US-Iran Enrichment Talks Collapse Pushes Uranium Contracts to $93/lb, Repricing OECD Assets Over Frontier Peers

US-Iran tensions push uranium contract prices $9/lb above spot, favoring OECD producers amid Western fuel supply gaps.

- The collapse of US-Iran enrichment talks over a proposed 20-year moratorium reintroduces geopolitical disruption risk into nuclear fuel pricing frameworks, reinforcing uranium's classification as a critical mineral rather than a commoditized energy input.

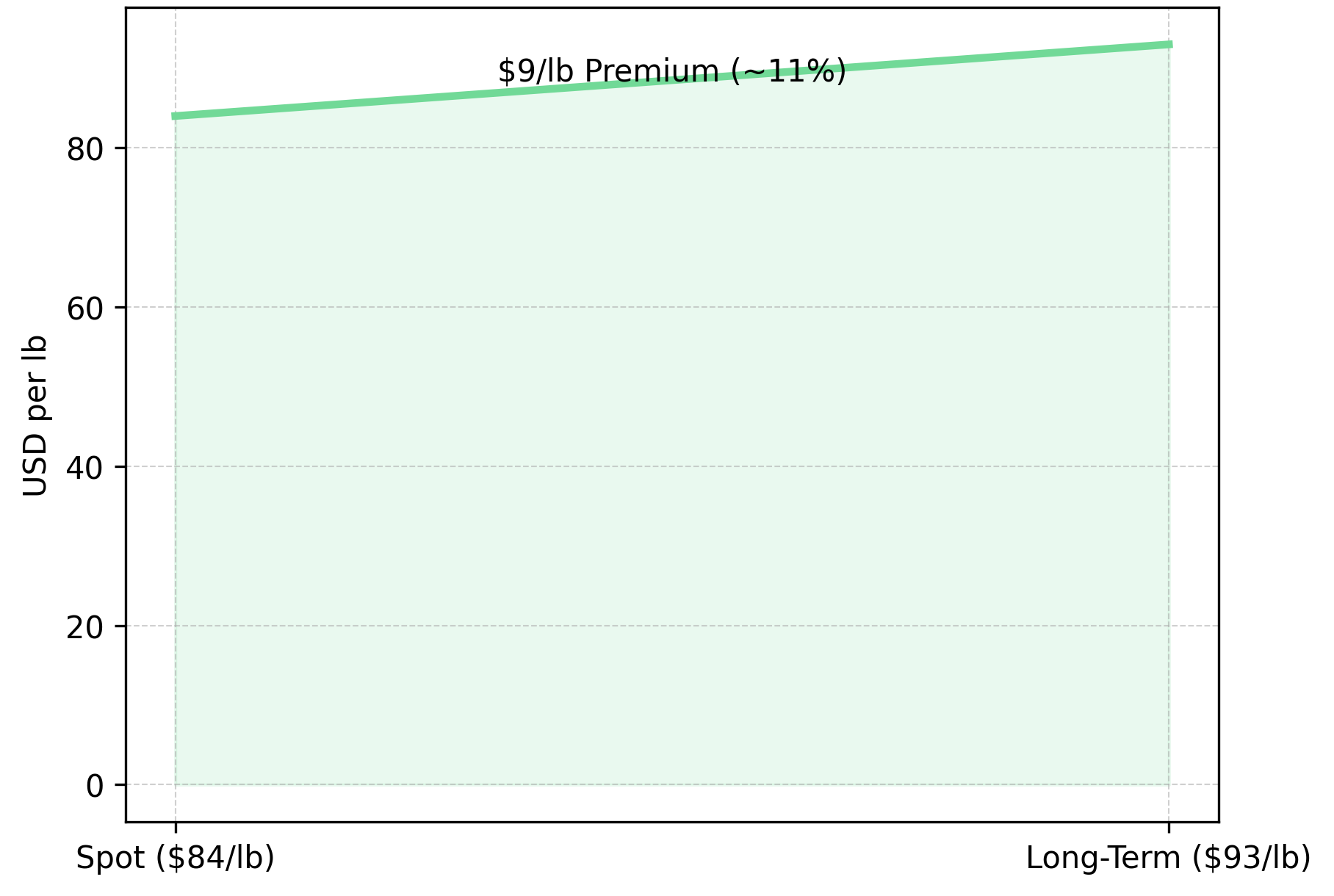

- A $9/lb difference between spot prices (~$84/lb) and long-term contract prices (~$93/lb) reflects utilities accelerating contract coverage to reduce exposure to supply interruptions, compressing the window for spot-market opportunism.

