Wallbridge Mining (WM) - Growing Grade on 2.7Moz M&I MRE

Interview with Marz Kord, President & CEO of Wallbridge Mining

We caught up again with Marz Kord, President, and CEO of Wallbridge Mining. He shared with us some updates about the company’s Fenelon and Martinière projects in Québec, Canada. He provided details about the recent announcement about the maiden resource estimate (MRE) at Fenelon and Martinière. Be sure to access the earlier conversation we had in 2021 with Kord already loaded onto Crux Investor.

Company Overview

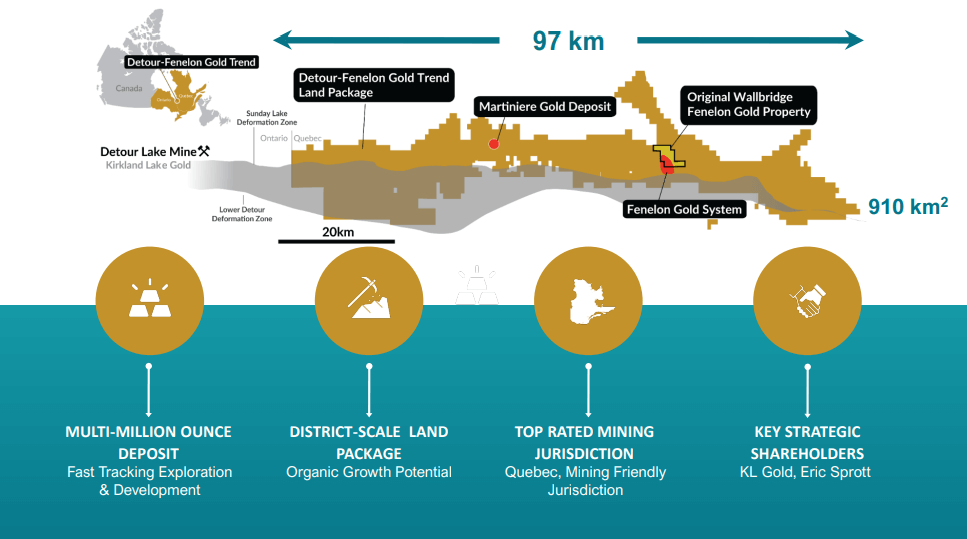

Wallbridge Mining is a Canadian exploration and development company that utilizes a strategic and targeted approach to value generation. The company primarily explores for gold as well as copper, nickel, and platinum group metals (PGM). The company is currently focused in the Detour-Fenelon Gold Trend of Québec, Canada, where it has a land position of over 900 km2

The company has a market capitalization of $307 M. Its shares are listed on the TSX and the OTC. There are over 834 M fully diluted shares outstanding.

Management Team

In addition to the CEO, Kord, the company is managed by Brian Penny, CFO; Francois Demers, Vice President Mining and Projects; Mary Montgomery, Vice President Finance; Attila Péntek, Vice President Exploration; Sean Stokes, Corporate Secretary; and Victoria Vargas, Investor Relations Advisor. A diverse nine-member board, chaired by Alar Soever, assists the management team.

