Vox Royalty (VOX) - High Growth Pure Play 3rd Party Royalties

Interview with Simon Cooper, VP Corp. Development & Riaan Esterhuizen, Exec. VP, Australia of Vox Royalty

Vox Royalty is a high growth precious metals royalty and streaming company with a portfolio of 50 royalties and streams spanning nine jurisdictions across the globe. The Company was established in 2014 and has since built unique intellectual property, a technically focused transactional team and a global sourcing network which has allowed Vox to become the fastest growing company in the royalty sector.

We recently receive a welcomed update from Spencer Cole, Chief Investment Officer at Vox Royalties. He was excited, as are the shareholders, about record revenues so far in 2021.

Overview of Vox Royalty

Vox Royalty is an Australian precious metals royalty and streaming company with a portfolio of 50 royalties and streams spanning nine separate jurisdictions across four continents. The assets are weighted 80% to Tier 1 mining countries including Australia, Canada and the USA.

Vox was established in 2014 and has since built unique intellectual property, a high-energy transactional team, and a global sourcing network, which has allowed the company to become the fastest growing in the royalty sector. Since the beginning of 2019, Vox has announced over 20 separate transactions to acquire over 45 royalties.

Vox Royalty trades on the TSXV. It has over 39 M shares outstanding.

Management Team at Vox

Vox is headed by Kyle Floyd, CEO and Chairman. In addition to Chief Investment Officer Cole, Floyd has the following individuals on the management team: Simon Cooper, Vice President Corporate Development; Pascal Attard, CFO; Riaan Esterhuizen, Executive Vice President, Australia; and Adrian Cochrane, Vice President Legal Affairs and General Counsel.

Record Revenues in Q1, 2021

Cole told us that Vox recently announced blockbuster revenues for the 1st quarter of 2021, totaling CAD $699,000, including inaugural revenues received from the Koolyanobbing royalty. This news is very exiting, he said. Cole reminded us that the company has been guiding investors that they were on the cusp of exponential revenue growth.

We asked Cole if Vox was expecting a big revenue upswing as early as this year? We were under the impression that it would really kick off in 2022. Cole responded by saying that this quarterly result is in line with that previous guidance.

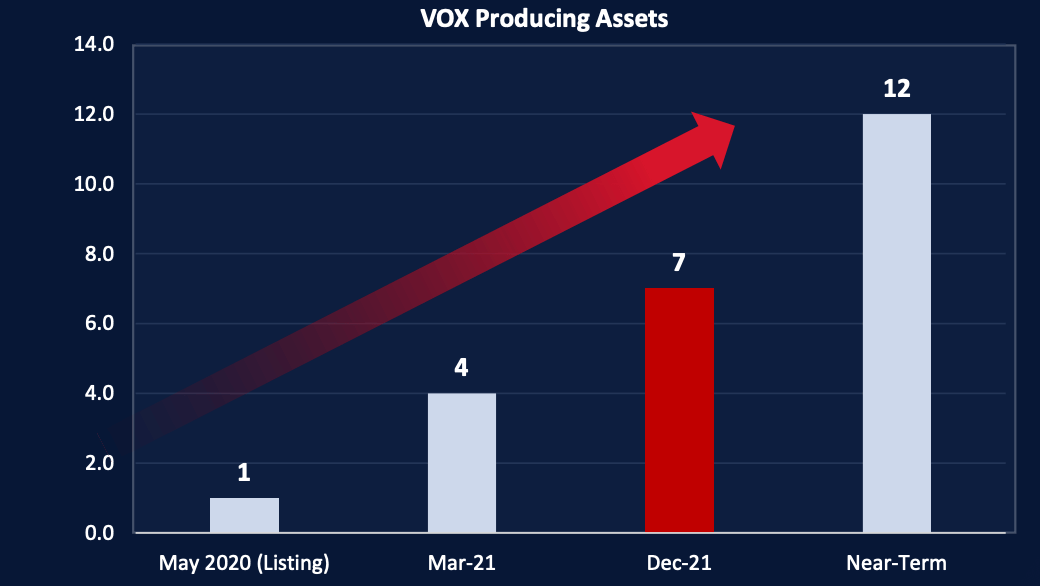

Keep in mind, he said, that they went public in May of last year with only one producing asset. They're on track to finish this year with seven producing assets, and that's without any further acquisitions. He thinks that this is just a natural maturing of Vox’s royalty portfolio, so they fully expected this evolution.

Koolyanobbing: A Big Impact

To bring people up to speed, said Cole, Vox acquired the Koolyanobbing producing iron ore royalty from a telecommunications company. Historically, the predecessor company to that had actually been prepaid a balance of $3M on that royalty. At the end of March 2021, Vox opportunistically elected to settle the outstanding prepayment balance on that royalty, which is about $1.7 M. Vox thought that it was the right time to capture that cash flow, Cole told us.

