Battery Metals & the Copper Conundrum: The Critical Link in Global Electrification

Copper emerges as the critical backbone of battery metals supply chains, driving electrification with surging demand from EVs, renewables, and energy storage systems.

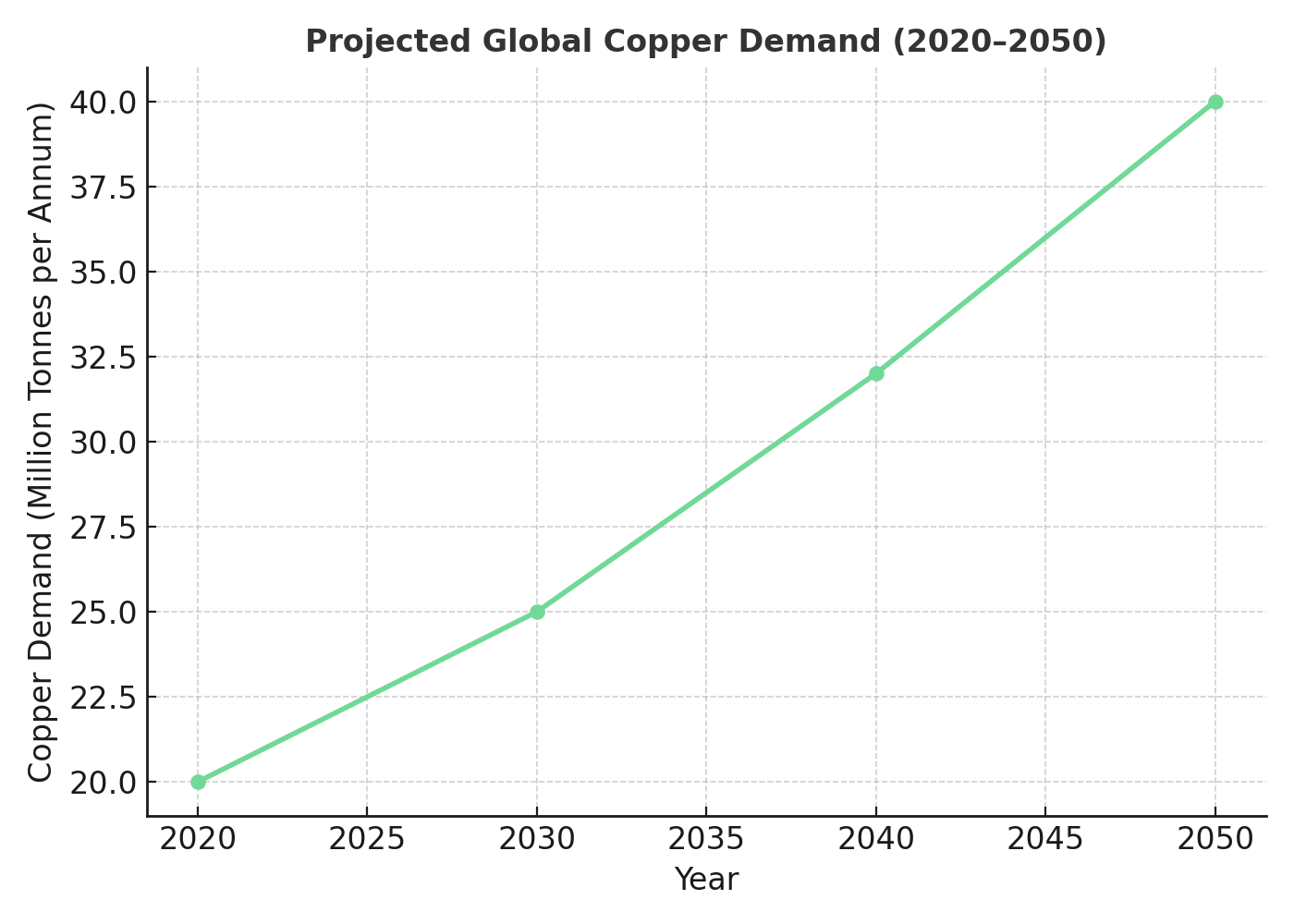

- Copper demand is projected to double from 20 million tonnes per annum to 40 million tonnes by 2050, driven primarily by battery energy storage systems, electric vehicle infrastructure, and renewable energy networks that require 3-4 times more copper than traditional applications.

