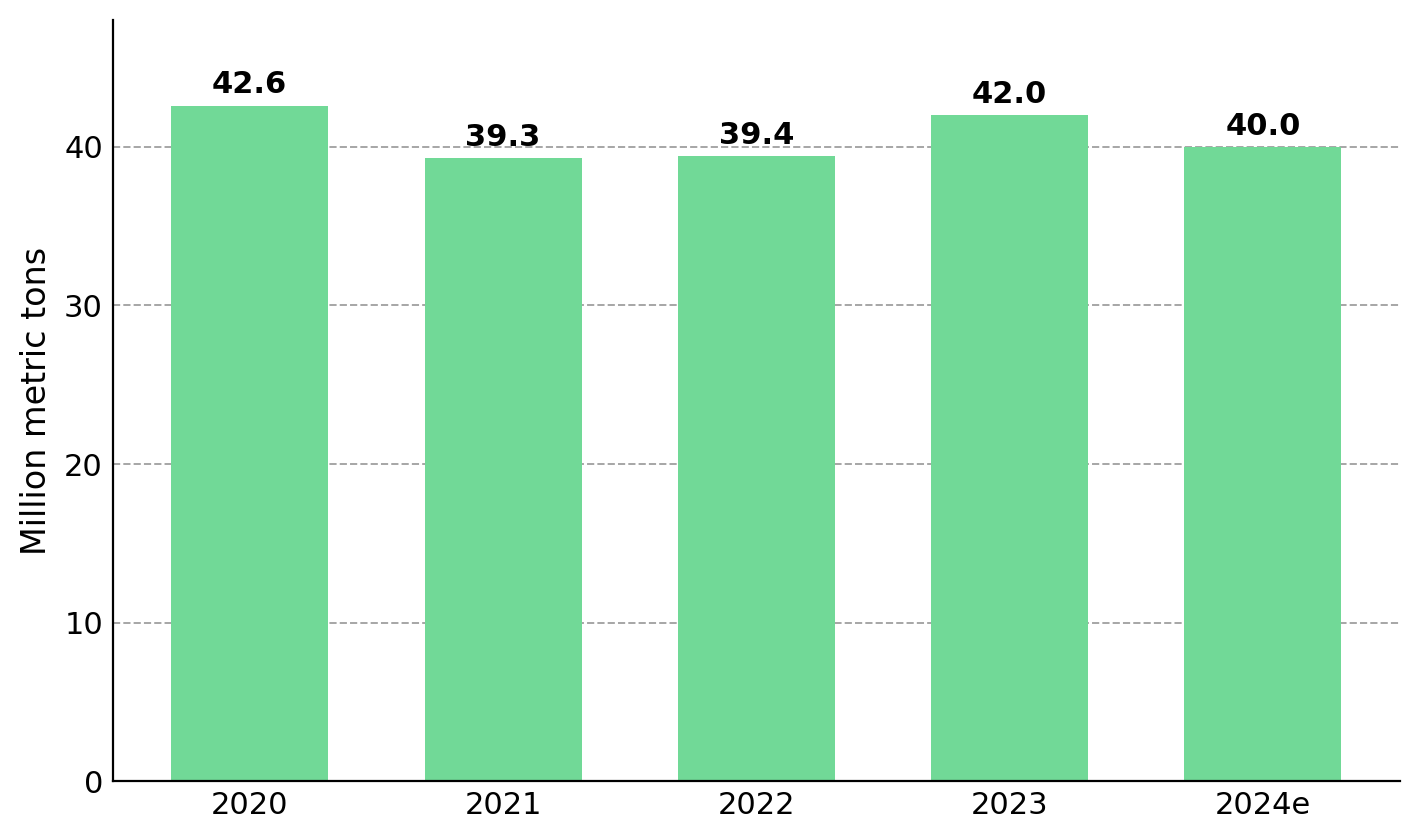

- Producer capital discipline has kept US salt output near 40 million tons annually since 2020, reducing the likelihood of a rapid supply response despite stable demand.