Looking deeper, because of this prepayment, Vox hadn't been seeing the benefit of a cash flow from Koolyanobbing. Thus, in terms of Vox’s multiple and where its stock trades, they wern’t getting the benefit of multiple arbitrage or rerates based on that cash flow.

To speak candidly, said Cole, Vox aspires to trade at a premium multiple. One of the levers to do that is to be able to generate cash flow. Overall, the Koolyanobbing move cost Vox about $75,000, so it wasn't cost neutral. However, when they looked at the incremental revenue, it unlocked to the bottom line for the multiple rerate from that incremental cash flow. Management became convinced that it was the right investment decision. They believe that it was money well spent, Cole said.

Rerates and Vox Royalty

We asked Cole to help the average investor understand rerates better and their impact on the bottom line of Vox Resources. He responded that one could value royalty companies based on a number of different conventional metrics, generation of cash flow being one of the principal measures. Vox has been buying a number of royalties that are “immediately pre-producing”, i.e. 3 to 28 months out until first production. Vox does this because they find fantastic value in that tranche. The downside is that these are pre-revenue when acquired, so it attracts a discount in the market. Upon producing cash, the discount closes.

The reality is that investors expect a certain amount of cash flow, and Koolyanobbing is now contributing just that. The action they took at Koolyanobbing was a important in removing valuation discount.

Why Did You Go Public in 2020?

You recently went public, we bought up to Cole? Was this just a market exercise, we asked?

The rationale was two-fold, he told us. One, with iron ore trading at long-time highs, they wanted to take advantage of the opportunity at Koolyanobbing. That generated cash flow, which led into the second reason: they wanted to move Vox Royalty into a company that trades at a premium in the public arena.

Vox is not about promotion, Cole told us, instead Vox all about prudent capital allocation. To be absolutely clear, their total net cost for Koolyanobbing is still about AUD$3.5M. It is generating approximately $1M/year, so when you look at it on an internal rate of return basis, it is still an incredible investment for the shareholders, even with the prepayment settlement. This is certainly not Vox changing its strategy or moving away from being prudent allocators of capital. Koolyanobbing is still one of the best investments in the Vox portfolio. Nothing has changed from that perspective, Cole said.

More broadly, he said, every time Vox allocates capital, whether it's to a new acquisition or to something like a prepayment settlement, it's always through the lens of shareholder value. Management always looks to unlock the greatest alpha for shareholders, Cole said.

Revenue Guidance Going Forward

By the end of this year you will have seven paying Royalties. You've got 50 Royalties in total; about 30 of those are exploration. What can we expect next year, we asked Cole?

Vox hasn't provided formal guidance to the street for 2022 as yet, he replied. However, brokers have us going from about $2M this year to $6M next year, then towards $8M the following year in top-line revenue.

Investors can expect contributions from three main components in the royalty portfolio going forward, Cole told us:

· Producing Assets. They had one in mid 2020, now they have seven.

· Developing Assets. There are a number approaching key construction decisions, including Lynn Lake, Bowdens Silver, Sulphur Springs, and other. In total, these will add in multiple $M’s of annual revenue.

· Exploration Assets. Vox has about $130,000 m of partner-funded drilling each year in its 30 or so exploration assets. One of these, the Mt. Moss royalty, is set to be brought into production as early as this year. They also have an exciting Vanadium discovery in Brazil that is scheduled to go into trail mining in Q1 2022. Shareholders should not be surprised for major surprises to the upside at Vox, said Cole.

One project that the company is undertaking is the preparation of an asset handbook for interested parties as well as current shareholders. It’s a best practice that some of the big companies such as Franco Nevada use to their advantage, he said. Their asset handbook is intended to provide soup-to-nuts details on each royalty, from inherent geology all the way through expected royalty return and asset lifespan.

The Impact of Letters of Intent (LOI’s)

The last time we spoke, we talked about LOIs. Can you fill us in on how some of these are progressing at Vox, we asked?

Indeed, he said, when they completed their last financing they had 10 potential deals that were covered by letters of intent. As of the time of this interview, they've acquired three separate gold royalties in Western Australia: the producing Janet Ivy Royalty, the pre-production Otto Ore Royalty, and the very large, development-stage Barabolar Royalty. Behind the scenes, they are still working on confirmatory due diligence to make sure that all the other letters of intent and the royalties that they cover are up to Vox’s internal investment thresholds and standards.

Business has been brisk, he said. He thinks Vox has lost about 7 separate royalties to mining companies in recent months. It’s frustrating, he said, but as prudent allocators of capital, they will not overpay.

Investors should look for more of these LOI’s to close in coming months. But, he cautioned, Vox prefers value investing, so they will be selective. Each one must meet very rigorous, technical and financial hurdles, such that the cash on cash returns that they'll be generating will be very attractive, Cole indicated.

