West Red Lake Gold Delivers Strong Economics with Rowan Project PEA, Targeting 35,000 oz Annual Gold Production

West Red Lake Gold's Rowan Project PEA shows 41.9% IRR, $125M NPV, and 35,230 oz/year production over 5 years with low $70M initial capital in Red Lake district.

- The underground mine targets 35,230 oz average annual gold production over 5 years with an exceptional 8.0 g/t average diluted head grade, demonstrating high-grade mining operations

- Post-tax NPV reaches $125.3 million at $2,500/oz gold price with robust 41.9% IRR, rising to $239 million NPV at current gold prices near $3,250/oz, delivering strong financial returns

- The project requires modest $70.4 million initial capital by leveraging regional toll milling capacity, with all-in sustaining costs of $1,408/oz representing low capital requirements

- The resource base provides high confidence with 63% of mined tonnes and 72% of ounces from indicated category, creating a solid foundation for prefeasibility advancement

- Multiple expansion opportunities exist through depth extension, parallel vein development, and exploration of new high-potential targets, offering significant growth potential

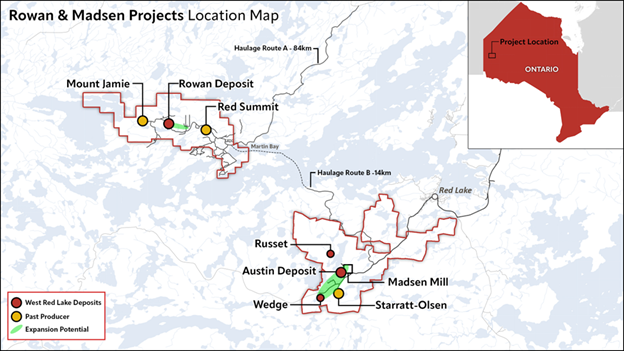

West Red Lake Gold Mines Ltd. (TSXV: WRLG) (OTCQB: WRLGF) is a Canadian gold mining company strategically positioned in Ontario's renowned Red Lake Gold District, one of the world's most productive high-grade gold regions. The company operates its flagship Madsen Gold Mine on a 47 km² highly prospective land package, benefiting from the district's exceptional geological endowment that has produced over 30 million ounces of gold from high-grade zones. Beyond Madsen, West Red Lake Gold holds the wholly owned Rowan Property covering 31 km² in Red Lake, which includes three past-producing gold mines: Rowan, Mount Jamie, and Red Summit. This strategic asset base positions the company to capitalize on the district's continued gold production potential while leveraging existing infrastructure and regional expertise.

Robust Economics Drive Rowan Project Forward

The Preliminary Economic Assessment for the Rowan Project reveals compelling economics that underscore the deposit's potential as West Red Lake Gold's second operating mine in the Red Lake district. As President and CEO Shane Williams noted:

"Rowan is a high grade, relatively wide, nearly vertical deposit that starts at surface and this PEA captures how such designed-for-mining characteristics lead to strong economics."

The study, prepared by independent consultants Fuse Advisors with input from specialized firms, demonstrates how the project's high-grade, near-vertical deposit characteristics translate into strong financial performance. With an average diluted head grade of 8.0 g/t gold and annual production averaging 35,230 ounces over the five-year mine life, Rowan represents a significant addition to the company's production profile.

The financial metrics highlight the project's attractiveness to investors and stakeholders. At a long-term gold price of $2,500 per ounce, the post-tax net present value reaches $125.3 million with an internal rate of return of 41.9%. These figures become even more compelling when considering current gold market conditions, with the NPV rising to $239 million at $3,250 per ounce gold pricing. Williams emphasized the significance of this valuation:

"A NPV of $239 million at close-to-spot gold pricing provides a compelling case to advance Rowan swiftly from here."

The project's sensitivity to gold prices provides substantial upside potential, with a 30% increase in gold prices resulting in an 82% IRR.

The economic foundation rests on the project's low capital intensity and operational efficiency. Initial capital requirements of just over $70 million reflect the strategic decision to pursue toll milling, taking advantage of excess capacity at regional processing facilities. This approach significantly reduces upfront investment while maintaining operational flexibility. The all-in sustaining costs of $1,408 per ounce position Rowan competitively within the industry cost curve, ensuring strong margins across various gold price scenarios.

