Cameco Restarts Cigar Lake - A Bullish Signal to the Market?

Restarting Cigar Lake is an exercise in balancing risk – but which risks and what can we learn about Cameco’s market view? Uranium experts Brandon Munro and Malcolm Rawlingson discuss.

Restarting Cigar Lake is an exercise in balancing risk – but which risks and what can we learn about Cameco’s market view? Uranium experts Brandon Munro and Malcolm Rawlingson discuss the impacts on both the sector and you, the investor.

Meet the Experts

Malcolm Rawlingson is a 50 year veteran of the nuclear power business in both the UK and Canada. He holds a Bachelors in Nuclear Engineering from the University of London. He is now CEO of Global Fire Corporation that specialises in the fire protection of nuclear power plants.

Brandon Munro is a uranium market expert and CEO of Bannerman Resources Ltd, which is developing the Etango uranium project in Namibia. He serves as the Co-Chair of the World Nuclear Association’s Nuclear Fuel Demand working group and is an expert contributor on uranium to the UN Economic Commission for Europe.

Cameco Announces the Opening of Cigar Lake

The uranium world is abuzz with Cameco’s announcement that it plans to restart production at Cigar Lake uranium mine in April. This follows a temporary closure at the mine that will impact global 2021 production – and widen this year’s uranium supply deficit – by at least 6 million pounds (Mlbs) U3O8.

Whilst the restart was inevitable, the timing has raised eyebrows given Canada’s Saskatchewan province is reporting the highest new COVID cases in months and Canada’s vaccine roll out is yet to gain real momentum.

The spot price has retracted on the news and equities have pulled back, seemingly on the assumption that the return of this 1.5 Mlbs per month supply source will reduce spot price growth through suppressing Cameco’s spot market demand.

However, uranium is a nuanced business and things are often not what they seem at first sight. We believe there is more to the story given Cameco, known for its carefully measured decisions and an excellent vantage point to the uranium supply chain, will have balanced market dynamics against the risks of restarting too early.

The World's Highest Grade Uranium Mine

Cigar Lake is the world’s highest grade uranium mine and, at annual production of 18 Mlbs, is currently the world’s largest uranium producer representing 13% of global mine supply. The mine is located in Northern Saskatchewan, Canada and is a remote fly-in-fly-out operation with a high proportion of First Nations employees.

Cameco was the first uranium producer to react to the pandemic threat, announcing on 23 March 2020 the temporary suspension of Cigar Lake for four weeks, which was then extended on April 13 for an undetermined period. After losing 6 months of production (around 9 Mlbs) Cigar Lake recommenced production at the beginning of September 2020, about two weeks after recommencing full operations at the site.

When Cameco announced on 14 December 2020 that Cigar Lake would be suspended for the second time, there had only been a handful of cases on site and all of Cameco's COVID-19 protocols were working well. However, Cameco was concerned that a lack of workers in critical roles at the mine would threaten mine safety and productivity.

Cigar Lake is a highly complex operation and worker availability was reduced by pandemic-induced self-isolation, absenteeism and increasing regional transport restrictions from remote communities to the site. At the time, Cameco noted that the timing for restarting the mine would depend on availability of required workforce, pandemic trends in Northern Saskatchewan and "the views of public health authorities".

In Cameco's 9 April announcement, Tim Gitzel stated that:

"further safety measures, along with the provincial vaccine rollout program and increased confidence around our ability to manage our critical workforce, have given us greater certainty that Cigar Lake will be able to operate safely and sustainably."

Cameco did not offer a restart date or production rate as these "will be dependent on how quickly we are able to remobilize the workforce." The announcement noted twice that there is uncertainty regarding the achievable production rate, stating that 2021 guidance will only be updated once production resumes and the company understands the sustainable production rate. Further,

“we will not hesitate to take further action if we feel our ability to operate safely is compromised due to the pandemic.”

