Copper at Investment Crossroads for Global Electrification, Renewable Energy, and AI Revolution

Copper demand surges with electrification and AI growth while supply constraints tighten; mining companies expanding exploration as prices remain historically undervalued.

Copper stands at a pivotal crossroads in the global economy, positioned to benefit from multiple converging megatrends that are reshaping the 21st century. As highlighted in recent industry analysis, despite relatively stable prices in recent months, fundamental factors suggest copper may be positioned for significant growth in the coming years. The metal has maintained a steady upward trajectory over the past 25 years, yet when measured against gold as a proxy for "real money," copper remains at historically low valuations, presenting a potential opportunity for investors with a long-term horizon.

With industry experts noting that despite relatively stable prices, fundamental factors suggest copper may be positioned for significant growth, the metal's central role in the ongoing global energy transition, digitalization, and industrial development puts it in a unique position among commodity investments.

This comprehensive analysis examines the supply and demand dynamics, major projects in development, and the investment case for copper as we navigate a world increasingly driven by electrification and renewable energy.

Megatrends Driving Copper Demand

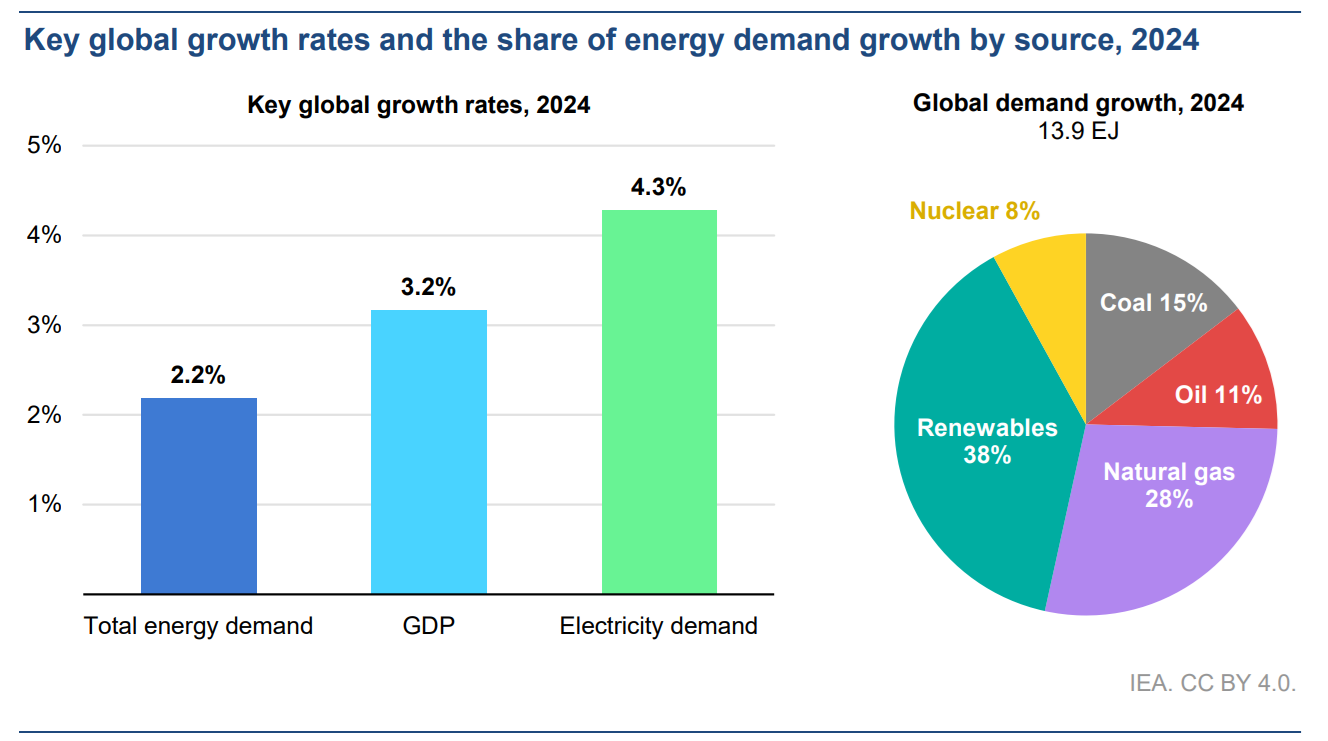

The International Energy Agency's Global Energy Review published in early 2025 reveals compelling data supporting copper's growth trajectory. Global energy demand grew by 2.2% in 2024, faster than the average rate over the past decade. More significantly, electricity demand surged by 4.3%, substantially outpacing the 3.2% growth in global GDP. This exceptional growth was driven by record temperatures, accelerating electrification, and digitalization.