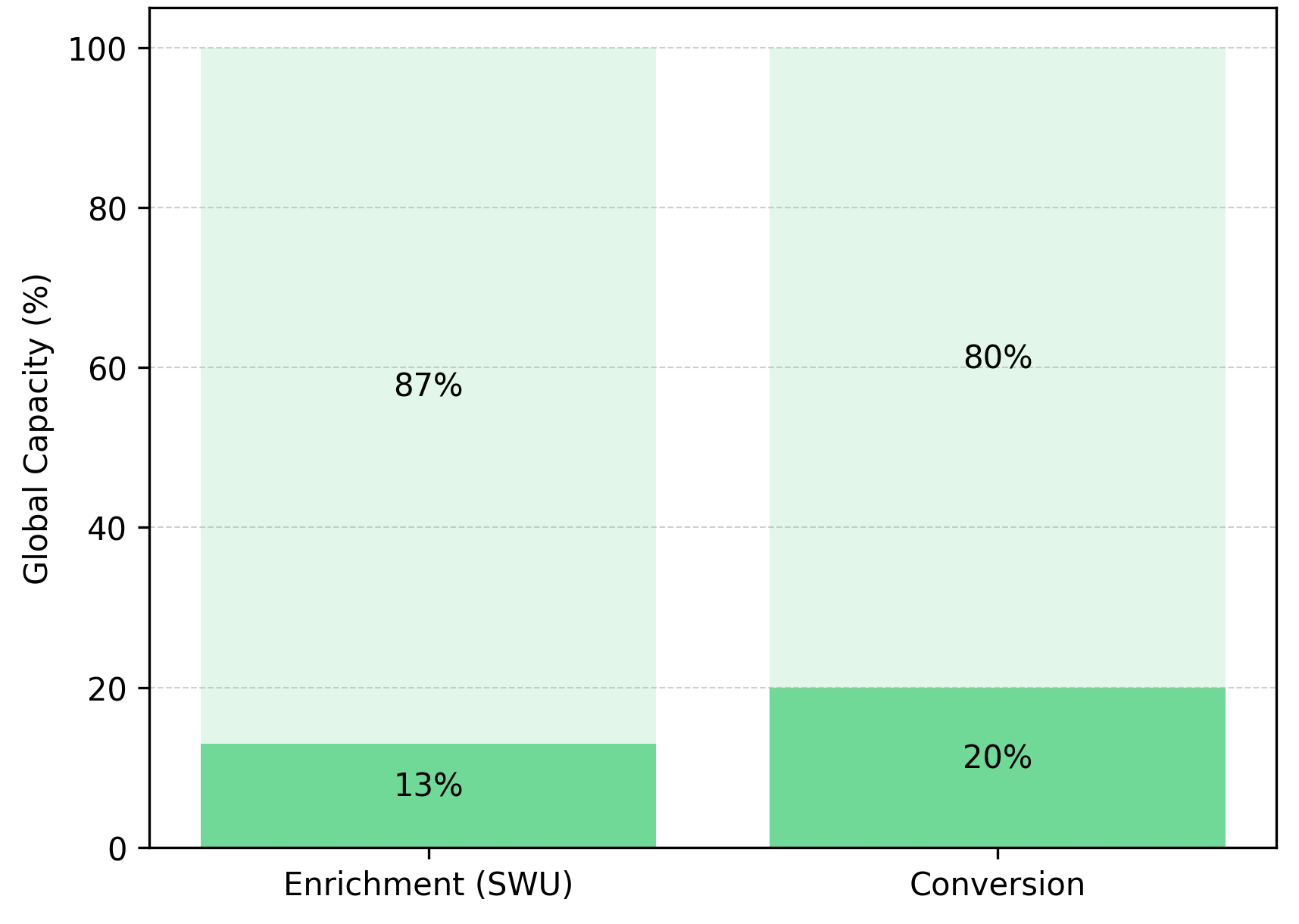

- Western enrichment capacity represents approximately 13% of global separative work unit (SWU) output, and conversion capacity covers roughly 20% of global requirements, creating a downstream bottleneck that tightens fuel availability independent of mine supply increases.

- Producers and developers operating in OECD jurisdictions, Canada and the United States in particular — are attracting institutional capital at compressed discount rates, as jurisdictional alignment with energy security mandates now functions as a primary valuation variable alongside grade and NPV in a market where long-term contracts are pricing at $93/lb.

- Exploration-stage companies holding large, high-grade land packages in tier-one basins carry NPV sensitivity that increases materially at $93/lb contract pricing, but realized value depends on completing NI 43-101-compliant resource estimates and securing institutional capital before the contracting upcycle peaks.

Geopolitics Re-enters the Uranium Pricing Framework

The breakdown of US-Iran negotiations over enrichment, centered on Washington's demand for a 20-year moratorium on all enrichment activity versus Tehran's preference for a shorter-term, monitored arrangement, has reintroduced a class of risk that uranium pricing models had largely discounted: geopolitical control over the fuel cycle itself. The expectation of constrained availability is sufficient to alter contracting behavior, and utilities are responding accordingly.

This follows the same logic that repriced oil when OPEC consolidated supply authority in the 1970s and rare earths when China dominated processing in the 2000s. In both cases, the pricing inflection was not driven by resource scarcity but by concentration of processing control. Western enrichment capacity at roughly 13% of global SWU output, combined with heavy dependence on Russian and Chinese conversion infrastructure, creates an equivalent vulnerability for nuclear fuel. Sanctions, diplomatic deterioration, or conflict scenarios that further restrict enrichment availability would tighten realized fuel supply without any corresponding reduction in mine output, a mechanism that spot-price models do not adequately reflect. The United States faces a particularly acute version of this supply challenge, where domestic production falls well short of reactor requirements.

From Commodity Input to Contract-Driven Asset Class

The $9/lb spread between spot and long-term uranium prices reflects a shift in how utilities are managing fuel procurement risk. Historically, utilities balanced spot purchases against contract coverage to minimize blended cost. The current spread inverts that logic: utilities are accepting a premium of approximately 11% over spot to secure forward supply, a behavior more consistent with energy security mandates than cost optimization.

Discount rates in stable OECD jurisdictions are compressing as revenue predictability improves through long-term contract coverage. Projects with mine lives exceeding 15 years are attracting re-rating because they can deliver against multi-year contracts without volume risk. Energy Fuels has anchored its revenue base with supply agreements extending to 2032, converting uranium production into a cash-generating platform that funds a broader critical minerals strategy.

Mark Chalmers, Chief Executive Officer of Energy Fuels, describes the strategic intent:

"Energy Fuels is a unique company because it is focused on building a critical mineral hub... that revolves around the uranium business."

Global Atomic's Dasa Project in Niger carries a base-case NPV of approximately $1.6 billion and an internal rate of return (IRR) of roughly 57%, according to the company's published feasibility study. With 700 personnel currently on site and mine development reaching the third level, the project is targeting first production in 2026, placing it in a position to enter the market during what analysts broadly expect to be a sustained contracting upcycle. The alignment of strong project economics and a contract-driven pricing regime increases the probability of above-feasibility realized pricing.

Enrichment & Conversion Constraints Redefine Where Value Is Captured

The nuclear fuel cycle runs from uranium mining through conversion, enrichment, and fuel fabrication. Mine supply is the most visible segment, but enrichment and conversion are where geopolitical fragility is most acute. Western nations operate roughly 13% of global SWU enrichment capacity and cover about 20% of conversion requirements, with the balance concentrated in Russia, China, and France. Any sanctions-related disruption to that non-Western capacity tightens fuel availability for utilities that cannot quickly redirect their supply chains.

In-situ recovery (ISR) operations, which extract uranium through solution mining while bypassing several conventional processing steps, carry shorter permitting timelines than heap leach or underground methods and are particularly well-positioned under this framework. enCore Energy controls over 50% of what its executive chairman describes as the seventh-largest uranium district in the world, with approximately 80 million pounds of resources across four US deposits.

William Sheriff, Founder and Executive Chairman of enCore Energy, identifies the bottleneck that still constrains even domestically positioned operators:

"Still, the big challenge will be the permitting."

Permitting Timelines and Vertical Integration Separate the Leaders

The permitting constraint is real, but it is not uniform. Sheriff notes that some of enCore's assets are suited to heap leaching, which carries a materially shorter permitting pathway than conventional ISR. That optionality within a single resource base allows the company to sequence development toward the assets with the fastest path to production, reducing the timeline risk that ordinarily discounts pre-production valuations.

With over ten critical minerals across its asset base and a stated capacity to deploy approaching one billion dollars in capital, Energy Fuels is building toward a supply chain position that extends from uranium production through rare earth processing and alloy production.

