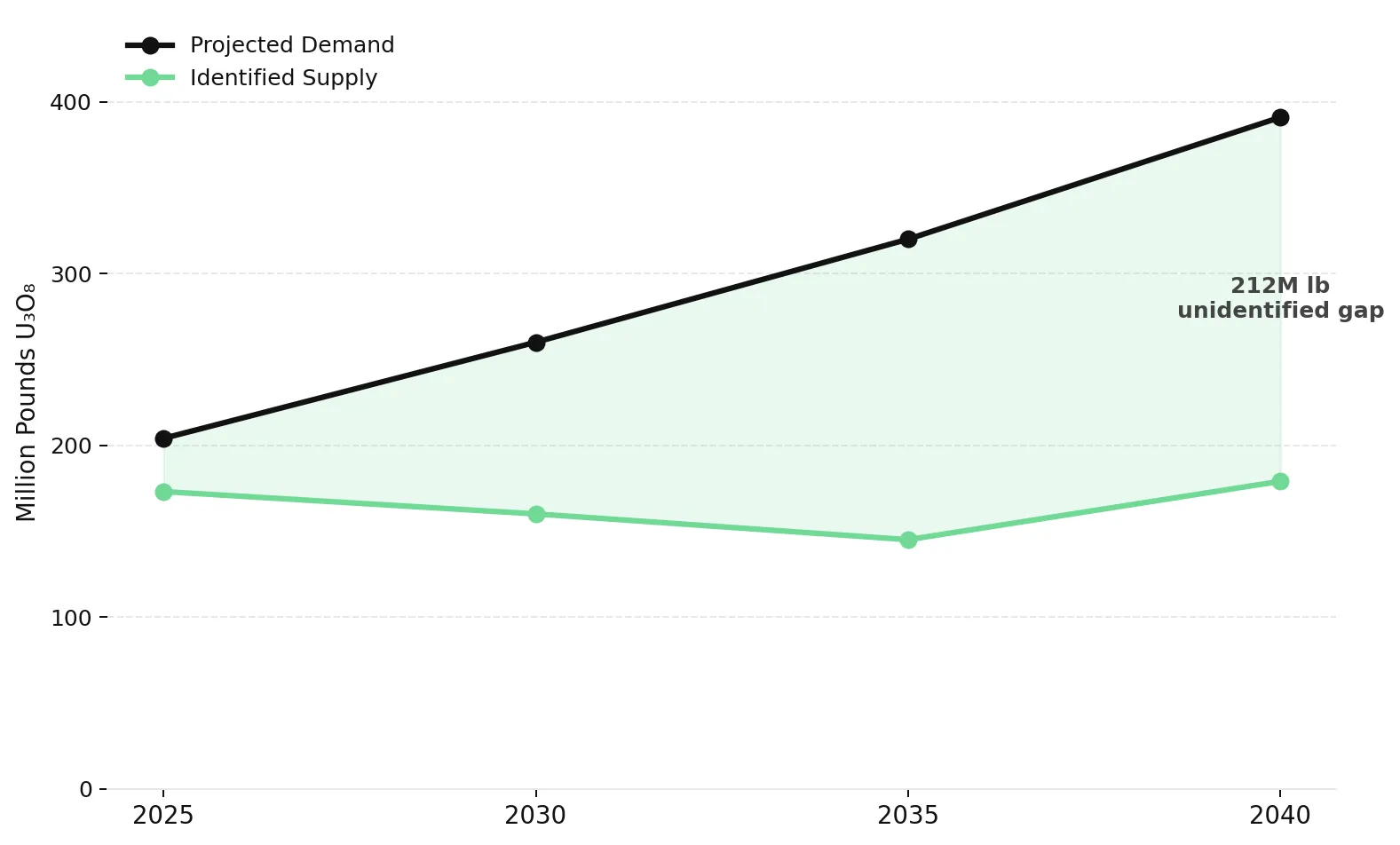

212M-Pound Supply Gap: Energy Security Tightens Uranium Supply as 2040 Demand Outpaces Production

Energy security policies and sovereign buying are tightening uranium supply as projected 2040 demand exceeds identified supply by 212 million pounds.

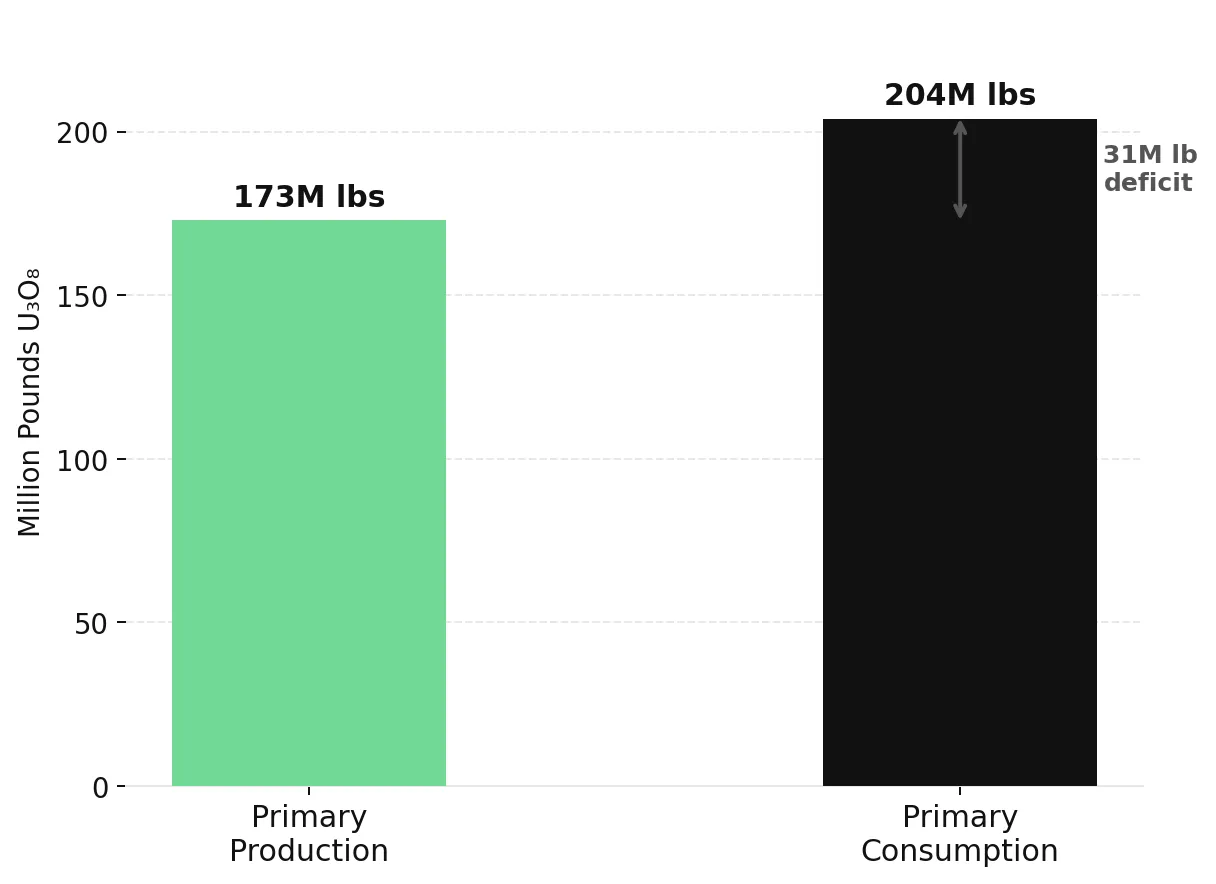

- Sovereign buyers including India, the US, and China are securing long-term uranium supply at prices near an 18-year high, removing material from a market that already ran a 31-million-pound primary supply deficit in 2025.

