Cabral Gold (TSX-V: CBR) - PFS and Construction Decision Planned for the Oxide Blankets

Interview with Alan Carter, President & CEO of Cabral Gold (TSX-V: CBR)

Cabral Gold Inc. is a mineral exploration company focused on gold and copper. The company's key assets include the Cuiú Cuiú Project in Northern Brazil, the Tapajos Region, and the Bom Jardim project. The company was founded in 2016 and is headquartered in Vancouver, Canada.

Merlin-Marr Johnson caught up with Alan Carter, President, CEO, and Director, Cabral Gold. Dr. Carter is a Co-founder at Peregrine Metals Ltd. and Cuprum Resources Ltd. He currently serves as a Director and Chairman at both Fremont Gold Inc. and Altamira Gold Corp. His educational credentials include a B.Sc. degree in Geology from the University of Nottingham, U.K., and a Ph.D. in gold geochemistry and structural geology from the University of Southampton, U.K. He also co-founded Magellan Minerals Inc. which was acquired by Anfield Gold Corp. in 2016. Alan founded Cabral Gold in late 2016 and took the company public in November 2017.

Company Overview

Cabral Gold is a publicly-traded company focused on advancing its flagship, district-scale Cuiú Cuiú Gold Project in Brazil. The company is looking to grow its existing resource through trenching, sampling, and drilling. Magellan Brazil and Cabral Gold B.C. Inc. are the company’s subsidiaries. It is listed on the Toronto Stock Exchange (TSX-V: CBR), the OTC Markets (OTCQX: CBGZF), and the Frankfurt Stock Exchange (FRA: C3J).

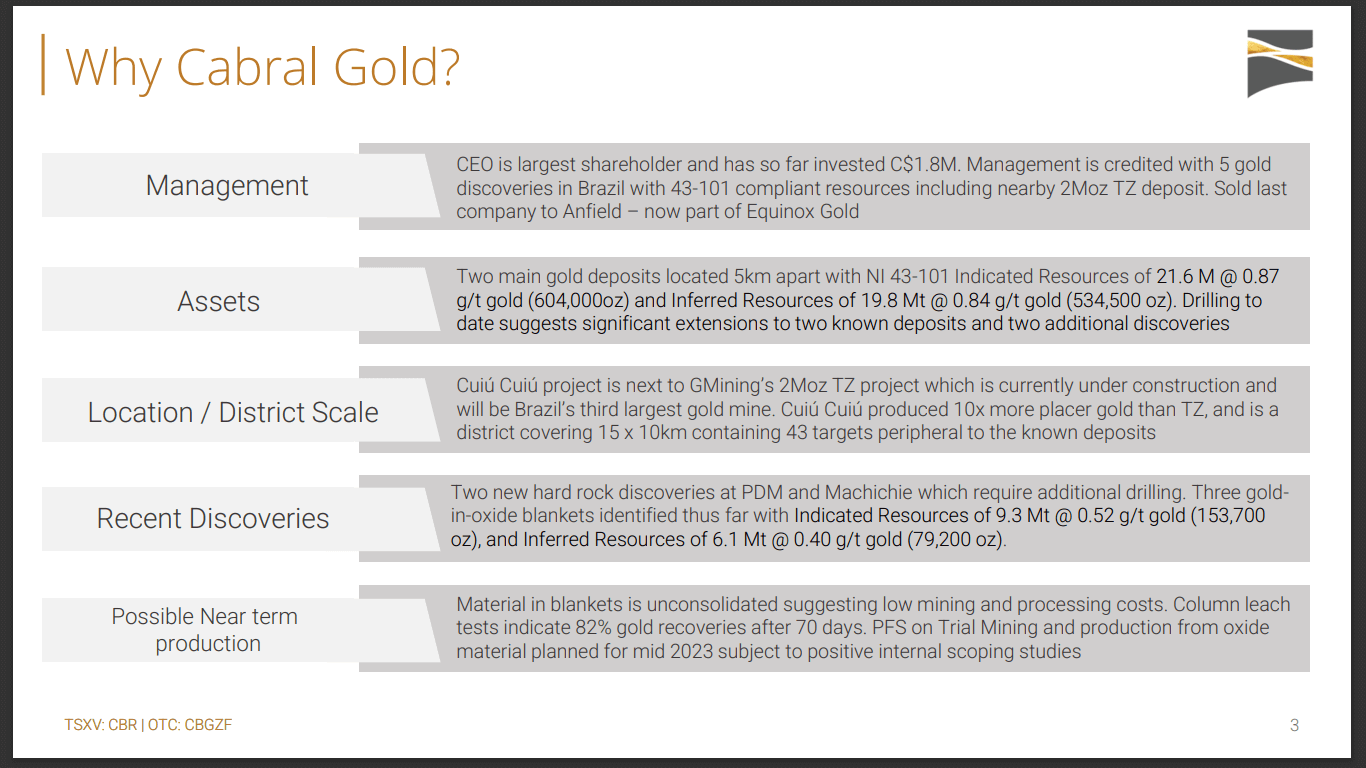

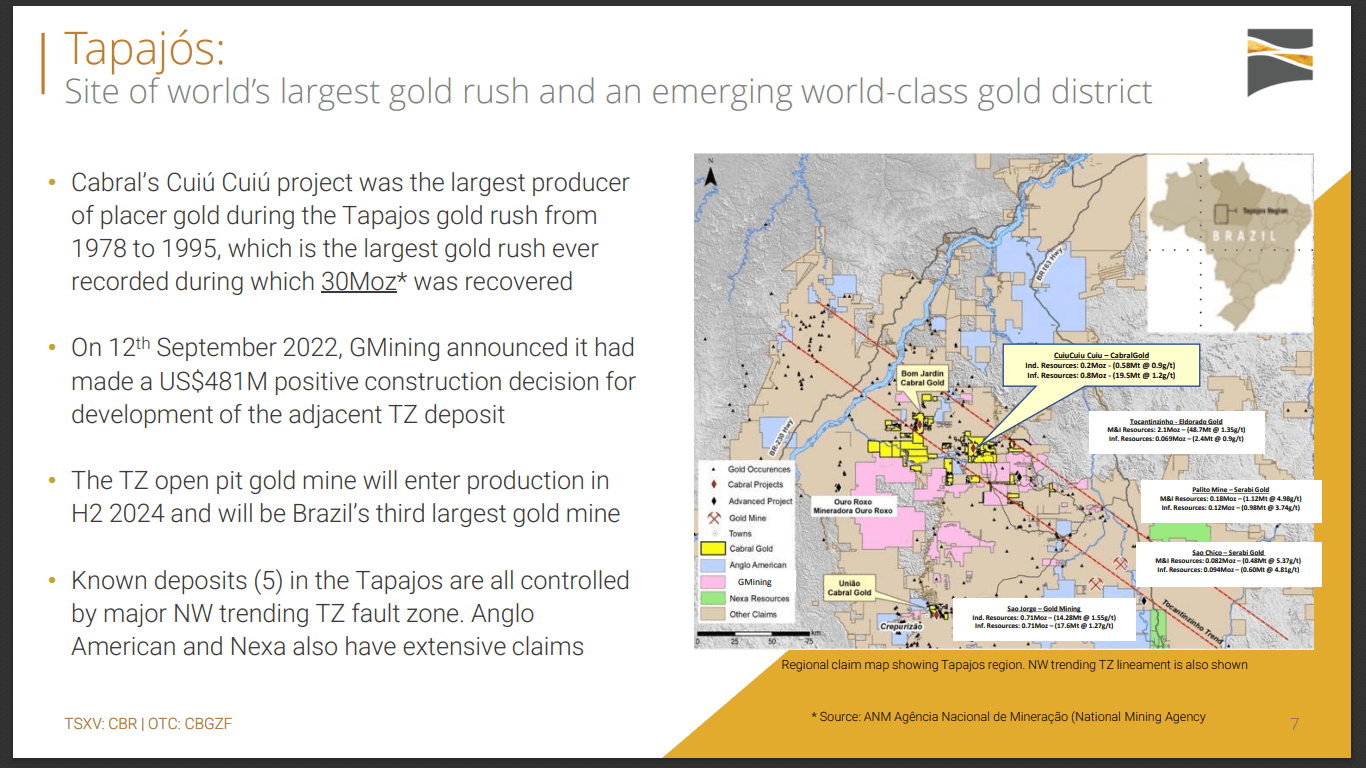

Cabral Gold has an advanced exploration project in Brazil called the Cuiú Cuiú Project. It is based in the Tapajós region, which is the site of one of the world’s largest-ever gold rushes. Here, the company has 2 gold deposits with resources totaling almost 1.2Moz. Over the last 12 months, the company has made 2 discoveries.

The Market Landscape

The last 12 months have been extremely challenging for the mining industry. This is a difficult time, despite the fact that the company has added a lot of value to the project. It has expanded the deposit along with the resources and several new discoveries. The company has also outlined a lot of oxide mineralization on the surface, along with some spectacular drill results. Last year, the company put out a total of 29 press releases, many of which had excellent drill results. Despite this, the challenging market environment has made it increasingly difficult to operate.

On the flip side, the company believes that there are some fantastic opportunities available in the mining sector. Cabral Gold is a company with extremely strong fundamentals. The company has been successful in strengthening its position over the past 12 months.

In recent times, the gold price has recovered by about $250/oz. It is up from $1,620/oz at the beginning of November. It is evident that some of the speculative money is coming back to the market. Last year, the speculative investments were definitely out of flavor, which posed a problem. This was the case not only with the gold exploration stocks but anything that was speculative and without cash flow. Investors fled the market, leading to a drop in share prices across a series of different sectors. According to the company, most sectors are speculative. If the gold price continues to appreciate, there will be a cascade of interest and money from the gold price into major gold companies through the mid-tiers before it eventually arrives in the junior companies.

The juniors offer the most leverage. In 2020, Cabral Gold went up by 8 times in the space of a few months. While there are discussions surrounding the continued improvement of the gold price, the high inflation environment has raised concerns about an upcoming recession. A recession has been traditionally beneficial for gold in the past. There is also a lot of political instability around, including the Russia-Ukraine crisis. Additionally, some of the issues in the cryptocurrency space are also expected to fare positively for the gold market.

In 2023, the gold market fundamentals are expected to be extremely strong. Investors looking to invest more in the speculative exploration space and the gold exploration space are looking at companies with significant gold assets. The company recently updated the resource, bringing the combined inferred and indicated resources to almost 1.2Moz. Investors will be looking at projects with a significant upside.

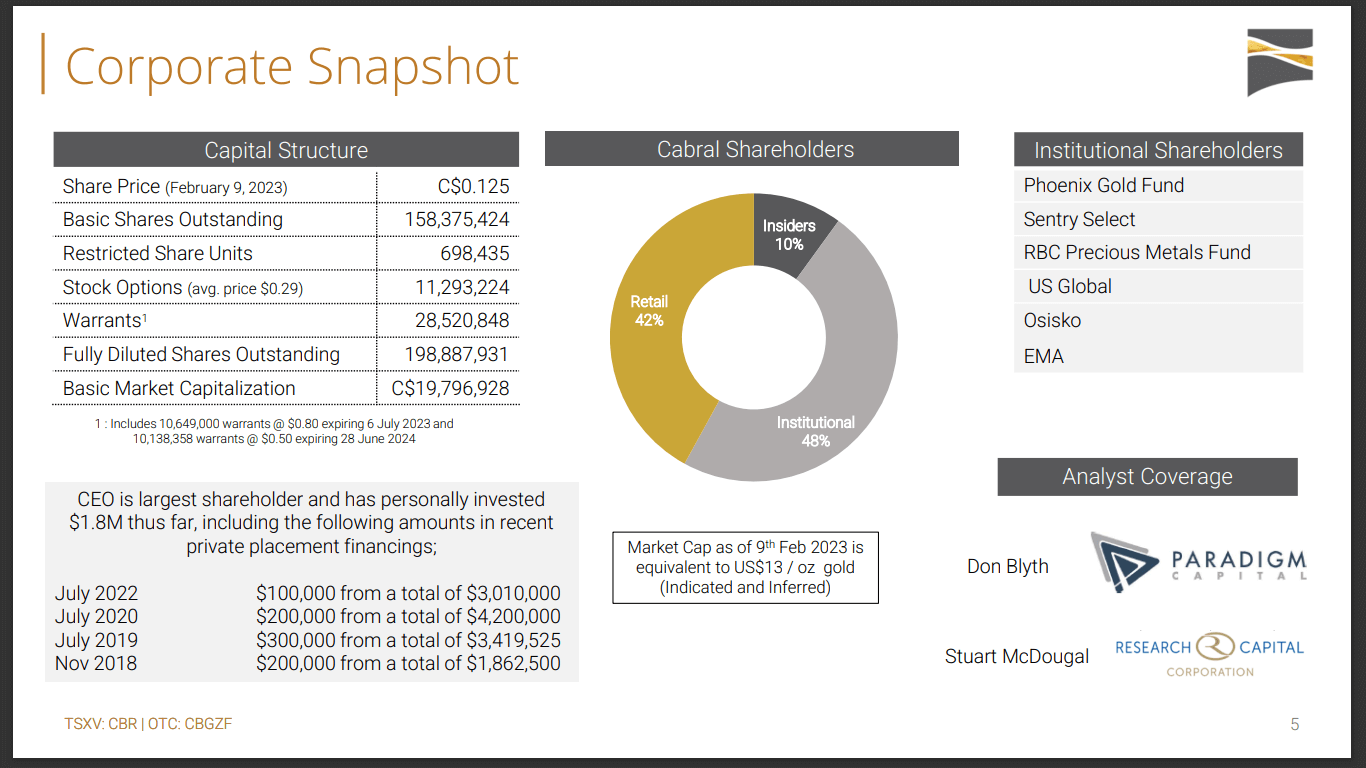

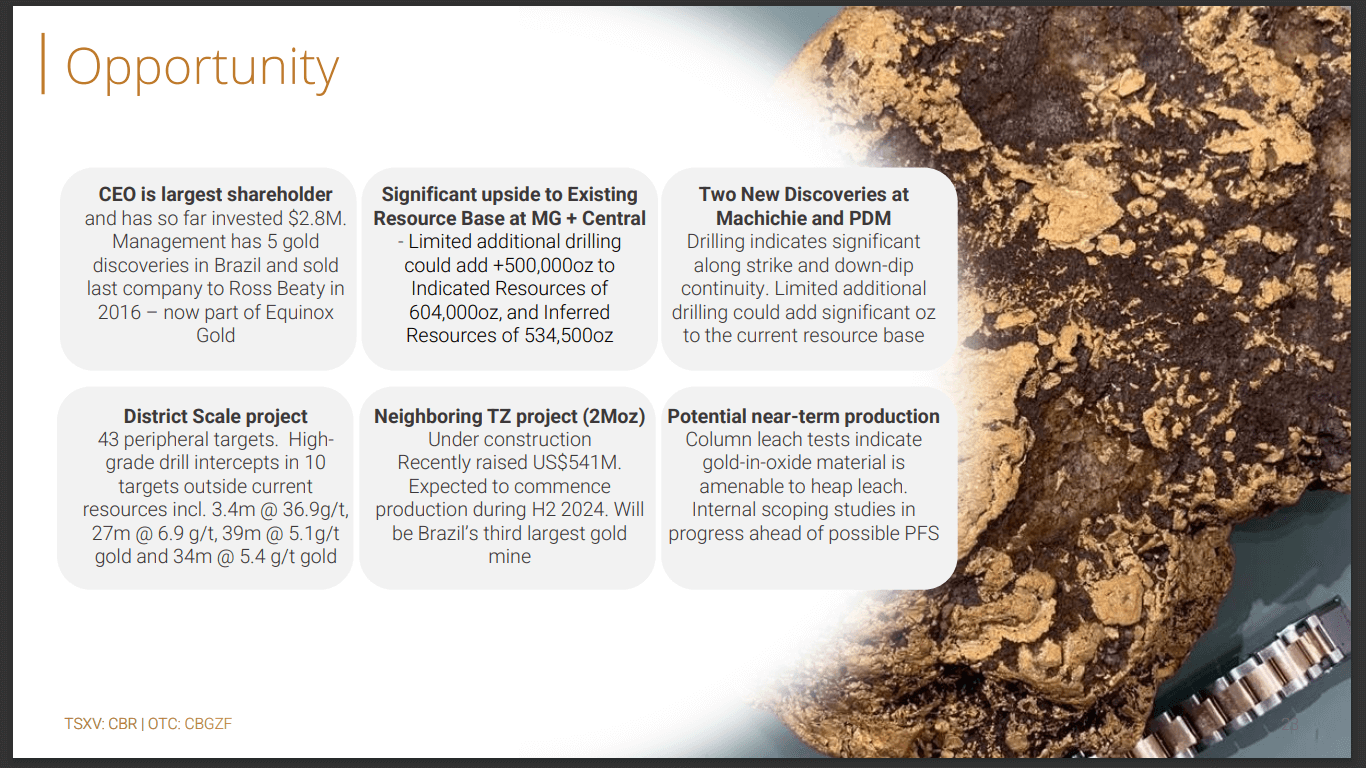

Cabral Gold has made several discoveries in recent times, which makes it a compelling investment opportunity. Investors are looking at companies with significant news flow and companies where the management has a sizable stake. Alan Carter, Cabral Gold’s CEO has invested $2.8M of his personal wealth into the company. This shows that the company is aligned with shareholders.

Cabral Gold’s operations are based in Brazil, which is considered a good jurisdiction. Since there’s no winter period in the country, mining can be carried out throughout the year. Investors are looking for teams that have had exploration success. In the last 2 decades, the company’s management team has made 5 discoveries. The company has also demonstrated that it can raise capital even during difficult periods.

Cash Position

In November 2022, Cabral Gold announced a $2M capital raise. The raise was open and the company was able to get the first tranche down at about $1.2M. The company did not complete the second tranche as it ran into a wall of selling due to the tax loss selling season. During this time, people offset the tax gains by selling stocks that have dropped in value. In late November or early December, the company traded around 15M shares. The company is currently waiting to see how things progress. In the exploration sector, the aggressiveness of a company is dependent on access to capital. The past 12 months have been extremely difficult for raising money, which ends up dictating the company’s aggressiveness on the exploration program and a plan moving forward. The company anticipates that 2023 will be a lot better than the previous year.

Due to the limited availability of funds, the company had to stop operating the 5 rigs that were deployed at Cuiú Cuiú in the second quarter of 2022. The company is currently in cash conservation made. It is cognizant that the current market conditions are extremely difficult for raising capital. There has been a jump in the gold price, which is expected to lead to a better market environment in the coming months.

In July 2022, the company raised capital at $0.30. The funds raised in the middle of last year were at $0.54. It has been a downward trend, despite the company posting excellent drill results and new discoveries. According to the company, the market’s appetite has gone steadily worse during the last year. In the last 6-9 months, the appetite for speculative stocks including exploration stocks, junior tech stocks, and junior pharmaceutical stocks has been largely absent.

Operational Strategy

Similar to the vast majority of junior exploration companies, Cabral Gold’s strategy has been to raise capital, drill, make a discovery, and work on growing the discovery. Following this, the company is looking to focus on resource expansion, which can help the share price. While this is possible to achieve during a rising market, over the past few years, the market has seen limited, short-lived growth cycles.

According to Cabral Gold, this trend isn’t specific to junior exploration companies. The strategy is similar to a junior pharmaceutical company trying to find the next blockbuster drug. Projects have costs and ongoing costs. However, revenue is absent as a result of ongoing research and development. In the case of Cabral Gold, it requires capital for drilling and exploration. The company also needs to expend capital to pay geologists, listing fees, press release fees, and other expenses. In the past few years, there have been relatively few periods where the market is trending in an upward direction.

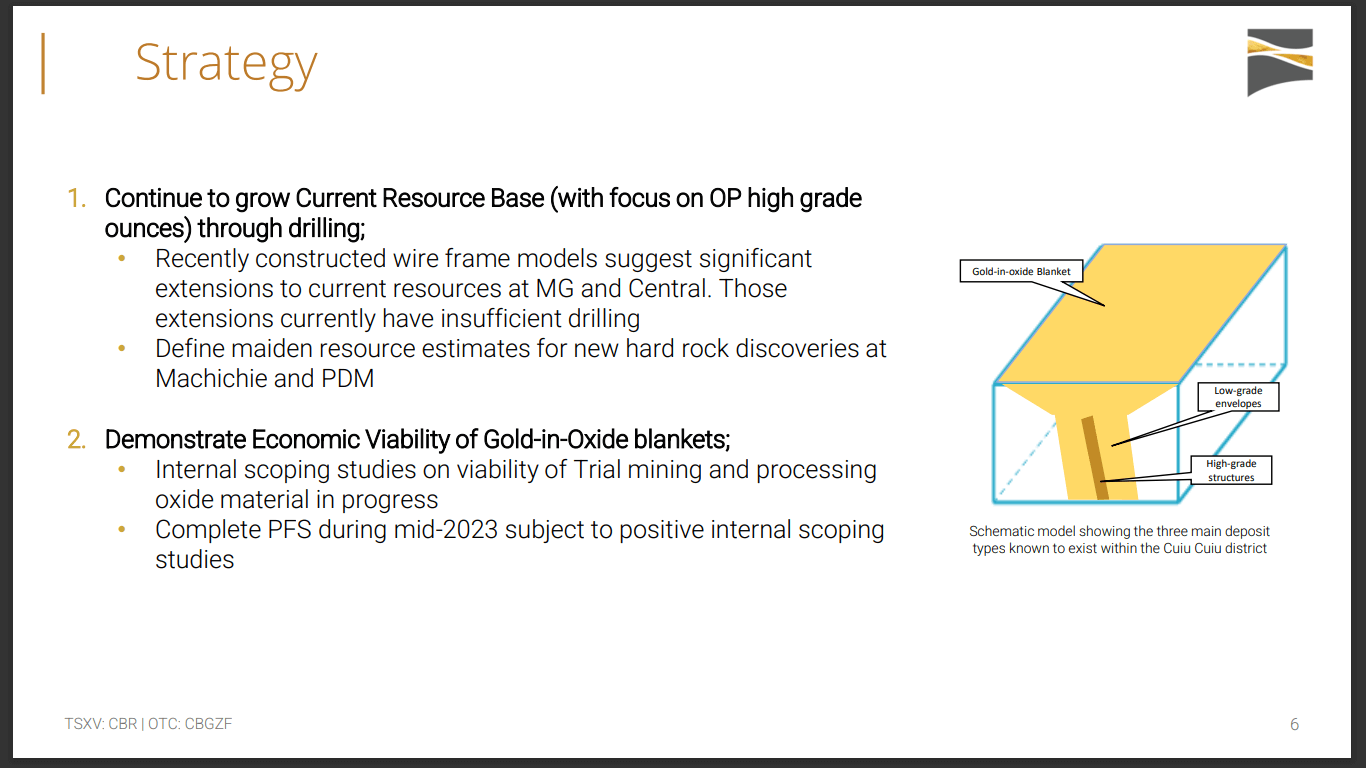

Cabral Gold has the opportunity to step off the hamster wheel, which is unusual for a junior exploration company. The company is fortunate to have a 250,000oz gold resource, and it believes that the deposit has the potential for significantly more oxide mineralization. The material is weathered from underlying rock featuring gold deposits that form the bulk of the existing resource. The material has been weathered in-site for millions of years. The company currently has 50m-60m of weathered material which comprises saprolite, mud, soil, and sand sitting above the deposits which are located on hilltops.

Since the material is extremely weathered, it is soft and can be dug with hands. As a result, the mining costs for the material are expected to be very low as it does not require any drilling or blasting. Similarly, the company wouldn’t require a big mill with lots of different crushing and grinding circuits to process the material. It does not need to reduce the hard material to a fine powder, because nature has already done the hard legwork.

Last year’s metallurgical results indicate the presence of oxide material that is sitting on the surface. The oxide material allows for very good gold recoveries through heap leaching. Notably, heap leaching is employed in about 300 mines around the world and it is the cheapest way to recover gold. The company has the opportunity to get the oxide material into production pretty quickly and generate some cash flow. This means that the company is not dependent on going to the market for equity raises, which would lead to continual dilution of the capital structure.

The company has carried out a lot of internal work on the oxide blankets. In 2023, the company is looking to conduct a PFS (Preliminary Feasibility Study) on producing from the oxide material. The company would require a little more capital to execute the plan. While the company is yet to put out anything in terms of the economic viability of the oxide material, looking at comparable operations, it is evident that there’s a capital cost associated with bringing the heap leach into operation. The margins make this an amazing revenue-generation opportunity. One of the key objectives this year is to advance the idea and complete a PFS, subject to the availability of capital. The company has the opportunity to step off the hamster wheel and get into production fairly quickly.

In terms of financing, the company is examining all available options going forward. It does not intend on waiting for the market to improve. One of the financing options includes the disposal of some non-core assets. The company has a few exploration claims with limited drilling outside of Cuiú Cuiú. Selling non-core assets can help raise capital. Having a resource in a non-core asset offers a certain value, which is expected to be relatively modest given the market conditions. According to the company, the appetite from larger companies to pick up the non-core assets is largely absent in the current market environment.

A lot of companies seem reticent and are not making the most of the current market cycle. Instead, the companies are content with paying much higher prices when capital is readily available. In the case of a joint venture, the major often seeks a majority interest in the project. While this may be desirable for a major company, it isn’t ideal for a junior company or its shareholders.

This is because usually the major comes in and pays all the exploration costs, and drilling expenses. The junior company either sits back or operates using its own capital. The problem arises when the project is shaping up to be a significant deposit and the major ends of farming on the opportunity. The major company will always want a majority stake, at which point they farm after 2-3 years, eventually gaining control of the asset. As a result, the junior company no longer has control over the project’s direction.

This way, the major ends up earning 51%, 60%, or 70%, while the junior company is left with a minority interest. At this point, the major decides on a much bigger program which comes with a much larger share of the cost going forward. As the junior company is unable to raise that kind of capital, it gets diluted. In most cases, this isn’t a viable route for most junior exploration companies and it isn’t in the best interest of shareholders either. Notably, the situation would be different in the case of a non-core asset.

Ongoing Operations

Cabral Gold has a CAD$25M current market cap. It has inferred and indicated resources just under 1.2Moz. Converting the resources on a per-ounce basis comes out to about USD$16/oz. Taking the current cash flow out of the situation, the company is being valued at around $15/oz, against a $1,870/oz gold price.

The company anticipates that the current gold price offers an enormous opportunity for most people, given the new discoveries and the exceptional drill results. It is important to note that the company does not have any resources at the moment. It anticipates that the resources are larger than what the current resource statement suggests. In order to determine the scale of the resource, the company would need to drill additional holes.

Cabral Gold’s current valuation on a per ounce basis is around $15, which is close to the historic lows. According to the company, the actual value of the resource in the ground is closer to $50/oz to $100/oz. In a rising market environment, companies would expect to trade at least in the $50/oz-$100/oz range, some of them trading at up to $200/oz. The deposit offers a lot of upside potential. The company is looking to demonstrate the economic viability of the oxide material as quickly as possible to show the investors that it has the route to step off the hamster wheel while ensuring that the capital structure isn’t continually diluted.

If the share prices start to improve, the company will contemplate raising additional capital which will enable it to drill holes into the deposits and develop some maiden resources. The company hopes to get this done in 2023 through capital raises and additional drilling. The Machichi and PDM discoveries have amazing drill holes and are located 2km from the 2 existing deposits. There are 2 more discoveries where about 6,000m-7,000m is drilled in each hole. The company is looking to drill another 5,000m or 6,000m to get to a resource statement on both discoveries. In the last 12 months, the results published on the 2 discoveries have been highly promising. Towards the end of last year, the company reported material grades of 5m at 27.6g/t at Machichi, which was on top of 6.4m at 11.6g/t. The results indicate that there’s a high-grade zone emerging at Machichi.

Cabral Gold has also published some excellent results at the PDM deposit with material grades of 12m at 3.3g/t and 18m at 2.5g/t. The company anticipates that there is a new deposit emerging at PDM, which could potentially be as big as Central or even larger. If the market continues to improve along with investor appetite, the company expects to be in a strong position among exploration stocks. According to the company, people should look at the management cash invested, management track record, the asset, the jurisdiction, the year-round news flow, and the upside potential before investing in the sector.

Targets 2023 and Beyond

Cabral Gold has been conducting a lot of internal scoping work that hasn’t been published to the market. Because of the rules, the company is precluded from doing so. Over the course of the next few months, the company intends on taking the internal work and rolling it into a PFS. While the timing is not guaranteed, the company is looking to get it done as fast as possible, subject to capital availability. The timing for this strategy largely depends on the company’s ability to raise money quickly and the speed at which the markets improve.

The company’s top priorities are as follows. The first priority is to demonstrate the economic viability of the oxide blanket in terms of the PFS. The second priority is to continue expanding the resource by getting additional drilling done on the 2 new discovery zones. The third priority is to carry out additional drilling work at the MG and PDM deposits. While the company has been actively looking at the disposal of non-core assets, 99% of its effort has been focused on Cuiú Cuiú over the last few years. It does not intend to parcel the project up.

The company does have the option to carry out a PEA, but it is expected to take some time. Instead, the company is focused on going straight to a PFS as it offers a much higher degree of confidence around project economics. The majority of the oxide material is currently in the indicated category. The company has over 600,000oz of indicated material. It was one of the big success stories from the updated resource statement that was published a few months ago. The company was able to achieve a 250% growth in the indicated resource base, going from 160,000oz - 180,000oz to well over 600,000oz. There’s a similar amount of inferred material present as well.

Cabral Gold currently has close to 50 different targets, many of them with fantastic drill holes. While a lot of targets remain to be tested, the drill results so far have been promising. The company anticipates that there could be a number of additional deposits at Cuiú Cuiú. The company would need additional capital in order to determine the economic viability of the deposits. The company is looking to drill an additional 12,000m at Machichi and PDM and another 5,000m on the Central and the 2 existing deposits. At a $250oz all-in cost, a 20,000m drill program is expected to cost $5M. The company would need an additional $1M as a buffer, bringing the overall capital requirements to $6M.

It is difficult to raise capital in the current market conditions. The company is cognizant that patience is key as the market can turn very quickly in the junior exploration space. In mid-2021, the company carried out an $11.5M bought deal at $0.54. Since then, the project has gotten significantly bigger in terms of ounces in the ground and new discoveries.

Cabral Gold estimates that it would require around $1M in capital in order to get the PFS done. A completed PFS will enable the company to reach a construction decision on Cuiú Cuiú. Normal mines take several years to build, however, a small oxide operation has the potential to generate cash very quickly. An ongoing cash flow would prevent the company from further dilution.

A junior company, despite having fantastic exploration success can still struggle when the market conditions have been unfavorable over a long period of time. These conditions have led people to flee the sector, which results in a further drop in prices. Companies need to raise capital to pay for costs and stay afloat. The current market landscape serves as an amazing investment opportunity in the sector. Over the last few weeks, there have been indications that the market recovery has started. When the market does bounce back, investors positioned in stocks with strong fundamentals are likely to make the most of the opportunity.

The gold price is currently about $1,870, while Cabral Gold’s is valued at less than 1% of the material in the ground, or at $15/oz. The company considers this as an opportunity as a lot of value can be unlocked through operations. Cabral Gold is cognizant that it is a difficult issue to nail down because the company needs access to capital in order to complete the milestones and execute the plan. In the short term, the company intends to continue demonstrating the economic viability of the oxide blankets. It has some exceptional metallurgical tests from last year. The company is also prioritizing a PFS study in order to move the project toward a construction decision in the coming months.

As the share price starts to trend upward, the company will consider raising additional money through equity to fund drill operations that would add ounces at the base level of the resource. At the same time, the company will continue to look at deals on non-core assets.

On the institutional side of the equation, the funds are largely dried up. Over the last few months, the company raised some institutional money. Given the current market valuation, some of the investors and fund managers recognize that there’s a massive opportunity. According to the company, the market’s appetite for investment appears to be gradually increasing. This is driven by the decline in other investment classes and the rise in gold pricing. A $250 rise in the gold price has caught the attention of a lot of people. The fundamentals for the gold pricing are quite strong and the company anticipates that institutional money is starting to come back into the junior resource stocks.

Cabral Gold’s management is aligned with the shareholders. The company isn’t looking to raise capital at the expense of significantly diluting the capital structure. According to the company, investors should have a long-term view when investing in speculative exploration stocks. While people might make money over a 6-18 month period, the investment can be crushed by market cycles. Instead, holding a stock for 5-7 years can offer significant returns on investment. When taking a long-term view, it is important to choose a company with strong fundamentals, strong assets, good management teams, good jurisdictions, and lots of upside.

To find out more, go to the Cabral Gold website

Analyst's Notes

Subscribe to Our Channel

Stay Informed