AI-Driven Demand Growth & Supply Constraints Signal Uranium Structural Repricing in 2026

Uranium's structural supply deficit and AI-driven demand signal 2026 repricing. Long-term contracting, not spot volatility, now drives investment relevance.

- Uranium's 2025 price behavior reflects a market transitioning from speculative momentum to structurally constrained supply, with long-term contracting, not spot volatility, emerging as the dominant signal for future pricing.

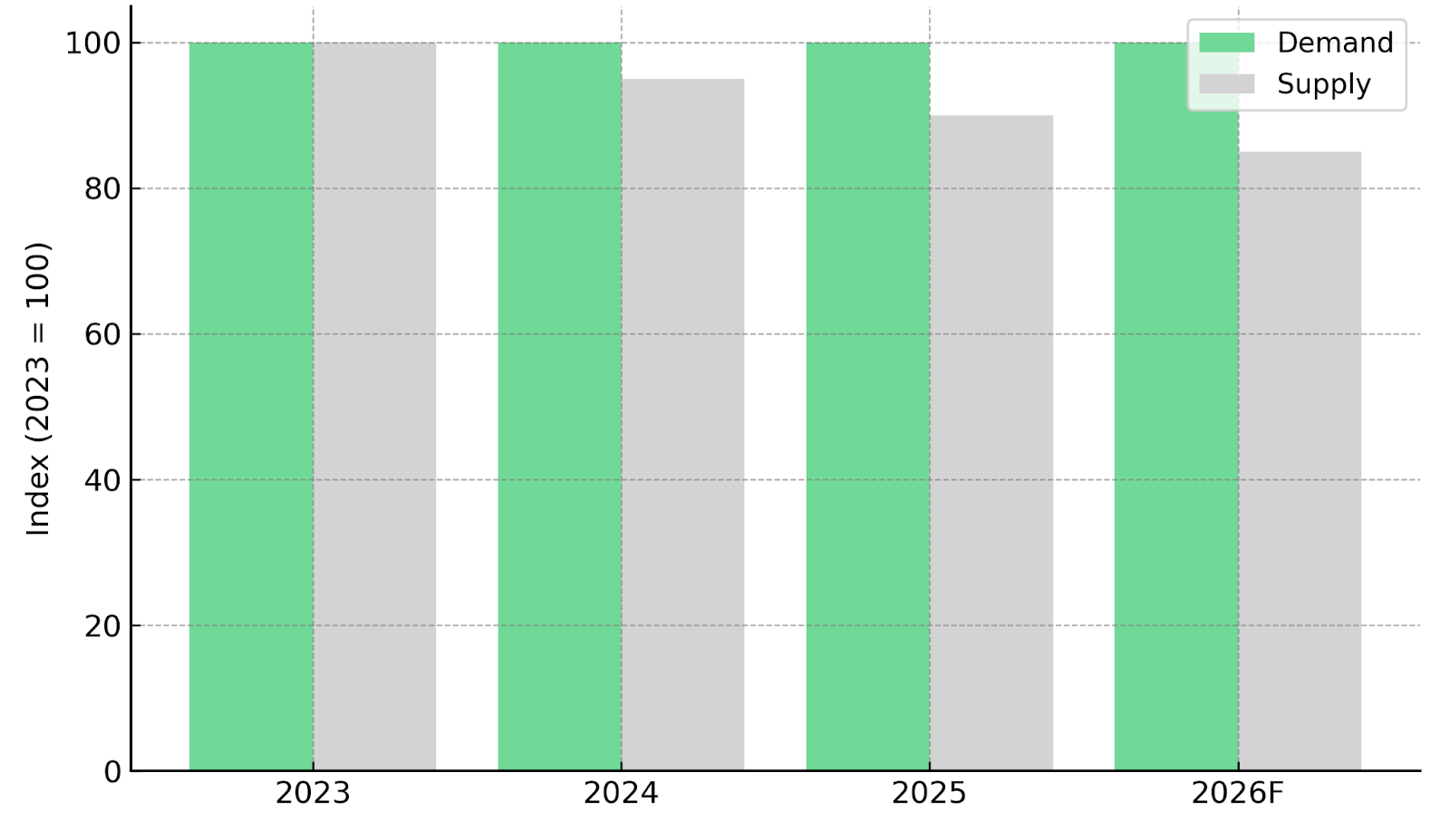

- Persistent under-delivery from global producers and delayed project restarts have accelerated expectations of a structural supply deficit into 2026, despite incentive prices above US$80/lb.

