Brent's Drop Below $80 Shifts the Risk for Fuel-Intensive Equities From Supply Shock to Fed Timing

Iran's return of 25 million barrels pushed Brent below $80, with ceasefire stability and Fed policy now driving the next move in oil prices.

- US and Iranian negotiators signed a memorandum of understanding in Switzerland extending the ceasefire by at least 60 days.

- Iran's export waivers allowed more than 25 million barrels of oil to reach international markets, increasing near-term global supply.

- ANZ forecasts 2 million to 3 million barrels per day of supply returning within four weeks, while its downside case leaves up to 2 million barrels per day offline for an extended period.

- Keir Starmer's resignation increased political uncertainty, making UK gilt and sterling valuations more sensitive to future fiscal policy decisions.

- Fresh military strikes could restore a geopolitical risk premium and push Brent back toward $82.30 a barrel.

Ceasefire Extension & Brent's Drop Below $79

Oil prices fell after US-Iran talks in Switzerland reduced the risk of further supply disruptions. Brent fell 2.5% to $79.22 a barrel, while WTI August futures declined to $75.29.

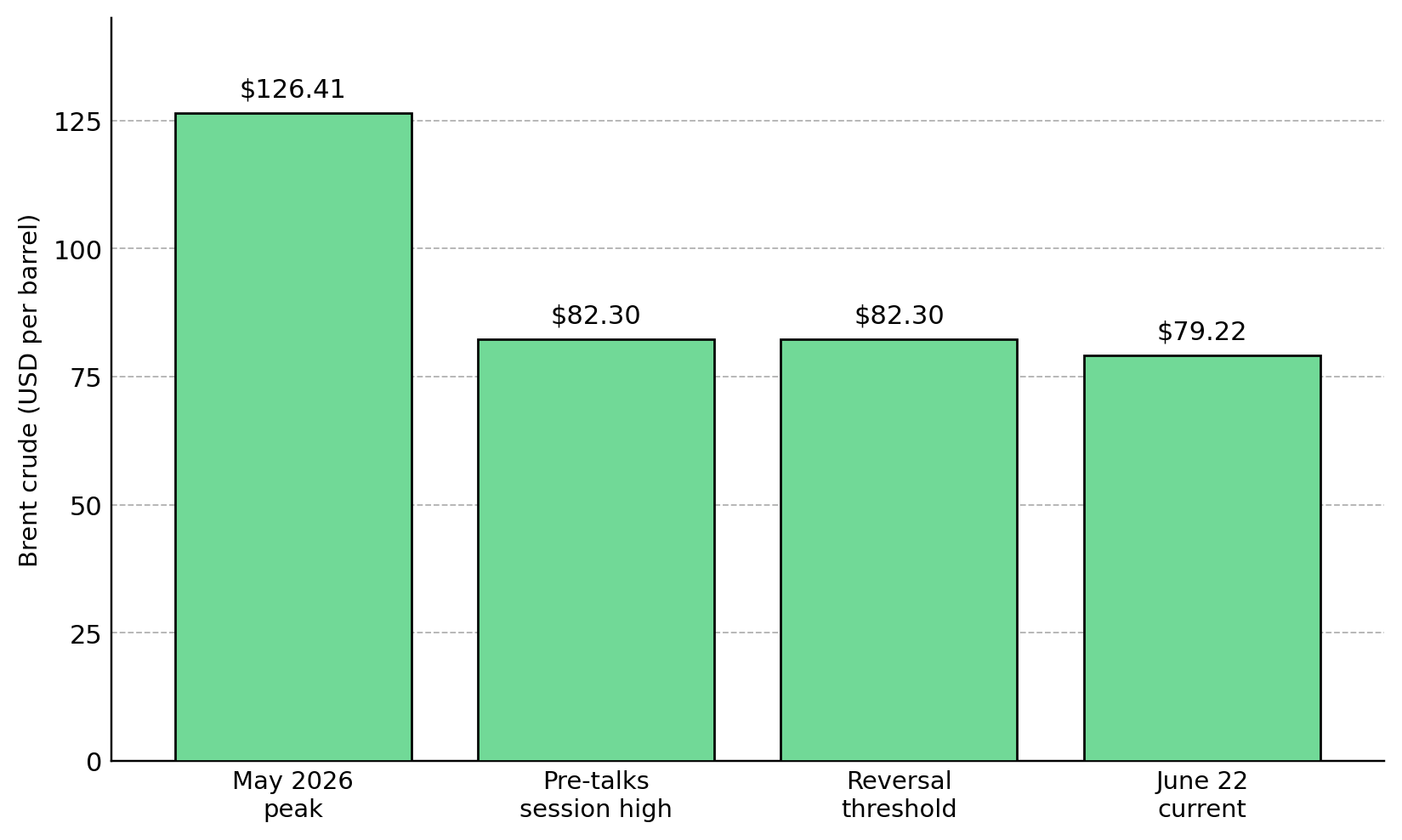

Brent traded as high as $82.30 before ceasefire talks reduced supply-risk concerns. The rally reflected renewed fears of military escalation and disruption to oil flows through the Strait of Hormuz. Progress in the talks shifted market focus from supply disruption to the return of Iranian and Gulf crude exports.

Iran Export Waivers & Rising Global Oil Supply

Oil prices fell as export waivers allowed Iran to resume crude shipments and increase global supply. More than 25 million barrels of Iranian oil have returned to export markets since the waivers took effect. Iraq is targeting crude output of 4.2 million to 4.3 million barrels per day, with additional cargoes from the UAE and Kuwait adding to regional supply.

The 60-day ceasefire extension has reduced the immediate risk of disruption to oil flows through the Strait of Hormuz. Oman, Qatar, and Pakistan said negotiators are working toward a permanent agreement during the ceasefire period. The agreement has supported shipping activity after vessel traffic through the waterway fell to 32 ships. Any breakdown in negotiations could renew closure risks and quickly restore a geopolitical premium to oil prices.

Lower oil prices reduce one of the largest variable cost inputs for mining operations. Diesel and heavy fuel oil account for 20% to 35% of total cash costs at most open-pit and underground mines, meaning a sustained Brent price below $80 a barrel directly expands operating margins without requiring any change in production volume or ore grade.

Export Recovery & Delayed Production Restart

Oil exports are recovering faster than production, delaying a full restoration of supply. ANZ expects shipping activity to drive the initial recovery, with upstream and refinery operations unlikely to return to full capacity before year-end.

Oil prices now depend on whether the 60-day ceasefire holds. ANZ's base case restores 2 million to 3 million barrels per day of global supply within four weeks. Continued regional stability could return an additional 2 million to 3.5 million barrels per day in the third quarter. A supply setback could leave 1 million to 2 million barrels per day offline for an extended period.

For mining equities specifically, the lag between export recovery and full upstream restart extends the window of below-$80 Brent, giving cost-sensitive operators a margin tailwind that precedes any volume-driven demand recovery in industrial metals.

Tighter Fed Policy & Rising Borrowing Costs

Lower oil prices are being offset by tighter Fed policy and higher borrowing costs. Markets are pricing a 75% chance of a September rate hike and 41 basis points of tightening by year-end, lifting 2-year Treasury yields to 4.23% and strengthening the US dollar. Higher rates and a stronger dollar increase financing costs for rate-sensitive and dollar-funded sectors.

The key risk is that inflation remains high enough to force the Fed to raise rates sooner than markets expect. JPMorgan's Fabio Bassi expects the first rate hike in the second half of 2027 but warns that stronger inflation could bring forward the tightening cycle.

Political uncertainty has increased risk for UK assets. Gilt markets are assessing whether a new government could change fiscal policy and increase public spending. UK bond and currency markets may remain volatile until the leadership transition clarifies fiscal policy.

Renewed Supply Risk & Brent's $82.30 Reassessment Point

The 60-day ceasefire has kept Brent near $79.00 to $80.00 a barrel, well below May's peak of $126.41. Lower oil prices support fuel-intensive sectors while Iranian export waivers continue to add supply to the market.

A breakdown in the Switzerland talks or renewed military escalation could disrupt oil flows through the Strait of Hormuz and push Brent back toward $82.30 a barrel. The yen is trading near its 40-year low of 161.96 per dollar, increasing the likelihood of intervention by Japanese authorities.

The yen's position near its 40-year low of 161.96 per dollar raises the probability of Japanese intervention, adding a currency transmission channel to an already multi-variable price environment. Mining equities leveraged to fuel-intensive operations, particularly open-pit copper, gold, and iron ore producers, are the direct beneficiaries of the current price range, but that margin advantage compresses immediately if the Strait of Hormuz disruption scenario pushes Brent back above $82.30.

Analyst's Notes

Subscribe to Our Channel

Stay Informed