The timing of Cameco's decision was a little unexpected, given an announcement of a positive case amongst the mine's maintenance crew only a week ago and Saskatchewan's high case load. However, active cases the Far North East zone, in which Cigar Lake is located, have fallen to only 20. Further, vulnerable groups, including First Nations people, have been given prioritised vaccination amongst the 21% of Saskatchewan's population to have received a first dose.

Why has Cameco Restarted Cigar Lake?

Whilst restarting was simply a matter of time (or, rather, timing) Cameco was keen to restart to contain its care and maintenance costs. Cigar Lake's closure costs amount to around US$7m per month, imposing a large operating cost impost regardless of the company's healthy balance sheet. The impact of these costs would increase in early June - the completion date for Canada's Emergency Wage Subsidy program, which covered up to 75% of wages for business operations suspended due to COVID-19.

Nonetheless, the decision to restart right now indicates a willingness to take more risk than we would have expected, given Cameco's determination not to "yo-yo" the mine with any further suspension and the strength of their commitment to the health of workers and the broader community. Further, Cameco is highly attuned to its public image - as demonstrated by previous decisions to put the safety of its workers and communities ahead of production targets – so it would be aware of the potential for negative PR based on perception alone.

We are inclined to believe, therefore, that Cameco's board has accepted these risks after weighing up concerns regarding uranium supply - or conversely, the benefits of having owned production that can deliver into supply concerns.

Might spot supply concerns be playing a role?

Cameco confirmed that it will continue to purchase material, as needed, to meet its committed deliveries.

The spot market has tightened considerably in recent weeks, largely due to purchasing from listed uranium companies. Yellow Cake plc announced late February that it would exercise its option to acquire 3.5 Mlbs U3O8 from Kazatomprom - plus it will top up another 1 Mlbs with their cash balance.

Since then, junior uranium companies have exerted unexpected pressure by buying pounds in an illiquid market, with Denison (2.5 Mlbs), UEC (2.1 Mlbs) and Boss Energy (1.25 Mlbs) raising money to buy pounds, in addition to smaller purchases from Peninsular Energy (450,000 lbs for contract delivery), Uranium Royalty Corp (350,000 lbs) and Encore Energy (200,000 lbs). Tellingly, Denison was reported to have needed 17 transactions with 12 different parties to secure its 2.5 Mlbs order.

Cameco has not been visible in the spot market this year. This is partly explained because some customers will have deferred deliveries to later in the year when they expect to have resources to divert from the pandemic to managing their fuel cycle. Further, Cameco is believed to have used spot price weakness last year to partly rebuild its capacity to buy-to-deliver through deferred transaction settlements. Nonetheless, we also assume the company has run down inventories over the last months.

Even with Cigar Lake returning to full production, Cameco will need to initiate buy-to-deliver purchases in the order of 10 Mlbs this year. In recent months management have stated their goal to maximise the arbitrage between spot prices and their delivery prices, so the narrowing of that spread by an increasing spot price makes the suspension of low cost production harder to bear.

We believe this decision is a strong signal to the market that Cameco wants to use its own production pounds as much as possible, rather than be forced to buy spot pounds at pricing that may well move higher than the lower part of their contract portfolio. Any buy-to-deliver losses on those contracts will compound care and maintenance costs and create friction in Cameco’s ability to enter into long term contracts.

Kazakh Supply Uncertainty

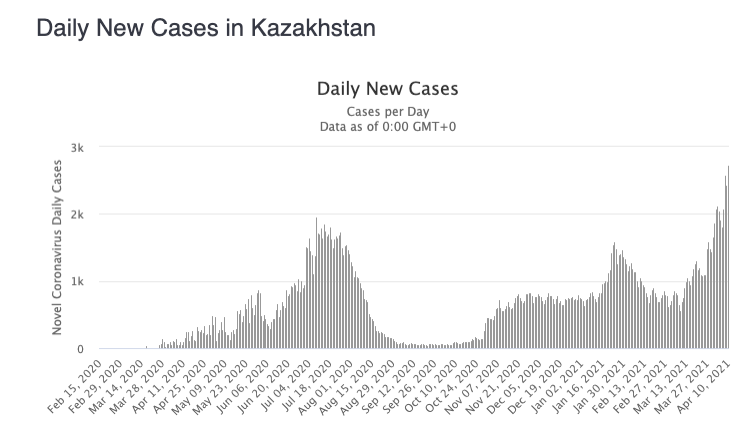

But it might be that the most relevant COVID stats to Cameco's decision lie outside Saskatchewan. Kazakhstan is reporting its highest caseload yet, a dramatic increase in the last month to over 2,500 new cases each day. Whilst Kazatomprom have not directly flagged any issues, this situation has prompted CGN to warn of potential disruption to its 49% owned Samizbai operations.

Whilst many thousands of miles from each other, Kazatomprom’s uranium production is equally susceptible to the availability of skilled production workers, and we suspect the tipping point in Cameco’s thinking may be their concern regarding continuing operations at Inkai, Cameco’s joint venture with Kazatomprom. Kazatomprom have committed to supporting government actions to control the pandemic, which might well include another strict lockdown. A disruption at Inkai would represent a heightened business risk to Cameco in the absence of alternative mine supply.

Cameco would also be aware that any further disruption in Kazakh production will push Kazatomprom more firmly into the spot market, competing head-to-head with Cameco (and other producers) in the buy-to-deliver market.

Pressure from Partners?

Bear in mind that Cigar Lake is jointly owned – Cameco owns 50.1% and is the operator. However, Orano has considerable influence as a 37% owner of the mine and the operator of the McLean Lake mill through which Cigar Lake’s ore is processed.

Orano has just finished closing down COMINAK operations in Niger and will be nervously reading tea leaves on the potential for its own Kazakh joint venture supply to be interrupted. Further, Orano is not as exposed as Cameco to public relations push back at Cigar Lake, so with little downside risk is likely to be pushing hard for the restart. Orano is a supplier of early fuel to the four new reactors at Barakah in the UAE.

Unit 1 has just commenced generating and Unit 2 has just been loaded with fuel, leaving two more initial loads to be completed in 18 months. Plus it will have one eye on its obligation to repay the 5.4 Mlbs uranium loan to Cameco in early 2024, a deadline already extended by 2 years when McArthur River was placed into indeterminate care and maintenance.

Relevance to Term Contracting

Tim Gitzel reminded us that “we have a home in our contract portfolio for these low-cost pounds.” Beyond the clear preference for delivering into contracts from low-cost production, restarting Cigar Lake is important to Cameco’s broader contracting strategy, which ultimately will underpin returning the larger McArthur River to production.

Without confidence in its production rate, Cameco will find it difficult to expand its contract portfolio: its pricing modelling will contain uncertain cost assumptions and buyers will argue for more favourable terms. Cameco will find contract negotiations difficult without a secure supply of uranium which is firmly under its control - and with Inkai vulnerable to pandemic conditions in Kazakhstan that only leaves Cigar Lake.

We believe Cameco, with a firm nudge from Orano, is taking a well-calculated risk to ensure current contracts remain profitable at a time when its contract delivery schedule gets busier and competing spot market demand is building. This decision is also to ensure Cameco has the confidence to remain a first mover in the next contracting round.

Both of which should be a bullish signal to the market, regardless of a few cents here or there on the spot price.

Eager for more?

Want to hear more from Brandon, or looking for consistent returns for more confident investing? That's where we come in. Crux Investor is an investing app for busy people.

You’ll receive a single stock recommendation each month, curated by industry experts and presented in a clear and focused one-page memo. You’ll also receive access to a platform full of programmes that will allow you to grow your financial knowledge, overall, all at your own pace.

Crux Investor is for anyone interested in saving time while investing with confidence. It's an ideal resource for the novice that needs guidance and is tired of throwing money away with guesses and gambles. But it's also a perfect fit for the experienced investor that wants a faster and more efficient way to arrive at the perfect stock or significantly increase their knowledge.

Finally, you can afford the analysts the big funds use. No more gambling, no more guesswork. Instead, save time, slay stress, and start investing with confidence by joining Crux Investor today.

Analyst's Notes

Subscribe to Our Channel

Stay Informed