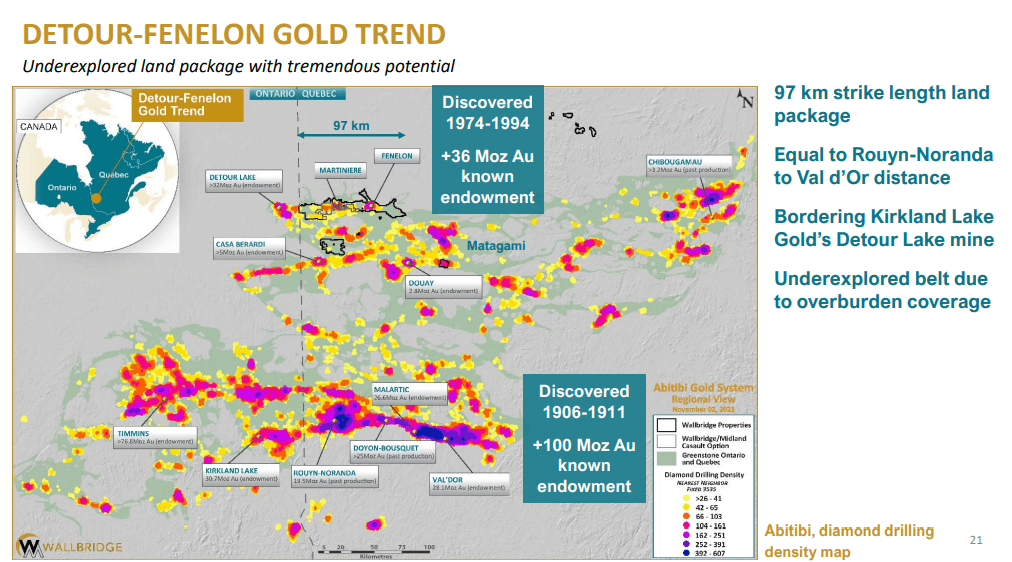

The Detour-Fenelon Gold Trend

Walbridge’s properties are located in the Detour-Fenelon Gold Trend, which is part of the Precambrian Abitibi Sub-Province in Québec. Gold and other minerals in the Abitibi are typical of orogenic gold deposits in terms of metal associations, ore grades, associated alteration assemblages, and structural geological controls.

Interestingly, the Detour-Fenelon Gold Trend remains relatively underexplored in comparison to the other prolific gold belts within the Abitibi Province. Since 1901, the Abitibi has produced over 100 mines and 170 million ounces of gold have been extracted.

The Flagship Project: Fenelon Gold

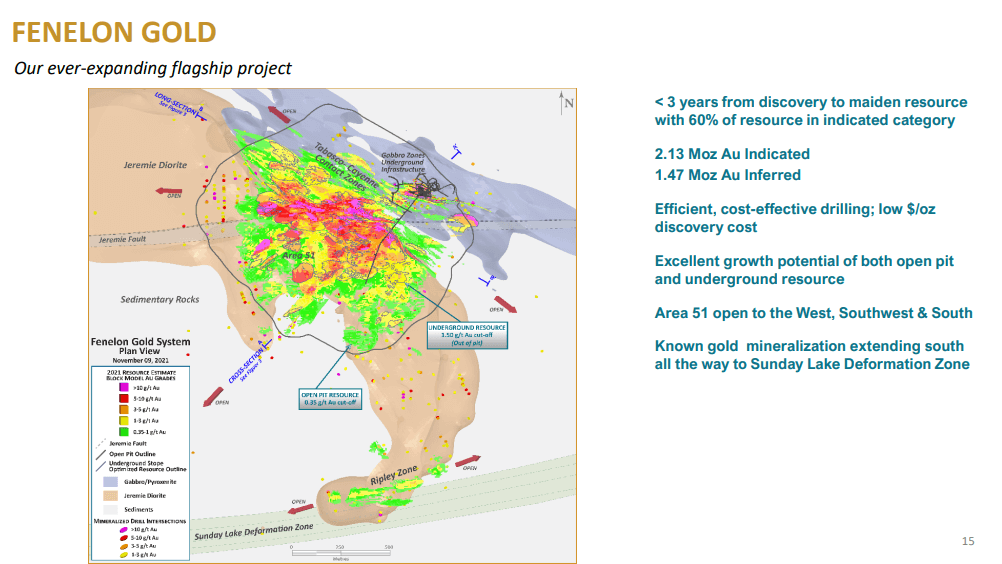

The Fenelon Gold project, comprising a 73-km2 land package, is located approximately 75 km west-northwest of Matagami, Québec, Canada. The company owns 100 percent of the mineral rights at Fenelon. Gold mineralization on the Fenelon Gold property was first discovered by Cyprus Canada in 1988. Wallbridge acquired Fenelon in 2016 from Balmoral Resources.

