Fed Hawkishness & Platinum's Persistent Supply Deficit Widen a 297koz Valuation Disconnect

Platinum's supply deficit persists despite lower prices as Fed policy, a stronger US dollar, and Section 232 tariffs shape the investment outlook.

- Platinum has fallen to a seven-month low near $1,600 per ounce, roughly 45% below its January 2026 record, but the decline reflects a hawkish Fed and a stronger US dollar rather than any deterioration in supply or demand.

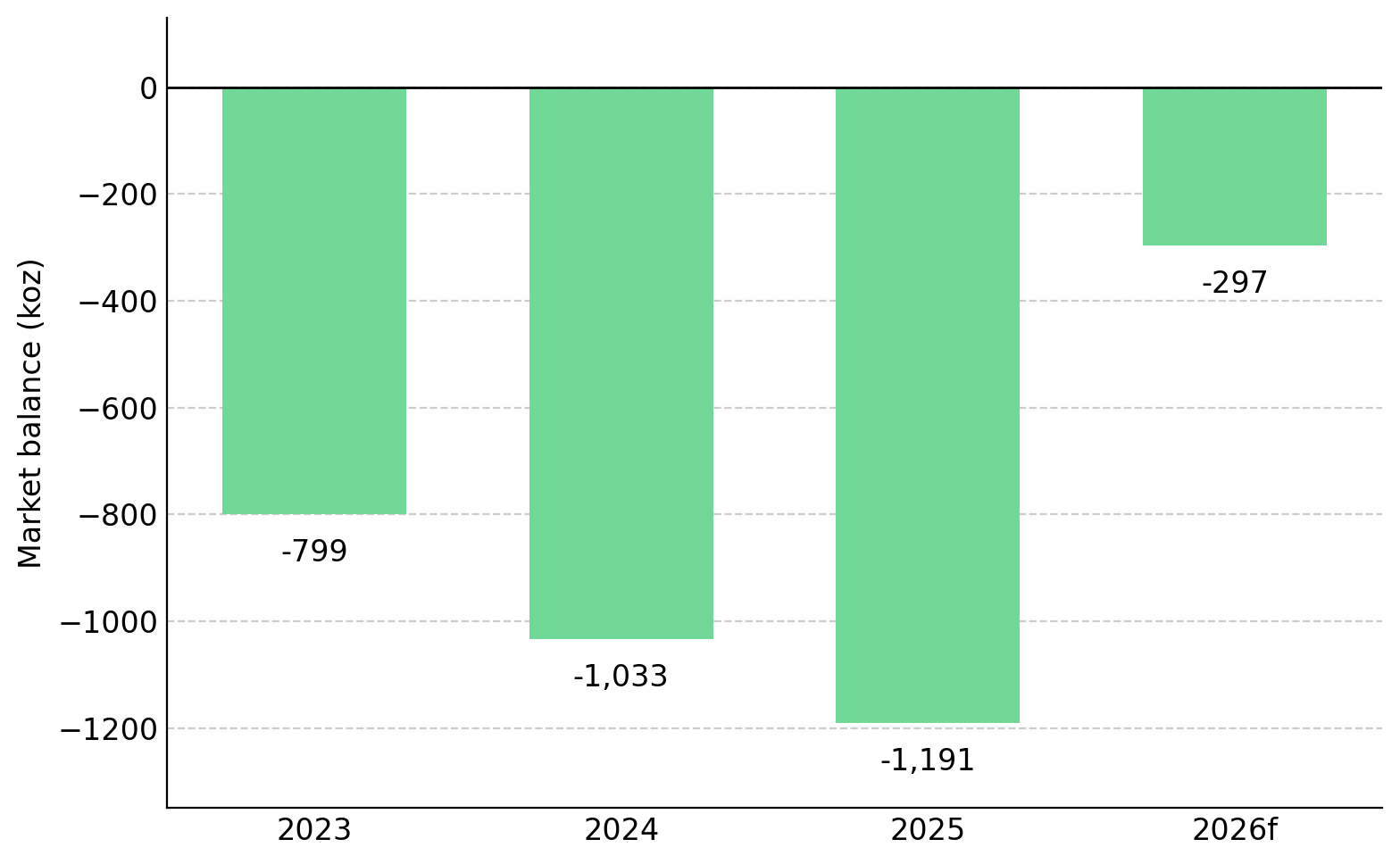

- The World Platinum Investment Council's Platinum Quarterly forecasts a fourth consecutive annual deficit of 297,000 ounces in 2026, with above-ground stocks projected to fall below three months of demand cover.