- The global copper supply crisis is intensifying as ore grades have declined 40% since 1990 while development timelines have extended from 12.3 to 16.3 years, creating a dangerous lag between discovery and production precisely when electrification demand is accelerating.

- Battery energy storage system installations are multiplying copper requirements exponentially, with the US adding 1.5 GW in Q1 2025 alone and Wood Mackenzie forecasting a 1.4 TW global shortfall requiring US$1.2 trillion in copper-intensive infrastructure investment by 2034.

- Junior exploration companies with high-grade, near-surface deposits in tier-one jurisdictions are positioned to capitalize on supply constraints, with projects like Canada Nickel's Crawford (DFS Q4 2025), Rome Resources' DRC operations (maiden resource September 2025), and Gladiator Metals' Whitehorse Belt exploration offering strategic exposure to the copper supply gap.

- The convergence of ESG requirements, supply chain reshoring initiatives, and geopolitical considerations has created premium valuations for North American copper assets, while polymetallic projects like Sovereign Metals' Kasiya (combining rutile and graphite by-products) demonstrate how integrated approaches can optimize battery metals value chains.

While lithium, nickel, and cobalt dominate battery metals headlines, copper has quietly emerged as the indispensable backbone of global electrification. The metal's role extends far beyond traditional wiring applications, positioning it as a critical component in battery storage systems, electric vehicle infrastructure, and renewable energy networks. By 2050, copper demand is forecast to double from 20 million tonnes per annum to 40 million tonnes, driven primarily by battery storage, electric vehicles, and 5G/AI infrastructure development. The supply-demand imbalance has created unprecedented opportunities for junior exploration companies with strategic assets in tier-one jurisdictions, particularly those developing near-surface, high-grade deposits. As the energy transition accelerates, copper's status as both a conductor and an enabler of battery technology makes it perhaps the most undervalued component of the battery metals complex. The convergence of declining ore grades, extended development timelines, and surging electrification demand has created a perfect storm that could reshape global copper markets within the next decade.

Copper's Pivotal Role in the Battery Revolution

Beyond Conductivity: Copper as Battery Infrastructure

Copper's relationship with battery metals extends well beyond its traditional role as a conductor. In battery energy storage systems (BESS), copper forms the critical infrastructure that enables grid-scale storage solutions. The rapid expansion of BESS installations globally, with the US adding 1.5 GW in Q1 2025 alone, representing a 57% year-over-year increase. This directly translates to massive copper consumption. Each gigawatt-hour of battery storage requires approximately 3-4 tonnes of copper for inverters, transformers, cables, and grid connections.

Tesla's emergence as the leading BESS (Battery Energy Storage System) integrator in 2023 with a 15% market share exemplifies how the convergence of electric vehicles and energy storage amplifies copper demand. The company's 60% year-over-year growth in North America demonstrates the exponential scaling effect, where each new installation multiplies copper requirements across multiple applications. This integration trend creates a compounding effect on copper demand that traditional forecasting models may underestimate.

A forecast of a 1.4 TW global shortfall in grid-forming batteries by 2034 represents approximately US$1.2 trillion in investment, and potentially 4.2-5.6 million tonnes of additional copper demand. This massive infrastructure buildout positions copper as the metal most directly leveraged to the energy storage boom, with exposure that rivals or exceeds traditional battery metals like lithium and nickel.

The Electric Vehicle Multiplication Effect

The electric vehicle revolution has fundamentally altered copper's demand profile, with each EV requiring 3-4 times more copper than internal combustion vehicles. Beyond the vehicles themselves, the charging infrastructure represents an often-overlooked copper consumption multiplier. Fast-charging stations require substantial copper for high-voltage cables, transformers, and grid connections, with each DC fast-charger consuming approximately 50-100 kg of copper.

The regional buildout patterns reveal significant implications for copper supply chains. In Asia-Pacific, where Chinese battery manufacturers like CATL and BYD dominate with over 40% of global stationary LFP cell production, copper demand from integrated EV-battery manufacturing complexes is creating localized supply pressures. European expansion forecasts show 7× battery capacity growth by 2030, translating to an increase in investment potential from €30 billion to €80 billion, much of which will be copper-intensive infrastructure.

Middle Eastern markets present particularly compelling copper demand stories, with Saudi Arabia targeting top-10 global storage market status by 2025 through 11 GWh of planned capacity, while the UAE launches 19 GWh solar plus storage systems. These projects, predominantly supplied by Chinese integrators, represent concentrated copper demand that could strain regional supply chains.

The Global Supply Crisis: Why Junior Exploration Matters Now

Structural Supply Constraints

The copper industry faces unprecedented structural challenges that make new discoveries increasingly critical. Ore grades have declined 40% since 1990, meaning miners must process significantly more material to produce the same amount of copper. This grade decline directly impacts energy consumption, processing costs, and environmental footprint - factors that become increasingly important as ESG considerations drive investment decisions.

.png)

Development timelines have extended from an average of 12.3 years to 16.3 years, creating a dangerous lag between discovery and production at precisely the moment when demand acceleration requires rapid supply responses. The pipeline problem is severe: only 10 of 30 major copper projects forecast in 2014 have actually been built, highlighting the execution challenges facing large-scale developments.

Perhaps most concerning is the collapse in grassroots exploration budgets, which have dropped from 50-60% of total exploration spending to just 28%. This reduction in early-stage exploration creates a discovery gap that will manifest as supply shortages in the 2030s, precisely when electrification demand reaches peak acceleration.

Junior Exploration & Development

These supply constraints have created exceptional opportunities for junior exploration companies with strategic assets. Projects that combine high grades, near-surface geometry, and tier-one jurisdictions offer compelling economics that larger producers struggle to replicate through brownfield expansion or complex greenfield developments.

As Canada Nickel CEO Mark Selby aptly notes:

"If you're a CEO of a company in a metal that's not one of the core ones or the flavour of the month, you have to spend time doing this. Otherwise you will be dead in the water."

This reality has intensified focus on strategic positioning and narrative clarity among junior mining companies across all battery metals, not just the headline-grabbing lithium and cobalt stories. Canada Nickel is currently advancing its flagship Crawford project through definitive feasibility study (DFS) completion scheduled for Q4 2025, with the project boasting a 2nd largest global nickel reserve at 3.8 Mt and targeting 48 ktpa peak production over a 41-year mine life.

Gladiator Metals, located in the Whitehorse Copper Belt in Yukon, Canada exemplifies this opportunity. With established grid hydro power, road access, and proximity to infrastructure, projects in this region avoid the massive capital expenditures typically required for remote copper developments. The absence of fly-in/fly-out requirements and existing workforce availability create operational advantages that translate directly to project economics.

High-grade intersections like those seen at Cowley Park - 98 meters at 1.49% copper with 187 ppm molybdenum - demonstrate the grade advantages available through focused junior exploration. These grades compare favorably to global averages and offer the potential for low-cost, heap-leach processing that minimizes both capital requirements and environmental impact.

Polymetallic Advantages in Battery Metal Supply

The emergence of molybdenum as a battery-relevant metal adds another dimension to copper exploration strategies. Molybdenum's role in steel alloys that support battery manufacturing infrastructure, combined with potential direct applications in next-generation battery chemistries, creates polymetallic value propositions that pure-play copper projects cannot match.

Projects with copper-molybdenum mineralization offer revenue diversification that improves project economics and reduces single-commodity price risk. As battery technology evolves toward long-duration storage applications requiring new material combinations, polymetallic deposits provide optionality that could prove increasingly valuable.

Regional Supply Chain Reshoring & North American Strategic Positioning

The geopolitical dimensions of battery metals supply chains have elevated copper's strategic importance. US and EU legislation pushing for domestic battery manufacturing and supply chain resilience creates premium value for North American copper production. Projects in stable jurisdictions with established infrastructure and regulatory frameworks command premium valuations due to supply chain security considerations.