The gold occurrences are structurally controlled and affected by ductile deformation. Gold occurs in three main areas: The main Gabbro Zones, the Cayenne and Tabasco area, and Area 51. Gold is associated with disseminated pyrrhotite, chalcopyrite, and pyrite, plus minor sphalerite, arsenopyrite and marcasite. Visible gold is common in all zones.

Fenelon is currently in an advanced stage of exploration. Wallbridge is engaged in a robust drilling program at the project.

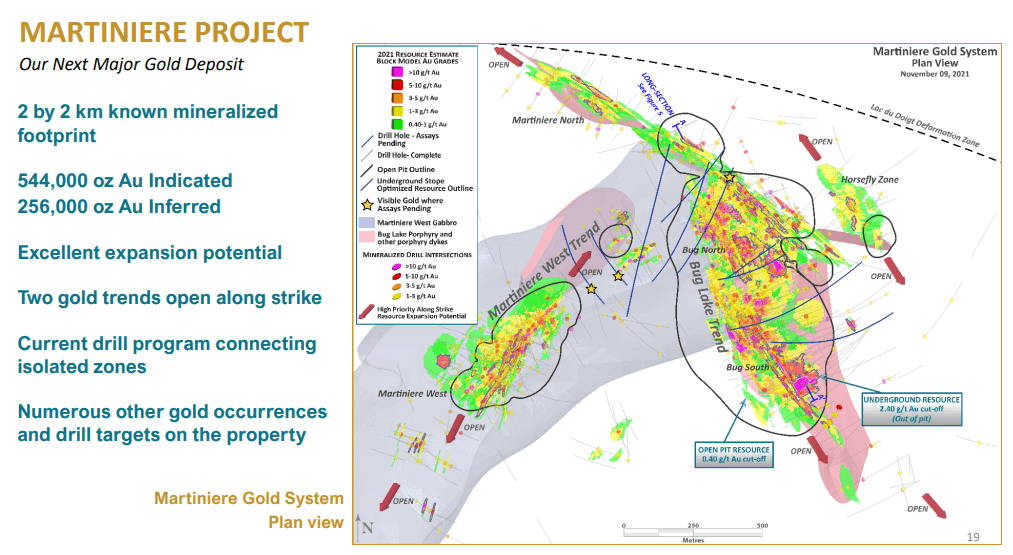

The Martinière Project

Martinière is about 30 km west of Fenelon and 45 km east of the Detour Lake mine operated by Kirkland Lake Gold. Martinière is 100 percent owned by Wallbridge. Gold occurrences are hosted by mafic volcanic rocks and are strongly controlled by the Precambrian structural fabric, including the Sunday Lake Deformation Zone, the Martinière West Shear Zone, and the Bug Lake Fault Zone.