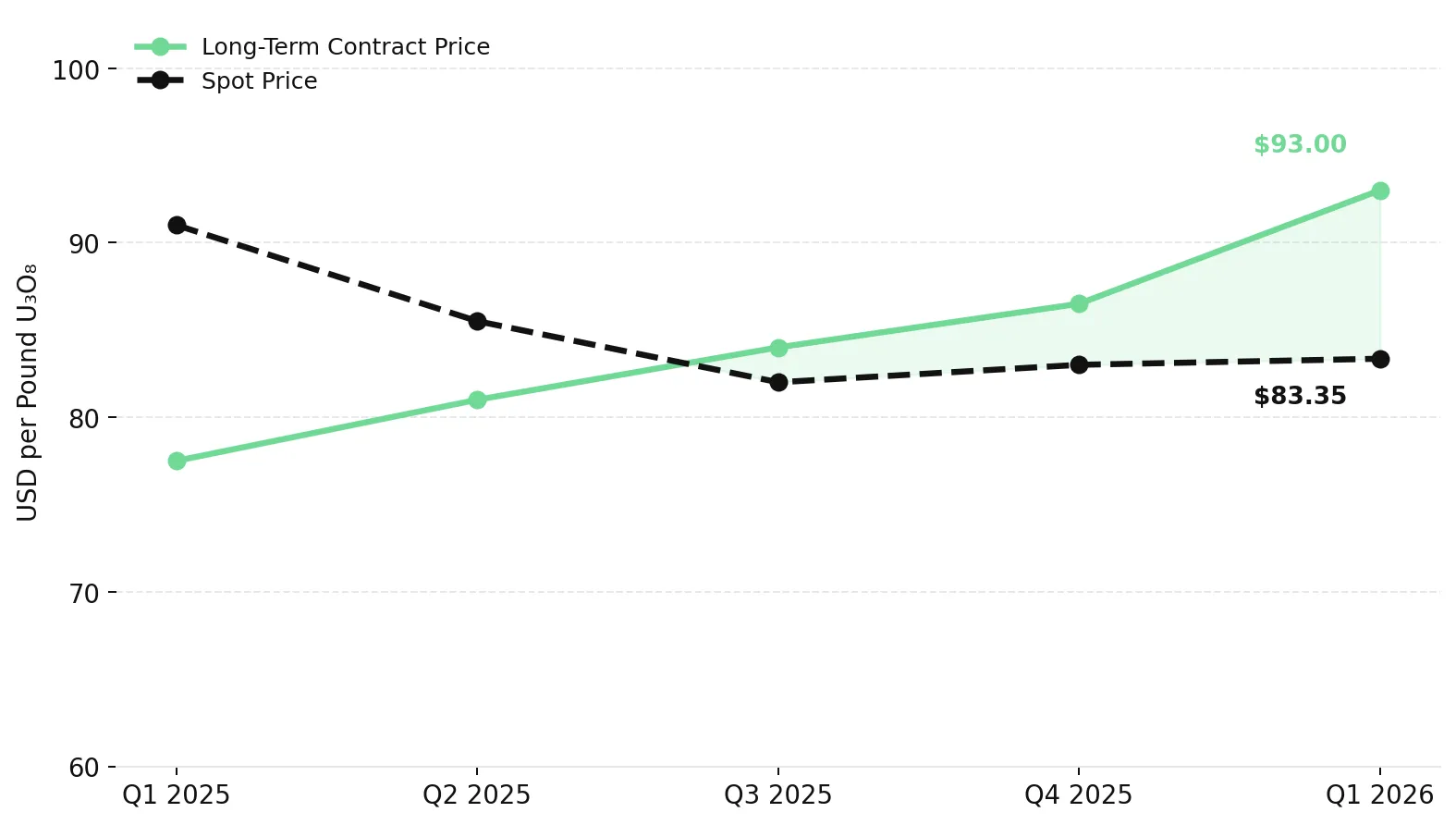

- Long-term uranium contract prices reached $93.00 per pound in Q1 2026, an 18-year high and $9.65 per pound above the $83.35 spot price, indicating that utilities are paying a premium to secure future supply.

- Western utilities face tightening uranium supply: Kazatomprom cut its 2026 production target by approximately 10%, the US ban on Russian uranium imports removed a source that historically supplied about 20% of US reactor fuel, and global mine production fell 31 million pounds short of consumption in 2025.

- Producers are lowering costs and returning to profitability, developers are advancing projects toward production, and explorers are expanding drill programs to define new uranium resources.

- Investors in uranium producers, developers, and funded explorers are gaining exposure to a market where projected demand exceeds identified supply and new mines typically require a decade or more to reach production.

Energy Security Priorities Drive Renewed Nuclear Power Demand

Governments and utilities are prioritizing energy security alongside decarbonization when procuring electricity generation capacity. Reliable, non-fossil electricity generation is increasingly being treated as an energy security requirement rather than solely a decarbonization objective.

