Americas Gold & Silver Positions Galena for Production Growth & Antimony Upside

Americas Gold & Silver targets higher output at Galena through shaft upgrades, mechanised mining, spare mill capacity and antimony processing.

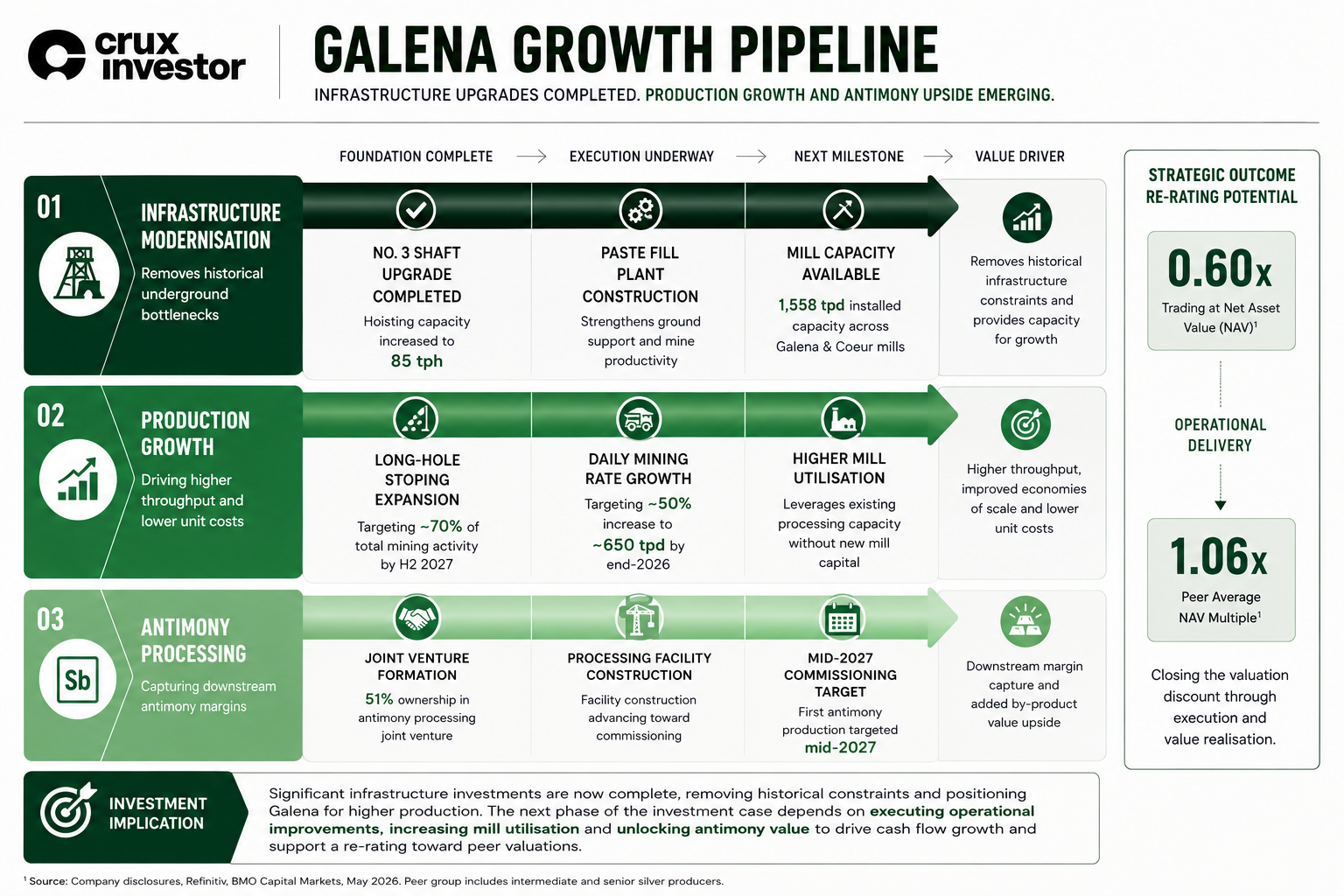

- Phase 2 upgrades to the No. 3 Shaft increased average hoisting rates from 42 tonnes per hour to 85 tonnes per hour, removing the primary constraint on higher production at the Galena Complex.