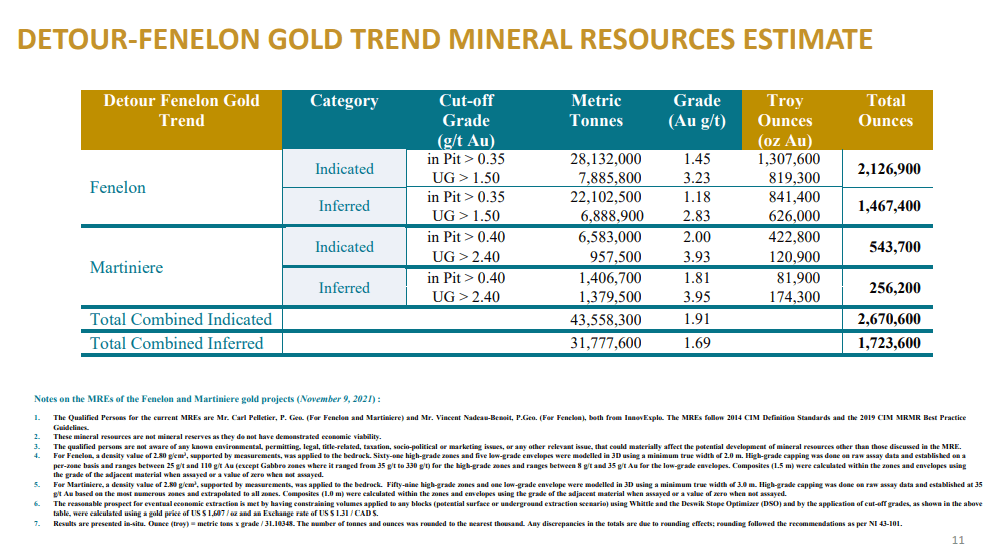

Maiden Resource Estimate at Fenelon and Martinière

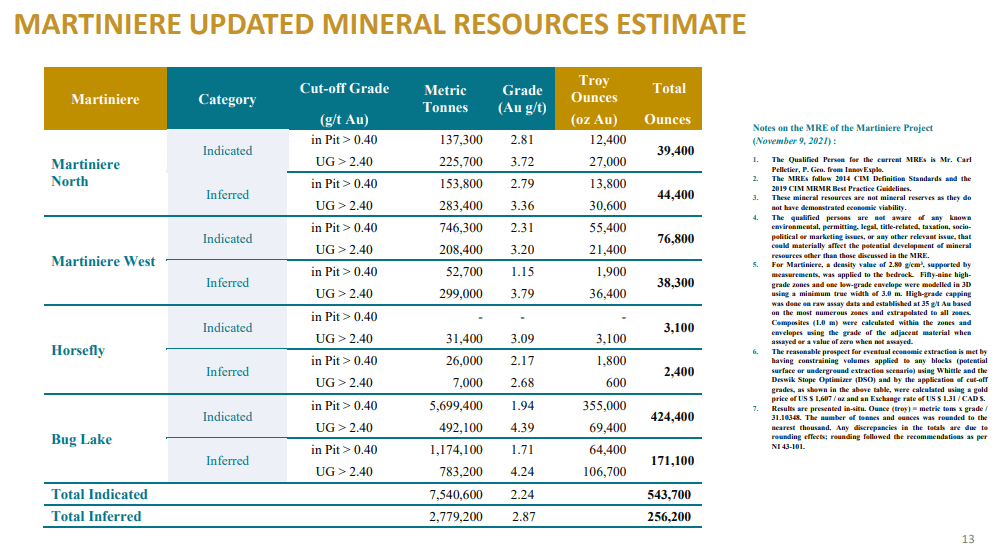

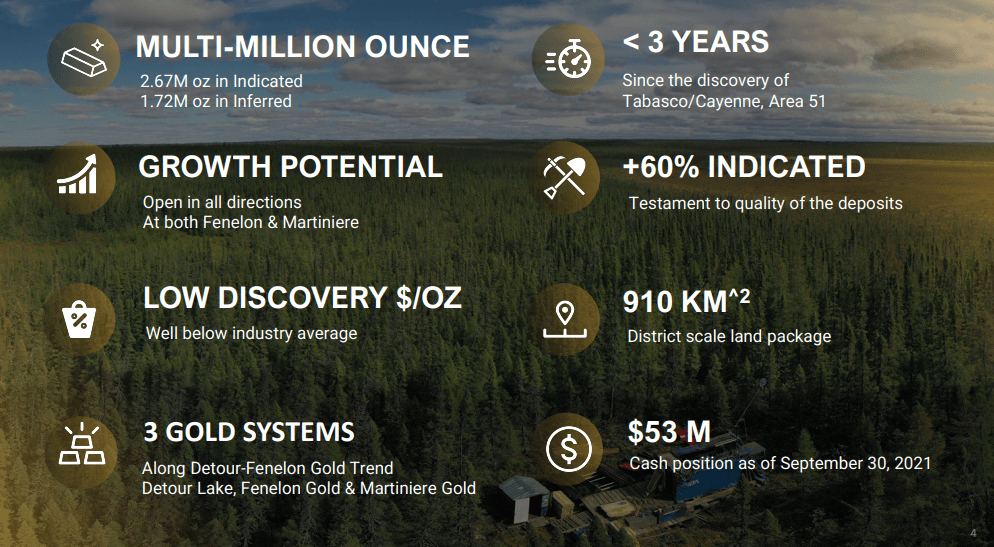

In November 2021, Wallbridge announced a MRE estimate at Fenelon consisting of 2.13 million ounces of indicated gold and 1.47 million ounces of inferred gold. An MRE was simultaneously announced at Martinière, consisting of 543,700 ounces of indicated gold and 256,200 ounces of inferred gold.

Delay In Reporting the Maiden Resource

Earlier, Kord publicly indicated that the MRE at Fenelon was to be released publically by September 2021. It actually came out two months later. Kord stressed that the company was waiting on assay results and was having ongoing interactions with its consultants regarding the timing of the release.

Despite that, Wallbridge is very pleased with the numbers in the MRE. Including both Fenelon and Martinière, it announced 4.4 M oz. of gold. Sixty percent of that is indicated, which is unusually high for most first resource estimates. It just speaks to the quality of the deposit, added the CEO. And these numbers are just the first results; Fenelon in particular has tremendous room for growth.

The delay in announcing the MRE was not because of prolonging the drilling. In fact, the drilling was actually cut off at the end of July. The company anticipated that the assay results from that drilling would be in time for a September MRE release, but these analyses were delayed.

Was Delaying the MRE release Prudent?

Could Wallbridge have made a public announcement that it intended to delay the release of the MRE? Did the company delay the release so that they could have better MRE numbers? Kord said no, and indicated that the market expected the company to actually deliver a baseline result and it was very conscious of not coming up with a certain range of numbers. At the end of the day, it’s an independent consultant who does that.

Details on the Growth Potential

The great MRE numbers point to continued upside potential. Now, the company’s focus will be on expansion drilling rather than trying to convert from inferred resources to indicated resources. This focus will actually save the company some drilling costs as well.

