Concentrated PGM Supply Drives Platinum Stockpiling as CME Inventories Reach 624,000 Ounces

Section 232 review drives platinum positioning as CME inventories reach 624,000 ounces, highlighting concentrated PGM supply risks and diversification trends.

- A Section 232 critical minerals status report is due to the US President by July 13, 2026, and the review's 50-mineral list includes platinum, palladium, rhodium, ruthenium, and iridium.

- Platinum held in CME-approved warehouses has risen from 270,000 ounces at the start of 2025 to 624,000 ounces as end users pay to hold metal in US warehouses ahead of the July 13 Section 232 decision.

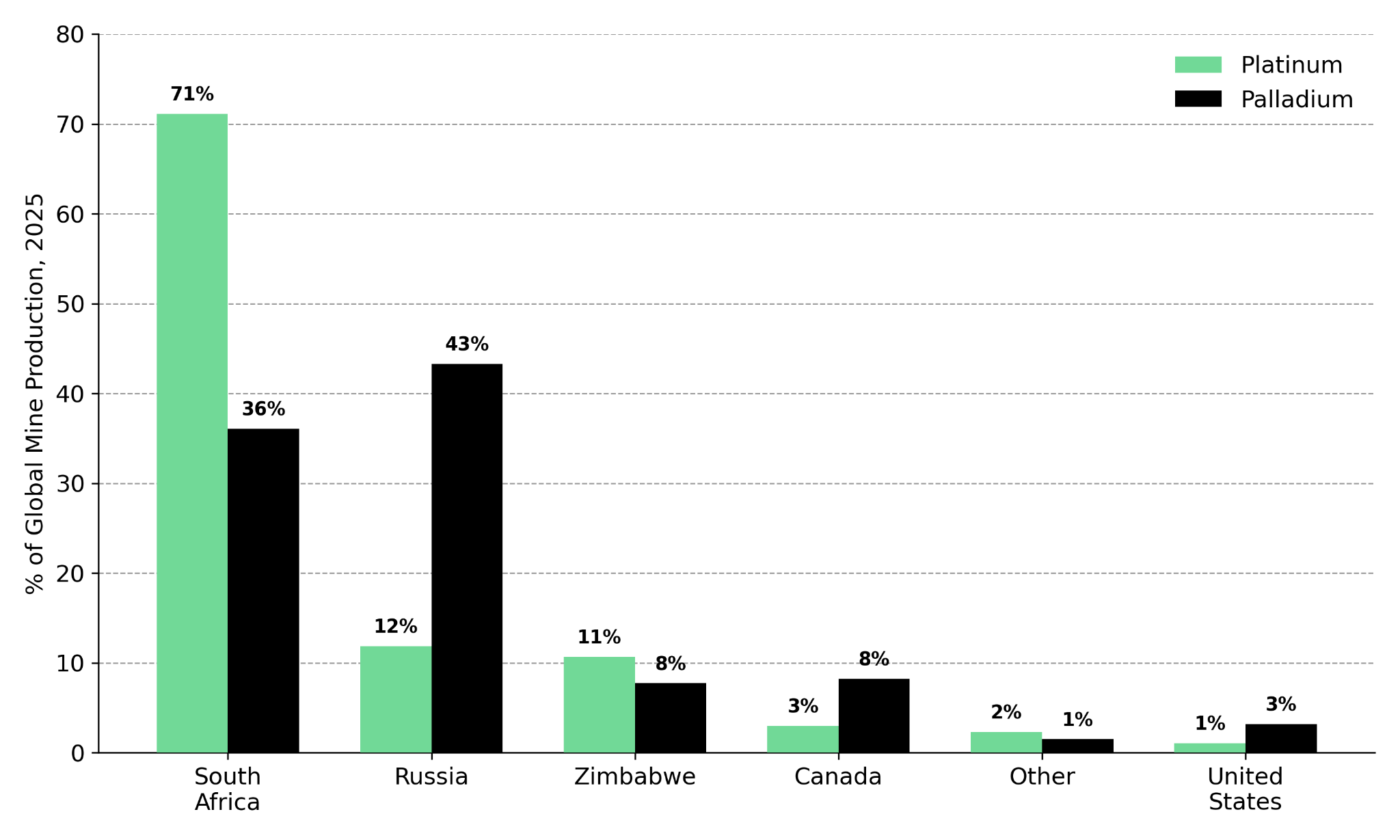

- South Africa supplied about 71% of global platinum mine output in 2025, while Russia and South Africa together supplied an estimated 70% to 80% of global palladium. That supply concentration existed long before the Section 232 review, making the policy a catalyst for an existing risk rather than its cause.

- Exploration outside the dominant South Africa-Russia supply base offers geographic diversification, though most projects remain at the pre-economic study stage.

- The review has already changed physical platinum positioning, with rising CME inventories showing that buyers are moving metal into the US before any tariff decision.

Limited PGM Substitution & Critical Minerals Policy Raise Supply Risk

The US Department of Commerce's Bureau of Industry and Security opened a Section 232 investigation into processed critical minerals and their derivative products in April 2025 and submitted its final report to the President on October 24, 2025. On January 14, 2026, the President directed Commerce and the US Trade Representative (USTR) to negotiate trade measures with global partners within 180 days instead of imposing immediate tariffs, setting a July 13, 2026, deadline. The review covers 50 minerals, including lithium, cobalt, rare earth elements such as neodymium, and platinum, palladium, rhodium, ruthenium, and iridium. That places PGMs inside the same policy review as battery materials, extending its relevance beyond the energy transition metals that have received most attention.

