What You Need to Understand About the Nuclear Sector Before You Invest in Uranium - Part 3

Uranium demand exceeds 1B lbs post-2027 as utilities shift to long-term contracts. Efficiency gains, jurisdictional premiums, and supply tightness drive investment thesis.

- Uncommitted and uncovered reactor demand is rising sharply, underscoring future supply tightness as utilities extend procurement horizons.

- Efficiency drivers (capacity factors, cycle lengths, burn-up rates) alter near-term uranium needs but cannot offset structural long-term growth.

- Procurement strategies are shifting from spot exposure to long-term contracts, with tails assay dynamics linking uranium and enrichment costs.

- Developers and producers with Tier-1 assets in stable jurisdictions, Canada, U.S., Niger, are best positioned to capture pricing leverage.

- Companies such as Energy Fuels, IsoEnergy, enCore Energy, ATHA Energy, and Global Atomic demonstrate how scale, jurisdiction, and balance sheet strength intersect with macro uranium demand trends.

Rising Reactor Requirements & the Forward Demand Curve

Global uranium demand is fundamentally tied to reactor requirements, calculated through a methodology developed by the World Nuclear Association that multiplies reactor capacity by fuel cycle parameters. This framework provides forward visibility into structural demand; however, the input variables, capacity growth, operational efficiency, and cycle length, introduce meaningful variability that investors must track closely.