- Financial demand, led by physical uranium vehicles, has tightened available spot supply and altered price discovery dynamics without resolving underlying utility procurement needs.

- New electricity demand from AI data centers has reinforced nuclear energy's role as baseload infrastructure, strengthening uranium's long-duration demand profile.

- Producers, near-term developers, and high-grade explorers with jurisdictional certainty and permitting visibility are increasingly differentiated as capital seeks execution over optionality.

Uranium's 2025 Price Action Signals a Market Moving Beyond Spot Volatility

The year 2025 marked a transition point for uranium pricing dynamics. After the sharp spot-driven rally of 2023-2024, price action became more range-bound, testing investor conviction while reinforcing the durability of the long-term thesis. According to Trading Economics data, spot U₃O₈ fluctuated between US$63.17 per pound in March and US$83.33 per pound in September, with the price appearing to find support at the US$75 level since late August. This pricing behavior suggests downside risk is increasingly constrained by cost curves and contracting economics rather than sentiment alone.

For institutional investors, the more consequential signal emerged from the long-term contract market. According to data compiled via Cameco, long-term prices rose from approximately US$80/lb at the start of 2025 to US$86/lb by late November, reflecting active negotiations between utilities and producers rather than speculative flows. These prices approach incentive levels required to justify mine restarts, in-situ recovery expansions, and new project development.

Within this context, U.S.-based producers and near-term developers began attracting renewed attention. The investment case shifted from spot price leverage toward the ability to respond to contract demand within realistic permitting and construction windows. enCore Energy exemplifies this positioning as an ISR operator with two Central Processing Plants now operational in South Texas. The Rosita and Alta Mesa facilities represent scalable production infrastructure, with Alta Mesa having commenced operations in Q2 2024. As of June 2025, Alta Mesa averaged daily production of 2,678 pounds, demonstrating the ramp-up trajectory.

enCore's operational momentum underscores how execution capability translates into market relevance. William Sheriff, Executive Chairman of enCore Energy, describes the production acceleration:

"Our production rate on a daily basis has gone, depending on what time frame you're measuring it against, from up 200% to up 300%."

Long-Term Contracting Has Re-Emerged as the Market's Primary Signal

The uranium market remains structurally opaque relative to other commodities, but 2025 confirmed that long-term contracting, not spot pricing, defines investment relevance. Utilities facing requirements into the late 2020s increasingly returned to multi-year contracts as confidence in supply availability eroded. The widening gap between spot volatility and contract price stability increasingly defines how sophisticated capital evaluates uranium exposure.

Long-term prices approaching US$86 per pound have begun to incentivize production in theory. In practice, however, the market has discovered that price alone does not translate to near-term supply. Restart timelines, regulatory approvals, labor availability, and processing constraints all impose delays that cannot be solved by price signals alone. This reality has shifted utility focus toward counterparties with demonstrated operational track records and regulatory certainty.

This divergence explains why ISR operators in the United States are viewed differently from greenfield developers in utility negotiations. ISR assets benefit from lower upfront capital expenditure, shorter permitting timelines, and scalable production profiles. Similarly, producers with licensed processing infrastructure occupy a strategic position within the contracting cycle. Energy Fuels' White Mesa Mill in Utah represents precisely this type of scarcity asset, characterized by the company as the only operating conventional uranium mill in the United States, providing processing optionality that extends beyond the company's own production.

Supply Discipline Has Become Structural Rather Than Cyclical

A defining feature of 2025 was the persistent inability of global uranium suppliers to meet revised production guidance. Major producers adjusted targets downward, while junior developers continued to struggle with execution, financing, or permitting delays. These outcomes reinforce that uranium supply constraints are no longer merely cyclical consequences of past underinvestment, they have become structural features of the market.