At Fenelon, the MRE results are strictly from a 1-km2 area. To the south of that, there is considerable potential that exists for about a km toward the Sunday Lake Deformation Zone. Additionally, to the southwest where the company has already done some drilling, it found over 10 g/t of gold, so expansion is envisioned in that direction as well.

Over to the northwest, there are a lot of areas that the company was looking at when it was drilling the Gabbro Zone. Historically, previous owners didn’t sample much there because they were all looking specifically for double- or triple-digit grades in the gabbro. In addition, Gabbro East Zone, discovered only a few months ago, also has the potential to add ounces.

Closer to the MRE area, some drill holes have encountered rock with over 5 g/t and 10 g/t of gold. These weren’t included in the MRE. Additional drilling will almost certainly enable more resources to be added from there as well.

All told, the original 1 km2 can probably be expanded to a 2 km2 area, essentially quadrupling the area size of the resource.

Considerations About the Ore Quality

It is important to keep in mind that these discoveries occur in orogenic-type ore bodies. These types of ores can indeed be high grade, but more often occur as lower- to medium-grade ores interspersed with higher-grade veins.

In the company press releases, it indicated in several places the high-grade ore it was encountering. Kord went back to some of these and the company has been assessing whether it should have communicated better. Assays were disclosed in the 2021 press releases on March 8th, March 22nd, May 6th, June 2nd, June 29th, and October 6th. In each of these, the bulk-mining ability of the deposit is discussed. The releases indicated the fact that there are high-grade veins as well as lower grade veins. Typical of this is one case where the company released a discussion about high-grade veins containing 3 to 10+ g/t of gold surrounded by zones having from 1g/t to 3g/t of gold. Wallbridge can effectively mine the whole ore range because it will be low-cost mining.