Canada's position as both a stable democracy and a mining-friendly jurisdiction makes Canadian copper projects particularly attractive to international battery manufacturers seeking supply chain diversification away from Chinese dominance. The combination of political stability, established mining expertise, and existing infrastructure creates compelling investment conditions for battery metals supply chains.

The integration of First Nations partnerships into modern mining development adds both social license advantages and operational stability. Capacity funding agreements and community engagement protocols demonstrate how modern exploration companies can build sustainable, long-term relationships that support project development while respecting Indigenous rights and environmental stewardship.

ESG & Sustainable Mining Practices

Environmental, social, and governance considerations have become central to battery metals supply chain decisions. Copper projects that demonstrate strong ESG credentials command premium valuations and preferential access to capital markets. Near-surface deposits with lower energy requirements, reduced water consumption, and minimal environmental disturbance align with the sustainability objectives of battery manufacturers and their end customers.

Gladiator Metals leadership exemplifies this evolved approach to community engagement. As one executive notes:

"I would much rather have positive community engagement, acceptance and social license than be remote and have overbearing capital requirements or other challenges with what being remote brings."

This philosophy reflects how modern mining companies recognize that social license represents both risk mitigation and competitive advantage. Gladiator Metals is currently advancing exploration across the Whitehorse Copper Belt with 12,000 meters planned at Cowley Park and 10,000 meters at Little Chief in 2025, while pursuing Class 3 permit approval and building on high-grade intersections including 98 meters at 1.49% copper with 187 ppm molybdenum.

Legacy environmental cleanup and community investment programs demonstrate how responsible exploration companies can create positive social impacts while advancing their projects. STEM education initiatives, youth support programs, and local workforce development create lasting benefits that extend well beyond mine life cycles.

The emphasis on environmental restoration and habitat protection reflects the evolving expectations for mining operations in developed jurisdictions. Projects that integrate environmental stewardship from the exploration phase through to eventual closure demonstrate the responsible resource development that modern capital markets increasingly demand.

Advanced Processing Technology & By-Product Optimization

The evolution of copper processing technology has created new opportunities for smaller-scale, more efficient operations. Sovereign Metals demonstrates this trend through its Kasiya project in Malawi, which combines the world's largest rutile resource (17.9 Mt) with the second-largest flake graphite resource (24.4 Mt). The company has achieved ultra-low incremental costs of US$241/t for graphite production as a by-product of rutile operations, with DFS completion scheduled for Q4 2025 targeting 265 ktpa graphite output. This integrated approach showcases how polymetallic projects can optimize revenue streams across multiple battery-relevant commodities.

Heap leach processing, particularly for oxide and mixed oxide-sulfide ores, offers capital-efficient extraction methods that make previously marginal deposits economically viable. These technologies are particularly relevant for near-surface deposits where conventional mining methods would be over-engineered.

The integration of digital technologies and automated processing systems allows smaller operations to achieve efficiency levels previously available only to major producers. Real-time monitoring, predictive maintenance, and optimized extraction protocols maximize recovery rates while minimizing operational costs and environmental impact.

Selective mining techniques that target high-grade zones within broader mineralized systems optimize capital deployment and maximize early cash flows. This approach is particularly effective for projects with multiple prospects, allowing companies to develop high-return areas first while preserving expansion optionality for future phases.

Infrastructure Advantages & Capital Efficiency

Access to existing infrastructure creates significant capital advantages for well-positioned copper projects. Grid power availability eliminates the need for on-site generation, reducing both capital costs and operational complexity. Road access and proximity to established communities minimize transportation costs and workforce challenges that plague remote developments.

The availability of experienced mining contractors and support services in established mining regions reduces project risk and accelerates development timelines. Access to specialized equipment, maintenance capabilities, and technical expertise creates operational advantages that translate directly to project economics and execution certainty.

Near-surface geology that enables open-pit mining methods minimizes capital requirements compared to underground operations while maximizing operational flexibility. The combination of surface mining, established infrastructure, and proven processing technologies creates a development pathway that minimizes execution risk while maximizing returns.

Market Fundamentals & Investment Implications

The copper market stands at an inflection point where traditional supply sources struggle to meet accelerating demand from electrification applications. The concentration of existing production in politically unstable regions creates supply security concerns that premium North American production directly addresses.

Long-term price forecasts reflect the structural supply deficit developing over the next decade. Conservative estimates suggest copper prices must rise significantly to incentivize the capital investment required to meet projected demand, creating favorable conditions for new production from economically viable deposits.

The time lag between copper price signals and new supply response creates extended periods of elevated prices that benefit existing producers and advanced development projects. Companies with near-term production capabilities are positioned to capitalize on these favorable market conditions while avoiding the execution risks associated with longer-term developments.

Strategic Value Creation

The convergence of supply constraints, demand acceleration, and geopolitical considerations creates multiple value creation pathways for strategically positioned copper assets. Beyond traditional mining returns, these projects offer strategic value to integrated battery manufacturers and technology companies seeking supply chain security.

The optionality value of polymetallic deposits increases as battery technology evolves and material requirements expand. Projects with diverse mineral inventories provide exposure to multiple commodity markets while maintaining focused development strategies that minimize execution complexity.

Acquisition premiums for high-quality copper assets reflect the strategic value of secured supply chains in an increasingly complex geopolitical environment. Major producers and technology companies increasingly view equity investments or acquisition strategies as essential for long-term competitiveness in battery metals markets.

Energy Transition Technology Evolution & Copper Demand Acceleration

The evolution of battery technology toward long-duration storage applications will likely increase rather than decrease copper intensity per unit of energy storage. Grid-forming batteries that provide frequency regulation and voltage support require additional copper infrastructure compared to simple energy storage applications.

The integration of artificial intelligence and 5G networks creates additional copper demand layers that compound electrification trends. Data centers supporting AI applications require massive copper infrastructure for power distribution and cooling systems, while 5G networks demand extensive copper cabling for high-speed data transmission.

Emerging applications in electric aviation, marine electrification, and industrial process electrification represent demand categories that current forecasting models may underestimate. These applications often require specialized copper products and infrastructure that command premium pricing and create additional market opportunities.

Investment Strategy Implications

The copper supply-demand imbalance creates compelling investment opportunities across the development spectrum, from grassroots exploration through advanced development projects. Companies with high-grade deposits in tier-one jurisdictions offer exposure to potentially exponential value creation as supply deficits develop.

The emphasis on ESG compliance and supply chain transparency favors companies with strong community relationships, environmental stewardship records, and transparent operational practices. These factors increasingly influence capital allocation decisions and determine access to both debt and equity financing.

Strategic partnerships with established mining companies, technology firms, or end-users provide development capital while validating technical and commercial viability. These relationships often create value beyond traditional financing by providing technical expertise, market access, and operational support that accelerate development timelines.

Copper Market Review by Merlin Marr-Johnson

For Investors

The energy transition has fundamentally altered copper's role from a traditional industrial metal to a critical component of the global battery metals complex. The intersection of supply constraints, demand acceleration, and geopolitical considerations creates unprecedented opportunities for companies with strategic copper assets in tier-one jurisdictions.

The supply gap developing over the next decade cannot be filled by existing operations or announced developments, creating an imperative for new discovery and development. Projects that combine high grades, near-surface geometry, established infrastructure access, and strong ESG credentials offer the best combination of economic returns and execution certainty.

As the battery metals sector continues to evolve, copper's role as the enabling infrastructure for electrification becomes increasingly critical. The companies that successfully develop high-quality copper assets in the next five years will be positioned to capture exceptional value as the energy transition accelerates and supply constraints intensify.

The convergence of technological innovation, regulatory support, and capital market evolution creates a uniquely favorable environment for copper development. Companies that recognize and act on these opportunities while maintaining strong operational and environmental standards will define the next chapter of the global energy transition.

Analyst's Notes

Subscribe to Our Channel

Stay Informed