- The transition to mechanised long-hole stoping has increased productivity by more than 300%, while management reports mining cycles that are approximately 12 times faster than the previous mining method.

- The acquisition of the Crescent Mine supports a production growth strategy because the Galena and Coeur mills have an installed capacity of 1,558 tonnes per day, while current mining rates remain below that level.

- The joint venture (JV) with United States Antimony Corporation is targeting a mid-2027 processing facility to increase the value captured from antimony already produced alongside silver and copper.

- The company reported $122 million in cash, $50 million drawn from a $100 million debt facility, and a valuation of approximately 0.60 times net asset value (NAV) compared with a peer average of approximately 1.06 times NAV.

The Re-Rating Opportunity Depends on Production Delivery

Americas Gold & Silver (TSX: USA | NYSE American: USAS) currently trades at approximately 0.60 times net asset value (NAV), compared with an average of approximately 1.06 times NAV for intermediate and senior silver producers. The valuation discount persists despite the completion of shaft upgrades that increased hoisting capacity from 42 tonnes per hour to 85 tonnes per hour and productivity gains exceeding 300% from mechanised mining. Management is targeting a significant increase in mining rates through 2026 as operational improvements are rolled out across the Galena Complex. Demonstrating that infrastructure investment is translating into higher production and lower unit costs would provide the clearest pathway toward narrowing the current valuation discount.

Consolidating the Idaho Silver Valley

Americas Gold & Silver's Idaho strategy is built around increasing throughput through existing infrastructure rather than constructing new processing facilities. The company acquired 100% ownership of the Galena Complex in December 2024 and followed with the approximately $65 million acquisition of the Crescent Mine in December 2025. Crescent is located approximately 9 miles from Galena and was acquired to provide additional feed opportunities for the existing processing infrastructure.

The Galena and Coeur mills have a combined installed processing capacity of 1,558 tonnes per day, while current mining rates remain substantially below that level. The company is targeting higher production rates through ongoing mine development and operational improvements. Achieving those targets would utilise a significant portion of the available processing capacity without requiring construction of a new mill, thereby reducing capital intensity compared with most mine expansion projects.

Executive Vice President of Corporate Development at Americas Gold & Silver, Oliver Turner, highlighted the scale and grade of the asset:

"We've got over 200 million ounces at Galena at 500 grams per tonne. It's the second-highest-grade silver mine in the world right now."

The strategic significance of the Crescent acquisition lies in infrastructure utilisation rather than in resource growth alone. Higher throughput across existing shafts, mills, and fixed infrastructure would spread operating costs over more tonnes processed, creating operating leverage without major new capital requirements.

De-Risking the Underground Infrastructure

Americas Gold & Silver identified hoisting capacity as the primary constraint on production growth following the Galena consolidation. Phase 2 upgrades to the No. 3 Shaft increased average hoisting rates from 42 tonnes per hour to 85 tonnes per hour by installing a new hoist motor, upgraded braking systems, communications infrastructure, and modernised control systems. This increase of more than 100% removed the operational bottleneck that limited ore movement from underground workings to the surface and created the infrastructure required to support higher mining rates.

The upgraded shaft has also enabled the transition from conventional underhand cut-and-fill mining to mechanised long-hole stoping. The long-hole stoping cycles are approximately 12 times faster than the legacy mining method and have increased productivity by more than 300%. The company is constructing a paste fill plant, targeting it as a prerequisite for expanding long-hole stoping to approximately 70% of mining activity by the second half of 2027.

Turner linked productivity gains directly to margin expansion:

“And the more tonnes that you move with the same equipment, the lower your operating cost per tonne, so you're expanding margins in both directions.”