The rock system is similar, for example, to what is currently being developed at Yamana’s Wasamac Project, consisting of about 6,000 to 7,000 low-cost t per day. These aren’t low-grade, uneconomic ounces. Yamana has obtained at 2.17 to 2.65g/t for the past three years at Wasamac.

Another example is Gold X Mining Corp. They are mining gold from rocks with 1.3 g/t and are making money.

How Does Wallbridge Ally Investor Fears and Concerns?

Despite this reassurance, the high grades released to the press have the power to attract bigger players and funding. The reality of mining an aggregate of big, medium, and lower grades in bulk may present a different scenario to some.

Kord realized that he must become a better communicator in order to allay any investor concerns. Even though he reviewed the bulk mining aspects in each of the referenced press releases, he also agrees that he needs to do a better job in the communications area. Clearly, he realizes that the high-grade ore exists, but in these orogenic systems it’s the bulk ore grade that is important. Everything needs to be looked at in order to optimize the ounces that are going to be mined.

The Plan Forward

Kord indicated that there is no doubt in the company’s mind that it needs to drill more to bring Fenelon and Martinière to the next stage to really get after their ultimate size. About 150,000 to 200,000 m of drilling at Fenelon, and some 50,000 m at Martinière would get the company to the point where it would be able to carry it out to an economic study. But first, the next exploration programs must be completed before moving forward with an economic study.

Company Cash Situation

Wallbridge had CAD $53M on hand at the end of September 2021. It is expecting a refundable tax credit of about $7M from the Québec government, which would bring the amount in the company coffers up to about $60 M. After planned expenditures, about CAD $40 will remain in the company treasury.

Wallbridge is expecting to receive a 2020 tax credit of roughly $10M, before mid-year 2022. The upcoming drilling program would require more than that $50 M. The company intends to review funding optionality in 2022 for the balance of its program.

Quantifying the Size of the Prize

Without some type of economic study, the company needs to address how it intends to quantify the value of what they are creating by way of the drilling program in 2022. The majority of the retail investing crowd may have a tough time understanding exactly how this will be done. The company is already down over $300 in market capitalization since the beginning of 2021.

Kord intends to quantify some of that based on what the company’s expenditures have been. Looking at the costs incurred at Fenelon alone, it was an under-$30-per- ounce discovery in terms of the total ounces. Looking at that in terms of what the potential growth would be, Wallbridge expects to match the same dollar per ounce discovery in the future in the next phase of the exploration program.

The industry average is roughly about $50 to $55 just for the inferred gold resource, and then an additional $30 to $50 to convert that to the indicated category and bring it up to an economic study. Those are the kind of metrics that the company will be applying going forward.

Without mentioning any specific names, Kord referenced some other gold companies. For example, there is one company that’s over $1Bn and its discovery cost is over $78 per oz. Other companies are in that range as well.

Hence, the quality of the deposits at Fenelon and Martinière will allow Wallbridge to be in a lower quartile in the discovery-cost-per-ounce category. The company hopes to operate in that mode during the next phase of the exploration program.

Of course, the other component of quantifying the value is to prove up an increase in ounces with the upcoming drilling program. That goes not only for Fenelon but for Martinière as well. Martinière was 600,000 oz. when acquired from Balmoral Resources. It’s currently at 800,000oz. Wallbridge believes that it is going to be able to significantly improve the resource there to perhaps a multiple of where it is today with the additional exploration drilling.

Should Investors View Fenelon and Martinière as a Single Asset?

Both deposits can be considered as a single asset according to Kord. The two deposits are 30 km apart. In other places in Canada, such as in the Sudbury area, multiple occurrences 50 to 70 km apart function as a single asset.

Martinière doesn’t need a tailings facility. It doesn’t require a mill. All of that will be at Fenelon and all that is needed is the transportation costs of the Martinière ore over the 30 km distance to Fenelon.