Cole’s Thoughts About Recent Share Price Action

We’ve seen some volatility in the Vox share price, we noted. We asked Cole to comment on that.

As long-term shareholders themselves, leadership keeps a sharp eye on that, he relied. Management owns about 15 % of the outstanding shares, and they are not particularly happy with the share price, he told us. One thing they are concerned about is a certain type of shareholder that was picking up shares because of their warrants. It became painfully obvious, he said, that some were just interested in clipping the warrant and then selling out of that position that they picked up during the financing. They see that as a short-term abnormality, he said. To be perfectly honest, he went on, management doesn’t including warrants as part of any financing, so they won't include warrants unless they absolutely have to.

Regarding cash flow, they are in great shape today according to Cole. He said that they are not going to need to tap the market from an equity perspective anytime soon. They are selectively speaking to some groups about potential debt capacity, which would only be used for the right type of royalty acquisitions. In addition, there are other non-dilutive ways that they're looking at for unlocking value for shareholders that could come to market in the next couple of months.

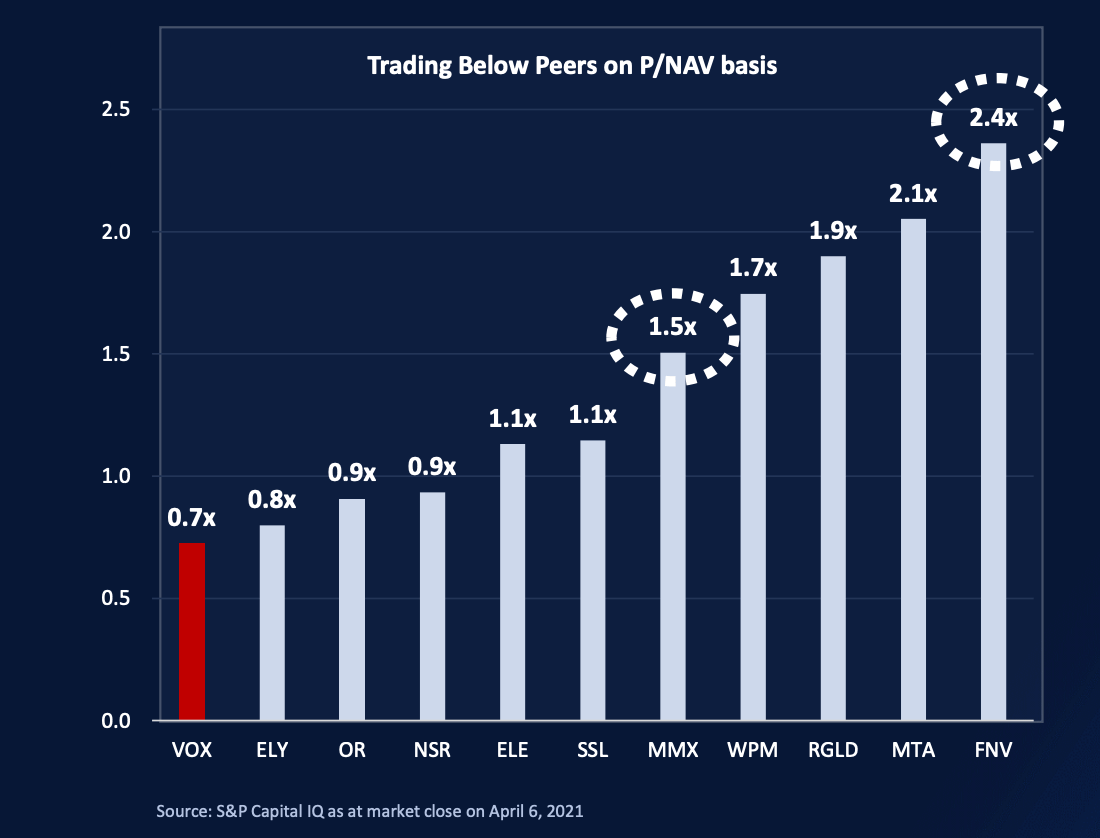

They remain frustrated by the share price but that is delinked from the fundamentals of the business, Cole told us. As cash flow continues to grow and as their royalties continue to deliver surprises to the upside, the market will reflect increases in fundamental value. Cole believes that Vox can't stay trading for very much longer at 0.7 times net asset value (NAV) when the rest of the industry is trading at two times NAV.

Forward-Looking Thoughts

It looks like you’ve got your hands full, we exclaimed! Cole closed out the dialogue by saying that they’re continuing to work with their major investors to understand exactly their preferences and to ensure that the company’s knowledge of its share register and its relationships with key investors are as strong as they could possibly be. They intend to focus on long-term shareholders who are really aligned with the vision of what Vox is building.

To find out more, go to the Vox Royalty website

Analyst's Notes

Subscribe to Our Channel

Stay Informed