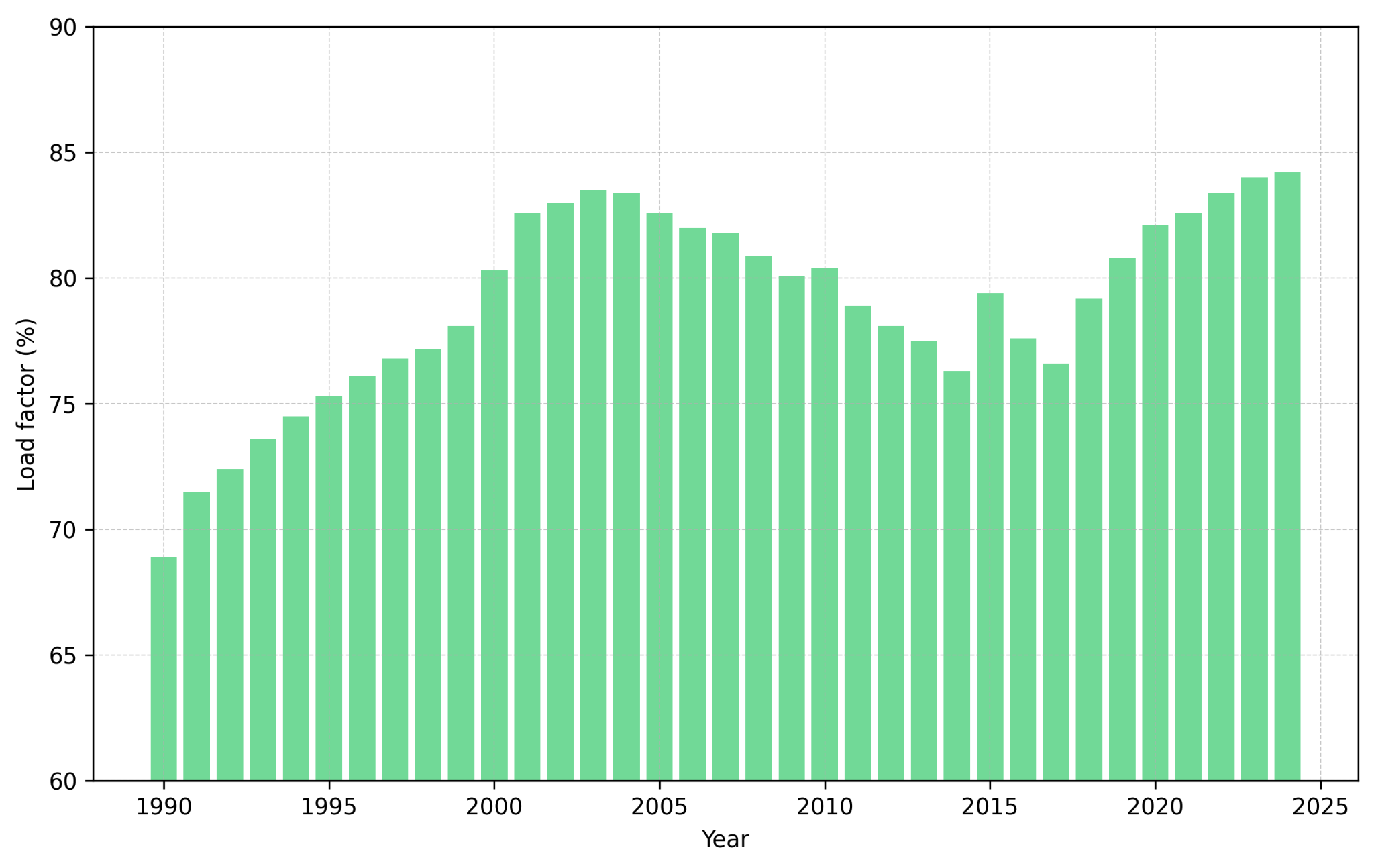

Operational efficiency has improved materially over the past three decades. Global capacity factors, the ratio of actual output to maximum possible output, have risen from 69% in 1990 to over 80% today in many OECD markets. Higher capacity factors increase uranium consumption per reactor, as units operate closer to full capacity throughout the year. Similarly, cycle length extensions, which allow reactors to operate longer between refueling outages, increase uranium consumption by 8% to 18% depending on design specifications. These efficiency gains do not reduce uranium demand; they amplify it. The investment implication is clear: forward demand curves that incorporate capacity growth and efficiency improvements reveal structural supply deficits that widen significantly after 2027. Utilities must contract years in advance to secure supply, creating opportunities for developers with near-term production timelines and producers with licensed capacity.

The Procurement Shift: From Spot Reliance to Contract Rebuilding

Utility procurement strategies have undergone a fundamental reassessment following the uranium price volatility of 2022-2024. Historically, utilities balanced cost minimization with security of supply by maintaining a mix of spot purchases and long-term contracts. However, the post-Fukushima era saw a secular decline in contracting activity, with many utilities opting for spot exposure as prices remained depressed. That calculus has reversed. The majority of global uranium consumption is now shifting back toward multi-year contracts, driven by recognition that spot markets lack sufficient depth to support reliable fuel supply.

This transition is visible in the term-spot pricing disconnect: while spot prices remain volatile, term prices have established a higher floor, reflecting utilities' willingness to pay for supply certainty. This bifurcation has direct implications for equity valuations, as companies with contracted production command premium multiples relative to those dependent on spot sales. Energy Fuels, as the largest conventional uranium producer in the United States, operates licensed production capacity exceeding 10 million pounds annually across multiple facilities, including the White Mesa Mill in Utah. This infrastructure provides U.S. utilities with near-term security of supply at a time when domestic production accounts for less than 10% of annual consumption.

IsoEnergy's toll milling agreement with Energy Fuels demonstrates the flexibility that contracted capacity provides. The agreement allows IsoEnergy to process future production from its Larocque East project through Energy Fuels' licensed facilities, reducing permitting risk and accelerating time-to-market. This model indicates how near-term production optionality is increasingly valued in a market where utilities are extending procurement horizons and seeking North American supply sources. The procurement shift is not merely a function of price, it reflects a structural reassessment of supply chain risk.

Uncommitted & Uncovered Demand

Uncommitted demand refers to reactor requirements not yet covered by utility contracts, while uncovered demand represents the subset of uncommitted demand that exceeds identified supply. Both metrics are critical forward indicators for uranium pricing and investment opportunities. Near-term demand appears stable, with most utilities holding sufficient inventory and contracts, consistent with the observation that uncommitted and uncovered demand typically approach zero in the very short term. However, the demand curve widens dramatically post-2027, creating a structural supply gap that exceeds 1 billion pounds over the subsequent decade.

This widening gap reflects two dynamics: capacity additions and contract expiration. New reactors coming online in China, India, and the Middle East require incremental uranium supply, while existing reactors in OECD markets face contract rollovers at a time when supply optionality has diminished. The result is a forward market where utilities must contract years in advance, often at prices that reflect long-term supply scarcity rather than current spot dynamics.

The United States faces a particularly acute uranium supply challenge that creates strategic vulnerabilities and investment opportunities. Stephen Roman, President and Chief Executive Officer of Global Atomic, quantifies the deficit:

"They're burning 50 million pounds a year, they're making with everything ramped up four or five million pounds a year in the United States."