The International Monetary Fund's April 2026 World Economic Outlook downgraded global growth to 3.1% and identified a 24% surge in energy prices as the dominant macroeconomic shock of the year. Higher energy prices are increasing utility and government interest in nuclear power because it provides reliable zero-carbon electricity with a relatively small fuel-cost component. The International Energy Agency's Electricity 2026 report projects continued growth in nuclear generation, supporting long-term uranium demand. For investors, the key difference is that current uranium pricing is increasingly being influenced by supply constraints rather than demand forecasts alone. Production shortfalls, sovereign contracting activity, and supply restrictions are reducing the volume of uranium available to utilities.

Sovereign Uranium Procurement Tightens Long-Term Supply

India's 2026 uranium supply agreements demonstrate the growing role of sovereign buyers in the uranium market. In early 2026, India contracted simultaneously with Cameco for nearly 22 million pounds of uranium ore concentrate over nine years at an estimated value of $2.6 billion, and with Kazatomprom through a separate arrangement valued at over $4 billion. These contracts reduce the volume of uranium available to other buyers and increase competition for long-term supply agreements.

Uranium Supply Deficits Deepen as New Mine Development Lags Demand

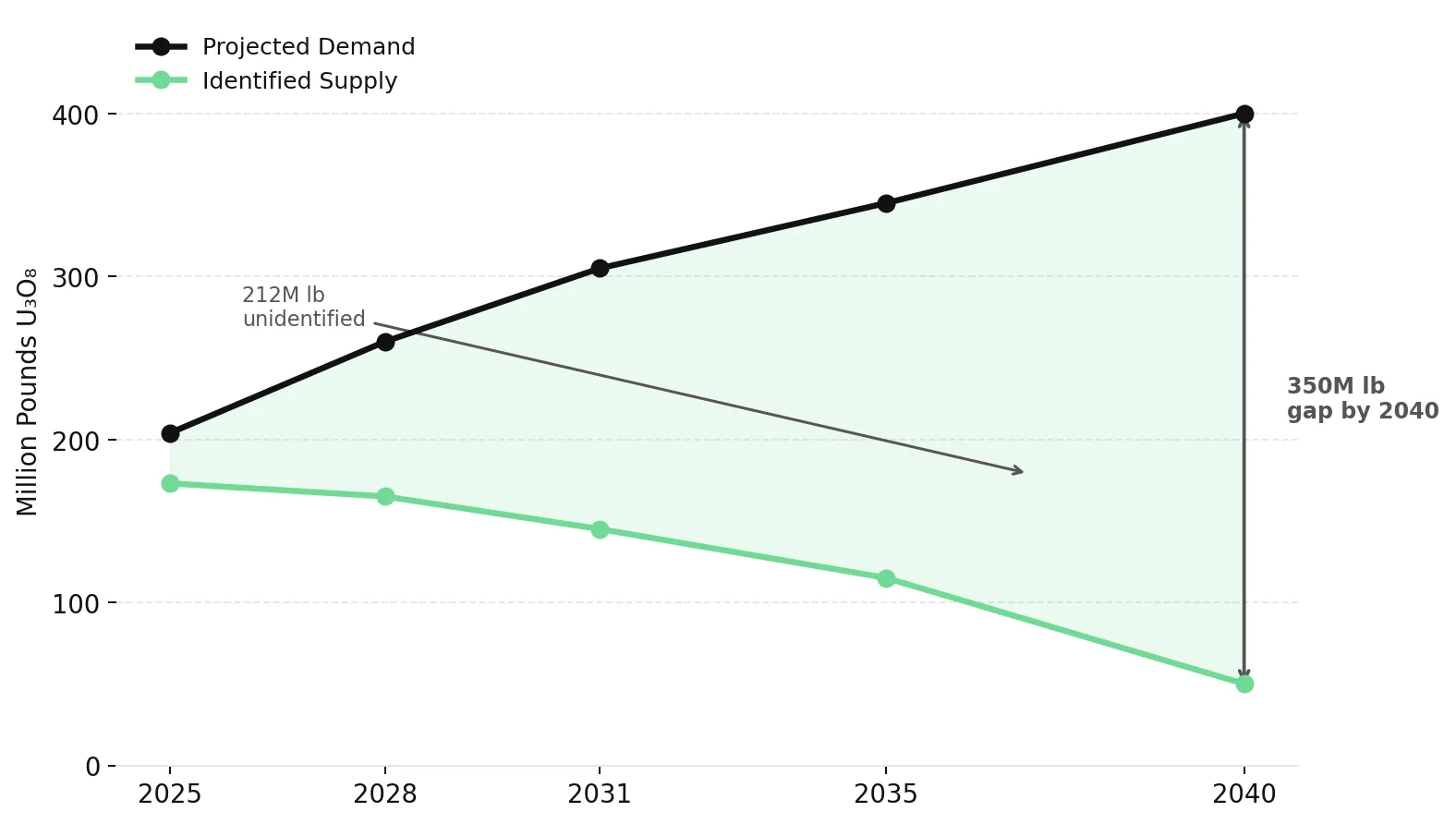

Global primary uranium production in 2025 was approximately 173 million pounds against consumption of approximately 204 million pounds, leaving a 31-million-pound deficit met through secondary supplies. The WNA's 2025 Nuclear Fuel Report projects that all identified supply sources combined cover only 46% of projected 2040 demand. The remaining 212 million pounds of projected demand has no identified supply source. Filling this gap requires new mines to be discovered, permitted, financed, and built, a process that typically takes a decade or more.

Kazatomprom reduced its 2026 nominal production target from 32,777 tU to 29,697 tU, a cut of approximately 8 million pounds representing roughly 5% of total global supply. This was not a forced cut attributable to operational failures; sulphuric acid supply for 2026 was confirmed as stable. It was a strategic decision reflecting the producer's assessment that market conditions do not justify a return to full capacity. The Prohibiting Russian Uranium Imports Act, effective through 2040, has permanently removed Russian-origin low-enriched uranium from accessible US channels, eliminating a source that historically supplied approximately 20% of US reactor fuel annually.