The report's outcome remains uncertain until its release, making current market positioning more informative than attempts to predict the final policy. What can already be measured is how end users have positioned ahead of the July 13 deadline through rising physical platinum inventories. The increase in CME-approved platinum inventories from 270,000 ounces at the start of 2025 to 624,000 ounces shows that buyers are moving metal into US warehouses before the policy decision, regardless of the review's final outcome. PGMs warrant separate attention because many end users have limited substitution options. Automotive catalyst manufacturers, industrial glass producers, and electronics fabricators cannot easily replace PGMs with alternative materials, making supply disruptions more difficult to offset than in many battery mineral markets.

Supply Concentration & Platinum Market Exposure Increase Disruption Risk

A trade policy focused on national security and import dependence places the greatest attention on commodities with concentrated sources of supply. PGMs have one of the most geographically concentrated supply chains on the 50-mineral list, making existing production concentration more important than the review's final outcome.

South African Supply Concentration & Platinum Production Raise Supply Risk

South Africa supplied about 71% of global platinum mine output in 2025, with production falling 4% year over year to 3.965 million ounces after flooding and maintenance disruptions at operations including Valterra Platinum's Amandelbult complex, according to Metals Focus data compiled for WPIC. Eskom has gone more than a year without scheduled load-shedding, shifting the primary production risk from electricity shortages to declining ore grades and operational disruptions. That changes the main drivers of South African supply risk even though the country's share of global platinum production remains unchanged.

Russian Palladium Supply & Ore Grade Decline Increase Supply Risk

Russia and South Africa together supply an estimated 70% to 80% of global palladium output, and Russia's largest producer, Norilsk Nickel, is targeting a 2% decline in 2026 production because of lower ore grades. Because palladium supply is concentrated in a small number of producers, even a 2% production decline at Norilsk Nickel can tighten the global market more than a similar reduction in a more geographically diversified commodity.

