US Critical Minerals Policy Acceleration & Battery Metals Re-Rating: Why Domestic Supply Chains Are Reshaping Project Economics

DOE policy is reshaping battery metals investing, shifting valuations from price cycles to ESG, jurisdiction, and cost advantages in strategic supply chains.

- The US Department of Energy's $500 million funding initiative represents a structural commitment to domestic battery supply chain security, prioritizing lithium, nickel, cobalt, and copper as strategic inputs.

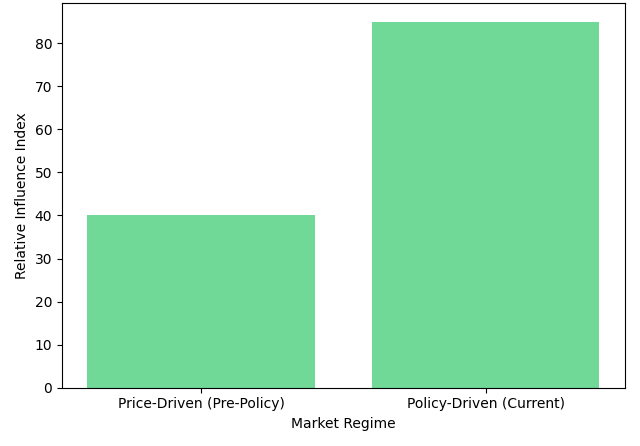

- Policy-driven demand is decoupling battery metals from purely cyclical price behavior, anchoring long-term project economics through government-backed capital flows.

- Projects in Tier-1 jurisdictions, specifically the United States and Canada, are commanding valuation premiums as permitting visibility and geopolitical alignment become discrete inputs to discount rate assumptions.

- Institutional capital is rotating toward low-cost, scalable sulphide deposits and integrated processing assets capable of meeting localization and environmental, social, and governance requirements.

- Developers demonstrate how project economics measured by net present value, internal rate of return, and all-in sustaining cost are being re-rated by policy tailwinds independent of spot commodity prices.

Policy as the Primary Driver of Demand

The global battery metals market is shifting from a demand-driven cycle anchored to EV adoption toward a policy-driven supply chain realignment, where Western governments act as capital allocators rather than passive consumers. The US Department of Energy’s $500 million funding initiative marks a clear inflection point, targeting domestic processing, recycling, and manufacturing across lithium, nickel, cobalt, and copper.

Unlike prior cycles driven by price signals alone, the current environment reflects state-backed capital allocation aimed at reducing geopolitical concentration risk. The DOE’s goal of cutting foreign dependence by up to 15% within four years signals a programmatic procurement shift, aligned with broader Western strategies to counter supply dominance in China (graphite processing) and Indonesia (Class 1 nickel refining).

For capital markets, this introduces three structural re-rating mechanisms. First, capex-intensive projects are becoming financeable earlier through non-dilutive funding. Second, jurisdictional risk is now a quantified input in NPV models, not just a qualitative discount. Third, strategic metals are increasingly treated as policy assets, compressing required returns and expanding the investable universe for ESG-aligned capital.

From Exploration Risk to Infrastructure

The DOE framework’s eligibility criteria are reshaping which mining projects attract institutional-grade financing. Projects must demonstrate commercial or demonstration-scale capacity, integration into battery value chains, and support for processing, recycling, or downstream conversion. This effectively filters out early-stage exploration assets and redirects capital toward integrated platforms delivering battery-grade material from mine to refined product.

Energy Fuels, a uranium producer expanding and diversifying its operations to become a major rare earth element (REE) processor while maintaining its position as the largest US producer of uranium, is advancing a bankable feasibility framework for processing infrastructure at its White Mesa Mill in Utah. Existing licensing and infrastructure provide a cost advantage over greenfield projects, lowering capital requirements and accelerating permitting, positioning the company within the policy-eligible tier due to its near-term production capability rather than speculative resource exposure.

Policy Alignment as a Valuation Catalyst

Canada Nickel is advancing its Crawford nickel-cobalt sulphide project in Timmins, Ontario, as more than a mine, positioning it as the anchor of a downstream industrial cluster with integrated carbon capture and processing. This structure aligns with localization and ESG requirements under US and Canadian funding frameworks, with 2025 estimates ranking it among North America’s largest sulphide nickel deposits by contained metal.

On the strategic relevance of government endorsement to project financing and valuation, Canada Nickel's Chief Executive Officer, Mark Selby, has been direct about the company's positioning relative to peers:

"We’re the only project in Canada with both federal and provincial endorsement, and it’s attracting significant global attention."

Supply Chain Security is Repricing Jurisdictional Risk

The jurisdictional premium, once a qualitative factor in mining valuations, is now a quantified variable embedded in discount rates, financing structures, and offtake terms. The Fraser Institute’s 2025 survey ranks Ontario 2nd globally out of 68 jurisdictions, reflecting strong permitting predictability, regulatory transparency, and infrastructure, all of which lower the cost of capital versus higher-risk regions.

Canada Nickel’s Crawford project captures this premium through access to rail and power infrastructure, inclusion in federal permitting pathways, and alignment with North American supply chain priorities. These factors reduce timeline risk, a key driver of discount rate expansion, and improve access to commercially viable debt financing.

Asset Quality as a Counterbalance to Jurisdictional Risk

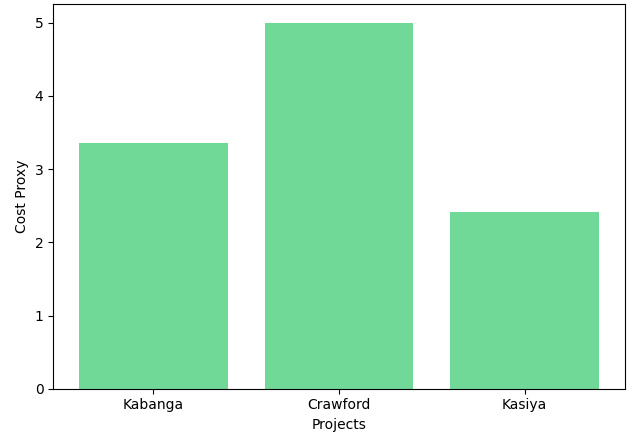

Lifezone Metals’ Kabanga project in Tanzania shows how assets outside Tier-1 jurisdictions can remain competitive through superior asset quality. With a ~2.09% nickel grade, it ranks in the first quartile globally, while an estimated AISC of ~$3.36/lb and ~23% IRR provide sufficient margin to absorb jurisdictional risk. Development Finance Institution support further mitigates sovereign risk, supporting a targeted ~60/40 debt-to-equity structure.

Ingo Hofmaier, CFO of Lifezone Metals, has articulated the connection between Kabanga's asset quality and its strategic positioning within critical minerals supply chains clearly:

"There’s a strong recognition that this is a strategic asset, and that nickel is a critical material for US supply chain security."

Battery Metals Demand is Broadening Beyond Electric Vehicles

While electric vehicles remain the primary demand driver for battery metals, the DOE framework highlights a broadening set of end uses that reduces cyclicality. Grid-scale storage, data center backup systems, and defense electronics are increasingly drawing from the same supply pool, distributing demand across sectors and supporting more stable pricing.

Global battery capacity continues to expand, with lithium-ion battery demand reaching approximately 1.59TWh in 2025, up 29% year-on-year, driven increasingly by non-automotive applications. Energy storage systems (BESS) are now the fastest-growing segment, with demand rising 51% in 2025, significantly outpacing EV growth and increasing its share of total battery demand, while EV share declined to 75% from 79% in 2023. This diversification extends the pricing window for offtake agreements and lowers commodity price risk in project financing

Multi-Commodity Exposure Enhancing Demand Resilience

Sovereign Metals’ Kasiya project in Malawi provides exposure to two commodities with diversified demand. It hosts the largest known rutile deposit, a key feedstock for titanium dioxide used in industrial, aerospace, and defense applications, alongside the second-largest natural graphite deposit by contained material, linked to battery anodes. This dual-commodity structure supports revenue diversification and pricing resilience across demand cycles.

Sovereign Metals' Chief Executive Officer, Ben Stoikovich, has emphasized both the scale and the cost advantages that define Kasiya's competitive position:

"It is a massive deposit, the largest rutile deposit ever discovered, and it ranks as the second-largest natural graphite deposit."

Cost Curve Positioning is Becoming the Primary Differentiator

In a policy-supported market, not all projects benefit equally from macro tailwinds. Institutional and development capital is concentrating on first-quartile cost assets, where financing terms are more favorable and margins remain resilient across commodity price cycles. Key variables include all-in sustaining cost, capital intensity, and metallurgical complexity, which determine access to non-dilutive funding versus reliance on equity markets.

Lifezone Metals targets an AISC of ~$3.36/lb nickel at Kabanga, supported by high-grade feed and hydrometallurgical processing that lowers energy and reagent costs. Canada Nickel’s Crawford project leverages a bulk tonnage model with low strip ratios and carbon sequestration potential, while Sovereign Metals’ Kasiya deposit benefits from a free-dig saprolite resource, targeting graphite costs of ~$241/t at the low end of the global curve.

Infrastructure Leverage and Processing Scale as Cost Advantages

Energy Fuels' competitive cost position in rare earth processing derives from its existing licensed infrastructure at the White Mesa Mill, which eliminates the need for greenfield facility construction. The company is scaling a phased, high-throughput processing model, with current capacity of ~10,000 tpa of monazite and expansion plans to ~60,000 tpa, targeting production of both light and heavy rare earth oxides from a single hub. This integrated, multi-commodity platform, spanning uranium, rare earths, vanadium, titanium, and zirconium, distributes fixed infrastructure costs across multiple revenue streams and reduces per-unit processing costs relative to single-commodity processors.

On the strategic imperative of full value chain integration as a cost and competitive advantage, Energy Fuels' Chief Executive Officer, Mark Chalmers, has quantified the company's ambition:

“We’re pushing a billion dollars of deployable capital. People are seeing that two billion is achievable to build out a world-significant, low-cost critical mineral company.”

Permitting, ESG, & Carbon Intensity Are Now Core Valuation Inputs

The integration of environmental, social, and governance considerations into mining project valuations has moved beyond regulatory compliance into direct economic relevance. Projects demonstrating low carbon intensity, responsible sourcing protocols, and community engagement frameworks are increasingly eligible for government incentives, strategic partnerships, and premium offtake agreements that carry price floors above spot market levels. This creates a measurable valuation differential between ESG-compliant and non-compliant assets at equivalent resource and cost profiles.

Canada Nickel's carbon sequestration capability, which the company's technical studies estimate at approximately 1.5 million tonnes of carbon dioxide annually through the natural carbonation of magnesium silicate tailings, positions Crawford as a net-negative carbon project across its mine life. This characteristic aligns the project directly with Canada's federal clean technology investment incentives and creates eligibility for additional non-dilutive capital beyond the standard mining funding framework. The company's current market valuation of approximately 15% of net asset value, relative to the sector norm of 50% for projects at comparable development stages, implies that the market has not yet fully priced in either the policy tailwinds or the carbon sequestration premium.

ESG compliance also introduces timeline risk that must be incorporated into project models. Sovereign Metals' Kasiya project requires completion of an Environmental and Social Impact Assessment and regulatory sequencing through Malawi's Environmental Affairs Department before it can progress to a bankable feasibility study. This regulatory pathway represents a defined, manageable risk rather than an open-ended permitting uncertainty, but it does directly affect the timeline to financial investment decision and the draw schedule for development financing.

The Investment Thesis for Battery Metals

- Policy-backed demand floors established through the DOE's $500 million funding initiative and the US Inflation Reduction Act provide structural support for long-term pricing of lithium, nickel, cobalt, and rare earth elements, reducing the cyclicality premium historically embedded in battery metals project discount rates.

- North American projects, particularly those with federal and provincial endorsements such as Canada Nickel's Crawford project, are commanding valuation premiums that reduce financing costs and accelerate timelines to financial investment decisions.

- First-quartile cost assets including Lifezone Metals' Kabanga deposit at approximately $3.36 per pound of nickel all-in sustaining cost and Sovereign Metals' Kasiya project targeting $241 per tonne graphite production cost are positioned to maintain positive margins across a wider range of commodity price scenarios, improving financing viability.

- The broadening of battery metals demand beyond electric vehicles into grid-scale energy storage, defense electronics, and data infrastructure distributes demand risk across multiple sectors with independent demand cycles, supporting long-term offtake agreement pricing.

- Non-dilutive capital instruments including government grants, tax credits, and development finance institution debt are compressing equity financing requirements for qualifying projects, reducing dilution risk for existing shareholders at critical development inflection points.

- Carbon intensity and ESG compliance are generating direct economic value through eligibility for clean technology incentives, as demonstrated by Canada Nickel's 1.5 million tonne annual carbon sequestration capability, which creates access to additional capital pools unavailable to conventional mining projects.

- Vertically integrated processing platforms such as Energy Fuels' White Mesa Mill model distribute fixed infrastructure costs across multiple critical mineral revenue streams, targeting deployable capital of up to $2 billion to establish a globally significant low-cost processing hub.

The battery metals market is no longer defined solely by supply and demand fundamentals operating through commodity price signals. Government policy has become the marginal buyer and capital allocator, functioning through direct funding mechanisms, localization requirements, and strategic procurement frameworks that create a valuation hierarchy among development-stage projects that did not exist in prior commodity cycles.

The investment implication is precise: projects that combine first-quartile cost positioning with jurisdictional alignment and ESG compliance are being re-rated based on strategic relevance rather than commodity price exposure alone. Canada Nickel, Lifezone Metals, Energy Fuels, and Sovereign Metals each represent distinct expressions of this framework, operating across different jurisdictions and commodity sets but sharing the characteristic of being structurally positioned within the policy-eligible tier of the global critical minerals supply chain.

The key determination is not which commodity will outperform over the next price cycle, but which projects will attract non-dilutive capital, achieve financial investment decisions within definable timeframes, and deliver returns that are anchored by policy support rather than dependent on commodity price recovery alone. That distinction is reshaping how mining projects are financed, developed, and valued, and it represents a fundamental change in the risk-return calculus of battery metals investing.

TL;DR

Government policy, led by the US Department of Energy’s $500M initiative, is fundamentally reshaping battery metals investing by shifting valuation drivers away from commodity prices toward policy alignment, jurisdiction, ESG compliance, and cost competitiveness. Capital is increasingly flowing to advanced, integrated projects in Tier-1 regions like the US and Canada, where permitting certainty and government backing reduce risk and financing costs, while exceptional low-cost assets can still compete globally. As demand expands beyond EVs into energy storage and defense, and as non-dilutive funding becomes more available, projects that combine scalability, low operating costs, and strategic relevance to Western supply chains are being re-rated and prioritized by institutional investors.

FAQs (AI generated)

Western governments have shifted from passive consumers of battery metals to active capital allocators, using direct funding mechanisms, localization requirements, and strategic procurement frameworks to secure domestic supply chains. The DOE's $500 million initiative, combined with the US Inflation Reduction Act, creates demand floors that are structurally independent of EV adoption cycles. This means projects in eligible jurisdictions can achieve financing and reach financial investment decisions even in soft commodity price environments, because government-backed capital compresses required returns and reduces reliance on equity markets, a fundamental change from prior commodity cycles.

To qualify for government-backed funding, projects must demonstrate commercial or near-commercial scale, integration into battery value chains, and the ability to deliver battery-grade material from mine through to refined products. Early-stage exploration assets are effectively filtered out. Projects benefit most when they combine federal and provincial endorsements, existing permitting pathways, and proximity to infrastructure. Canada Nickel's Crawford project is a prime example, it holds both federal and provincial endorsement in Ontario, ranks among North America's largest sulphide nickel deposits, and is structured as an integrated industrial cluster rather than a standalone mine.

ESG is no longer just a reputational consideration, it is a direct economic input. Projects with low carbon intensity, responsible sourcing protocols, and community engagement frameworks become eligible for government clean technology incentives, premium offtake agreements with price floors above spot, and additional non-dilutive capital pools unavailable to conventional mining assets. Canada Nickel's Crawford project illustrates this most concretely: its natural carbon sequestration capability of approximately 1.5 million tonnes of CO₂ annually positions it as a net-negative carbon operation, unlocking federal clean technology investment incentives and creating a measurable valuation premium relative to peers at comparable development stages.

Yes, but the pathway is narrower and depends almost entirely on asset quality and development finance institution support. Lifezone Metals' Kabanga project in Tanzania demonstrates this: despite operating outside a Tier-1 jurisdiction, its approximately 2.09% nickel grade places it in the first quartile globally, and its estimated all-in sustaining cost of roughly $3.36 per pound provides sufficient margin to absorb the higher jurisdictional risk premium. DFI backing further mitigates sovereign risk and supports a targeted 60/40 debt-to-equity financing structure. The key principle is that exceptional asset quality, paired with institutional risk mitigation, can substitute, partially, for jurisdictional safety.

Battery metals demand has broadened well beyond electric vehicles into grid-scale energy storage, data center backup systems, and defense electronics, sectors with independent demand cycles that reduce overall commodity price volatility. Global battery capacity surpassed one terawatt-hour annually in 2023, with energy storage now representing a growing share of lithium demand that is entirely separate from automotive trends. This diversification extends the viable pricing window for long-term offtake agreements, lowers commodity price risk in project financing models, and supports more stable revenue projections, all of which improve a project's ability to attract debt financing on favorable terms.

Analyst's Notes

Subscribe to Our Channel

Stay Informed