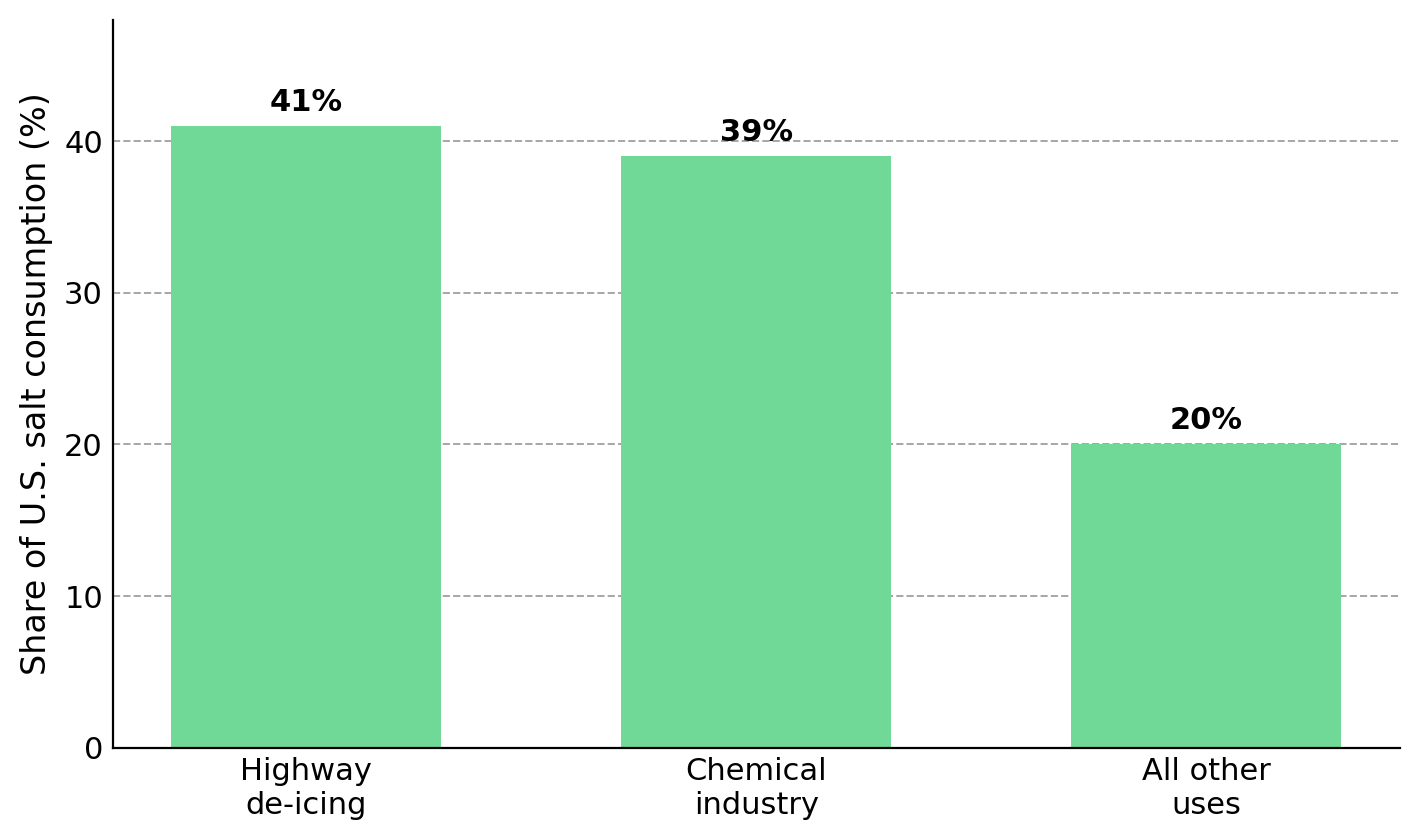

- Government-driven de-icing demand accounted for about 41% of US salt consumption in 2024, supporting recurring demand through economic cycles.

- Imports supplied roughly one-quarter of US salt consumption in 2024, exposing buyers to freight, fuel, currency, and logistics risks that increase the value of domestic supply.

- Supply constraints, import dependence, and stable demand support pricing power and a security-of-supply premium for projects capable of adding new domestic production.

Supply Scarcity Creates a Security-of-Supply Premium in North American Salt

Salt's market structure supports pricing power because demand remains stable while new supply additions have been limited for decades, reducing competitive pressure on incumbents. Demand is inelastic because de-icing and chemical feedstock are non-discretionary uses, meaning consumption changes little when prices rise; these end markets accounted for roughly 80% of US salt consumption in 2024, with highway de-icing representing about 41% and the chemical industry about 39%.

Pricing is regional and determined largely through annual contracts rather than a global spot benchmark, giving producers with low freight costs and proximity to customers greater pricing leverage and margin protection. Because salt pricing depends more on contract position, logistics advantages, and operating costs than ore quality, investors should place greater weight on cash-flow durability, contract exposure, and transportation economics when valuing producers.