Global Atomic's Dasa project in Niger is advancing toward first production in the first quarter of 2026, with scale and grade, 6 million pounds per year at fully ramped rate, making it one of the most significant new uranium sources globally. The project represents the type of large-scale supply addition necessary to address uncovered demand in the 2028-2035 window. enCore Energy's in-situ recovery restart in South Texas demonstrates the operational leverage available to producers that can accelerate production timelines. The company has reduced average well completion time, allowing daily production rates to increase by 200% to 300%. This speed-to-market advantage positions ISR operators to capture near-term contracting opportunities as utilities seek to cover uncovered demand.

Efficiency Gains & Technical Drivers of Uranium Demand

Efficiency improvements in reactor operations have material implications for uranium demand, though the directional impact varies by metric. Three primary levers influence consumption: capacity factors, cycle length, and burn-up rates. Understanding how each variable interacts with demand forecasting is essential for assessing the durability of the uranium supply thesis. Capacity factors have improved from 69% globally in 1990 to over 80% in many OECD markets today, reflecting advances in reactor reliability, maintenance scheduling, and regulatory oversight.

Higher capacity factors increase uranium consumption per reactor, as units operate closer to full output throughout the year. Higher capacity factors increase uranium consumption per reactor. According to sensitivity analysis, raising the capacity factor from the base value of 80% to 85% increases uranium consumption requirements by 6%. Cycle length extension represents a separate efficiency lever. By extending the interval between refueling outages, often from 18 months to 24 months, utilities reduce operational downtime and increase capacity utilization. However, longer cycles require higher initial fuel loads, increasing uranium consumption per cycle by 8% to 18% depending on reactor design.

Burn-up rates, which measure the amount of energy extracted per unit of uranium fuel, have increased through advances in fuel fabrication and enrichment. Higher burn-up rates reduce the quantity of fresh fuel required per cycle, creating a marginal decrease in uranium demand. Increasing burn-up by 5 GWd/tU reduces uranium requirements by 3%.

ATHA Energy's exploration strategy in Canada's uranium-rich basins targets high-grade discoveries capable of supplying incremental demand as reactors optimize fuel cycles. The company's recent drilling success demonstrates the district-scale potential in underexplored Canadian basins. Troy Boisjoli, Chief Executive Officer of ATHA Energy, describes the exploration momentum:

"This is our fourth discovery in one single drill program within that Angikuni Basin… RIB in particular now has conductive corridors that are mineralized over 12 kilometers."

IsoEnergy's Hurricane deposit highlights how high-grade assets maintain strategic value across demand scenarios. High-grade deposits, Hurricane averages over 20% U3O8 in its high-grade zone, are less sensitive to demand swings driven by efficiency optimization, as they represent the lowest-cost supply on the global cost curve.

The long-term supply dynamics in Saskatchewan underscore the strategic value of high-grade discoveries as existing mines deplete. Philip Williams, Director and Chief Executive Officer of IsoEnergy, frames the timeline:

"Hurricane will be a mine in the Athabasca basin… Cigar Lake will run out of ore by 2035… It's more valuable the longer we hold on to it."

The stress-test conclusion is clear: efficiency gains moderate near-term demand variability but cannot offset the structural growth driven by capacity additions and operational optimization.

Tails Assay Selection & the Price Link Between Uranium & Enrichment

Tails assay selection represents a technical but strategically important variable in uranium demand forecasting. During enrichment, uranium is processed to increase the concentration of U-235, the fissile isotope required for reactor fuel. The "tails assay" refers to the U-235 concentration remaining in the depleted uranium byproduct. A lower tails assay, such as 0.22% rather than 0.25%, extracts more U-235 from the same quantity of natural uranium, reducing uranium feed requirements by approximately 6%.

This operational lever allows utilities to adjust uranium consumption based on the relative cost of uranium and enrichment services. When uranium prices are high relative to enrichment, utilities optimize for lower tails assays, reducing uranium demand but increasing enrichment demand. Conversely, when enrichment costs rise, utilities accept higher tails assays, increasing uranium consumption but reducing enrichment requirements. This dynamic introduces volatility into uranium demand forecasting, particularly during contracting cycles when utilities reassess fuel procurement strategies.

The investor implication is twofold. First, tails assay optimization creates short-term demand variability that can decouple spot uranium prices from underlying reactor requirements. Second, companies with operational flexibility across multiple inputs, uranium, rare earth elements, enrichment services, are better positioned to respond to relative price shifts. Energy Fuels scores this optionality through its production capabilities at the White Mesa Mill, which processes uranium, vanadium, and rare earth elements. The enrichment-uranium price relationship also intersects with geopolitical supply chain dynamics. Western enrichment capacity remains constrained, with significant reliance on Russian supply through TENEX despite ongoing trade restrictions. As Western governments invest in domestic enrichment capacity, the relative cost structure may shift, influencing utility tails assay decisions and uranium demand.

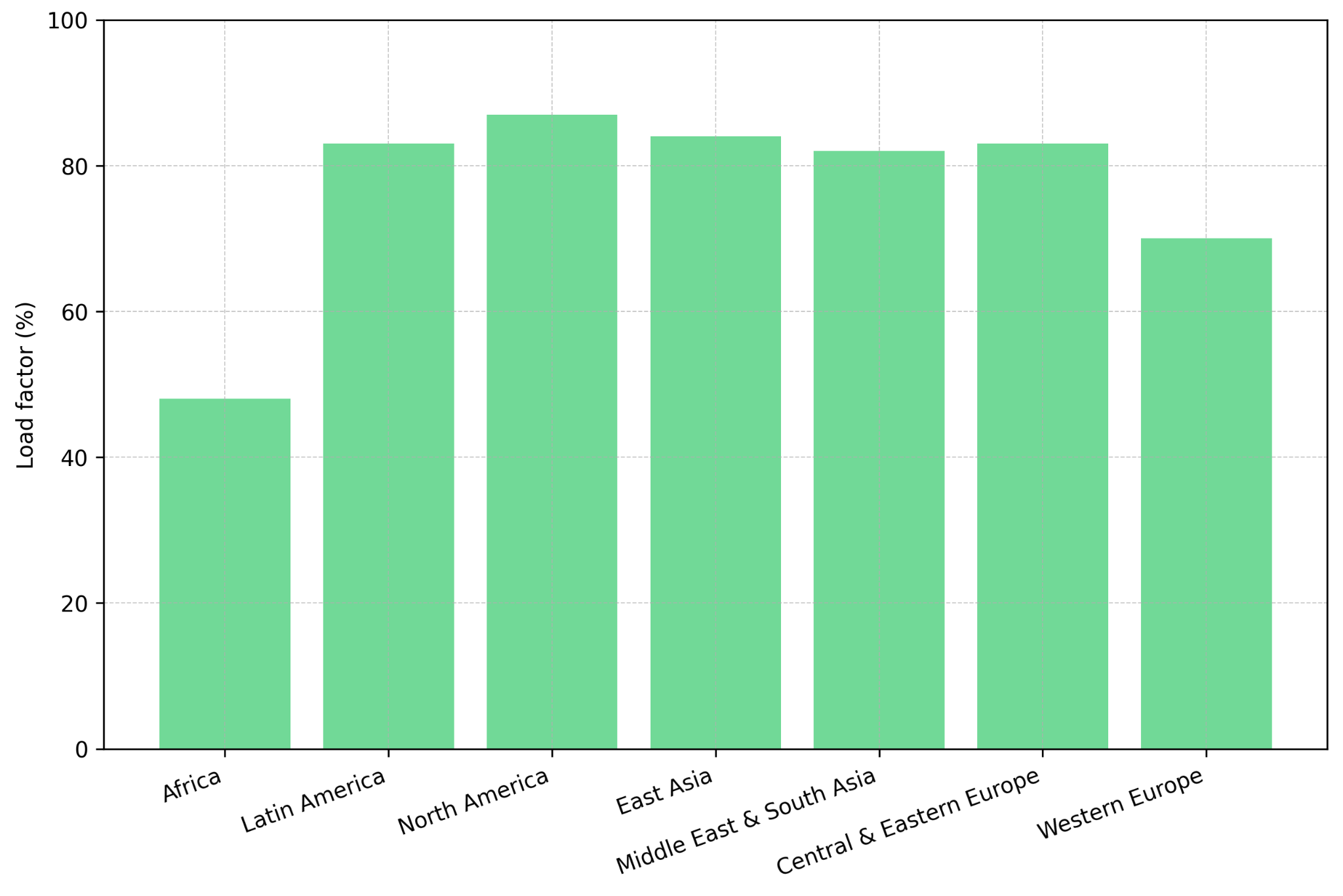

Jurisdictional Risk & Policy Shifts in Nuclear Supply Chains

Jurisdictional risk has emerged as a primary determinant of valuation for uranium developers and producers. The geopolitics of nuclear fuel supply are bifurcating markets, with Western utilities increasingly prioritizing supply sources in allied jurisdictions, Canada, the United States, Australia, over historically significant producers in regions with heightened political risk. Niger represents a case study in jurisdictional complexity. The country has historically been a major uranium supplier, but military coups, government transitions, and nationalization risks have created financing and operational challenges for projects in the region.

Global Atomic's Dasa project has navigated these challenges through engagement with multilateral development banks and direct outreach to U.S. policymakers. The project's advancement reflects both the strategic importance of new supply sources and the complexity of operating in jurisdictions with elevated political risk. U.S. policy is accelerating domestic nuclear fuel independence through direct Department of Energy support for ISR projects and enrichment capacity expansion. The FAST-41 permitting framework, which provides coordinated federal review and transparent timelines, has become a critical tool for de-risking U.S. uranium projects.

Laramide Resources has secured FAST-41 designation for its Church Rock project in New Mexico, one of the largest known ISR deposits under single project control with Nuclear Regulatory Commission permitting. Marc Henderson, President and Chief Executive Officer of Laramide Resources, emphasizes the permitting certainty provided by the framework:

"We applied and got involved in FAST-41… The current administration is totally receptive... It's encouraging that a government is telling you the schedule on which you're going to get permitted."

The project's scalability, starting at 1 million pounds annually and expanding to 3 million pounds, positions it to serve long-term utility contracting needs as domestic supply becomes increasingly prioritized. enCore Energy operates two licensed plants while building a pipeline of permitted projects across multiple states, demonstrating the strategic value of operational readiness in a contracting-driven market.

William Sheriff, Chief Executive Chairman of enCore Energy, underscores the competitive advantage of operational capacity and permitting progress:

"We're the only company out there that has two plants that are operational. Our South Dakota project got FAST-41, which cuts timelines dramatically and increases certainty."

Canada remains the Tier-1 jurisdiction for high-grade uranium assets, with Saskatchewan's Athabasca Basin hosting the world's richest deposits. Regulatory stability, transparent permitting, and established infrastructure make Canada the preferred jurisdiction for institutional investors and strategic acquirers.

The strategic importance of Canadian supply to U.S. utilities cannot be overstated, particularly as domestic production remains insufficient to meet consumption. Dev Randhawa, Chairman and Chief Executive Officer of F3 Uranium, articulates this structural dependency:

"The grades in the Athabasca will always be the best... No matter what they do in the U.S., I don't believe they're ever going to produce 50 million pounds. They still need uranium from Canada. They can't avoid it."

F3 Uranium's exploration strategy in the Athabasca Basin leverages proven management's track record of discoveries and exits, with the team having previously discovered and sold assets to Cameco and Paladin Energy. Jurisdictional premiums are now embedded in equity valuations, with Canadian and U.S. developers trading at materially higher multiples than peers in regions with heightened political risk. This premium reflects not only permitting certainty but also access to capital, offtake partnerships, and strategic M&A optionality.

Scale, Grade & Conventional Mining Economics

The uranium supply response is not solely defined by jurisdiction, deposit scale and mining method introduce material variability in project economics and development timelines. Conventional mining projects, which extract uranium through open-pit or underground operations followed by heap leaching or milling, offer distinct advantages in specific geological settings. These projects typically require higher initial capital expenditures than ISR operations but can access deposits in fractured basement rock where in-situ recovery is not technically feasible.

Scale matters for attracting both utility offtake and project financing. Deposits exceeding 10 million pounds in stable jurisdictions provide sufficient inventory life to support multi-decade utility contracts, while projects in the 8 million to 10 million pound range offer strategic value as satellite operations to existing processing infrastructure. American Uranium is advancing domestic projects with a focus on scaling resources toward economic thresholds that attract development capital.

Bruce Lane, Executive Director and Chief Executive Officer of American Uranium, frames the near-term exploration objective:

"We've ended up with 8.57 million pounds, 32% of that is indicated… If we can get it past 10 million pounds, that'll be a nice outcome for this year."

Strategic partnerships with established producers provide operational credibility and potential toll milling pathways for developers lacking processing infrastructure. The conventional mining model also provides optionality in districts where ISR geology is marginal, allowing developers to access uranium in fractured basement rock or low-permeability formations.

Myriad Uranium's Copper Mountain project in Wyoming shows the scale potential of conventional uranium deposits in the United States, with historical resource estimates ranging from 15 million to 30 million pounds. Recent reinterpretation of historical data using modern analytical techniques has materially improved grade estimates. Thomas Lamb, Chief Executive Officer of Myriad Uranium, describes the impact of data reanalysis:

"Our Copper Mountain project in Wyoming has historical resources of 15 to 30 million pounds… The U.S. Department of Energy said 200 million pounds in 1983… Anything over 1,000 parts per million we got a 60% boost, anything over 500 parts per million we got a 50% boost."

The substantial grade reinterpretation reflects advances in analytical methodology and data processing since the original assessments were completed. Large-scale conventional deposits offer long inventory life and strategic value in supply chains increasingly focused on North American sources.

Financial Health & Strategic Positioning Across Developers & Producers

Balance sheet strength defines which companies can capture the upcoming procurement cycle. In a capital-intensive sector where development timelines span multiple years and permitting risk remains elevated, financial capacity determines execution capability. Companies with strong cash positions, strategic equity stakes, and access to debt markets are best positioned to advance projects through feasibility studies, permitting, and construction without dilutive equity raises.

IsoEnergy demonstrates the strategic value of financial strength and institutional backing through C$84.7 million in cash and a 30.9% equity stake from NexGen Energy. This capital position funds exploration across multiple Saskatchewan projects while providing optionality to advance Hurricane toward feasibility. ATHA Energy's enterprise value of approximately C$260 million reflects a fully funded exploration program with near-term catalysts across four discovery zones. The company's financial positioning allows for aggressive drilling campaigns without immediate capital-raising requirements, reducing execution risk and maintaining shareholder alignment.

Energy Fuels operates the largest conventional uranium production capacity in the United States, exceeding 10 million pounds annually, alongside rare earth element production and vanadium optionality. This diversified revenue base provides cash flow optionality that development-stage companies lack. enCore Energy's recent debt financing underscores the improving capital markets environment for near-term producers. The company raised $115 million through a non-secured note offering with a 5.5% coupon, significantly below historical cost of capital for junior uranium producers. Balance sheet strength is not merely a defensive attribute, it is an offensive tool for capturing market share, securing offtake agreements, and executing mergers and acquisitions strategies. As the uranium sector consolidates and utilities prioritize supply security, companies with financial capacity and operational track records will outperform peers dependent on equity markets for growth capital.

The Investment Thesis for Uranium

The structural case for uranium investment rests on the intersection of supply tightness, procurement cycle dynamics, and jurisdictional premiums. The following factors define the investment framework for producers and developers positioned to capture value from the current cycle:

- Uncommitted and uncovered reactor demand exceeds 1 billion pounds post-2027, creating structural pricing leverage for new supply sources as utilities extend procurement horizons to secure long-term fuel contracts.

- The shift from spot exposure to long-term contracting underpins price stability and revenue visibility for low-cost producers with licensed capacity and established utility relationships in key markets.

- Efficiency gains and enrichment-uranium price dynamics introduce short-term demand volatility but do not offset the long-term growth trajectory driven by capacity additions and operational optimization across the global reactor fleet.

- Jurisdictional security elevates valuation premiums for Canadian and U.S. suppliers as Western utilities prioritize supply chain resilience and reduce dependence on geopolitically sensitive sources.

- Balance sheet strength and near-term catalysts differentiate companies capable of executing production restarts, securing project financing, and advancing developments through permitting without dilutive equity raises.

- High-grade assets in Tier-1 jurisdictions provide the lowest-cost supply on the global curve, offering margin resilience across uranium price scenarios and strategic optionality for long-term value creation.

- Scale matters for attracting utility offtake and development capital, with projects exceeding 10 million pounds offering sufficient inventory life to support multi-decade contracts and strategic partnerships.

- Conventional mining projects provide access to deposits where ISR is not technically feasible, expanding the supply response in fractured basement geology and low-permeability formations.

From Demand Curve to Equity Positioning

The uranium demand curve provides the foundational logic for the current investment cycle: rising reactor requirements, tightening uncommitted supply, and structural supply deficits that widen materially after 2027. These dynamics are not speculative, they reflect the operational realities of nuclear fuel procurement, where utilities must contract years in advance and supply sources require multi-year development timelines. Investors must track three primary variables: procurement cycles, uncovered demand, and jurisdictional shifts.

Procurement cycles are shifting decisively toward long-term contracts, creating revenue visibility for producers and developers with near-term capacity. Uncovered demand represents the forward investment signal, quantifying the supply gap that new projects must fill. Jurisdictional shifts are elevating premiums for Canadian and U.S. assets as Western utilities prioritize supply chain resilience. Companies aligned with these macro currents, Energy Fuels, IsoEnergy, enCore Energy, ATHA Energy, Global Atomic, F3 Uranium, Laramide Resources, American Uranium, and Myriad Uranium, demonstrate how scale, jurisdiction, mining method, and balance sheet strength intersect with demand fundamentals. These companies are not merely exposed to uranium price appreciation; they are positioned to deliver structural value creation through execution, cash flow generation, and strategic positioning in a supply-constrained market. The investment opportunity lies not in predicting uranium prices, but in identifying which companies can convert demand visibility into operational delivery and shareholder returns.

Read more:

Part 2 - Nuclear Energy Security Imperatives

TL;DR

Global uranium demand faces structural tightening as uncommitted reactor requirements exceed 1 billion pounds post-2027. Capacity factors have risen from 69% (1990) to 83% (2024), increasing per-reactor consumption despite efficiency gains in burn-up rates. Utilities are shifting from spot market exposure to long-term contracts, creating pricing leverage for producers with permitted capacity in Tier-1 jurisdictions. Tails assay optimization introduces short-term demand volatility but cannot offset long-term growth driven by reactor additions. U.S. domestic production (4-5 million lbs/year) meets less than 10% of consumption (50 million lbs/year), elevating strategic premiums for Canadian and U.S. suppliers. Companies with balance sheet strength, operational capacity, and jurisdictional security—Energy Fuels, IsoEnergy, enCore Energy, ATHA Energy, Global Atomic, F3 Uranium, Laramide Resources, American Uranium, and Myriad Uranium—are positioned to capture value through execution rather than price speculation.

FAQs (AI-Generated)

Uncommitted demand refers to future reactor fuel requirements not yet covered by utility contracts. Post-2027, uncommitted demand exceeds 1 billion pounds, creating a structural supply gap as utilities must contract years in advance. This forward visibility creates pricing leverage for developers with near-term production capacity and producers with licensed facilities in stable jurisdictions like Canada and the United States.

Contrary to intuition, efficiency gains increase uranium demand. Global capacity factors rose from 69% (1990) to 83% (2024), meaning reactors operate closer to full capacity throughout the year, consuming approximately 30% more uranium at 90% capacity factor versus 70%. Cycle length extensions (from 18 to 24 months) require higher initial fuel loads, increasing uranium consumption by 8-18% per cycle. While burn-up rate improvements marginally reduce fresh fuel requirements, these are more than offset by capacity utilization gains.

Tails assay refers to the U-235 concentration remaining in depleted uranium after enrichment. Lowering tails assay from 0.25% to 0.22% reduces natural uranium requirements by 5.2% but increases enrichment needs by 7.3%. Utilities optimize tails assay based on relative uranium and enrichment costs, creating short-term demand variability. When uranium prices rise relative to enrichment, utilities lower tails assays, temporarily reducing uranium demand. This technical lever decouples spot prices from underlying reactor requirements during contracting cycles.

Jurisdictional risk premiums reflect three factors: permitting certainty, supply chain security, and access to capital. The U.S. FAST-41 framework provides transparent permitting timelines, reducing regulatory uncertainty. Western utilities increasingly prioritize allied jurisdictions (Canada, U.S., Australia) over geopolitically sensitive regions following supply chain disruptions. Saskatchewan's Athabasca Basin hosts the world's highest-grade deposits with established infrastructure. These factors command materially higher equity multiples and attract institutional capital unavailable to developers in higher-risk jurisdictions.

Three criteria define execution capability: balance sheet strength, operational capacity, and jurisdictional positioning. Companies with strong cash positions and strategic backing can advance projects without dilutive equity raises. Licensed production capacity or permitted near-term projects provide immediate contracting optionality as utilities extend procurement horizons. Assets in Tier-1 jurisdictions (Canada, U.S.) offer permitting certainty and strategic value to utilities prioritizing supply security. High-grade deposits and scale (10+ million pounds) provide cost curve advantages and sufficient inventory life for multi-decade utility contracts.

Analyst's Notes

Subscribe to Our Channel

Stay Informed