Jurisdictional Premiums & Capital Reallocation in Uranium Equities

Geopolitical fragmentation is producing a measurable difference in how equity markets price uranium assets across jurisdictions. OECD assets in Canada, the United States, and Australia are attracting institutional capital at lower discount rates, reflecting lower political risk, more predictable permitting frameworks, and alignment with government energy security mandates. Frontier jurisdiction assets, including those in Zambia and West Africa, continue to offer higher IRR potential at the feasibility level but carry jurisdiction-specific risk premiums that widen the gap between stated project economics and equity market valuations.

IsoEnergy holds a portfolio anchored in the Athabasca Basin of Saskatchewan, Canada, including the Hurricane deposit, which grades at 34.5% U3O8 on an indicated resource basis, placing it among the highest-grade uranium deposits globally. That grade, combined with Athabasca's status as one of the most established and fully serviced uranium mining jurisdictions in the world, has allowed the company to attract institutional capital at scale.

Philip Williams, Chief Executive Officer of IsoEnergy, describes the capital market response to that positioning:

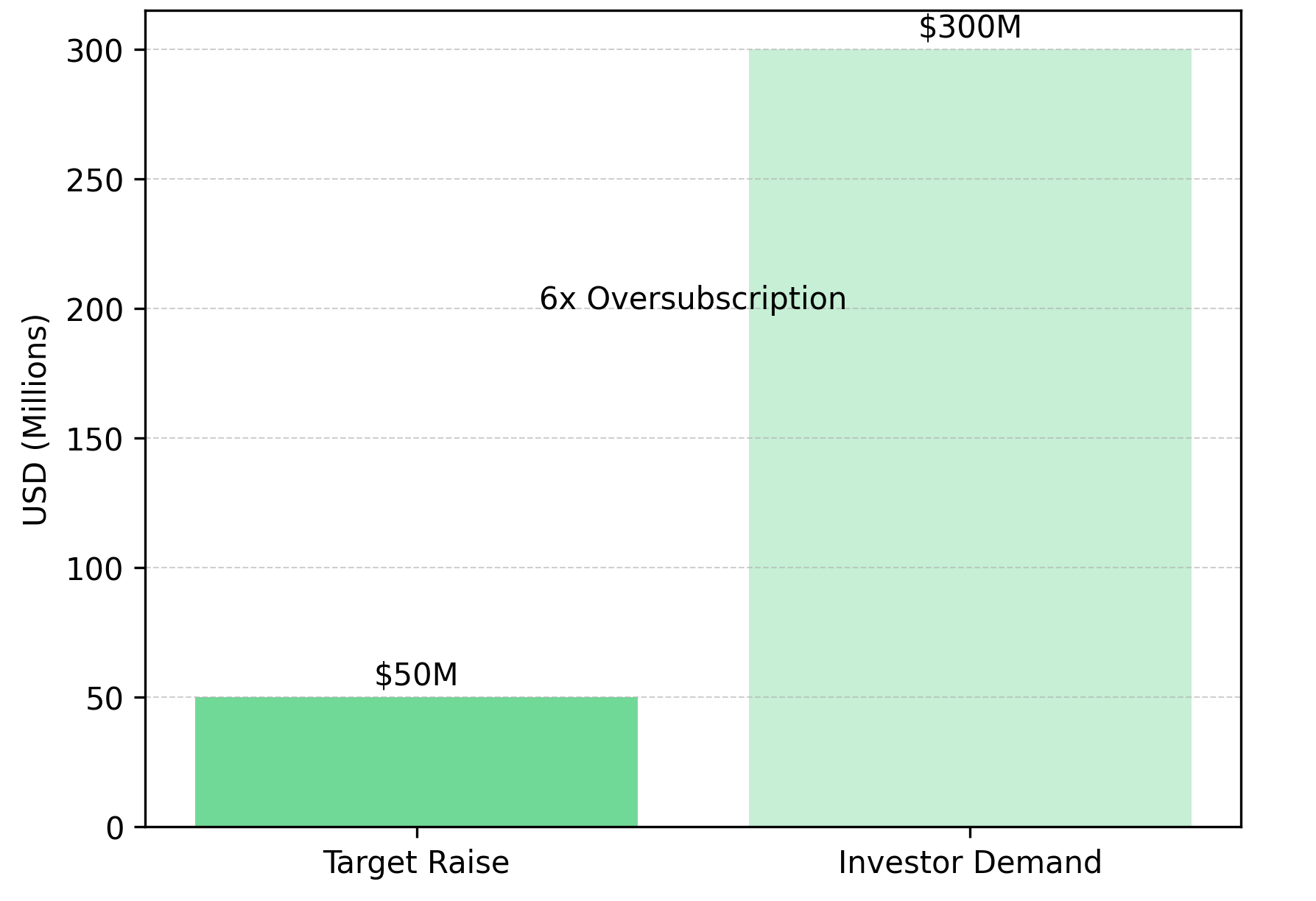

"We went out to raise $50 million, there was over $300 million in demand. It was a global set of institutional investors with very large appetites."

A six-to-one oversubscription ratio on a $50 million raise is a direct measure of institutional appetite for jurisdictionally premium uranium assets.

Frontier Jurisdictions Trade at a Discount Despite Strong Project Economics

At the frontier end of the jurisdictional spectrum, Atomic Eagle is advancing a fully permitted heap leach uranium project in Zambia with post-tax NPV of approximately $243 million and average metallurgical recoveries above 90%.

Chief Executive Officer Phil Hoskins identifies scale as the mechanism to convert strong technical parameters into compelling project economics:

"The way to make it make economic sense is scale. Our strategy is to increase the size of the resource."

Zambia's regulatory stability has improved materially over the past several years, but the jurisdictional discount relative to Canadian or US assets persists in institutional valuation frameworks. Atomic Eagle's strategy of resource expansion before a construction decision is the appropriate response to that dynamic: widening the resource base lowers the unit capital intensity of the project and reduces the discount rate justification that frontier jurisdiction risk currently imposes.

Exploration Optionality in a Supply-Constrained Market

Exploration-stage uranium companies provide leveraged exposure to uranium price appreciation but carry execution risk tied to resource definition milestones and permitting timelines. In a market where long-term contract pricing is running above $90/lb, the NPV sensitivity of a high-grade discovery to uranium price assumptions is substantial, which is why institutional capital has been willing to fund aggressive drill programs in tier-one basins.

ATHA Energy holds full control over the Angikuni Basin in Nunavut, Canada, with mineralization observed across 12 kilometers of strike length.

Troy Boisjoli, Chief Executive Officer of ATHA Energy, describes the geological results to date:

"These are the type of results that you hope for, very thick grade thicknesses of mineralization. This is an Athabasca-style intersection, both in terms of thickness and grade."

The key investment variable for ATHA is not the presence of mineralization but the conversion of drill intercepts into a compliant mineral resource estimate (MRE) under NI 43-101. Until an indicated resource is established with sufficient confidence for economic studies, the asset carries exploration-stage risk regardless of intercept quality. Resource classification, specifically the indicated-to-inferred ratio, determines the discount rate applied to the asset. Companies that advance from inferred to indicated during a contracting upcycle capture a disproportionate valuation re-rating, as improved confidence reduces the technical risk premium precisely when rising contract prices are also improving NPV assumptions.

The Investment Thesis for Uranium

- Escalating US-Iran enrichment tensions have elevated uranium's classification from a commodity input to a policy-sensitive strategic asset, supporting a sustained premium in long-term contract prices relative to spot.

- Utilities locking long-term supply agreements at approximately $93/lb provide producers and near-term developers with multi-year revenue visibility that compresses downside risk and justifies tighter discount rates in NPV models.

- Western enrichment and conversion capacity covering less than 20% of global requirements creates a structural bottleneck that tightens realized fuel availability independent of mine supply, elevating the value of domestically integrated supply chains.

- Producers and developers with permitted assets in OECD jurisdictions, particularly Saskatchewan's Athabasca Basin and US ISR districts, are benefiting from institutional capital allocation that explicitly prices jurisdictional alignment as a primary investment variable.

- Near-term producers entering the market during the current contracting upcycle are positioned to secure contract pricing well above long-run historical averages, materially improving realized project economics relative to feasibility assumptions.

- Vertical integration from mine production through conversion and rare earth processing reduces single-commodity revenue exposure and positions operators to capture value across the full critical minerals supply chain.

- High-grade exploration programs in Athabasca-style basins offer leveraged upside to uranium price appreciation contingent on successful resource definition under NI 43-101 standards.

The US-Iran enrichment standoff is functioning as a stress test on the assumption that nuclear fuel supply chains are resilient. They are not. With Western enrichment capacity covering roughly 13% of global SWU output and long-term contract prices diverging from spot by $9/lb, the market has already begun pricing the consequences of that vulnerability. The implication is concrete: valuation frameworks that rely on spot price assumptions and ignore jurisdictional risk and supply chain integration are systematically underpricing assets positioned on the right side of those variables, and overpricing those that are not. Uranium is not being repriced because of sentiment. It is being repriced because the mechanisms of fuel supply control have shifted, and the capital flows are following.

TL;DR

The collapse of US-Iran enrichment talks has reclassified uranium from a commodity input into a geopolitically sensitive strategic asset, pushing long-term contract prices to a $9/lb premium over spot. With Western enrichment and conversion capacity covering less than 20% of global requirements, utilities are locking multi-year supply agreements to reduce fuel cycle exposure, compressing discount rates for OECD-jurisdiction producers and creating a widening valuation gap between Athabasca Basin and US ISR assets versus frontier-jurisdiction peers. Near-term producers, operators, and explorers are each positioned to capture a distinct layer of that repricing, contingent on resource definition milestones, permitting timelines, and contract execution during the current upcycle.

FAQs (AI-Generated)

The $9/lb spread between spot (~$84/lb) and long-term contract prices (~$93/lb) reflects a structural shift in utility procurement behavior rather than a temporary arbitrage. Historically, utilities balanced spot purchases against contract coverage to minimize blended cost. The breakdown of US-Iran enrichment negotiations, alongside chronic Western enrichment and conversion deficits, has prompted utilities to prioritize supply security over price optimization, accepting an ~11% premium over spot to lock forward volume. That behavior is more consistent with energy security mandates than cost management, and it signals that the spread is likely to persist as long as geopolitical uncertainty around the fuel cycle remains elevated.

Western nations operate roughly 13% of global separative work unit (SWU) enrichment capacity and cover approximately 20% of conversion requirements, with the balance concentrated in Russia, China, and France. This means that sanctions, diplomatic deterioration, or conflict scenarios that restrict non-Western enrichment availability can tighten realized fuel supply for Western utilities without any reduction in mine output, a mechanism that spot-price models do not adequately capture. The parallel to China's dominance of rare earth processing in the 2000s is instructive: pricing inflections in resource sectors are frequently driven not by scarcity at the mine level but by concentration of control at the processing level.

Institutional capital is now explicitly pricing jurisdictional alignment as a primary investment variable alongside grade and NPV. Assets in Canada's Athabasca Basin, US ISR districts, and Australia benefit from predictable permitting frameworks, lower political risk, and direct alignment with government energy security mandates, factors that compress discount rates and support higher valuation multiples. IsoEnergy's Hurricane deposit, grading at 34.5% U3O8 in Saskatchewan, attracted over $300 million in demand on a $50 million raise, a six-to-one oversubscription that quantifies institutional appetite for jurisdictionally premium assets. Frontier-jurisdiction projects like Atomic Eagle's Zambia heap leach operation can carry strong feasibility-level economics, post-tax NPV of ~$243 million and metallurgical recoveries above 90%, yet still trade at a discount due to the risk premium that frontier jurisdiction classification imposes.

Exploration-stage companies like ATHA Energy benefit from the elevated NPV sensitivity that a $90+/lb contract pricing environment creates; high-grade discoveries in Athabasca-style basins carry substantially more value per pound of resource at current prices than at historical averages. However, the key investment variable is not drill intercept quality but the conversion of those intercepts into a NI 43-101-compliant mineral resource estimate with a meaningful indicated-to-inferred ratio. Until that threshold is reached, exploration-stage assets carry a technical risk premium regardless of geological results. Companies that achieve the inferred-to-indicated transition during the current contracting upcycle are positioned for a disproportionate valuation re-rating, as reduced technical risk and improving contract pricing reinforce each other simultaneously.

Vertical integration, extending from mine production through conversion, rare earth processing, and alloy production, reduces single-commodity revenue exposure and allows operators to capture value across multiple segments of the critical minerals supply chain. Energy Fuels exemplifies this strategy, anchoring its uranium revenue base with supply agreements extending to 2032 while deploying that cash flow into rare earth processing capacity. This structure converts uranium production into a platform asset rather than a price-sensitive commodity business, justifying tighter discount rates and higher valuation multiples than standalone mine operators. In a market where enrichment and conversion bottlenecks are increasingly recognized as the primary supply risk, operators with domestically integrated supply chains occupy a structurally differentiated position.

Analyst's Notes

Subscribe to Our Channel

Stay Informed