No greenfield salt mine has been built in North America for roughly 25 years, limiting new supply growth and increasing the value of projects that can add domestic production. US output is also geographically concentrated, with seven states accounting for about 95% of domestic salt production in 2024, leaving some consuming regions dependent on long-distance transportation and creating an advantage for new supply located closer to end markets.

Government De-Icing Demand Supports Salt Pricing Power

De-icing salt demand remains stable because municipal, state, and provincial governments must maintain safe road conditions regardless of economic activity. Highway de-icing accounted for about 41% of US salt consumption in 2024, making it the industry's largest end market. Because demand remains stable even during economic slowdowns, limited supply can translate more directly into pricing power for producers.

Nolan Peterson, Chief Executive Officer of Atlas Salt, explains how legal de-icing obligations create recurring government demand for salt:

"The primary customer for our salt is cities and governments. They are, in many cases, legally obligated to purchase salt to de-ice roads for liability reasons."

Producer Capital Discipline & Capacity Constraints Limit New Salt Supply

Producer capital discipline is limiting new salt supply by directing capital toward cash generation and balance-sheet strength rather than capacity expansion. Mining companies are prioritizing cash generation and balance-sheet strength over production growth, reducing investment in new salt capacity. US production has remained within a narrow range of roughly 39 to 43 million tons annually since 2020 (42.6, 39.3, 39.4, 42.0, and an estimated 40.0 million tons from 2020 through 2024), showing little production growth despite stable demand. By limiting capacity growth despite stable demand, incumbents reduce competitive pressure and support pricing power across the market.

Recent earnings disclosures suggest that this capital-discipline strategy remains in place even when de-icing demand softens. Rather than increasing production to offset weaker volumes, producers are focusing on margin protection, inventory management, and operating cash flow, reducing pressure on prices and supporting industry profitability.

When the largest producers prioritize margins over market share and guide volumes lower, they reduce competitive pressure and support pricing power across the market, increasing the value of new projects capable of adding domestic supply.

Capacity Constraints and Capital Discipline Limit Supply Growth

Supply growth is limited by output ceilings at legacy mines, rising distribution costs, and producer preference for margin preservation over capacity expansion. Together, these constraints reduce the likelihood of meaningful new supply entering the market, allowing stable demand to support pricing power for existing producers and new projects.

Import Dependence Creates a Security-of-Supply Premium for Domestic Producers

North America relies on imported salt to meet a meaningful portion of demand, exposing buyers to ocean freight costs, currency movements, and supply-chain disruptions. US imports for consumption were an estimated 14 million tons in 2024, and net imports have supplied between 24% and 30% of apparent consumption each year since 2020. Imported supply is concentrated among Canada, Chile, Mexico, and Egypt, which together accounted for roughly 78% of US imports over 2020-23, increasing exposure to transportation and currency costs. During severe winters, tighter imported supply can increase the value of domestic production, particularly for producers located close to major end markets.

Peterson explains how import dependence can increase domestic salt pricing during periods of supply stress:

"There's actually only upside potential in cold winters when there's fuel shortages… we're seeing now that it puts pressure on the price that drives the price up because a lot of our salt is imported."

During periods of tight supply, proximity and security of supply command a premium, supporting pricing power for domestic developers.

Security-of-Supply Premiums Support Long-Term Salt Contracts

Supply scarcity and import dependence create a security-of-supply premium for domestic salt. Buyers signing multi-year contracts and strategic acquirers will pay for certainty of delivery. For development-stage suppliers, that premium can translate into contracted revenue if the project reaches production.

Long-Life Cash Flows Change How Salt Assets Are Valued

Salt projects are valued differently from most mining projects because long reserve lives and stable demand support cash-flow-based valuation. Development-stage mining equities are commonly valued using P/NAV, which compares market value with project value. Development-stage projects typically trade below NAV because financing and execution risks remain unresolved before construction. Project value is typically assessed using NPV and IRR estimates from feasibility studies.

Salt lacks the metallurgical and grade variability found in gold and copper, placing greater importance on logistics, contract exposure, operating costs, and cash-flow generation when valuing projects. Pricing instead varies by product form: in 2024, average unit values ranged from about $10 per metric ton for salt in brine and $56 for rock salt to roughly $140 for solar salt and $230 for vacuum and open-pan salt. Long reserve lives support stable cash flows, making EBITDA multiples and free-cash-flow yield more relevant valuation tools than in shorter-life mining projects. For developers, the Lassonde Curve suggests valuations can increase as financing, permitting, and construction milestones reduce project risk and improve confidence in future cash flows.