If Martinière gives a certain number of ounces to Fenelon, those ounces should be multiplied by a factor that accounts for Wallbridge no longer having a milling and tailings CAPEX to add in. And that is just regarding the gold from Martinière. Wallbridge has a 97-km-long land package. It is currently drilling at another project, Grasset, only 2 km from Fenelon. A discovery at Grasset would definitely help the economics at Fenelon.

Discussion on Value Creation

Success obviously requires the development of a mine or mines on Wallbridge’s properties. Although this is a bit down the road, Kord realizes that he needs to make it a plain-vanilla story going forward. The company has a nearly 1000-km2 land package. It will not go and poke holes everywhere it sees targets.

At the current time, Fenelon is clearly the most advanced and number one asset. The second priority is Martinière. Then Wallbridge will dedicate some 5 to 10 percent of its exploration drilling efforts for regional exploration efforts, to identify other targets. The intent is to create value for the shareholders: Fenelon can grow on its own, Martinière can add value to it, and then, on top of that, there are other projects that could come through the pipeline. That is the scenario that would set up the best outcome for Walbridge’s gold assets.

The company expects to be drilling aggressively in 2022. Then, in 2023, the time would be right for economic studies, according to the CEO. Additionally, Eric Sprott, one of the company’s shareholders, is happy with the company’s progress so far and the scenario going forward just presented.

Sprott and other large Wallbridge institutional shareholders are comfortable with a development scenario that incorporates a large open pit. That’s the ultimate development plan.

Wallbridge’s Nickel Assets

In addition to gold, Wallbridge holds a large portfolio of nickel assets in Ontario and Québec as well. Kord has some comments on these assets as well. He indicated that nickel prices typically shouldn’t matter in terms of exploration. When the nickel prices are high, some companies focus their efforts on nickel but by the time they come up with the resource, nickel prices will have gone down. Cycles don’t always work in a company’s favor.

From Wallbridge’s point of view, it sees a lot of value in the nickel at its Grasset Asset, and it also sees tremendous value in its copper-nickel-PGM asset in Sudbury, Ontario.

Grasset is closely attached to Fenelon. Wallbridge sees a lot of potential for gold at Grasset. For Wallbridge to sell Grasset or do any kind of deals with anyone, you have to look at two different groups. One would be the major companies, another would be the junior companies.

At Grasset, there is 5.5 Mt of very good nickel grade but this is not something that the majors are interested in purchasing. In terms of a joint venture, there hasn’t been as much interest, particularly because of the asset’s location.

There are a lot of interested parties from the junior side. But, at the end of the day, Wallbridge doesn’t want to end up as the largest shareholder of any junior company because, obviously, they’re not going to be able to pay the cash to use towards the exploration program at Fenelon.

Until now, Wallbridge has not seen enough credible groups that can actually get more value for it than simply holding onto it until it does something better with it. The material is not rotting, it’s still in the ground, and it’s still there. A value proposition will eventually manifest.

In terms of the copper-nickel-PGM assets in Sudbury, it’s always been two joint ventures with Lonmin Canada and Stillwater. Wallbridge is working with them to unencumber those joint ventures in order to extract value.

Wallbridge is not going to spend a dollar on exploration for nickel, copper, or PGM. Its focus is on gold.

Summary Thoughts for Investors

Investors should look to additional press releases in 2022 updating the drilling results as they come in. Gold has been out of favor over the past few months. Wallbridge sees 2022 to be a better year in terms of the gold environment. The fact that the company will be sitting with CAD $40M in the treasury is a very flexible advantage that it will have over some of its competitors.

Kord intends to improve his communication efforts as well. At some point, the company will need to raise money, but it intends to do that as responsibly as it can. That’s what is needed to unlock value at its gold assets.

To find out more, go to the Wallbridge Mining Website

Analyst's Notes

Subscribe to Our Channel

Stay Informed