Temporary Platinum Surplus & Falling Inventories Keep Markets Tight

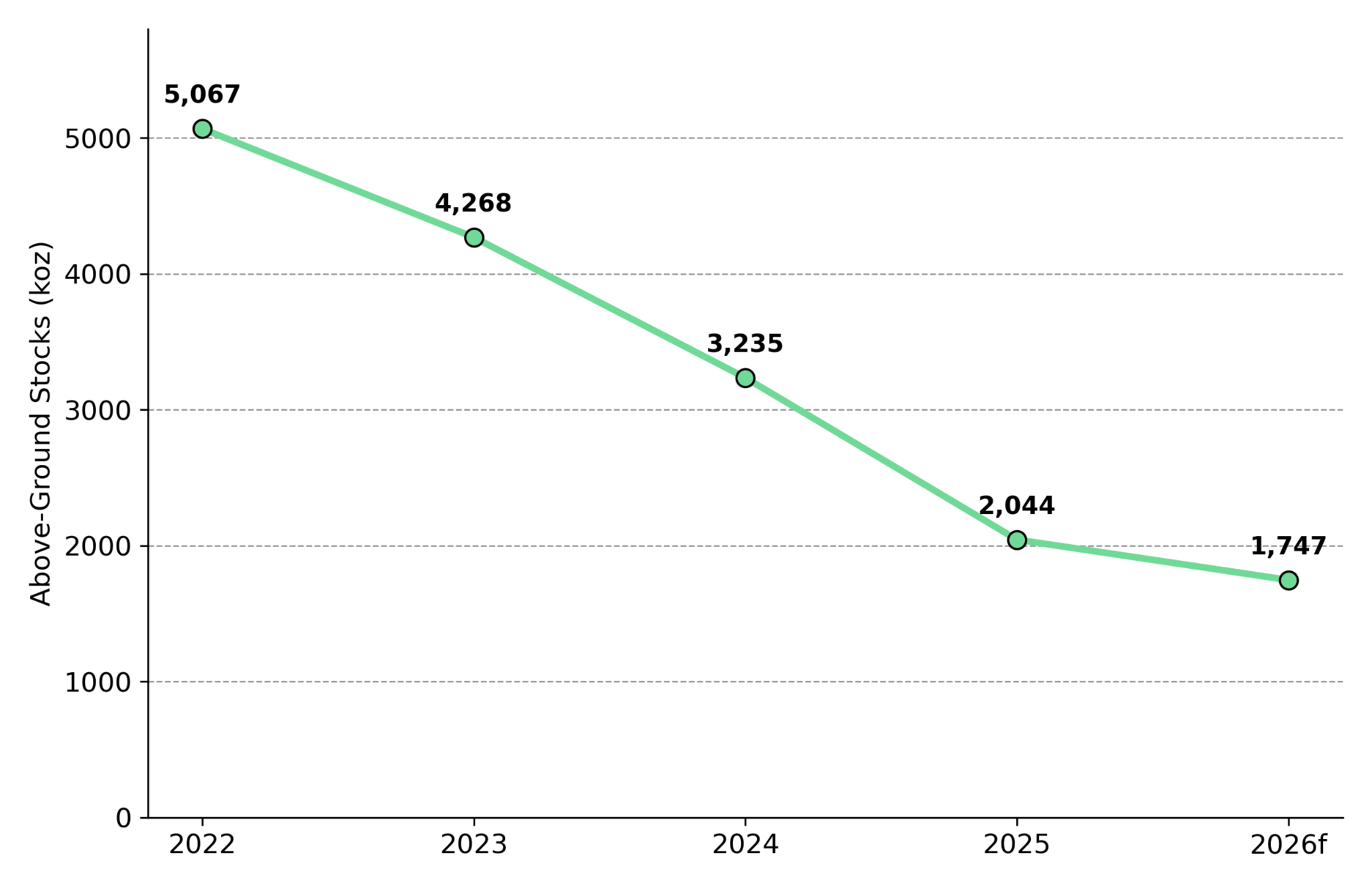

WPIC's Platinum Quarterly, published on May 18, 2026, shows that the platinum market shifted sharply between supply surplus and tighter inventory expectations during 2026. The platinum market recorded a first-quarter 2026 surplus of 268,000 ounces as supply rose 18% year over year to 1.736 million ounces on unseasonably strong South African production. Demand fell 31% year over year to 1.468 million ounces as exchange-traded fund and exchange warehouse outflows totaled 374,000 ounces. WPIC forecasts full-year 2026 demand will fall 9% year over year to 7.674 million ounces. Even so, above-ground stocks are projected to decline to less than three months of global demand by year-end, leaving the market more exposed to supply disruptions in South Africa or Russia.