Project De-Risking Drives Development-Stage Re-Ratings

The gap between development-stage valuations and NAV typically narrows as projects achieve key milestones. Key milestones include securing financing, advancing permitting, obtaining environmental approvals, and making a construction decision. Financing and execution risk remain the main uncertainties, making any re-rating contingent on project progress

Downstream Consolidation Increases the Value of Salt-Linked Supply Chains

The chemical industry accounted for about 39% of US salt sales in 2024, making it the sector's second-largest end market. Chlorine and caustic soda manufacturers are the primary consumers, with salt in brine representing about 91% of chemical feedstock. Berkshire Hathaway's agreement to acquire OxyChem for roughly US$9.7 billion highlights continued investor interest in chlor-alkali businesses that rely on salt as a core input. The transaction reinforces the importance of chemical demand as a long-term source of salt consumption.

Large acquirers are increasing their exposure to salt-linked chemical assets rather than exiting the sector. These buyers favor long-term feedstock agreements, supporting term pricing and demand visibility.

Consolidation Supports Long-Term Contracting & Revenue Visibility

Concentrated downstream demand can increase contracting opportunities for new domestic supply because larger buyers value security of supply and can support multi-year agreements. For developers, those contracts can support the revenue commitments lenders require before financing construction.

Supply Constraints & Import Dependence Support Domestic Salt Supply

The salt market combines limited supply growth with demand anchored by de-icing and chemical feedstock consumption. A roughly 25-year gap in new North American salt capacity, producer capital discipline, government-driven demand, and import dependence continue to constrain available supply. With US apparent consumption at roughly 51 million tons in 2024 against domestic output of about 40 million tons, imports remain necessary to balance the market. Recent acquisitions also highlight continued investor interest in chlor-alkali businesses that rely on salt as a core feedstock, reinforcing demand visibility for one of the industry's largest end markets.

Limited supply growth, stable demand, and import dependence are increasing the value of secure domestic salt supply. The greatest benefit goes to projects capable of adding new domestic supply.

The Investment Thesis for Salt

- A roughly 25-year gap in new North American salt capacity has constrained supply growth and increased the value of projects capable of adding domestic production.

- Producer capital discipline has kept US salt output broadly flat since 2020, limiting competitive supply growth despite stable demand conditions.

- Government-driven de-icing demand and chemical feedstock consumption accounted for roughly 80% of US salt demand in 2024, supporting long-term consumption visibility.

- Imports remain necessary to balance the market, supplying roughly 24% of US apparent consumption in 2024 and increasing the strategic value of reliable domestic supply.

- Regional pricing, annual contract structures, and transportation costs create competitive advantages for producers located close to major end markets.

- Long reserve lives and recurring demand support cash-flow durability, making EBITDA, free-cash-flow yield, and contract exposure more relevant valuation metrics than grade-based measures.

- Development-stage projects can re-rate as financing, permitting, and construction milestones reduce project risk, although financing and execution remain the primary risks to realizing value.

The salt investment case rests on limited supply growth meeting demand that remains anchored by de-icing and chemical feedstock consumption. A roughly 25-year gap in new North American capacity, producer capital discipline, import dependence, and stable demand from government and chemical end markets support pricing power and increase the value of new domestic supply. Investors should balance this supply-driven opportunity against financing and execution risk, focus on cash-flow durability and logistics advantages, and monitor whether future capacity additions begin to outpace demand growth.

TL;DR

North America's salt market faces limited supply growth after roughly 25 years without a new greenfield mine. Producer capital discipline has kept US output near 40 million tons annually since 2020, while government-driven de-icing demand accounted for about 41% of salt consumption in 2024. Import reliance, at roughly a quarter of US consumption, increases exposure to freight, fuel, and logistics disruptions, making domestic supply more valuable during periods of market stress. Together, these factors support pricing power and increase the value of projects capable of adding reliable domestic supply. For investors, the opportunity lies in development-stage salt assets that can reach production on time and within budget, while financing and construction remain the primary risks to realizing that value.

FAQs (AI-generated)

Analyst's Notes

Subscribe to Our Channel

.jpg)

.jpg)

.jpg)

Stay Informed