Production Growth Is the Operational Test

The central operational objective is converting completed infrastructure upgrades into sustained production growth. Management's targeted increase in daily mining rates represents an approximate 50% increase from current production levels. Achieving that target would demonstrate that investments in hoisting capacity, mine development, and mechanised mining are translating into higher throughput.

The significance extends beyond production volumes alone. Higher utilisation of existing infrastructure would spread fixed operating costs across a larger production base while increasing the contribution from mechanised mining methods. The resulting improvement in operating efficiency is a key component of management's strategy to improve margins and generate stronger cash flow from the Galena Complex.

The market's valuation discount suggests investors remain focused on execution risk rather than infrastructure completion. Future operating results will therefore provide the clearest measure of whether the company's capital investments are delivering the productivity gains implied by the current growth strategy.

Byproduct Monetisation & The US Antimony Joint Venture

Silver remains the primary economic driver of the Galena Complex. Turner described the role of byproducts within the operating model:

"We're always going to be focused as a primary silver producer. We're about 75% to 80% exposed to the metal right now. But these byproducts are extremely helpful in bringing down those costs over time."

Galena produced approximately 561,000 pounds of antimony during 2025 and has produced more than 20 million pounds since 2001. The operation is currently the largest active antimony mine in the US. Because antimony is mined alongside silver and copper, additional antimony revenue can be generated without incremental mining activity.

Americas Gold & Silver has formed a joint venture (JV) with United States Antimony Corporation, with Americas holding a 51% ownership interest. Management is targeting completion of a domestic antimony processing facility by mid-2027. The facility is designed to process antimony already produced at Galena, increasing revenue per tonne mined by adding a downstream processing margin that is currently captured elsewhere in the supply chain.

Valuation & Capital Structure

Americas Gold & Silver is trading at approximately 0.60 times NAV, compared with an average of approximately 1.06 times NAV for intermediate and senior silver producers. The discount exists despite a balance sheet that management believes is sufficient to fund current growth initiatives.

The company held approximately $122 million in cash and had drawn only $50 million from a $100 million debt facility. Available liquidity is funding shaft infrastructure, underground development, fleet modernisation, paste fill construction, mill upgrades, and an approximately 64,000-metre exploration program.

Turner outlined management's focus on operational delivery:

"We want to make sure that we execute quarter after quarter on that growth strategy and that all comes down to project execution."

The valuation gap will likely be determined by operating performance rather than financing. If management demonstrates that infrastructure upgrades and mechanised mining are translating into higher production rates and lower unit costs, investors will have a measurable basis for reassessing the current discount to peer valuations.

Investment Thesis for Americas Gold & Silver

- The company has removed its primary underground production bottleneck by increasing hoisting capacity from 42 tonnes per hour to 85 tonnes per hour, creating the infrastructure required to support higher mining rates.

- The acquisition of the Crescent Mine provides additional feed sources for 1,558 tonnes per day of installed milling capacity while current mining rates remain below available processing capacity, allowing production growth without constructing a new processing facility.

- The transition from conventional underhand cut-and-fill mining to mechanised long-hole stoping has increased productivity by more than 300% and is targeting lower unit operating costs through higher tonnes mined per shift.

- A 51%-owned antimony-processing joint venture and a balance sheet with $122 million in cash provide exposure to critical minerals while funding the next phase of operational growth.

- The Galena Complex contains more than 200 million ounces of silver resources at an average grade of approximately 500 grams per tonne, providing a large, high-grade inventory capable of supporting production growth over multiple years.

TL;DR

Americas Gold & Silver has completed infrastructure upgrades that doubled hoisting capacity at the Galena Complex and is targeting production growth through mechanised mining and spare mill capacity. The strategy combines existing infrastructure, productivity improvements, and antimony monetisation to increase production without requiring the construction of a new processing facility. The next test is whether those investments can deliver higher throughput and lower operating costs, supporting a re-rating from the company's current valuation discount.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed