What the Incoming U.S. Government Term Means for Oil Producers and Investors

Donald Trump's re-election in 2024 is set to bring major deregulation for the U.S. oil industry, but production may not surge as markets remain soft.

- Donald Trump's re-election in 2024 is expected to bring a major rollback of environmental regulations and restrictions on the U.S. oil and gas industry put in place under the Biden administration. Trump has vowed to abolish emissions rules, expand drilling access, speed up pipelines and export terminals, and repeal Biden's corporate tax hikes and climate legislation.

- Oil and gas executives and lobbyists strongly support Trump and are eagerly anticipating the deregulatory push, but analysts caution that U.S. production is unlikely to surge significantly higher during his second term due to continued capital discipline by companies and weak global demand.

- If OPEC follows through with plans to increase supply and consumption remains sluggish, especially in China, it could push prices lower, which would benefit consumers but hurt U.S. shale producers. Trump has shown a willingness to intervene in oil markets to manage prices by pressuring OPEC.

- Beyond deregulation, reforming the slow and convoluted federal permitting process for new oil and gas infrastructure is a top policy priority for the industry.

Major Deregulation for the U.S. Oil Industry

The election of Donald Trump to a second term as U.S. President in 2024 is expected to usher in a period of significant deregulation for the oil and gas industry. During his campaign, Trump vowed to slash environmental rules and restrictions in order to unshackle U.S. oil producers and drive up domestic production. His victory is seen as a major boon by industry executives who poured money into his campaign and are now eagerly awaiting the rollback of regulations put in place under the Biden administration.

Trump's Energy Plans

Trump has pledged to abolish rules on vehicle emissions, expand oil and gas leasing on public lands and in offshore waters, weaken endangered species protections, and greenlight new LNG export terminals. He also plans to eliminate the corporate tax hikes and climate provisions in Biden's signature Inflation Reduction Act, although some in the industry actually benefit from that legislation and are lobbying to keep parts of it intact.

To spearhead his "drill, baby, drill" energy agenda, Trump is considering appointing North Dakota Governor Doug Burgum to a new "energy czar" role that would coordinate the deregulatory push across multiple government agencies. "We have more liquid gold than any country in the world—more than Saudi Arabia," Trump declared in his victory speech, signaling his intent to unleash U.S. oil production. (According to sources, America’s oil reserves are actually only one-fifth the size of Saudi Arabia’s.)

Industry Reaction

Oil and gas executives and lobbyists expressed delight at Trump's victory and the expected regulatory relief to come:

"I couldn't be more thrilled by president-elect Donald Trump's victory," said Harold Hamm, founder of Continental Resources and a major Trump donor. "This is a monumental win for American energy and the future of our nation's security."

Jeff Miller, CEO of oilfield services giant Halliburton, was also optimistic.

"It could only be positive. In fact, I'm quite optimistic," Miller said regarding Trump's re-election.

The American Petroleum Institute, the industry's top lobbying group, said it looked forward to the reversal of Biden's "regulatory onslaught" of the past four years.

Production & Price Outlook

Despite the anticipation of a major deregulatory push under Trump, analysts caution that U.S. oil output is unlikely to surge significantly higher during his second term. Domestic crude production already hit record levels under Biden, reaching 13.4 million barrels per day in August 2024, as high prices incentivized drilling. But going forward, investor pressure on oil companies to prioritize returns and capital discipline over production growth is expected to restrain activity.

"Price and Wall Street are the regulators of US production, not the president," said Jim Burkhard, head of oil market research at S&P Global.[3]

The firm expects U.S. output to average 13.2 million bpd in 2024, rising to 13.6 million bpd in 2025 before potentially dipping in 2026. Trump's re-election hasn't changed that near-term forecast.

Sluggish demand in China and plans by the OPEC+ group to increase supply could further weigh on prices in the months ahead.

"The market is oversupplied because the Chinese economy is not delivering the kind of demand that it has in the past," said energy historian Daniel Yergin. "That is the biggest overhang for the global and US oil industry."[3]

Although Trump has limited ability to impact pump prices near-term, a large increase in global supply relative to demand could send prices lower during his term. That would please drivers but hurt U.S. shale producers. Still, Trump has not shied away from intervening in oil markets, jawboning OPEC to adjust production to manage prices in his first term.

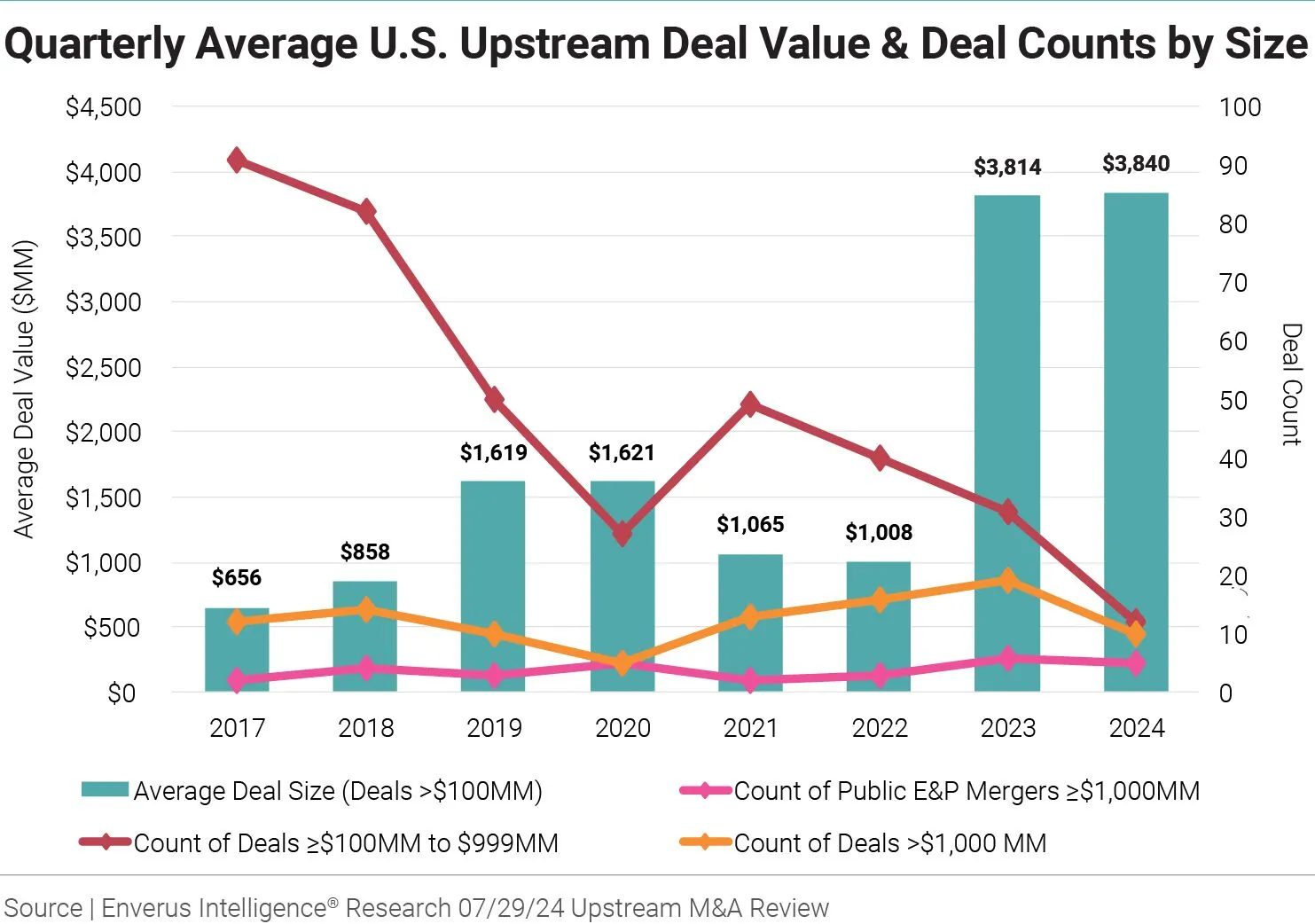

Continued M&A Momentum

The elevated level of oil and gas M&A activity seen in 2023 continued into the second quarter of 2024, with 285 deals announced worth a total of $62.1 billion. While deal value decreased 23% compared to Q1, volume increased 7%, indicating sustained momentum. The largest transaction was ConocoPhillips' $22.5 billion acquisition of Marathon Oil in May. Foreign direct investment accounted for a third of Q2 deal activity, a notable 20% uptick from the prior quarter.

While 2023's M&A wave was fueled by oil majors' record cash flows and a drive to boost reserves, 2024 is seeing a shift in deal motivations. With oil prices settling into a $65-85/bbl range, buyers are prioritizing assets with competitive supply costs and greater access to capital. The industry appears to be consolidating to create fewer, larger, more efficient companies better positioned for an evolving energy mix. Deals like the Chesapeake-Southwestern merger exemplify this trend, touting synergies, increased scale, and a lower cost of supply as key benefits. Gaurav Sharma, Energy Market Analyst and Senior Contributor for Energy Connects, described the implication of M&A deals last year versus the year:

"Evidence suggests this elevated level of M&A activityhas continued well into 2024. However, the motivation for deals appears to be alittle different given the market realities this year has thrown up for both buyers and sellers alike" [2]

"Even if deal valuations don’t quite match 2023 levels, expect further consolidation this year with similar offers to stakeholders stretching well into 2025. This may be particularly true of the US market, assub-$80 oil prices bring many to the negotiating table." [2]

Regulatory Priorities

Beyond deregulation, the oil industry's top policy priority under a second Trump administration will likely be overhauling the convoluted federal permitting process for new pipelines and infrastructure. Previous reform efforts failed, but Republican control of Congress could provide an opening.

"The expectation that they will be reducing emissions and investing in clean energy does not go away because Donald Trump was elected," said Paul Bledsoe, a former climate advisor in the Clinton administration. "That's a public expectation. That's an investor expectation."[3]

Investment Opportunity

is crucialThe global energy landscape is undergoing a significant transformation, with an increasing focus on renewable sources and decarbonisation. However, the oil and gas sector plays a crucial role in meeting the world's energy needs. Shell sees growth opportunities in LNG and in optimising integrated trading operations across various energy products.

"We are an active part of the energy transition, and we are very bullish on LNG. We believe LNG is a fantastic transition fuel and will continue to play an increasing role in the energy system." - Andreas Bork, Senior Investor Relations at Shell explains.

Shell Plc

Shell's strong stock performance since the March 2020 crash, returning to 2017-2019 levels, was due to both favorable industry conditions and company-specific factors. The economic recovery and geopolitical issues have boosted the sector, while Shell has also made operational improvements.

Elixir Energy, Empire Energy, and Trillion Energy are two ASX-listed junior exploration and production companies focused on developing unconventional and conventional resources in Australia and Turkey.

Elixir Energy

Elixir Energy (ASX:EXR) is an ASX-listed junior exploration company focused on developing a large unconventional gas resource in the Bowen Basin of Queensland, Australia. The company recently completed an extensive appraisal drilling program that provided mixed results but valuable data that Elixir believes will be attractive to potential farm-in partners. While the final well flow rates were lower than expected, the company remains confident in the geological potential of its acreage.

Elixir benefits from a highly favorable macro backdrop, with Queensland gas prices trading around A$12-15/GJ, a significant premium to global benchmarks. This structural pricing support provides insulation from weak international markets and enhances the economics of new supply developments. Elixir's key near-term catalysts include securing a major farm-in partner to fund further appraisal drilling and potentially monetizing its nearby conventional gas prospect or Mongolian coal bed methane asset.

Trillion Energy

Trillion Energy is a Turkish-focused oil and gas producer that has faced recent challenges with its offshore gas field due to water loading issues. The company has implemented a solution by installing smaller velocity strings in its wells, which has stabilized production at 2-2.5 MMcf/d per well. This has allowed Trillion to generate $1-2M/month in revenue, which it plans to use for debt reduction and low-cost growth initiatives.

The company has identified several low-cost well recompletion and sidetrack opportunities that could boost output to 10-14 MMcf/d and generate $25M/year in revenue. Additionally, Trillion sees significant upside potential in Turkey's under-explored oil and gas basins, with a prospective farm-in opportunity on a billion-barrel prospect.

Empire Energy

Empire Energy (ASX:EEG) has assembled a dominant 3 million net acre position in the core of the play and recently reported encouraging appraisal drilling results that suggest the reservoir properties are analogous to the prolific Marcellus Shale in the US. With an estimated 47 TCF of prospective resources, Empire's acreage could support decades of drilling inventory. A key differentiator for Empire is the highly favorable macro setup, with Australian East Coast gas prices trading at a substantial premium to the US due to declining conventional supply and growing LNG export demand. This provides downside protection and should enhance the economics of future development. Empire is targeting first production from its Carpentaria pilot project in 2025.

For investors, Elixir Energy, Trillion Energy and Empire Energy represent high-risk, high-reward bets on successfully cracking the code to a large, unconventional resource play. Elixir and Empire has a more favorable macro setup with Queensland gas prices trading around a significant premium to global benchmarks, while Trillion offers more near-term cash flow and production growth. Both stocks are likely to be driven by news flow around drilling results and farm-out deals in the near-term.