- A July 13, 2026 reporting deadline for the US Section 232 critical-minerals investigation could lead to tariffs or minimum import prices on platinum group metals, prompting traders to shift inventories into the US ahead of any policy changes.

- Platinum remains in supply deficit while palladium is moving into surplus as battery-electric vehicles reduce gasoline autocatalyst demand, making metal-specific exposure more important than treating platinum group metals as a single investment theme.

- The gap between a cyclical price decline and an ongoing supply deficit favors low-cost producers and companies with verified in-ground resources, although early-stage developers and explorers remain exposed to financing, permitting, and execution risk.

Fed Hawkishness & US Dollar Strength Drove Platinum Prices

Platinum enters the second half of 2026 trading near $1,600 per ounce, its lowest level since November 2025, down roughly 18% in four weeks and about 45% below the record of $2,920 per ounce set on January 26, 2026. Yet the physical market remains in deficit, with annual demand exceeding newly mined and recycled supply, leaving above-ground inventories in exchange warehouses, exchange-traded funds, and other stockpiles to meet the shortfall. That disconnect can persist only while above-ground inventories continue to offset the supply deficit, making inventory levels a key indicator of when prices may begin to reflect physical market conditions.

Platinum sold off because interest rates rose and the US dollar strengthened, not because supply increased or demand weakened. The key question is whether the gap between platinum prices and physical market fundamentals creates value in established producers and advanced development projects, or simply reflects the higher risks associated with early-stage exploration assets.

Hawkish Fed Policy & Dollar Strength Pressure Platinum Prices

Platinum's decline has been driven primarily by monetary policy and the strength of the US dollar rather than changes in the metal's underlying supply and demand. Two developments through June explain why platinum prices fell even as annual demand continued to exceed newly mined and recycled supply.

Hawkish Fed Signals Increased Pressure on Platinum Prices

At its June 17 meeting, the Fed held its benchmark rate at 3.5% to 3.75% for a fourth consecutive meeting, but the accompanying dot plot, which shows individual policymakers' rate projections, indicated that nine of eighteen officials projected at least one rate hike in 2026. The median year-end 2026 policy rate projection rose to 3.8% from 3.4% in March, signaling a higher expected interest-rate path. Fed Chair Kevin Warsh signaled a more hawkish policy stance by emphasizing price stability as consumer inflation remained near a three-year high following the energy-price shock linked to the Iran conflict.

Markets priced in roughly a 65% probability of a September rate hike. The higher expected rate path has a greater influence on platinum prices than monthly demand data because it raises the opportunity cost of holding a non-yielding asset.

Higher Real Rates Increased the Opportunity Cost of Holding Platinum

Platinum pays neither a coupon nor a dividend, making it a non-yielding asset. Its relative appeal falls as real interest rates, meaning nominal rates minus inflation, rise and interest-bearing assets such as cash and bonds offer higher returns. A stronger US dollar adds to that pressure because dollar-priced platinum becomes more expensive for buyers using other currencies.

The selloff extended across precious metals rather than being unique to platinum. Gold also recorded its worst quarter since the second quarter of 2013, reinforcing that higher interest-rate expectations weighed on the broader precious-metals market rather than platinum alone. The selloff reflects higher discount rates rather than weaker physical demand, an important distinction because changes in monetary policy can reverse more quickly than a sustained decline in demand.

Platinum Supply Deficit Persists Despite Lower Prices

Despite the recent price decline, platinum's underlying supply and demand balance remains largely unchanged from the conditions that supported record prices earlier in 2026. Mine supply remains broadly unchanged, while stronger industrial demand continues to offset weaker automotive and jewelry demand.Platinum Demand Is Shifting Across End Markets,

Platinum Supply Deficit Extends Into a Fourth Consecutive Year

The World Platinum Investment Council's latest Platinum Quarterly forecasts a 2026 supply deficit of 297,000 ounces (297koz), marking a fourth consecutive annual shortfall after the record 1.082 million-ounce deficit in 2025, the largest since the data series began in 2014. Above-ground stocks are projected to fall to roughly 1.747 million ounces (1,747koz) by year-end, leaving less than three months of demand cover. The reported first-quarter surplus of 268koz reflected 374koz of outflows from exchange-traded funds and exchange inventories rather than additional mine supply, making it an inventory-driven increase rather than an improvement in underlying production.

Nick Smart, Chief Executive Officer of ValOre Metals, an exploration-stage company advancing the Pedra Branca platinum group project in Brazil, describes the industry's supply inelasticity:

"Primary platinum mine production has declined over the past five years, even as the metal's price has doubled during the last year. That tells you something about how inelastic supply is and how difficult it is to bring new production to market."

Platinum Demand Is Shifting Across End Markets

According to the World Platinum Investment Council's latest Platinum Quarterly, industrial demand is projected to rise 9% to 2,238koz in 2026 as glass-capacity expansions resume. That increase offsets a 2% decline in automotive demand to 2,959koz, a 12% fall in jewelry demand, and is complemented by a 27% increase in bar and coin investment to 718koz. Demand from autocatalysts, where platinum is used in catalytic converters, remains supported by the growing share of hybrid vehicles, which continue to require the metal.

Palladium is moving into surplus as battery-electric vehicles reduce demand for gasoline autocatalysts, highlighting the need to evaluate platinum group metals individually rather than as a single commodity group. Longer-term demand for platinum is also supported by hydrogen technologies, including fuel cells and electrolyzers, and by growing platinum group metal use in hardware supporting artificial intelligence infrastructure. Demand is shifting across end markets rather than declining overall, allowing the platinum market to remain in supply deficit.

Section 232 Trade Policy Reshapes Platinum Supply Chains

The next major catalyst for platinum prices is US trade policy rather than a change in physical supply and demand. The US Department of Commerce's Section 232 investigation, a national-security review of critical-mineral imports, covers platinum, palladium, rhodium, iridium, and ruthenium. The Department is due to submit its report by July 13, 2026, after which the administration could impose tariffs or minimum import prices on these metals.

The prospect of US import tariffs has already prompted traders to move platinum into US warehouses. CME platinum inventories increased from about 270koz at the start of 2025 to roughly 624koz. If tariffs are imposed, much of that inventory could remain in the US, tightening supply in other markets. The same concentration of platinum group metal supply that creates supply-chain risk has also made the sector a focus of US trade policy.

US Trade Policy Raises the Value of Platinum Projects Outside Traditional Supply Hubs

The concentration of platinum group metal supply outside the Americas increases the strategic value of projects in alternative jurisdictions, providing context for exploration companies such as ValOre Metals. The near-surface ore body could support lower-cost open-pit mining instead of the deep underground operations common in South Africa, while the weathered upper zone is being evaluated for leaching rather than conventional sulfide flotation. A maiden Preliminary Economic Assessment, the first study to estimate project economics, is targeted for year-end 2026.

The macro rationale for a Brazilian platinum group asset rests on diversification away from concentrated supply, and Smart argues that critical-minerals policy will increasingly reward that geography:

"When you've got such a concentration within South Africa and Russia and Zimbabwe, there's going to be a realization of that and a desire to diversify some of where those metals are coming from. We've seen that in the world across a number of critical metals, and PGEs are critical metals."

Valuation Gap & the Catalysts That Could Close or Widen It

Enterprise value per ounce (EV/oz) divides a company's enterprise value by its resource ounces, providing a way to compare how the market values in-ground metal across companies at different stages of development. As of June 1, 2026, ValOre's market capitalization was approximately CAD $26 million, compared with CAD $126 million to CAD $440 million for selected peer developers cited in February, despite reporting a broadly similar resource size. Management attributes the valuation gap to the absence of a published economic study. The maiden Preliminary Economic Assessment, targeted for year-end 2026, is intended to provide the initial economic data needed to compare the project with more advanced peers.

The EV/oz gap therefore reflects project maturity and the absence of an economic study rather than market mispricing alone. Valuation discounts can persist for years without a clear development milestone. ValOre shares traded near CAD $0.09, resulting in limited liquidity, wider bid-ask spreads, and greater price volatility.

The investment case should be assessed against developments that could weaken it as well as those that could strengthen it. A disappointing resource update, a weak or delayed economic study, a dilutive equity financing, or a benign Section 232 outcome that releases US inventories back into global markets would each weaken the investment case. Capital invested in early-stage resource companies is at significant risk of loss.

Macro Catalysts Will Determine Platinum's Next Move

Platinum prices in the second half of 2026 will depend primarily on a small number of identifiable macroeconomic drivers. These include the next US employment report, the September Fed decision, the direction of the US dollar, and whether the Strait of Hormuz reopens. The World Platinum Investment Council assumes the Strait will reopen during the third quarter, a development that could reduce energy prices, ease inflation, and lessen pressure for the Fed to maintain a restrictive policy stance. Each of these affects platinum primarily through discount rates rather than changes in physical supply and demand.

The key takeaway is that platinum supply cannot respond quickly to changes in price because new mine capacity takes years to develop. Four consecutive annual deficits, despite prices first doubling and then correcting sharply, show that inventory drawdowns rather than new mine supply continue to balance the market. Because mine supply responds slowly, macro-driven price declines can persist even while physical inventories continue to fall. Once macroeconomic pressures ease, prices are more likely to reflect the underlying supply deficit if market conditions remain unchanged.

The Investment Thesis for Platinum Group Metals

- The 2026 supply deficit remains intact even as platinum prices have fallen, indicating that higher expected interest rates and a stronger US dollar are having a greater influence on prices than physical supply and demand. If those macro pressures ease while the deficit persists, prices could recover before new mine supply responds.

- Supply remains inelastic, with flat mine output and life extensions at existing mines limiting supply growth even as prices swing.

- Metal selection matters because platinum remains in supply deficit while palladium is moving into surplus as battery-electric vehicles reduce gasoline autocatalyst demand.

- Section 232 trade policy increases the value of assets in jurisdictions outside the concentrated Southern African and Russian supply base, making project location and verified in-ground resources more important.

- The valuation gap favors low-cost producers and developers with clear development milestones, though early-stage projects remain exposed to financing, permitting, and execution risk.

- Fees, liquidity, and the risk of capital loss remain important considerations, particularly for thinly traded junior companies where wider bid-ask spreads increase price volatility.

The Fed and the stronger US dollar drove platinum prices lower, but the supply deficit remains intact and could regain influence if the Strait of Hormuz reopens and inflation pressures ease. The July 13 Section 232 decision and the next US jobs report are the key near-term catalysts because both could influence interest-rate expectations or platinum supply. The current valuation gap depends on macro conditions rather than weaker physical supply and demand, but early-stage projects remain exposed to financing, permitting, and execution risk.

TL;DR

Platinum prices have fallen sharply in 2026 because higher US interest-rate expectations and a stronger US dollar increased the opportunity cost of holding non-yielding assets rather than because physical market fundamentals weakened. The market remains in a fourth consecutive annual supply deficit, with above-ground inventories continuing to decline as demand exceeds mine and recycled supply. The upcoming US Section 232 critical minerals decision could reshape global platinum trade flows, while easing inflation and Fed policy could allow the underlying supply deficit to support prices again. Investors should focus on low-cost producers and advanced development projects with defined milestones while recognizing that early-stage explorers remain exposed to financing, permitting, and execution risks.

FAQs (AI-Generated)

Analyst's Notes

Subscribe to Our Channel

Stay Informed