Strategic Toll Milling Approach Minimizes Capital Requirements

The decision to develop Rowan as a toll milling operation represents a strategic advantage that differentiates the project from traditional standalone mining operations. This approach leverages the Red Lake district's existing processing infrastructure, where multiple mills operate with excess capacity, creating an opportunity to minimize capital expenditure while accelerating development timelines. The toll milling cost of $67.44 per tonne, based on first-principle estimates and regional processing knowledge, provides a competitive processing solution that enhances project economics.

The infrastructure requirements focus on essential mining and material handling components rather than complex processing facilities. Surface infrastructure includes a crusher, sampling tower, polishing pond, water treatment plant, waste rock facility, mine dry facility, small camp, maintenance shop, and electrical infrastructure. This streamlined approach reduces both initial capital requirements and operational complexity while maintaining high safety and environmental standards.

The underground mining strategy employs longhole stoping methods optimized for the deposit's near-vertical orientation and 2-meter average width. The mine plan requires 1.4 kilometers of capital development, including remucks, sumps, and level access points, before accessing first ore. The mining sequence strategically targets high-grade zones early in the operation, achieving a 10.4 g/t gold average head grade in Year 1, which supports strong early cash flow generation and rapid payback of initial investment.

High-Grade Resource Base Provides Strong Foundation

The Rowan Project's mineral resource estimate demonstrates the quality and scale of mineralization that underpins the PEA economics. With 478,707 tonnes of indicated resources grading 12.78 g/t gold containing 196,747 ounces, plus 421,181 tonnes of inferred resources grading 8.73 g/t gold containing 118,155 ounces, the deposit represents a substantial high-grade gold inventory. The resource estimate, effective June 30, 2025, reflects non-material modifications to the previous technical report and provides a solid foundation for mine planning and development.

The confidence level in the resource base significantly enhances the project's feasibility and reduces development risk. With 63% of mined tonnes and 72% of mined ounces derived from the indicated category, the PEA mine design relies predominantly on higher-confidence resources. This distribution provides substantial certainty for transitioning to prefeasibility study level assessment and eventual production planning.

The metallurgical characteristics further strengthen the project's viability. Free gold-dominant mineralization achieves 75.8% to 94.9% gold recovery through gravity processing during metallurgical test work, supporting both the toll milling approach and processing cost estimates. The simple metallurgy reduces processing risk and supports consistent recovery rates throughout the mine life, with an assumed 97% overall gold recovery incorporated into the economic analysis.

Significant Expansion Opportunities Enhance Long-Term Value

Beyond the immediate PEA mine plan, Rowan presents multiple avenues for resource expansion and mine life extension that could substantially enhance the project's value proposition. Williams highlighted the company's strategic approach:

"There is ample opportunity to grow the resource further at Rowan along strike, at depth, and via discovery at new nearby targets, but we ideally want to do that work while turning this asset into a mine sending high-grade mineralization to an operating mill in the area and potentially generating significant revenue for the Company."

The current resource comprises 26 domains capturing multiple parallel veins, with only three veins included in the PEA mine plan. A fourth vein, v006b, represents the third-largest contributor of tonnes and ounces in the current mineral resource estimate but requires additional drilling to overcome data gaps from historic selective sampling practices.

The 2023 drill campaign demonstrated significant potential for resource expansion, particularly at depth where the highest-grade intercept ever recorded at Rowan returned 70.8 g/t gold over 8.3 meters. This intercept from the deeper portion of vein v001 indicates strengthening mineralization at depth, while the overall vein system remains open for expansion below the current 400-meter definition limit. The deposit also remains open along strike to both the east and west, providing additional expansion vectors.

West Red Lake Gold has identified a comprehensive 3,500-meter drill program targeting both resource upgrade and expansion objectives. Approximately 2,000 meters will focus on upgrading the v006b vein through strategic re-drilling of historic holes and testing expansion targets. The remaining 1,500 meters will target upgrading the 37% of resource tonnes currently categorized as inferred within the existing mine plan. This systematic approach to resource development supports the transition to prefeasibility studies while potentially expanding the economic inventory.

The exploration pipeline extends beyond immediate resource expansion to include new target areas identified through 2024 till sampling programs. Two new till anomalies align spatially with deflections and folding in the main regional shear structure that hosts gold mineralization, representing entirely new discovery opportunities. These targets, including the Apex and Big Bend areas, have received minimal historic drilling and could represent significant value-adding discoveries.

Development Timeline & Regulatory Pathway

West Red Lake Gold has established a clear development timeline that balances thorough engineering and environmental assessment with expedited project advancement. The company plans to complete a Pre-Feasibility Study by Q3 2026, providing the detailed engineering and economic analysis necessary for final investment decisions. Williams outlined the company's systematic approach:

"We plan to advance engineering work while completing a drill program to infill gaps that prevented parts of the resource from being considered in the mine plan and upgrade roughly 37% of the mine plan tonnes that currently sits within the inferred resource category. That work will inform and maximize the value outlined in a PFS that we target issuing within 12 months that would be completed in tandem with permitting efforts at Rowan."

This timeline aligns with ongoing baseline environmental data collection, now in its final year of a three-year program, and regulatory engagement designed to support an expedited permitting process.

The regulatory environment presents favorable conditions for project advancement. Ontario's new Bill 5 legislation specifically targets mining approval process acceleration, creating potential for collaborative and expedited permitting. Williams noted the positive regulatory developments:

"It is also positive that the recent enactment of Bill 5 in Ontario creates potential for a simplified, collaborative, and expedited permitting process."

West Red Lake Gold has initiated engagement with regulators and Indigenous partners to establish the groundwork for efficient permit processing and construction authorization. This proactive approach to stakeholder engagement and regulatory compliance positions the project for smooth advancement through the approval process.

The development strategy emphasizes simultaneous advancement of multiple workstreams to optimize project timelines. Engineering work will proceed in parallel with the planned drill program to infill resource gaps and upgrade inferred resources to indicated status. This integrated approach ensures that PFS-level engineering incorporates the most current geological understanding while maintaining development momentum. The company's experience with permitting and operating the Madsen Mine provides valuable institutional knowledge that supports efficient regulatory navigation for the Rowan Project.

Financial Performance & Sensitivity Analysis

The PEA financial analysis demonstrates robust returns across multiple gold price scenarios, with particular strength in higher price environments that reflect current market conditions. The base case scenario utilizing $2,500 per ounce gold pricing generates total revenue of $593.9 million over the five-year mine life, with cumulative post-tax net cash flow of $155.1 million. Operating costs of $213.6 million and sustaining capital of $102.6 million support a life-of-mine cash cost of $963 per ounce and all-in sustaining costs of $1,408 per ounce.

The project's sensitivity to gold prices provides substantial upside potential for investors. A 15% increase in gold prices to $2,875 per ounce lifts the post-tax NPV to $176 million with an IRR of 50.5%. At $3,250 per ounce gold pricing, closer to current spot prices, the NPV reaches $239 million with an IRR of 66.6%. This sensitivity profile demonstrates how the project's economics improve dramatically with higher gold prices, providing natural hedge value in inflationary environments.

Annual cash flow generation varies with grade distribution throughout the mine plan, ranging from strong Year 1 performance of $45.3 million pre-tax cash flow to peak Year 5 generation of $95.9 million. The average annual free cash flow of $39.6 million provides substantial returns on the initial $70.4 million investment, with a discounted payback period of 2.4 years. This rapid capital recovery timeline reduces investment risk while providing early returns to shareholders.

Key Takeaways for Investors

West Red Lake Gold's Rowan Project PEA represents a compelling opportunity for investors seeking exposure to high-grade gold production with strong economic returns and significant growth potential. The combination of exceptional grades averaging 8.0 g/t gold, low capital requirements of $70.4 million, and robust financial returns with 41.9% IRR creates an attractive investment proposition in the current gold market environment. The project's strategic position in the proven Red Lake Gold District, combined with the company's operational experience and regional infrastructure advantages, supports successful development and operation.

The PEA demonstrates how thoughtful mine planning and strategic toll milling arrangements can unlock value from high-grade deposits while minimizing capital intensity and development risk. With 63% of mined tonnes and 72% of ounces from indicated resources, the project provides a solid foundation for advancement to prefeasibility studies and eventual production. The significant exploration upside, including depth extension potential, parallel vein development, and new target discovery opportunities, offers additional value creation beyond the current mine plan.

For investors, the Rowan Project represents West Red Lake Gold's pathway to becoming a multi-mine operator in one of the world's premier gold districts. The project's strong economics, expedited development timeline targeting Q3 2026 PFS completion, and substantial sensitivity to gold prices position it as a valuable asset in the company's portfolio. Combined with the existing Madsen Mine operations and extensive regional land position, Rowan strengthens West Red Lake Gold's long-term growth trajectory and establishes the foundation for sustained production growth in the high-grade Red Lake Gold District.

Analyst's Notes

Subscribe to Our Channel

Stay Informed