This electricity demand growth directly translates to increased copper consumption. Unlike other commodities, copper's relationship with electrification is practically inevitable - every additional kilowatt-hour generated, transmitted, and consumed requires copper infrastructure. Industry expert Merlin Marr-Johnson notes,

"The more that you go down the intermittent, disperse energy collection processes like solar and wind, the more transmission lines you have, the more electrical...the more copper you're going to need."

The data shows an unprecedented acceleration in electricity consumption, particularly in buildings. Marr-Johnson points to a big spike in electricity demand in 2024 with buildings (accommodating AI infrastructure and air conditioning) showing dramatic growth, adding approximately 440 terawatt hours of electricity consumption. This represents a structural change in energy consumption patterns likely to persist long-term.

Merlin Marr-Johnson, CEO of Fitzroy Minerals

Chile's Production Plateau

While demand factors present a compelling case, supply dynamics strengthen the investment thesis. Chile, the world's largest copper-producing country, faces significant production limitations. According to projections from Cochilco (the Chilean Copper Commission), Chilean copper production is expected to peak at 6 million tons in the next three years before declining to approximately 5.5 million tons over the subsequent seven years. Essentially, production from the world's copper leader will remain flat over the next decade.

This plateau comes despite substantial investment commitments. BHP alone has announced plans for between $11 to 15 billion worth of investment over the next decade, mostly concentrated on Escandida, one of the world's largest copper mines. Overall, projected capital expenditure for Chilean mining has reached $83 billion, with approximately 70-75% directed toward copper.

Hot Chili's Costa Fuego copper-gold project and Huasco Water project, located along the coastal range of Chile, have both been registered before the Office for Sustainable Project Management by the Chilean Ministry of Economy. The registration marks a significant step forward, confirming that Hot Chili's projects meet the Chilean government's objective criteria to acquire priority status.

Marimaca Copper recently announced results from the re-interpretation of data in its Pampa Medina Project Area which incorporates the Pampa Medina and Madrugador deposits and the newly identified Pampa West oxide zone. The company believes Pampa Medina may be the central part of a larger manto system, which genetically links the Madrugador, Pampa Medina, Sierra Valenzuela (Antofagasta) and Pampa Norte deposits.

Additionally, projects in countries like Ecuador, the Philippines, and Colombia often face specific challenges related to environmental regulations, community relations, and political stability. Even in mining-friendly jurisdictions like Chile, water access and environmental concerns have become increasingly important factors.

The fact that such massive investments will merely maintain rather than significantly expand production highlights the growing challenges in copper mining - lower grades, deeper deposits, and more complex metallurgy - all factors that support higher long-term copper prices.

Geopolitical Shifts: China's Strategic Positioning

China's strategic approach to securing copper resources represents another critical factor for investors to consider. According to analysis from AidData published in January 2025, Beijing has become a major source of financing for projects around the globe that involve specific minerals including copper, which are essential for the energy transition.

These investments are not evenly distributed and reflect strategic priorities. As of 2021, 46% of China's mineral investment has gone into copper projects, with particular focus on Peru and the Democratic Republic of Congo (DRC). The results of this strategy are already evident in trade flows: Reuters data shows the DRC has now overtaken Chile as China's largest refined copper supplier, marking a significant "switcheroo" in global copper trade patterns.

This strategic positioning by China may create additional supply constraints for Western markets and companies, potentially supporting higher prices in non-Chinese markets.

The EV Revolution Continues

Despite some slowdowns in certain markets, the electric vehicle sector continues to drive significant copper demand globally. China maintains strong growth in both battery and plug-in hybrid vehicles, Europe remains steady at over 3 million units sold, while the United States has reached over 1.6 million units and the rest of the world accounts for approximately 1.4 million units.

This trend is particularly important for copper investors since EVs use significantly more copper than conventional internal combustion engine vehicles. As battery technology improves and range anxiety diminishes, EV adoption is expected to accelerate, creating sustained demand for copper in automotive manufacturing.

Junior Mining Opportunities and Activity

Across the junior mining space, there is significant activity in copper exploration and development. Pan Global Resources started drilling at its Bravo target in the Escacena copper-tin project in southern Spain. The company noted the geophysics at Bravo shows many of the signatures associated with the company's nearby La Romana copper-tin-silver discovery. Bravo has become a high-priority target amongst several previously untested targets in this highly prospective area for significant volcanogenic massive sulphide ('VMS') associated mineralization.

Similarly, Pacific Empire Minerals is advancing exploration at its Trident Copper-Gold Property in British Columbia, Canada. According to the news release for its 2025 exploration plans and permitting, the company intends to complete an initial 3–5-hole diamond drilling program at Trident. The initial diamond drill program at Trident is focused on the primary target area where over 50 years' worth of exploration suggests that the area immediately north of historical drilling is the most prospective.

Coda Minerals, South Australian copper-cobalt-silver explorer with a flagship project called Elizabeth Creek has completed a scoping study showing a pre-tax NPV of $1.2 billion ($802 million post-tax) and is moving into pre-feasibility study (PFS) phase. Elizabeth Creek is estimated to contain 800,000 tons of copper, 30,000 tons of cobalt, and 28 million ounces of silver in JORC resources. With $4.5 million cash, Coda is being capital-efficient, focusing on advancements that improve economics rather than expensive drilling, while waiting for improved market conditions for development-stage mining companies.

Chris Stevens, CEO of Coda Minerals

Successful junior companies typically demonstrate three key characteristics: growth (expanding resources), momentum (funded drilling programs and regular news flow), and value (reasonable valuation relative to resource potential).

For investors seeking higher-risk but potentially higher-reward exposure to copper, junior mining companies offer interesting possibilities. Several more companies are showing promising results, including:

- ATEX Resources: Growing from approximately $200-250 million to $568 million market cap over 15 months with impressive drill results.

- NGeX Minerals: With a $2.5 billion market cap and exceptional copper grades.

- Dundee Precious Metals: A $3 billion producer with impressive results from their Serbian asset.

Price Volatility & Market Dynamics

While long-term fundamentals appear strong, copper remains subject to short-term volatility driven by macroeconomic factors, inventory levels, and speculative positioning. Industry analysts note that LME (London Metal Exchange) and Shanghai inventory levels influence price movements, with declining warehouse stocks typically associated with price increases.

Interestingly, the International Copper Study Group actually forecasts potential surpluses in the coming years as refined production outpaces demand growth, despite global copper mine production only growing at 2.3-2.5%. This highlights the complex and sometimes contradictory nature of copper market forecasts.

The Long-Term Investment Case

The investment case for copper rests on a confluence of powerful long-term trends and supply constraints. The electrification of transportation, expansion of renewable energy, growth in artificial intelligence and data centers, and increasing electricity consumption in developing economies all point to sustained copper demand growth.

Meanwhile, production challenges, declining ore grades, and increasingly complex development environments suggest supply will struggle to keep pace. China's strategic positioning to secure copper resources adds another dimension to the supply equation for Western markets.

Industry assessment of copper pricing in "real money" terms (relative to gold) suggests copper may be undervalued relative to its fundamental importance in the global economy. For investors with appropriate risk tolerance and time horizons, copper exposure - whether through major producers, development companies, or carefully selected explorers - merits serious consideration as part of a forward-looking investment portfolio.

As global economies navigate the complex transition toward more electrified, digitalized futures, copper's role as the fundamental enabling metal for these transformations positions it uniquely among commodity investments. The metal that powered the industrial revolution may prove equally essential to the digital and renewable energy revolutions of the 21st century.

The Investment Thesis for Copper

- Long-Term Demand Growth: Invest in copper to benefit from structural megatrends in electrification, renewable energy, AI infrastructure, and electric vehicles – all sectors requiring substantial copper inputs.

- Supply Constraints: Position portfolios to benefit from the growing gap between increasing global demand and restricted supply growth, particularly as existing mines encounter lower grades and production plateaus.

- Portfolio Diversification: Add copper exposure as a hedge against inflation and currency debasement, with copper historically serving as an industrial "hard asset" that tends to perform well in inflationary environments.

- Strategic Positioning: Consider geographical diversification across copper investments to mitigate country-specific risks, focusing on tier-one jurisdictions with clear permitting pathways.

- Risk Management: Blend exposure across the risk spectrum – from established producers (lower risk, immediate cash flow) to developers (medium risk, near-term catalysts) to explorers (high risk, maximum upside potential) based on individual risk tolerance.

- Timing Considerations: Consider dollar-cost averaging into copper positions rather than attempting to time market cycles, as the structural case remains strong despite potential short-term volatility.

Copper's fundamental position at the intersection of multiple global megatrends makes it a compelling consideration for forward-thinking investors. The metal's essential role in electrification, renewable energy, and digital infrastructure, combined with significant supply constraints and declining ore grades, creates a structural environment supportive of higher prices over the long term. While short-term volatility should be expected due to macroeconomic factors and market sentiment, the underlying supply-demand dynamics strongly favor copper over a multi-year time horizon.

Investors have multiple pathways to gain exposure – from major producers to junior explorers, depending on risk tolerance and investment timeline. Companies with quality assets in favorable jurisdictions, strong management teams, and clear development pathways deserve particular attention. As the global economy continues its transition toward electrification and digitalization, copper's role as a critical enabling metal positions it uniquely among commodity investments for the decades ahead.

Analyst's Notes

Subscribe to Our Channel

Stay Informed