Conclusion

Donald Trump's re-election in 2024 is expected to usher in a period of significant deregulation for the U.S. oil and gas industry, as he has pledged to roll back environmental rules, expand drilling access, expedite pipelines and export terminals, and repeal President Biden's corporate tax hikes and climate legislation. Oil executives and lobbyists, who strongly supported Trump's campaign, are eagerly anticipating this deregulatory push and the gutting of Biden's climate policies.

However, despite the favorable regulatory outlook under Trump, U.S. crude oil production is unlikely to surge significantly higher during his second term, as oil companies remain under investor pressure to maintain capital discipline and limit spending on new drilling. Weak global demand, especially in China, and the potential for OPEC to increase supply could also weigh on prices and production. Nonetheless, the oil and gas industry sees potential for other policy victories beyond just deregulation, particularly in the area of permitting reform, which could gain traction with Republicans in control of both the White House and Congress. Still, large oil companies will continue to face pressure from investors and the public to reduce emissions and invest in clean energy, regardless of the administration's policies.

As a key supplier of equipment and services to oil and gas producers, Halliburton's fortunes are closely tied to the level of drilling and completion activity. If the removal of Biden-era regulations and restrictions leads to an uptick in production, even a modest one, Halliburton would see increased demand for its services. The company could also potentially benefit from expanded drilling on federal lands and offshore waters.

However, Halliburton's outlook will also depend on the trajectory of global oil prices and demand. If OPEC+ follows through with plans to increase supply and consumption remains sluggish, particularly in China, it would weigh on prices and drilling activity. Halliburton will also still face pressure from its oil company customers to keep service costs low, even in a more favorable regulatory environment.

The Investment Thesis for Oil & Gas

- Bet on deregulation: Expect the Biden administration's climate policies and drilling restrictions to be aggressively rolled back under Trump, creating a more favorable operating environment for oil and gas companies.

- Pick potential winners: Favor producers with prime acreage in areas like the Permian Basin that are set to benefit from expanded drilling access on federal lands. Oilfield services firms also stand to gain from any increase in activity.

- Monitor OPEC and demand: Keep a close eye on OPEC production plans and the pace of demand recovery, especially in China. Stubbornly high supply and weak consumption could continue to pressure prices.

- Expect capital discipline to reign: Despite the deregulatory tailwind, don't count on a return to the drill-at-will mentality of the past. Companies will remain under investor pressure to limit production growth and spending.

- Position for permitting reform: Besides deregulation, permitting reform is the industry's other big policy goal that could gain traction under united Republican control of Washington. Pipeline owners and operators could benefit from a streamlined approval process.

Donald Trump's return to the White House is undoubtedly a positive development for the U.S. oil and gas industry, which chafed under the Biden administration's climate and environmental policies. A second Trump term promises a broad deregulatory push that will likely make it easier and cheaper for companies to drill, build pipelines, and export their products.

However, the impact may not be as seismic as Trump's "drill, baby, drill" rhetoric suggests. U.S. oil production already hit record levels under Biden, and going forward, companies will remain constrained by investor demands to limit spending, even if regulatory roadblocks are removed. The industry's fortunes will also largely hinge on factors outside Trump's control, like OPEC production decisions, the strength of the Chinese economy, and the pace of post-pandemic demand recovery.

So while oil and gas companies can certainly expect a more hospitable policy environment, the production boom of the early shale era is unlikely to be repeated. Instead, the industry's focus under Trump is likely to be locking in structural policy changes, like permitting and leasing reform, that could reap long-term benefits beyond any one administration. For investors, selective bets on well-positioned producers and servicers could pay off if activity picks up, but caution is still warranted given the uncertain global supply-demand balance and the rising specter of peak demand.

References:

- GlobalData (November 2024). Oil & Gas: Filings Trends & Signals Q2 2024

- Sharma, G. (September 2024). Energy Connects' Opinion Thought Leadership. Oil and gas M&A activity appears buoyant in 2024 as crude prices dip

- McCormick, M., Smyth, Jamie (November 2024). Financial Times. US oil industry eagerly awaits Donald Trump’s deregulatory push

- Lawler, A. (November 2024). Reuters. OPEC again cuts 2024, 2025 oil demand growth forecasts

- Groom, N. (November 2024). Reuters. Trump picks oil-industry CEO Chris Wright as energy secretary nominee

- Crux investor (October 2024). Oil & Gas Giants: Cash Flow Kings in the Energy Transition

Analyst's Notes

Subscribe to Our Channel

Stay Informed