Tightening Uranium Supply Improves Producer Economics

Energy Fuels operates the White Mesa Mill in Utah, the only operating conventional uranium processing facility licensed to process uranium ore in the US. The company reported Q1 2026 revenue of $35.8 million, while finished uranium inventory cost fell approximately 16% to $36 per pound, supported by Pinyon Plain ore with all-in production costs of $23 to $30 per pound. Working capital totaled $956.6 million. Mark Chalmers, Chief Executive Officer of Energy Fuels, explains how tightening uranium supply and firming prices are improving producer economics:

"We'll provide guidance of up to 2.5 million pounds of uranium production, the highest in the US. Strong cost structures and firming uranium prices are supporting revenue growth."

enCore Energy, which produces uranium through in-situ recovery, returned to profitability in Q1 2026, earning $0.03 per share versus a loss of $0.13 per share in Q1 2025. Uranium extraction from the company's South Texas operations rose 22% year-over-year to 90,000 pounds at a cash extraction cost of $34.94 per pound, compared with $78.82 per pound for purchased third-party material.

Term Uranium Prices Signal Tightening Future Supply

TradeTech's Long-Term Uranium Price Indicator reached $93.00 per pound at the end of Q1 2026, an 18-year high and a $6.50 increase from the prior quarter. The long-term contract price exceeded the spot price by $9.65 per pound at the end of Q1 2026. Utilities are paying a 12% premium above spot prices to secure long-term uranium supply. Goldman Sachs forecasts spot uranium prices of approximately $91 per pound by the end of 2026, implying roughly 9% upside from current levels and narrowing the gap with current term prices.

Delayed Utility Contracting Supports High-Quality Uranium Developers

IsoEnergy's Hurricane deposit at the Larocque East project in Saskatchewan's Athabasca Basin contains an indicated resource grading 34.5% U3O8 across 48.6 million pounds, the highest-grade published indicated uranium resource in the basin. The next comparable undeveloped deposit within 50 kilometers of the McClean Lake mill grades 4.42% U3O8, making Hurricane nearly eight times higher by grade. Higher grades can reduce operating costs because less rock must be mined and processed per pound of recoverable uranium. The company holds approximately C$130.5 million in cash and a C$48.4 million equity portfolio.

Atomic Eagle is advancing the Muntanga Uranium Project in southern Zambia, a 58.8-million-pound resource grading 309 ppm across a 1,136-square-kilometer area covered by granted Mining Licences. The March 2026 mine plan outlined an after-tax NPV of US$243 million and a 3.5-year payback period using heap leach processing. The 2026 drilling program is expanding the resource, with 13 of the first 15 holes at the Chisebuka target intersecting mineralization outside the current resource estimate. Phil Hoskins, Chief Executive Officer of Atomic Eagle, explains the supply-demand imbalance driving the need for new uranium projects:

"Roughly 150 million pounds are being produced at the moment and 200 million pounds are being consumed. By 2040 that supply of 150 million pounds is going to drop to 50 million pounds based on current production, while demand will double to 400 million pounds."

Exploration Remains Central to Filling the 212-Million-Pound Uranium Supply Gap

Filling a 212-million-pound uranium supply gap requires new discoveries to be delineated and advanced toward production. ATHA Energy controls 100% of the 6.8-million-acre Angikuni Basin in Nunavut, Canada's largest uranium exploration land package. After making five regional discoveries in 2025, the company launched its largest programme on May 1, 2026, deploying three drill rigs to target approximately 20,000 metres across three mineralised corridors. The programme exceeds the combined metreage drilled in 2024 and 2025 and is fully funded through a CAD$63 million financing. The company has intersected uranium mineralization in 100% of targets tested across the previous two field seasons.

Troy Boisjoli, Chief Executive Officer of ATHA Energy, explains how the company is expanding exploration efforts to identify new uranium supply:

"We're fully funded through a $63 million financing, and we're embarking on our largest ever exploration program, targeting approximately 20,000 meters across three mineralized corridors."

The Investment Thesis for Uranium

- The World Nuclear Association's 2025 Nuclear Fuel Report estimates that identified supply sources cover only 46% of reference-case 2040 uranium demand, leaving 212 million pounds without an identified source.

- Sovereign procurement by India, China, and the US is reducing the volume of uranium available for long-term contracting, increasing competition among utilities that have delayed securing supply.

- Long-term uranium contract prices reached $93.00 per pound in Q1 2026, $9.65 per pound above the $83.35 spot price, indicating that utilities are paying a premium to secure future supply.

- Producers with low operating costs and strong balance sheets can remain profitable at lower uranium prices and benefit from higher contracted and spot prices.

- Developers with high-grade indicated resources, completed mine plans, and defined processing pathways face fewer permitting and development hurdles than earlier-stage projects and are closer to the production timelines utilities may require for future supply.

- Explorers with funded drill programs, successful discovery records, and projects in established uranium districts could benefit if the projected 212-million-pound supply gap increases the need for new uranium deposits.

- Consolidation in the US ISR uranium sector could improve access to capital, strengthen negotiating leverage with utilities, and increase institutional investor participation.

- Uranium projects outside Russian-linked supply chains may benefit as Western utilities place greater emphasis on fuel origin and supply security when awarding contracts.

Entering the second half of 2026, uranium spot prices remain below long-term contract prices despite sovereign procurement activity and ongoing supply deficits. Sovereign buyers are contracting uranium supply at prices near an 18-year high. Kazatomprom has reduced production despite stable operating conditions. Energy Fuels' White Mesa Mill remains the only operating conventional uranium processing facility in the US. Funded explorers are expanding drill programs to identify new uranium resources in established Canadian uranium districts. The World Nuclear Association's reference case identifies a 212-million-pound gap between projected 2040 demand and identified supply. Closing that gap will require new uranium supply to be discovered, financed, permitted, and brought into production over the coming decade.

TL;DR

Governments are increasingly treating energy security as a national priority, driving renewed support for nuclear power and strengthening long-term uranium demand. At the same time, sovereign buyers are securing large volumes of uranium through long-term contracts, reducing material available to other utilities. Global uranium production fell 31 million pounds short of consumption in 2025, while the World Nuclear Association estimates identified supply covers only 46% of projected 2040 demand. With new uranium mines often requiring a decade or more to reach production, supply growth cannot respond quickly. This combination of rising demand, constrained supply, and long development timelines is creating opportunities across uranium producers, developers, and explorers.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed