Sprott’s Physical Uranium Trust to Change the Uranium Game

Uranium expert and CEO, Brandon Munro, discusses how Sprott's physical uranium trust will change the uranium game. Plus what it means for investors...

Uranium investors will mark 28 April 2021 in their calendar and tell their grandchildren where they were when they heard the news. The day the sector finally turned. The day that Sprott Asset Management announced the acquisition of Uranium Participation Corp and the establishment of the Sprott Physical Uranium Trust. The start of a bull rally that may ultimately drive the price of uranium higher - and more sustainably - than the famed bull run of 2005-2007.

To get the party off to a happy start, UPC announced it will be shopping for uranium with a C$70M bought deal raising that was upsized from $50M in a day and could grow by a further C$10.5M if the underwriters take their over-allotment option. Demonstrating the contagion these moves create, Uranium Royalty Corp announced a C$37M financing to buy uranium and royalties.

Sprott & the Founding of UPC

Sprott knows the uranium sector very well, having backed multiple winners during the last boom. The sort of winners that made 10 baggers look like fixed interest returns. The Sprott group has grown from those days to a natural resources empire, including four physical bullion trusts that have a combined value of $13B and a following of 200,000 investors globally.

On the eve of another uranium bull market, Sprott has again positioned itself well, building leveraged positions in multiple names across the sector. And the corporate memory of 2007 remains strong - the famed volatility of uranium equities is legend within the organisation. As is the event that started it all: the founding of UPC.

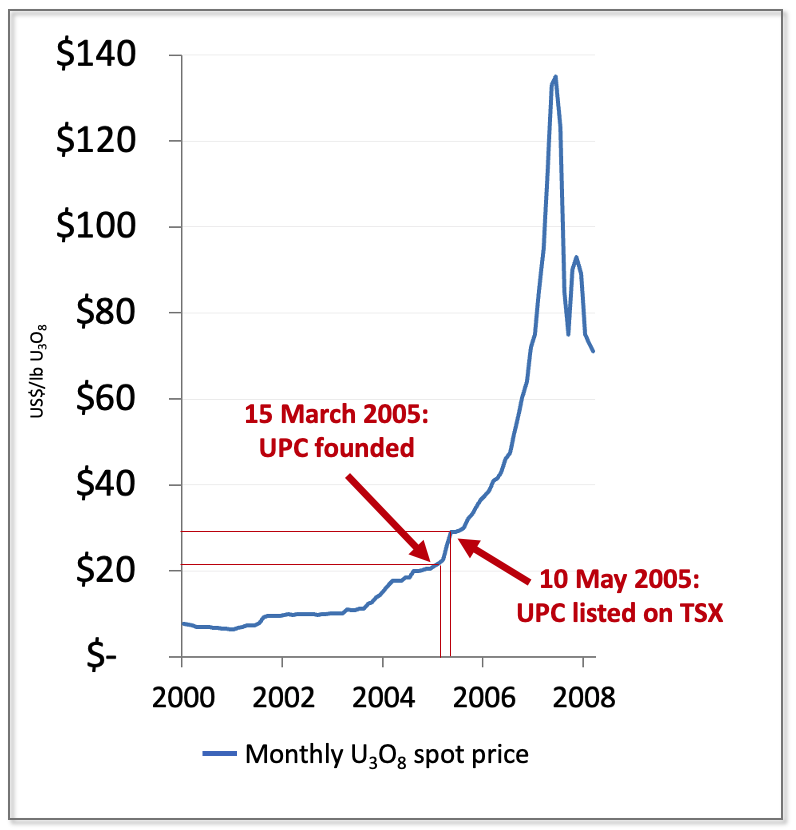

Kevin Bambrough, then President of Sprott Inc, conceived of Uranium Participation Corp in the mid-2000s after convincing Eric Sprott to bet big in uranium stocks off a base price of $11/lb. In the year before launching UPC, Sprott amassed substantial holdings in most juniors and a solid position in Cameco.

Just the launch of UPC’s IPO bumped the uranium price by a few dollars. That price grew further still after the UPC prospectus was filed and orders for the IPO started flowing. The listing was a success and UPC kept trading at a premium – issue after issue swallowed up millions of pounds of uranium. Utilities felt the pressure knowing the vehicle would continue to compete for supply and this contributed to the scramble for long term contracts.

This decision to take UPC back into the fold will also deserve a place in Sprott’s annals.

The timing couldn’t be better. Uranium equities have experienced an influx of investment from the US, pushing many companies’ share prices four times higher since November. In no small part, this interest grew on the narrative that Wall Street types would buy equities and then push a few hundred million bucks at buying spot uranium in a tight market, lifting the metal price and guaranteeing a successful equities trade.

And that was before GME and #silversqueeze democratised the big end’s monopoly on market manipulation. Or, rather, gave the more nimble asset managers a few million foot soldiers to generate volatility.

The lack of a suitable uranium vehicle for this purpose has held back physical buying – not a bad thing given fundamentals (with a bit of help from COVID) have tightened the sector to breaking point in the meantime. The only two vehicles in the sector (UPC and Yellow Cake plc) were quoted outside the US, coupling currency risk with the inconvenience for US fund managers - and ruling out the possibility of a Reddit fuelled squeeze.

Beyond that, many investors didn’t like the way UPC’s management was structured although, in fairness, both vehicles' fee structures were outdated in today’s ETF-driven world.

Sprott's UPC Takeover

Oh, how things have changed now!

Sprott Asset Management announced on 28 April that it would takeover UPC and create the Sprott Physical Uranium Trust, listed in both New York and Toronto, with UPC shareholders to receive SPUT shares and the Denison management contract to be paid out. UPC’s announcement pointed to the “modernisation” of the vehicle and its management/cost structures. Regardless of how the headlines read, this is a takeover of UPC by a new Sprott SPV which is expected to complete mid-2021, assuming no interlopers are prepared to pay a cash premium for UPC’s 17 million pound uranium bounty.

The move to NYSE is important.

By mid 2021 the sector will have a streamlined physical vehicle, no doubt enlarged by the might of Sprott’s metals sector reach, that can proceed to raise further funds from US investors on an at-the-market (ATM) basis. As Sprott Asset Management CEO, John Ciampaglia said, “We have found a high degree of overlap of interest between investors interested in precious metals and investors interested in uranium.”

ATM raisings are a well-worn path for Sprott, having raised around $4B this way into their bullion trusts over the past 15 months. This structure will enable SPUT to consistently nibble (if not gobble) at the bid in the spot market - the perfect way to fray fuel buyer nerves and terrify producers that need to obtain spot uranium for their contracted deliveries.

With the Sprott marketing machine dangling this $650M opportunity in front of its 200,000 gold and silver bulls, you can expect it to list in New York with plenty of fresh equity in the tin. Enough to ensure, once deployed into uranium, a nice lift in the underlying value of the core UPC material and gain an immediate track record that will position it for rapid further growth. From there the game plan is clear, as John Ciampaglia noted, “In our experience greater liquidity and scale begets greater liquidity and attracts a lot more institutional investors over time. It’s important to scale these funds to improve liquidity and lower overall costs - and attract larger investors.”

Last Cycle vs the Next 12 Months

Let’s have some fun comparing what occurred in the last cycle to what might logically happen over the next 12 months. Look away if you don’t have any exposure to uranium stocks, as this part may cause distress in the under-invested.

Last cycle, UPC filed its 2005 prospectus when spot uranium was approximately $20/lb – not that different to today’s spot price after adjusting for inflation. A few months later the spot price had risen 50% to $30 per pound (on its way to peaking at $136/lb two years further on).

These days the picture of the financial market is far more compelling. The value of the US market is 13 times more than Canada and has doubled since 2007. Once listed on the NYSE, SPUT will be accessible to a market more than 25 times larger than UPC could tap in the last cycle.

Now, there is social media to fizz the excitement amongst Robinhood traders that have shown enough irrational exuberance to take GME to $20b plus.

These days, passive flows are dramatically more influential. The three uranium sector ETFs have already increased assets under management five fold in the last year – but are still worth less than $1B combined. URA and URNM hold around 5% and 15% respectively in YCA and UPC. So when the bull market takes off, you can be sure of copious mindless flows of funds into uranium ETFs for no better reason than investor FOMO will force investors to make sure they have uranium exposure. And 5-10% of that mindless money will power SPUT’s hoarding of uranium. And the neat thing about passive flows, is that this money is price inelastic – the hotter and more unrealistic the commodity price becomes, the greater the flows.

SPUT will now be able to utilise ATM raising, which means it won’t need to trade up to a 10% NAV premium to justify the discount/fee impost of raising from professional money. Just like an ETF, SPUT will be able to raise quickly, cheaply and frequently – adding accretive pounds on even slight premiums. Uranium purchases can be executed as close to real time as possible in small frequent transactions, minimising spread and avoiding front-running traders. It also means both institutional and retail investors will be able to drive the purchasing of physical uranium.

In an investor era that gorges on expansionary monetary policy whilst punting on Robinhood, this could be potent scenario. Particularly for uranium, a thinly traded commodity that has positive fundamentals backing up behind multiple players in a freshly re-shaped game.

Eager for more?

Want to hear more from Brandon, or looking for consistent returns for more confident investing? That's where we come in. Crux Investor is an investing app for busy people.

You’ll receive a single stock recommendation each month, curated by industry experts and presented in a clear and focused one-page memo. You’ll also receive access to a platform full of programmes that will allow you to grow your financial knowledge (with a ton of Uranium content), all at your own pace.

Crux Investor is for anyone interested in saving time while investing with confidence. It's an ideal resource for the novice that needs guidance and is tired of throwing money away with guesses and gambles. But it's also a perfect fit for the experienced investor that wants a faster and more efficient way to arrive at the perfect stock or significantly increase their knowledge.

Finally, you can afford the analysts the big funds use. No more gambling, no more guesswork. Instead, save time, slay stress, and start investing with confidence by joining Crux Investor today.

Analyst's Notes

Subscribe to Our Channel

Stay Informed