Several factors contribute to this reality. Extended care-and-maintenance periods have resulted in long mine restart timelines, often measured in years rather than months. Skilled labor shortages affect mining jurisdictions globally, particularly for specialized uranium operations. Regulatory complexity has increased substantially for conventional mining and milling, while licensed processing facilities remain scarce. The convergence of these constraints means that even sustained incentive pricing may not resolve supply deficits within typical investment horizons.

In this environment, the market increasingly distinguishes between theoretical resources and deliverable pounds. Developers with permitted assets or toll-milling pathways gain disproportionate valuation attention relative to peers with similar enterprise value per pound metrics but longer timelines. IsoEnergy illustrates this differentiation by combining ultra-high-grade resources in Canada's Athabasca Basin with fully permitted past-producing assets in the United States, including the Tony M Mine, Daneros Mine, and Rim Mine in Utah. These permits provide an estimated three to five year time advantage versus greenfield permitting. Philip Williams, Chief Executive Officer of IsoEnergy, describes the strategic rationale:

"What resonated with investors is that uranium is a very difficult commodity to be in, and I've been in the space since 2006, and time and time again single asset, single jurisdiction companies have gone off the rails for some reason…What we've done is to not have all the eggs in one basket and give ourselves multiple shots on goal."

Financial Demand Has Tightened Supply Without Solving Utility Coverage

The growth of financial uranium demand in 2025 added a new layer to market structure. Physical accumulation vehicles removed significant volumes from the spot market, amplifying price sensitivity during periods of thin liquidity. While this activity contributed to higher spot prices and increased investor awareness of the uranium thesis, it did not materially advance long-term utility coverage.

For investors, understanding this bifurcation matters significantly. Financial demand can accelerate price signals and validate bullish positioning, but it does not substitute for production capacity. Utilities require physical delivery certainty, multi-year supply agreements, and counterparty reliability, none of which financial vehicles provide.

This dynamic has supported uranium equities broadly, but valuation dispersion has widened considerably. Companies with credible pathways to production or expansion have increasingly outperformed explorers dependent on future capital cycles. Exploration-focused companies such as ATHA Energy remain leveraged to discovery upside, particularly in tier-one jurisdictions. ATHA Energy's 2025 exploration program at the Angilak Project delivered five additional discoveries, including the Mineralized RIB Corridor where uranium mineralization has been intersected across a 4.4 kilometer eastern limb and approximately 4.0 kilometers along the parallel western limb. ATHA Energy’s Chief Executive Officer Troy Boisjoli articulates the company's strategic pivot toward development:

"For 2026, our intention is to move these projects forward in earnest and not be with an allocation of dollars between advancing deposits and exploration with a smaller amount on exploration. The large percentage of the focus from a strategic perspective now is about moving projects forward."

AI-Driven Power Demand Has Reframed Nuclear Energy's Strategic Role

One of the most significant narrative shifts in 2025 was the integration of nuclear power into discussions around AI infrastructure and data center growth. According to the IEA's Energy Demand from AI report, global electricity consumption from data centers is projected to grow substantially faster than overall electricity demand through the end of the decade. This trajectory has reinforced nuclear energy's role as a reliable, carbon-free baseload solution, particularly in jurisdictions prioritizing grid stability and energy security.

FThis reframing strengthens uranium's duration as a strategic commodity rather than a cyclical trade. It also increases the relevance of jurisdictions with established nuclear policies and domestic fuel-cycle ambitions. U.S.-focused operators are increasingly viewed not as spot price-takers, but as strategic suppliers aligned with national infrastructure priorities. Energy Fuels has positioned itself explicitly within this framework, building a critical minerals platform around its uranium foundation while advancing rare earth element separation capabilities, with commercial U.S. production of heavy REE oxides planned as early as Q4 2026. Mark Chalmers, Chief Executive Officer of Energy Fuels, explains the diversified commodity upside:

"Energy Fuels is a company that is unique from all others that you'd look at because we are focused on building a critical mineral hub that is built around our uranium business but also includes the rare earth suite of elements."

Capital Allocation Is Shifting Toward Execution & Jurisdictional Certainty

As uranium markets mature beyond the initial repricing phase, investor focus has shifted decisively from optionality to execution. Capital increasingly favors companies demonstrating permitted or permitting-advanced assets, clear development timelines, transparent cost structures, and jurisdictional alignment with nuclear policy objectives. This evolution reflects broader recognition that uranium's supply constraints cannot be resolved by capital availability alone.

The cost of capital has emerged as a differentiating factor, with established operators accessing institutional financing on terms unavailable to earlier-stage peers. enCore Energy's US$115 million convertible note offering, featuring a 5.5% coupon with capped-call structure, and Energy Fuels' US$700 million convertible senior notes offering closed in October 2025 demonstrate institutional appetite for uranium exposure through established operators. William Sheriff, Founder and Executive Chairman of enCore Energy describes the capital markets reception:

"The cost of capital is something we've never seen before in terms of a five and a half percent coupon on a non-secured note... It introduced us to an entirely new level of investor, most of these funds were 10, 20, 30 billion dollar funds."

The Investment Thesis for Uranium

- Structural supply deficits are emerging as execution challenges persist despite incentive pricing, suggesting that even sustained high prices may not resolve near-term shortfalls.

- Long-term contracting activity is accelerating, signaling utility procurement urgency rather than speculative enthusiasm and validating the durability of demand.

- AI-driven electricity demand has reinforced nuclear power's long-duration role in global energy systems, extending uranium's demand visibility beyond traditional utility replacement cycles.

- U.S. and Canadian operators benefit from jurisdictional alignment with energy security initiatives and critical minerals policy frameworks that prioritize domestic supply chains.

- Producers and near-term developers with permitted assets, ISR operations, or licensed processing infrastructure are best positioned to convert macro tailwinds into cash flow visibility.

- High-grade exploration success in tier-one basins retains significant value, particularly when coupled with strategic pivots toward project advancement.

- Access to institutional capital at favorable terms increasingly differentiates operators capable of funding growth without dilutive equity issuance.

Why 2025 May Be Remembered as Uranium's Inflection Setup

While uranium prices in 2025 did not deliver uninterrupted upside, the year fundamentally reshaped investor understanding of the market's true constraints. Supply discipline appears structural rather than cyclical, contracting activity accelerated beyond spot market noise, and new demand narratives reinforced nuclear energy's strategic relevance within global energy transition frameworks.

For investors, the implication is clear: uranium's investment case is no longer defined by spot price momentum, but by execution capability, jurisdictional certainty, and alignment with long-term power demand growth. As the market moves toward 2026, differentiation, not mere exposure, will increasingly determine returns.

TL;DR

Uranium's 2025 price action marked a shift from speculative momentum to structurally constrained supply. Long-term contract prices—rising to US$86/lb—have emerged as the dominant investment signal, reflecting utility procurement urgency rather than spot volatility. Global producers consistently under-delivered against guidance, confirming supply constraints are structural, not cyclical. AI-driven electricity demand has reinforced nuclear energy's strategic role as carbon-free baseload infrastructure. Capital is now flowing toward execution capability over optionality, favoring ISR operators, permitted assets, and licensed processing infrastructure. U.S. and Canadian operators with jurisdictional alignment and clear development timelines are increasingly differentiated as the market approaches a potential structural repricing in 2026.

FAQs (AI-Generated)

Persistent production under-delivery, extended mine restart timelines, skilled labor shortages, and regulatory complexity have created supply constraints that price signals alone cannot resolve. Long-term contract prices approaching US$86/lb indicate utilities are actively securing supply, signaling procurement urgency ahead of anticipated deficits.

AI data centers require substantial baseload electricity, and nuclear power offers reliable, carbon-free generation. This has reframed uranium as strategic infrastructure rather than a cyclical commodity, extending demand visibility beyond traditional utility replacement cycles.

Spot prices reflect near-term trading activity and can be volatile. Long-term contract prices—negotiated directly between utilities and producers—better indicate sustained demand and incentive economics required to justify new production.

Producers and developers with ISR operations, permitted assets, licensed processing infrastructure, and jurisdictional alignment with nuclear policy initiatives are outperforming. Execution capability and regulatory certainty increasingly differentiate valuations.

Mine restarts require years, not months. Skilled labor shortages, regulatory approvals, and scarce processing infrastructure impose delays regardless of price. This structural reality means incentive pricing may not resolve deficits within typical investment horizons.

Analyst's Notes

Subscribe to Our Channel

Stay Informed