US Industrial Policy for Rare Earths & Repricing of NdPr/HREE Midstream Cash Flows: Why Independent US Hubs Can Re-rate Returns

US industrial policy rewires REE midstream economics through DoD/DOE funding & price floors, creating investable cash flows for Western processors.

- A coordinated US push, via DoD/DPA, DOE, tax credits, grants, and potential price-support mechanisms, is rewiring the economics of REE separation (NdPr, Dy, Tb), targeting mine-to-magnet sovereignty and lowering project WACC.

- China’s export controls and technology restrictions elevate basis risk for ex-China supply; investors should expect supply-security premiums and differentiated multiples for validated Western midstream capacity.

- Winners will be determined by execution bottlenecks, specifically feedstock certainty, customer qualification (purity/spec), permitting windows, and ESG/community frameworks, which govern the ability to scale to cash-generating capacity.

- With a permitted hydromet hub at White Mesa Mill, commercial-scale NdPr production, and HREE (Dy/Tb) pilot separation, Energy Fuels is positioned to translate policy support into bankable, phased expansions.

- Investors should track policy disbursements, Phase-2 engineering and procurement, qualification milestones, and offtake architecture, because capacity that clears these gates is likely to command durable valuation premiums in a fragmented, region-aligned supply chain.

Policy Architecture Is Changing Midstream Economics

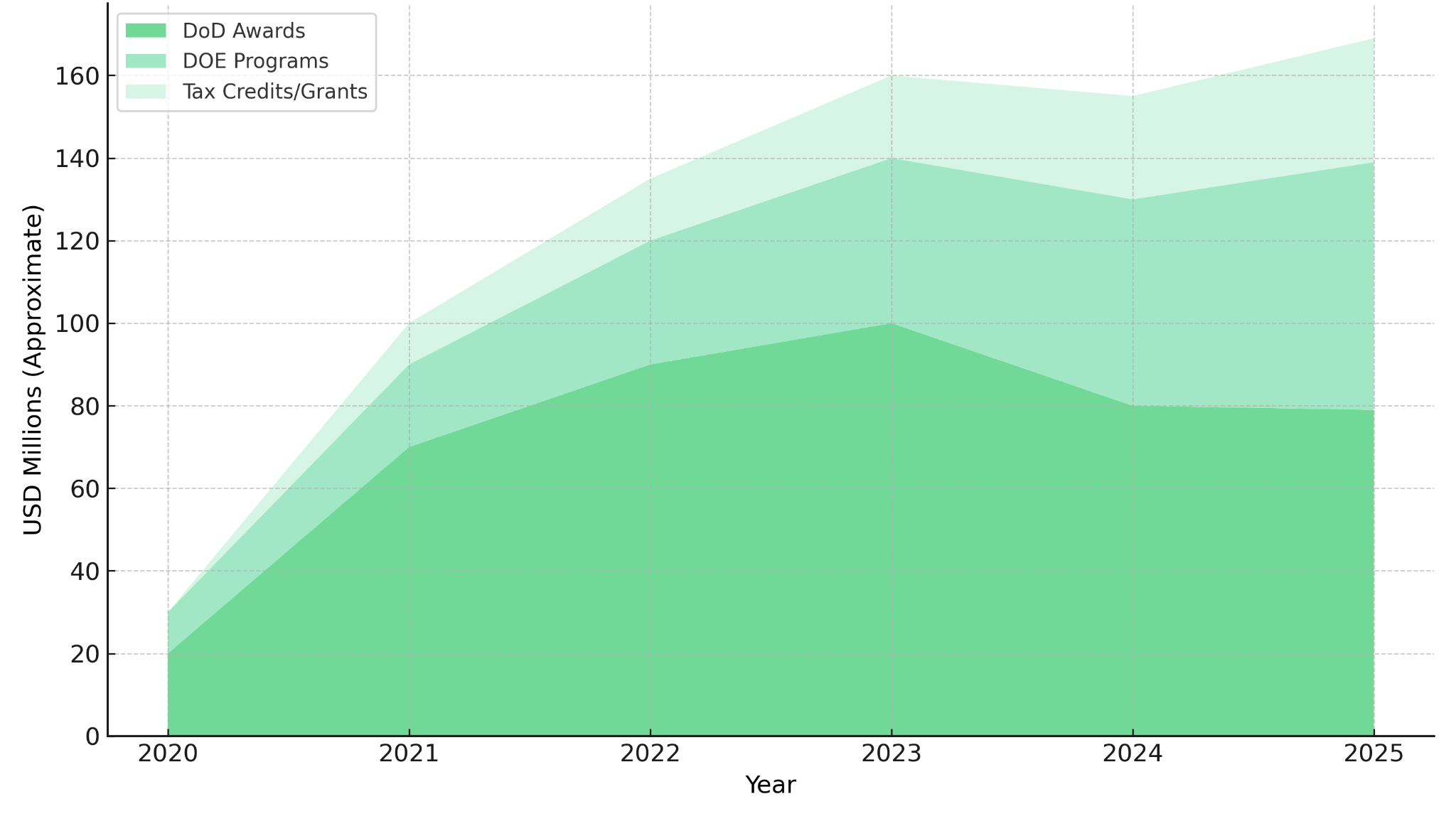

The US is building a public–private capital stack to close the rare earth element midstream gap through Department of Defense/Defense Production Act Title III awards for separation and magnets, Department of Energy programs for critical materials, production credits and tax incentives, grants and loans, and price-support mechanisms for neodymium-praseodymium that stabilize revenues through cycles. These tools deliberately move early-stage midstream projects from binary outcomes to phased, financeable plants, compressing downside scenarios and improving net present value and internal rate of return.

The impact translates into lower weighted average cost of capital, clearer final investment decision timing, and stronger lender appetite when matched with credible engineering, permits, and feedstock. The thesis is not that policy replaces competitiveness; rather, policy bridges commercialization risk until scale, recoveries, and customer qualification converge to sustainable cash flows. The Department of Defense has allocated over $439 million since 2020 to companies such as MP Materials, Lynas USA, and Noveon Magnetics to build light rare earth element and heavy rare earth element separation and processing capabilities.

Energy Fuels exemplifies how policy can accelerate neodymium-praseodymium/dysprosium/terbium capacity with incremental capital expenditure instead of greenfield risk. White Mesa's permitted hydrometallurgical base and Phase-2 expansion plan leverage existing infrastructure to scale separation capabilities. As Chief Executive Officer Mark Chalmers notes:

"We have commercially produced neodymium-praseodymium and we are recovering dysprosium and terbium right now in the heavies. When people see that there are some price floors put in and some investment and some loans and whatnot and recognizing the current price of neodymium-praseodymium is too low for Western producers, the governments are responding because they recognize they have to support these companies that have advanced their strategies."

Geopolitics, Price Formation & the Rise of Supply-Security Premiums

Rare earth element price formation remains China-centric, especially for medium and heavy rare earth elements. Export controls and technology restrictions create basis differentials between China and ex-China markets, with spillovers into inventory behavior, lead times, and contract terms. For Western capacity, the investment case is risk substitution: accept structurally higher operating costs in exchange for policy-backstopped volumes and prices with jurisdictional certainty.

China's April 2025 export restrictions on seven types of medium and heavy rare earth elements caused yttrium prices to spike 598% and samarium to increase 60-fold, exposing acute chokepoints in global supply chains. These disruptions led to production delays for major companies like Ford and Suzuki, underscoring the strategic vulnerability of China-dependent supply chains. The result is a supply-security premium for verified ex-China neodymium-praseodymium/dysprosium/terbium supply that meets original equipment manufacturer specifications.

Energy Fuels' neodymium-praseodymium production and heavy rare earth element pilot separation align with defense and electrification demand, where security of supply carries premium willingness to pay. The company's focus on monazite concentrates as byproduct streams from global heavy mineral sands operations raises total rare earth oxide grade and improves basket value due to higher neodymium-praseodymium and heavy rare earth element proportions.

As Mark Chalmers emphasizes regarding the company’s strategic positioning:

"China has a strangle hold on the heavies right now. The heavies are really used to improve the resistance to heat issues in these permanent electric motors so there's a bigger shortage of heavies than there is the lights which is really the neodymium-praseodymium. It just puts us in a spot where others are not."

The Monazite Route at a Permitted US Hydrometallurgical Hub

Not all flowsheets are equal. Scaling separation requires control of feedstock quality, impurity management, radio-nuclide handling, and selectivity for neodymium-praseodymium and heavy rare earth elements at magnet-grade specifications. Monazite-centric routes offer attractive elemental distributions (neodymium-praseodymium plus dysprosium/terbium) but demand proven hydrometallurgy and regulatory frameworks.

Feedstock Strategy & Basket Value

Energy Fuels pursues monazite concentrates as byproduct streams from global heavy mineral sands operations, raising total rare earth oxide grade and improving basket value due to higher neodymium-praseodymium and heavy rare earth element proportions. Strategically, the company targets a diversified pipeline including projects in Madagascar, Australia, and Brazil to secure throughput and reduce single-source risk. The Toliara Project in Madagascar represents one of the best heavy critical mineral development projects globally, with massive resources of titanium, zirconium, and rare earth elements.

The company's approach leverages the inherent economic advantage of low-cost byproduct monazite concentrates from globally located heavy mineral sands mines, deemed more cost-effective for producing separated rare earth element oxides than relying on primary rare earth production.

From Neodymium-Praseodymium to Heavy Rare Earth Elements (Dysprosium/Terbium)

White Mesa's rare earth element circuit is designed for neodymium-praseodymium separation while piloting heavy rare earth elements (dysprosium/terbium) critical to high-temperature magnets. Key diligence points include solvent extraction stage counts, reagent balance, recovery curves by element, and purity specifications with parts-per-million thresholds. Heavy rare earth element pathways carry higher margin potential but require more complex solvent extraction and tighter impurity control.

The company achieved commercial-scale production of high-purity neodymium-praseodymium in 2024 and demonstrated technical capabilities for six of the seven heavy rare earth oxides subject to Chinese export controls in April 2025.

The Phase-2 plan focuses on throughput increases, higher elemental recoveries, and modular equipment additions, limiting greenfield risk. Engineering for the Phase-2 rare earth element expansion at White Mesa Mill is ongoing, targeting 6,000 tons of neodymium-praseodymium per year at world scale.

Permitting, Environmental, Social & Governance & Community Agreements as Competitive Moats

Western timelines hinge on licenses, air, water, Resource Conservation & Recovery Act, and radiation permits, and community acceptance. Brownfield hydrometallurgical sites with multi-decade operating histories shorten execution risk versus greenfield builds. The social license, codified through community and tribal agreements, local hiring, and environmental monitoring, can be the deciding factor in appeal-heavy jurisdictions.

As a licensed, operating mill, White Mesa reduces permitting uncertainty for monazite processing and tailings and waste management within an established compliance framework. The facility has over 40 years of operational experience and expertise in mineral processing. Energy Fuels maintains significant community programs and tribal initiatives including education, health, environment, and economic advancement as part of a risk-mitigation architecture that investors can underwrite with higher confidence.

The company has established a landmark agreement with the Navajo Nation, including an initial $1 million contribution and ongoing funding representing 1% of annual Mill revenues to a Foundation supporting education, environment, health and wellness, economic advancement, and Native American priorities. Approximately half of its Mill employees are Navajo and Native American, demonstrating deep community integration.

Market Access, Offtake Validation & Revenue Quality

Rare earth element plants are offtake-led. Projects clear final investment decision when customer qualification is credible: magnet producers and original equipment manufacturers certify purity, particle size distribution, and consistency across lots. Contracts may blend take-or-pay, volume ramps, and index and floor formulas, each affecting working capital and credit risk.

Energy Fuels has reported commercial-scale neodymium-praseodymium with validation underway, a key trigger for long-tenor offtakes. Its heavy rare earth element pilot adds optionality in dysprosium and terbium, expanding basket value and addressing defense-relevant demand. The company has formed a collaboration with POSCO International, a major global supplier of electric vehicle and hybrid drivetrains, to build a non-China rare earth element supply chain.

Chief Executive Officer Mark Chalmers describes the qualification process:

"We're currently sending out the neodymium-praseodymium oxide for qualification and we've got a number of parties including POSCO have taken material from us and it's all very appealing to them because we believe that it all meets their specifications."

Capital Formation, Liquidity & the Role of Policy Instruments

Public grants and loans, tax credits, and price-support mechanisms can advance final investment decision, smooth ramp-up cash flows, and compress equity dilution. Investors should examine liquidity, undrawn facilities, and capital expenditure phasing against policy-award timing, ensuring runway through commissioning and customer qualification.

Energy Fuels maintains a strong balance sheet with over $210 million in liquidity as of March 31, 2025, comprising $73.0 million in cash, $89.6 million in marketable securities, $20.4 million in receivables, and $34.5 million in finished product inventory. The company operates with no debt, providing flexibility to either build inventory or sell uranium into strong markets.

A strong balance sheet, diversified cash flows including uranium, vanadium, and heavy mineral sands, and a modular capital expenditure plan create flexibility to build inventory or accelerate throughput as contracts finalize. The policy overlay, where applicable, can raise internal rate of return and reduce payback periods. The Phase-2 rare earth element expansion could attract hundreds of millions of dollars of investment, potentially representing the largest private investment in San Juan County, Utah history.

Valuation, Key Performance Indicators & Monitoring Framework for Rare Earth Element Midstream

Core key performance indicators include throughput and recoveries measuring overall total rare earth oxide, neodymium-praseodymium recovery, and dysprosium/terbium cut performance. Quality acceptance focuses on magnet-grade specification attainment, first-article acceptance, and lot-to-lot variance. Unit economics examine cash cost per kilogram neodymium-praseodymium/dysprosium/terbium oxide, reagent and energy intensity, and waste-handling costs.

Working capital metrics track days inventory and payables/receivables terms tied to offtake. Capital expenditure discipline measures adherence to Phase-2 budget and commissioning schedule. Policy linkage assesses timing and tenor of grants and credits and floor-price coverage versus merchant exposure.

Valuation lenses include enterprise value/earnings before interest, taxes, depreciation & amortization at steady-state, enterprise value/capacity in tons neodymium-praseodymium-equivalent, incremental net present value from Phase-2 and Phase-3 expansions, and internal rate of return uplift from policy supports.

The Investment Thesis for Rare Earths

- Policy-Backstopped Cash Flows: Grants, loans, credits, and floor-price constructs compress downside, enhance net present value and internal rate of return, and support multiple expansion for verified ex-China midstream capacity.

- Security-of-Supply Premium: Persistent geopolitical risk supports valuation premia for qualified Western neodymium-praseodymium/dysprosium/terbium output with credible offtakes and defense-relevant applications.

- Permitted Hubs Scale Faster: Brownfield hydrometallurgical facilities such as White Mesa shorten permitting and commissioning risk, enabling phased capital expenditure and leveraging existing infrastructure advantages.

- Feedstock Visibility: Heavy mineral sands monazite offtakes and joint ventures de-risk throughput and working capital, stabilizing earnings before interest, taxes, depreciation & amortization through diversified concentrate sources.

- Heavy Rare Earth Element Optionality: Dysprosium and terbium separation adds margin and defense relevance, diversifying revenue beyond neodymium-praseodymium while addressing critical supply chain vulnerabilities.

- Balance-Sheet Flexibility: Liquidity and modular capital expenditure reduce dilution risk and allow inventory strategy aligned with pricing cycles and contract ramps, supporting sustained operations through market volatility.

What Could Derail the Rerating, & How to Price It

Permitting and legal delays can affect even brownfield expansions through appeals, model schedule risk and covenant headroom into projections. Extended specification testing increases inventory carry costs; assume multi-quarter buffers for qualification timelines. Reagent and energy inflation stress tests should include 5–10% operating expense shocks on cash cost per kilogram and earnings before interest, taxes, depreciation & amortization margins.

Policy timing and risks arise when grants or price supports lag or undershoot expectations, raising bridging capital needs, score plans for contingency financing. Feedstock variability in monazite concentrates can lower recoveries or raise costs through impurity swings, build downside baskets into discounted cash flows. Foreign exchange and China basis risk emerge when US dollar strength and China-centric pricing whipsaw margins without contracts containing indexation and floor protections.

The investment framework requires monitoring Phase-2 execution milestones, specification acceptance timelines, and long-tenor contract development. Companies that demonstrate consistent qualification progress, maintain adequate liquidity headroom, and execute modular expansion plans should command sustained valuation premiums in an increasingly fragmented global supply chain.

Analyst's Notes

Subscribe to Our Channel

Stay Informed