Trade Policy Uncertainty & Physical Platinum Positioning Signal Market Expectations

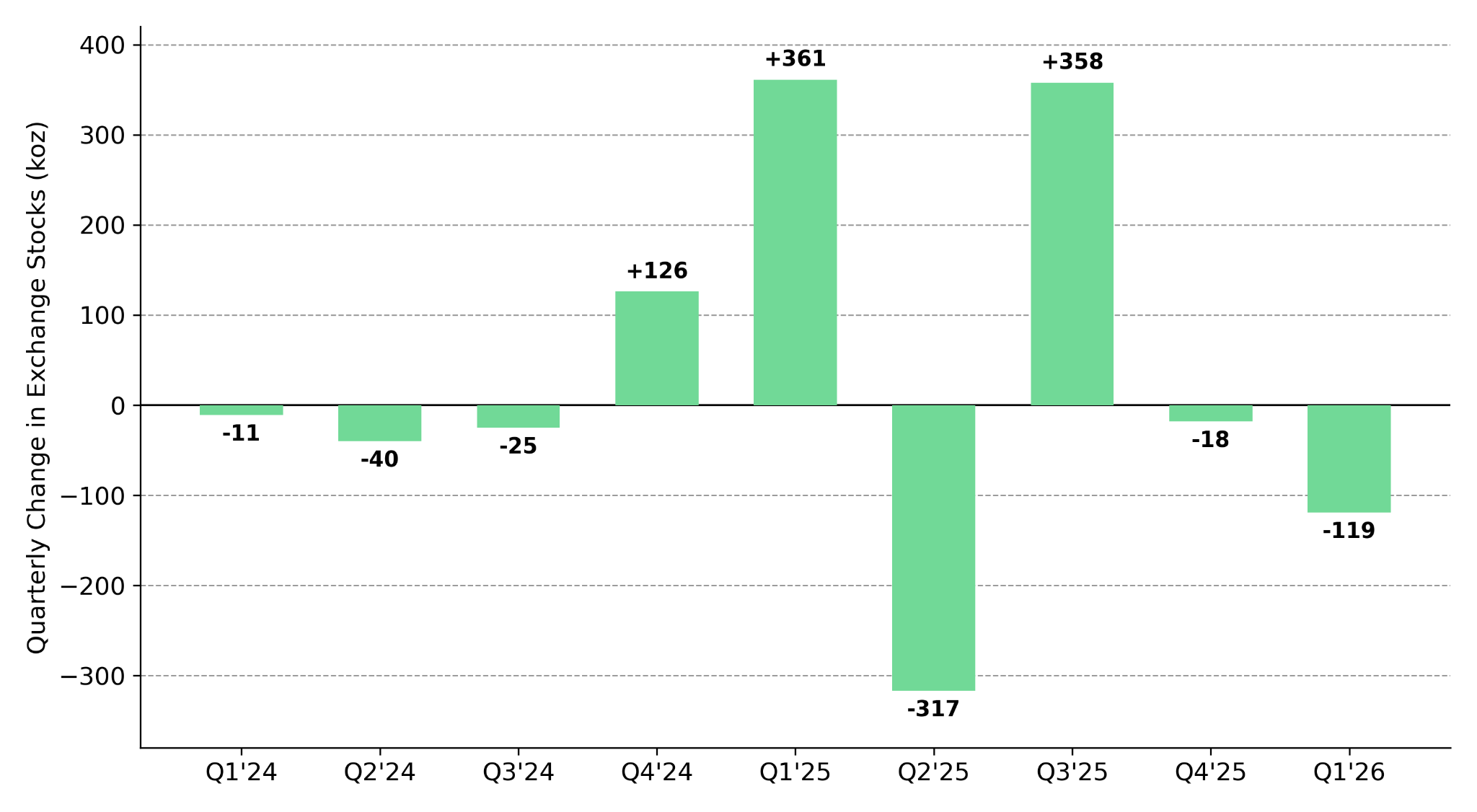

Market positioning ahead of the Section 232 review is already visible in weekly platinum exchange inventory data, with the US and London markets moving in opposite directions as buyers respond to different physical market conditions.

Trade Policy Risk & CME Platinum Inventories Signal Physical Positioning

Holding platinum in a CME-approved warehouse ties up working capital and forgoes lease income, costs that market participants typically incur only when they see sufficient value in holding physical inventory ahead of a potential policy change. Platinum inventories in CME-approved warehouses increased from 270,000 ounces at the start of 2025 to 624,000 ounces, a buildup that WPIC attributes to positioning ahead of potential tariffs by end users and speculators rather than stronger underlying demand. The same research notes that the US is a net importer of PGMs, consuming more metal than it produces domestically. The US supply deficit has also increased the cost of borrowing platinum. WPIC data shows the implied one-month platinum lease rate averaged 15% in the third quarter of 2025, up from 10% in the second quarter before additional credit spreads, making it more expensive to borrow metal than in the previous quarter.

China's VAT Policy & Exchange Destocking Drive Regional Market Divergence

Ex-China exchange inventories fell more than 40% from their year-start high to approximately 420,000 ounces by the end of June 2026, according to Shanghai Metals Market (SMM) weekly data. Part of that decline reflects Beijing's removal of China Platinum Company's value-added tax (VAT) exemption on November 1, 2025, which changed the economics of platinum jewelry fabrication independently of US trade policy. The opposing inventory trends show that regional platinum markets are responding to different policy drivers, increasing the potential for price differences between major trading hubs.

Supply Diversification & New PGM Demand Expand Long-Term Growth Opportunities

With more than 70% of platinum supply and a comparable share of palladium supply concentrated in two jurisdictions, projects in alternative producing regions become more relevant because geographic diversification does not depend on the Section 232 review resulting in new trade restrictions. Economic PGM deposits occur in only a few regions, primarily Southern Africa, parts of Australia, North America, and Brazil. That geological concentration limits how quickly global mine supply can diversify, even if trade policy encourages buyers to source metal from additional jurisdictions.

ValOre Metals is advancing the Pedra Branca project in Ceará State, Brazil, where a 2022 independent resource estimate defined 2.2 million combined ounces of platinum, palladium, and gold. The resource includes four zones exceeding 1 million ounces, with mineralization extending close to the surface in multiple areas. Because no economic study has been completed, the project does not yet have published AISC, capital expenditure, NPV, or IRR estimates. The company is targeting completion of a PEA by late 2026, with permitting and environmental review scheduled to begin in early 2027 if that study is completed. Until economic studies are available, the project's value rests on its jurisdiction and resource potential rather than demonstrated project economics.

Nick Smart, Chief Executive Officer of ValOre Metals, discusses geopolitical risks driving PGM supply diversification:

"When you've got a market for PGEs that is as concentrated as it is in platinum and palladium, so much production coming out of South Africa, Zimbabwe, and Russia, there's a geopolitical risk here. When you've got such a concentration within South Africa, Russia, and Zimbabwe, I think there's going to be a realization of that and a desire to diversify some of where those metals are coming from. We've seen that across a number of critical metals, and PGEs are critical metals."

Changing Demand & Higher PGM Prices Support Established Producers

Supply diversification does not reduce the importance of existing producers because new PGM projects require years to reach production. Valterra Platinum, demerged from Anglo American in 2025, reported a realized basket price of $1,852 per PGM ounce for the 2025 financial year, up 26% year over year. The company is targeting 2026 mined, concentrate, and refined production of 3.0 million to 3.4 million ounces, supported by capital expenditure of R17.0 billion to R18.0 billion and an AISC target of about $1,050 per 3E ounce sold.

Established producers are also expanding PGM demand beyond automotive catalysts, reducing reliance on a single end market. Sibanye-Stillwater and Valterra Platinum partnered with Johnson Matthey in February 2026 to develop new PGM applications in clean hydrogen technologies, emissions detection, and electronic materials, broadening demand beyond automotive catalysts as electric vehicle adoption continues. Valterra Platinum's chief executive said the collaboration is intended to accelerate innovation and develop new sources of demand for PGMs beyond their traditional end markets.

The push to expand PGM demand reflects measurable changes in end-market consumption rather than a precautionary strategy. China's electric vehicle exports rose 49% year over year in the first half of 2026, increasing the shift away from palladium-based catalytic converters. As internal combustion vehicle demand declines, producers are expanding industrial applications to diversify future sources of PGM demand.

Section 232 Policy & Critical Mineral Supply Chains Shape Future Market Positioning

Section 232 covers 50 critical minerals, placing PGMs within the same policy review as battery metals, rare earth elements, and other strategic inputs. The factors affecting PGM supply and demand illustrate how the review could influence sourcing decisions across multiple critical mineral markets. A separate Section 232 review covering semiconductors resulted in a 25% tariff on certain advanced computing chips effective January 15, 2026. The same action also directed Commerce to continue monitoring imports and report again by July 1, 2026, showing that Section 232 reviews can extend beyond the initial policy decision.

The platinum inventory buildup illustrates how policy uncertainty can influence physical commodity positioning before trade measures are implemented. Other minerals on the 50-mineral list with similarly concentrated supply chains, including cobalt and several rare earth elements, could experience similar inventory positioning ahead of future Section 232 reviews if production remains concentrated in a small number of countries.

The July 13 deadline is one milestone in a broader US critical minerals policy process rather than the conclusion of the Section 232 review. Commerce and USTR retain authority to monitor imports and recommend additional trade measures after the report is submitted. As long as the review process remains active, market participants may continue adjusting inventories and sourcing decisions in response to policy developments.

The Investment Thesis for Platinum Group Metals

- Trade-policy expectations are already influencing physical platinum positioning, with CME inventories rising from 270,000 ounces to 624,000 ounces before the Section 232 review is complete.

- Jurisdictional concentration is a measurable supply risk, with South Africa accounting for about 71% of global platinum mine supply and South Africa and Russia together supplying an estimated 70% to 80% of global palladium output.

- Established producers continue to benefit from higher realized basket prices, with stronger PGM prices supporting near-term revenue and operating margins despite uncertainty surrounding the Section 232 review.

- Exploration projects outside the traditional PGM supply base offer geographic diversification, but without a completed economic study they do not yet have published AISC, NPV, or other measures of project economics.

- Regional inventory trends show that platinum markets are responding to different policy drivers, with CME inventories rising ahead of the Section 232 review while ex-China exchange inventories declined following changes to China's VAT policy.

The Section 232 review has made a long-standing concentration risk observable through measurable changes in physical platinum positioning. CME-approved platinum inventories have increased to 624,000 ounces before any Section 232 trade measures have been implemented, providing a measurable indicator of market positioning ahead of the policy outcome. The direction of CME platinum inventories after July 13 will provide an observable indicator of whether market participants continue accumulating physical metal or begin reducing those positions. Exploration-stage projects outside the traditional supply base may offer geographic diversification, but without an economic study they do not yet have demonstrated operating costs, capital requirements, or project returns.

TL;DR

The US Section 232 review has already changed physical PGM market positioning before any trade measures have been implemented. Rising CME platinum inventories, concentrated mine supply in South Africa and Russia, and limited substitution options show that policy uncertainty is influencing physical metal positioning rather than just market sentiment. While established producers continue to benefit from stronger PGM prices, exploration projects outside traditional producing regions offer geographic diversification but remain pre-economic. The article argues that physical inventory movements provide a more reliable indicator of market expectations than policy speculation and that the implications of the review extend beyond PGMs to other critical minerals.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed